Why Your Repaired Car Is Worth Less Than You Think

Here’s a hard truth that often catches car owners off guard: a perfectly repaired car has an invisible mark that follows it forever. Imagine buying a brand-new designer handbag. If it gets a deep scratch and is professionally restored, it might look perfect to the naked eye. But once a potential buyer knows about the repair, they will never pay the original price. This exact principle applies to your vehicle after a collision.

This permanent loss in resale or trade-in value is called inherent diminished value. A diminished value report is the official document that calculates this financial loss, giving you the solid proof needed to claim the money you are owed. Without this report, you are essentially forced to accept a significant financial loss for an accident you didn’t cause.

The Problem of a Permanent Record

The main issue is that accident records don't just go away. Vehicle history reporting services create a permanent file of any reported incident. For instance, take a look at the homepage of a major vehicle history service, CARFAX:

This image shows just how easy it is for anyone to access a vehicle's history. Dealers and private buyers now routinely check a car's past before even considering an offer. An accident report, no matter how minor, instantly puts your vehicle at a disadvantage compared to similar cars with clean records. This information is widely available because over 95% of U.S. auto insurers report claims data to centralized databases. This ensures that accident histories directly affect resale prices.

Why Buyers and Dealers Pay Less

This permanent record creates a stigma that leads directly to you losing money. Car dealers and knowledgeable private buyers will automatically offer less for a vehicle with an accident history for a few key reasons:

- Risk Aversion: Buyers worry about possible hidden problems or the long-term reliability of the repairs, even if they were done at a top-notch body shop.

- Reduced Marketability: A car with an accident on its record takes longer to sell. Dealers have to account for the extra time and marketing effort it will take to move the car off their lot.

- Negotiating Power: The accident report gives the buyer a huge advantage. They know the car is less desirable and will use that information to drive the price down.

In the end, this stigma means your repaired car is worth much less on the open market. This isn't about the quality of the repair work; it's a direct result of its documented accident history. Understanding this reality is the first step in figuring out if a diminished value claim is the right financial move for you.

Understanding The Three Types Of Vehicle Value Loss

Not all value loss is created equal. Think of it as three distinct ways an accident can damage your car's resale price, each with its own cause and impact. To build a successful diminished value claim, you first need to understand which type of loss—or combination of losses—applies to your vehicle.

