When an insurance adjuster looks at a wrecked car, the first thing they have to figure out is a simple, yet crucial, question: will it cost more to fix this car than it's actually worth? That's the core of a total loss decision. They compare the shop's repair estimate to your vehicle’s Actual Cash Value (ACV), while also factoring in what they can get for the damaged car at a salvage auction. This basic formula drives the entire process.

Why Was My Car Declared a Total Loss?

Hearing an adjuster say your car is a "total loss" can be a real shock, especially if the damage doesn't look like a complete write-off. But this decision isn't about what the car looks like on the surface. It’s a numbers game, guided by state laws and the surprisingly high cost of fixing modern vehicles.

The key to this calculation is something called the total loss threshold. Each state sets a specific percentage. Once the repair costs hit that percentage of the car's value, the insurance company is legally required to declare it a total loss.

For example, many states have a threshold of 75%. If your car's ACV was $20,000 right before the crash, any repair estimate that climbs over $15,000 means it's automatically totaled.

The Role of Actual Cash Value (ACV)

Think of the ACV as the starting point for everything. It’s not about what you paid for the car or what a new one would cost—it's what your specific vehicle was worth in the open market the second before the accident happened.

To pin down that number, an adjuster digs into the details:

- Mileage and Age: Lower miles and newer model years mean a higher ACV. It's the biggest factor.

- Overall Condition: They’ll account for any pre-existing dings, scratches, or interior wear and tear.

- Trim Package and Options: A loaded model with a sunroof, leather seats, or a premium stereo is worth more than a base model.

- Local Market Data: They pull reports on what similar cars have recently sold for in your area.

This ACV becomes the benchmark. When the cost to repair the damage gets too close to that number, it just doesn't make financial sense for the insurer to fix it.

At the heart of any total loss claim are a few key variables that the insurance adjuster weighs. The process isn't random; it's a specific calculation based on these elements.

Key Factors in the Total Loss Decision

| Factor | Description | How It Affects the Calculation |

|---|---|---|

| Actual Cash Value (ACV) | The fair market value of your vehicle before the accident. | This sets the primary benchmark. All other costs are compared against this value. |

| Repair Estimate | The total projected cost for parts and labor to fix the vehicle. | This is the main figure compared against the ACV. |

| Total Loss Threshold | A percentage set by state law (e.g., 75%). | If Repair Estimate ÷ ACV is greater than this percentage, the car is a mandatory total loss. |

| Salvage Value | The amount the insurer can recover by selling the damaged vehicle. | This amount is subtracted from the ACV to determine the insurer's net payout, influencing their decision. |

Understanding these components helps demystify why a car that seems fixable might still be declared a total loss by the insurer.

Modern Cars and Rising Repair Costs

It’s not your imagination—repair costs have skyrocketed. A collision that might have been a straightforward fix a decade ago can now result in a staggering bill. Why? Because today's cars are packed with sophisticated technology.

That cracked bumper isn't just a piece of plastic anymore. It likely houses sensors for parking assist, blind-spot monitoring, or adaptive cruise control. Replacing it isn't enough; all those systems need to be professionally recalibrated, which requires expensive, specialized equipment.

A simple fender bender that would have been a $1,500 job ten years ago can easily top $4,000 or more on a new car. It's all because of the integrated sensors, cameras, and advanced driver-assistance systems (ADAS).

This problem is made worse by the fact that we're keeping our cars longer than ever. In the U.S., the average vehicle on the road is now a record 12.6 years old, a big jump from 9.5 years back in 2002. When these older, lower-value cars get into an accident, it doesn't take much damage to meet the total loss threshold, especially when you're up against today's inflated repair prices. You can read more about how the aging fleet impacts claims in a detailed report from Claims Journal.

How Insurers Figure Out a Car's Actual Cash Value (ACV)

When an insurance company declares your car a total loss, everything hinges on one number: its Actual Cash Value (ACV). This isn't what you originally paid for it, and it's definitely not what a brand-new replacement costs. ACV is the fair market price for your specific vehicle the second before the crash happened.

Getting this figure right is the single most critical part of the settlement process.

Insurers don't just pull this number out of thin air. The days of adjusters thumbing through a physical "blue book" are long gone. Today, almost all of them rely on sophisticated third-party valuation software. You'll often hear names like CCC ONE, which is a major player in the industry. These platforms are plugged into enormous databases that track real-world vehicle sales, giving them a starting point for your car's value.

But it's not a one-size-fits-all lookup. The software establishes a base value for your car's year, make, and model, and then the real work of fine-tuning that number begins.

It's All in the Details and Adjustments

This is where the adjuster comes in. They take all the specific details of your car and feed them into the system to get a more precise valuation. It’s a mix of automated data and manual input, which, importantly, means there's a real possibility of human error.

Here are the details that move the needle the most:

- Mileage: This is usually the biggest factor. Lower mileage means a higher value, and vice-versa. It's a straightforward but powerful adjuster.

- Trim Level & Options: A top-tier "Limited" or "Platinum" model is worth a lot more than the standard base version. The valuation report should account for every factory-installed feature, from a sunroof to a premium sound system or advanced safety package.

- Condition: The adjuster will assign a condition rating to your car (like excellent, average, or rough). They'll make deductions for any pre-existing damage, such as old door dings, deep scratches, or significant wear and tear on the interior.

Expert Tip: Never just accept the final number the insurer gives you. Always, always request the full, detailed valuation report. Go through it with a fine-tooth comb. Are they using the correct trim level? Did they miss the technology package you paid extra for? Is the condition rating fair? Mistakes are surprisingly common and can easily cost you thousands.

Finding "Comps" to Justify the Price

At the heart of any good valuation report is a list of comparable vehicles, or "comps." Think of these as real-world evidence. The software scours your local market to find recent sales of cars that are as similar to yours as possible—same year, make, model, and general features.

The software then averages the selling prices of these comps to create a baseline value for your car. From there, the adjuster makes final tweaks, adding or subtracting value based on how your car's specific mileage and options stack up against each individual comp. To get a better feel for how this works, you can dive into our guide on understanding fair market value.

It's also important to remember that the wider car market has a huge impact. For example, recent industry analyses showed North American light vehicle production was revised down to around 14.18 million units, a 6% drop from the previous year. When fewer new cars are being built, the supply of used cars tightens, and prices naturally go up. This market-wide pressure is a legitimate factor that should be reflected in your car's ACV.

Breaking Down Your Total Loss Settlement Offer

After the insurance company figures out your car's Actual Cash Value (ACV), you'll get a settlement offer. This isn't just one big number; it’s a detailed breakdown of several figures that add up to your final payout. You absolutely need to understand every line item to make sure you're getting a fair shake.

Think of the settlement sheet as the insurer showing their work. They start with the ACV, then add some costs and subtract others. Your job is to double-check their math and make sure everything that's legally required in your state is accounted for.