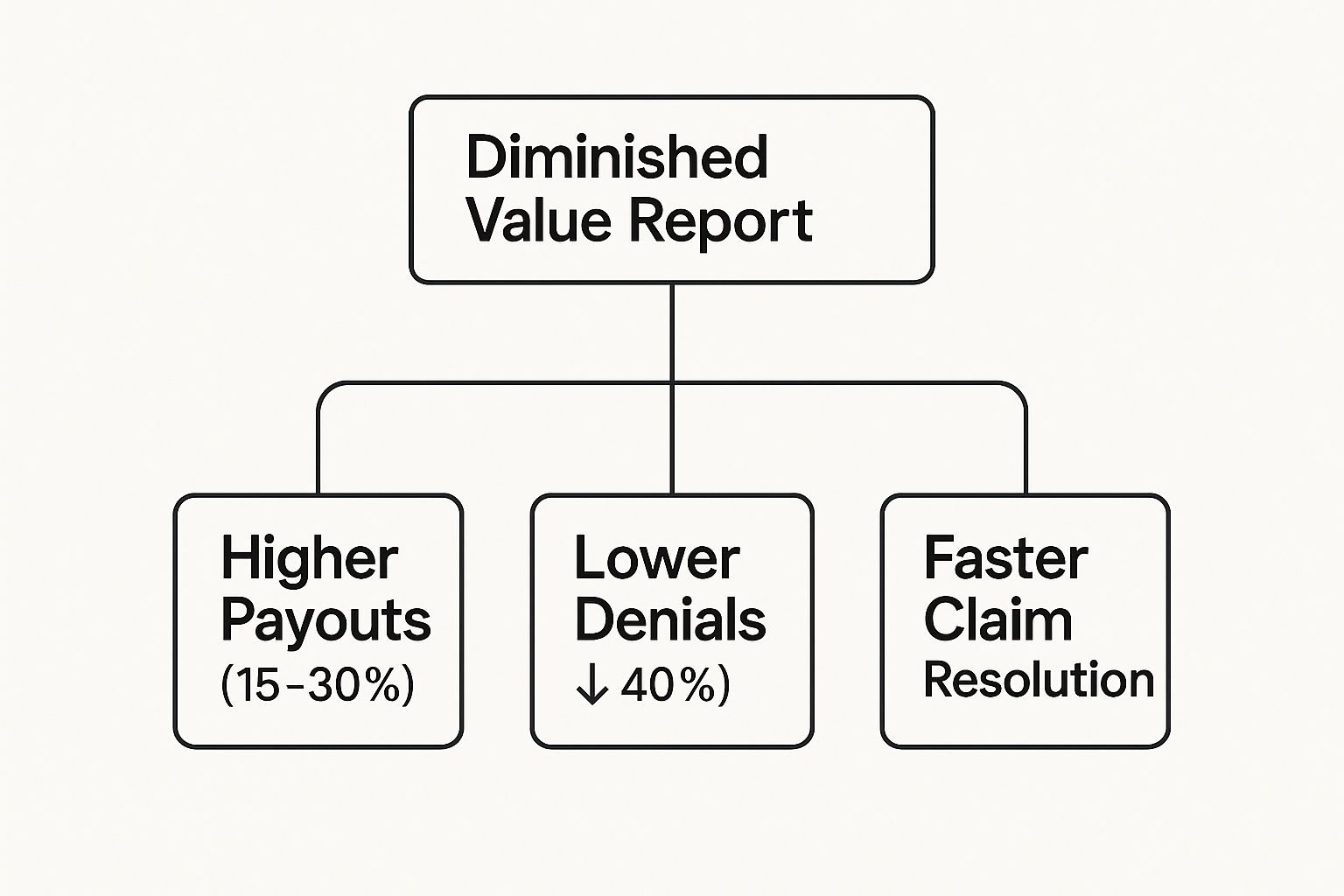

A professional diminished value report is your most important tool for proving this loss to an insurance company. The data shows just how much of a difference a documented report can make.

As you can see, investing in a professional report directly correlates with better outcomes, from higher settlement offers to quicker claim resolutions.

The Breakdown of Value Loss

There are three recognized categories of diminished value: repair-related, parts-related, and inherent diminished value. While all three can reduce your car's worth, inherent diminished value is typically the most significant and the one that insurance companies are most reluctant to pay.

The table below breaks down these three types to help you identify what might apply to your situation.

Types of Diminished Value Comparison

Comparison of the three types of diminished value, their causes, typical payout percentages, and difficulty of proving claims

| Type | Cause | Typical Payout Range | Proof Difficulty | Insurance Response |

|---|---|---|---|---|

| Repair-Related Diminished Value | Poor quality repairs or sloppy workmanship. | 1-10% of vehicle value | Low to Medium | Often accepted if poor work is obvious (e.g., mismatched paint). |

| Parts-Related Diminished Value | Use of aftermarket or non-OEM parts instead of factory originals. | 1-5% of vehicle value | Medium | Accepted if policy guarantees OEM parts; otherwise, often denied. |

| Inherent Diminished Value | The simple fact that the vehicle has a permanent accident history. | 10-25%+ of vehicle value | High | Most commonly disputed; requires strong market evidence to prove. |

This comparison highlights that while repair and parts-related issues are more tangible and easier to prove, inherent diminished value represents the largest financial loss and requires the most robust documentation to successfully claim.

Inherent Diminished Value: The Biggest Factor

Even if your car is repaired flawlessly with original factory parts, its value has still dropped. This is inherent diminished value, and it's the most common and financially damaging type. It exists simply because the vehicle is now branded with an accident history, making it less desirable to potential buyers.

Imagine two identical, late-model Audis for sale. One has a clean history, and the other was in a moderate collision but has been perfectly repaired. A savvy buyer will always choose the one with no accident history or will demand a significant discount for the one that does. That "discount" is the inherent diminished value you've suffered. This is especially true for newer, luxury, or specialty vehicles where a clean history is paramount. You can explore more detailed scenarios in our collection of auto appraisal insights.

Because it’s based on market perception rather than a physical flaw like a bad paint job, insurance companies often push back hard on inherent diminished value claims. This is why a well-researched, professional appraisal is not just helpful—it's essential.

How Diminished Value Gets Calculated In The Real World

Forget those simple online calculators that spit out instant, often unreliable, numbers. Figuring out your vehicle’s true diminished value is a lot like appraising a house. Just as a home's worth depends on its location, condition, and recent sales in the area, your car's lost value is a mix of several real-world factors. While formulas provide a framework, they are only the starting point for a professional appraiser who digs much deeper.

A credible diminished value report doesn’t come from a one-size-fits-all equation. Instead, certified appraisers follow a detailed process that weighs the unique circumstances of your vehicle and its accident history. This methodical approach produces a final figure that can stand up to the questions of insurance adjusters, who are trained to challenge generic estimates.

The Core Calculation Method

The most common starting point in the industry is often referred to as the 17c formula, named after a notable Georgia court case. It's important to see this as a basic framework, not the final answer. Professional appraisers use it to establish a baseline before applying their expertise to adjust the value based on specific details.

The process generally follows these steps:

- Establish Pre-Accident Value: First, the appraiser determines your car's fair market value before the crash. They use professional resources like NADAguides, pricing guides, and local market data to find this number.

- Apply a Damage Cap: A maximum loss percentage is applied to the pre-accident value. This is typically 10%, but it serves only as a base cap.

- Factor in Damage Severity: The appraiser then assesses how serious the damage was, applying a multiplier from 0.00 (minor cosmetic issues) to 1.00 (severe structural damage).

- Adjust for Mileage: Finally, a mileage modifier is used to account for the vehicle's usage, reducing the value for cars with more miles on the odometer.

This initial calculation gives a preliminary number, but the most important work comes next, where an appraiser's real-world market knowledge makes all the difference.

Beyond the Basic Formula: Real-World Factors

The biggest adjustments to the final value come from factors that online tools simply can't account for. Market data shows that diminished value settlements often land between 10% and 25% of a car’s pre-accident value. The specifics of the car and the accident determine where a claim falls in this wide range. For example, a 2024 Hyundai Tucson SEL valued at around $27,000 before an accident might have a strong claim after a $2,008 repair for minor structural damage. You can find more information on car value estimates at resources like KBB.com.

To help clarify how these variables work, the table below outlines the key factors a professional appraiser analyzes to build your diminished value report.

| Factor | Impact on Value | Typical Range | Notes |

|---|---|---|---|

| Vehicle Type & Prestige | High | 15%-25% Loss | Luxury, exotic, and newer electric vehicles suffer a greater percentage of loss due to buyer expectations for a clean history. |

| Accident Severity & Stigma | High | 10%-25% Loss | Any accident involving structural or frame damage creates significant stigma, severely impacting resale value. |

| Quality of Repairs | Medium to High | 5%-15% Loss | Even with high-quality OEM parts, signs of repair (e.g., mismatched paint, panel gaps) will lower the value. |

| Market Demand | Medium | +/- 5% Adjustment | A popular, in-demand model may experience slightly less diminished value compared to a less common vehicle. |

| Prior Accident History | Medium | 5%-10% Reduction | A vehicle with a previous accident history will have a lower starting value, thus a lower diminished value claim for a new incident. |

| Location & Market | Low to Medium | +/- 3% Adjustment | Regional market conditions and local buyer perceptions can slightly influence demand and final resale value. |

The table highlights that the type of car and the severity of the damage are the most influential factors. A luxury vehicle's value is much more sensitive to its history than an older economy car's.

This is why a $5,000 repair on a three-year-old luxury SUV could easily lead to a $6,000 diminished value claim, while the same repair cost on a ten-year-old sedan might only support a $500 claim. A skilled appraiser connects all these dots, creating a logical and evidence-based case to justify the final figure you present to the insurance company.

Getting Your Report: Professional Appraisers Vs DIY Methods

When you need to prove your car has lost value after an accident, you’ll face a key decision: should you hire a professional appraiser or build the case yourself? Think of it like preparing your taxes. A simple financial situation might be fine for DIY software. But if you have complex investments or business expenses, you’d hire a Certified Public Accountant (CPA) who can navigate the rules and defend their calculations. The same idea applies to creating a strong diminished value report.

The Professional Appraiser Route

Hiring a certified professional gives your claim instant credibility. Insurance adjusters are used to seeing weak, unsupported demands. A report from a recognized expert makes them sit up and pay attention. These specialists usually charge between $300 and $600, an upfront investment with no guarantee of a specific payout. However, the right appraiser can be well worth the cost.

It's important to know that not all credentials are the same. You need an appraiser with specific automotive knowledge, not just a general license. Look for certifications that are respected in the auto industry, like those from the American Society of Appraisers (ASA) or insights from the National Automobile Dealers Association (NADA). An appraiser's expertise in vehicle structures, repair methods, and local market conditions is what makes their report so persuasive.

Take a look at the homepage for ASE, a top certification organization for auto technicians. It shows what kind of specialized knowledge is crucial in this field.

The focus on "Automotive Service Excellence" shows why deep industry knowledge is essential. An appraiser with ASE certifications understands the details of collision repair and how it affects a car’s long-term safety and value. This expertise adds considerable weight to their assessment.

Before you commit to an appraiser, do your homework:

- Ask to see a sample report to understand their process.

- Check their credentials and look for client testimonials or past successes.

- Confirm they have experience with your car's make and model, especially for luxury, classic, or unique vehicles.

The Do-It-Yourself (DIY) Method

If your budget is tight or the claim amount is relatively small, the DIY path can work if you are thorough. Your job is to act like a professional by collecting objective, market-based proof. This isn’t about just saying you feel your car is worth less; it’s about demonstrating it with hard data.

Your DIY diminished value report should contain:

- Comparable Vehicle Research: Find at least five to ten recent online listings for cars that are identical to yours—same year, make, model, trim, and similar mileage—in your local area. Use websites like Autotrader, Cars.com, and local dealership inventories.

- Pre-Accident Value: Establish your car's value before the crash using tools like NADAguides or Kelley Blue Book. Back this up with the comparable sales data you found.

- Gather Quotes from Dealers: Call several used car managers at nearby dealerships. Ask them for two trade-in estimates for your vehicle: one assuming a clean history and another with its known accident record. Keep detailed notes of these conversations.

- Organize Your Evidence: Put all your research together in a professional document. Include screenshots of ads, emails with dealers, repair receipts, and photos of your car before and after the accident.

Whether you hire a pro or do it yourself, the strength of your claim comes down to the quality of your proof. If you're not sure which direction to go, getting an initial expert opinion can be a helpful first step. You can even find specialists who offer a free diminished value assessment to help you make an informed decision.

Navigating Insurance Companies With Your Documentation

With your professional diminished value report in hand, you're prepared to contact the at-fault driver's insurance company. Approaching this process is like playing a strategic game. The insurance adjuster you'll speak with handles claims like this every day. They are experienced in following scripts designed to pay out as little as possible. Your documentation is what levels the playing field, moving your position from defense to offense.

Submitting Your Claim and Handling the First Response

The first step is to write and send a formal demand letter. Keep it professional and to the point, and be sure to include your complete documentation package. This package is your evidence and should contain:

- The full, independent diminished value report.

- A copy of the final auto body repair bill.

- Photos showing the vehicle's damage before it was repaired.

- The official police report from the accident.

After you submit everything, expect the insurance company's opening move: a very low offer or an outright denial of your claim. This is normal, so don't get discouraged. It's a standard tactic. Adjusters have set limits on what they can approve for a settlement, and their initial offers are almost always on the lowest end of that scale. They are testing you to see if you’ll accept a small fraction of your claim's worth or just give up.

Turning a Denial Into a Negotiation

The best way to counter an initial denial is with a calm, evidence-based response, not an emotional one. Your objective is to demonstrate that your claim is backed by solid proof and that you're aware of your rights. This is where your professional report truly shines, providing the logical, third-party validation that adjusters must consider.

When an insurer makes a low offer, it's typically calculated using an internal formula, like the "17c method," which is known for producing low-end figures. For example, a 17c formula might calculate a payout between $650 and $715, but it’s common for an insurer to offer even less. In one case, Liberty Mutual offered just $400, which was only 1.5% of the vehicle’s pre-accident value. You can learn more about how these figures often miss the mark by reading about diminished value estimations on KBB.com.

Negotiation Tactics That Work

Focus your negotiation on the facts laid out in your appraisal. Point to specific market data and the appraiser's reasoning for the calculated loss in value. If the adjuster tries to dismiss your report, politely ask them to provide a detailed, written breakdown explaining how they calculated their offer. This shifts the burden of proof back to them.

Here are a few effective strategies to use:

- Stay Calm and Professional: Keep all communication business-like and maintain a written record of your conversations.

- Ask for Justification in Writing: Make the adjuster defend their low offer with data, not just vague policy statements.

- Escalate if Necessary: If you hit a wall, politely request to speak with a claims supervisor. Supervisors generally have more authority to approve higher settlements and resolve disputes.

Remember, persistence supported by solid evidence is your strongest tool. The process may involve a few back-and-forths, but having a professionally prepared diminished value report gives you the credibility needed to argue your case effectively. For a deeper look at the first steps to take, review our guide on what to do after a car accident.

How Technology Is Changing Diminished Value Claims

The way diminished value is calculated is undergoing a major update, thanks to technology that makes the whole process clearer and more supported by data. Think of artificial intelligence (AI) as your personal research expert, sorting through endless information to build a solid case for your claim. This new method is creating a more consistent standard for how these claims are figured out, which helps level the playing field for car owners.

In the past, figuring out a car's lost value was often a tricky and inconsistent task. But modern technology is changing that. AI, in particular, helps make diminished value claims more accurate and faster to settle by reviewing massive amounts of data and market trends much more effectively than old-fashioned methods.

The Rise of AI-Powered Appraisals

This shift is all about how a modern diminished value report is put together. Today, AI systems analyze huge databases filled with millions of pieces of information, such as:

- Up-to-the-minute results from vehicle auctions

- Private car sales from all over the country

- Data from dealership inventories and sales records

- Local market trends and changes in demand

These systems can look at thousands of similar vehicle sales in just seconds, spotting small details that a human appraiser might spend hours trying to find—or miss completely. For instance, an AI might find that a certain trim package on your car sells for a 15% premium in your area. That’s a key piece of information that can make your claim significantly stronger. By swapping subjective opinions for hard data, these reports are much tougher for insurance companies to argue against.

Easy-to-Use Tools for Everyone

This progress isn't just for the experts. New tools are now available that help regular people get a quick look at what their claim might be worth. There are even mobile apps that let you take a picture of your car’s damage and get a rough estimate of its lost value almost right away. These apps use image recognition to figure out how bad the damage is and check it against their own data.

Of course, these tools aren’t a replacement for a complete, certified appraisal, but they’re a great place to start. They can help you figure out if it’s worth your time and money to get a professional report and file a full claim.

Another exciting development is the potential of blockchain technology. Picture a secure, unchangeable digital file that records a car's entire history—from the factory floor to every oil change and, most importantly, any accidents. This kind of tamper-proof record could make it much easier to prove a car's condition before an accident and the value it lost afterward. This would cut down on arguments and make the claims process smoother for everyone. These new technologies are already shaping how a modern diminished value report is created, giving you more power to get back the money you're rightfully owed.

Your Complete Recovery Strategy And Action Plan

Winning a diminished value claim comes down to a simple but powerful mix: thorough preparation, consistent follow-up, and knowing which battles to fight. Think of this as your strategic map for what can sometimes feel like a confusing journey. Following a clear action plan helps you move through the process effectively, so you don't waste time or money on a claim that has little chance of succeeding.

Timing is everything. A well-timed claim can be the difference between a quick settlement and a long, drawn-out dispute. The best time to file your diminished value report is after all repairs are finished and paid for, but before you accept the final property damage settlement from the insurance company. This timing proves you have solid, quantifiable damages and are ready to close out the incident completely.

Phase 1: Meticulous Documentation And Evidence Gathering

Your claim's strength is directly tied to the evidence you provide. This means going far beyond just snapping a few photos of a dented bumper. You need to create a complete file that tells the full story of your vehicle’s value before the accident and the clear loss it has suffered since.

Your documentation checklist should include:

- Pre-Accident Condition: Gather recent maintenance records, receipts for upgrades like new tires or a premium stereo, and high-quality photos of your car before the crash, if you have them. This establishes that it was a well-maintained vehicle.

- Accident and Repair Records: Collect the official police report, the insurance adjuster’s first damage estimate, and the final, itemized repair bill from the body shop. The final invoice is essential because it details every part that was replaced and every hour of labor.

- The Professional Appraisal: This is the foundation of your claim. A credible diminished value report from a certified appraiser gives you the objective, third-party validation that insurance companies find difficult to ignore.

Think of this evidence file as the foundation of a house. Without a strong and complete one, anything you try to build on top of it could collapse. Each document adds another layer of undeniable proof.

Phase 2: Professional Communication And Persistent Follow-Up

With your evidence in hand, it’s time to contact the at-fault driver's insurance company. The goal is to be persistent without being a nuisance. Keep your communication professional, stick to the facts, and always communicate in writing to create a clear paper trail.

Here is a simple schedule to keep your claim on track:

- Initial Submission: Send your formal demand letter, your complete evidence file, and your diminished value report using certified mail with a return receipt requested.

- 7-Day Check-In: If you haven't received confirmation that they got your package after a week, send a polite follow-up email to the adjuster.

- 15-Day Follow-Up: If you still don't have a response or an offer, call the adjuster. On the call, refer to your written messages and ask for a specific timeline for their review. Send an email summarizing your conversation immediately after the call.

- 30-Day Escalation: If you get an unreasonably low offer or are being ignored, it's time to escalate. Send a formal letter to the adjuster’s supervisor, attaching copies of all your previous correspondence. This shows you're serious and won't just drop the claim.

Phase 3: Evaluating Offers And Knowing When to Settle

You should expect the first offer to be low. Don't get discouraged; this is a standard negotiation tactic. To evaluate their offer, compare it directly to the amount in your professional appraisal. A fair offer is one that is reasonably close to your appraiser's number, not one based on the insurer's internal, and often flawed, formulas.

Be aware of the warning signs that you might need professional help or should consider cutting your losses. If the insurer refuses to negotiate in good faith, stops responding completely, or if the amount in dispute is very large, it may be time to speak with an attorney. For most claims, however, a well-documented case paired with persistent, professional follow-up is enough to get a fair settlement.

Don't let an accident permanently reduce your vehicle's worth. At Loss Values Auto Appraisals, we provide certified, independent appraisals that hold up under insurance company review. If your vehicle has lost value after an accident that wasn't your fault, we can help you recover what you're rightfully owed. Contact us today for a fair and accurate settlement assessment.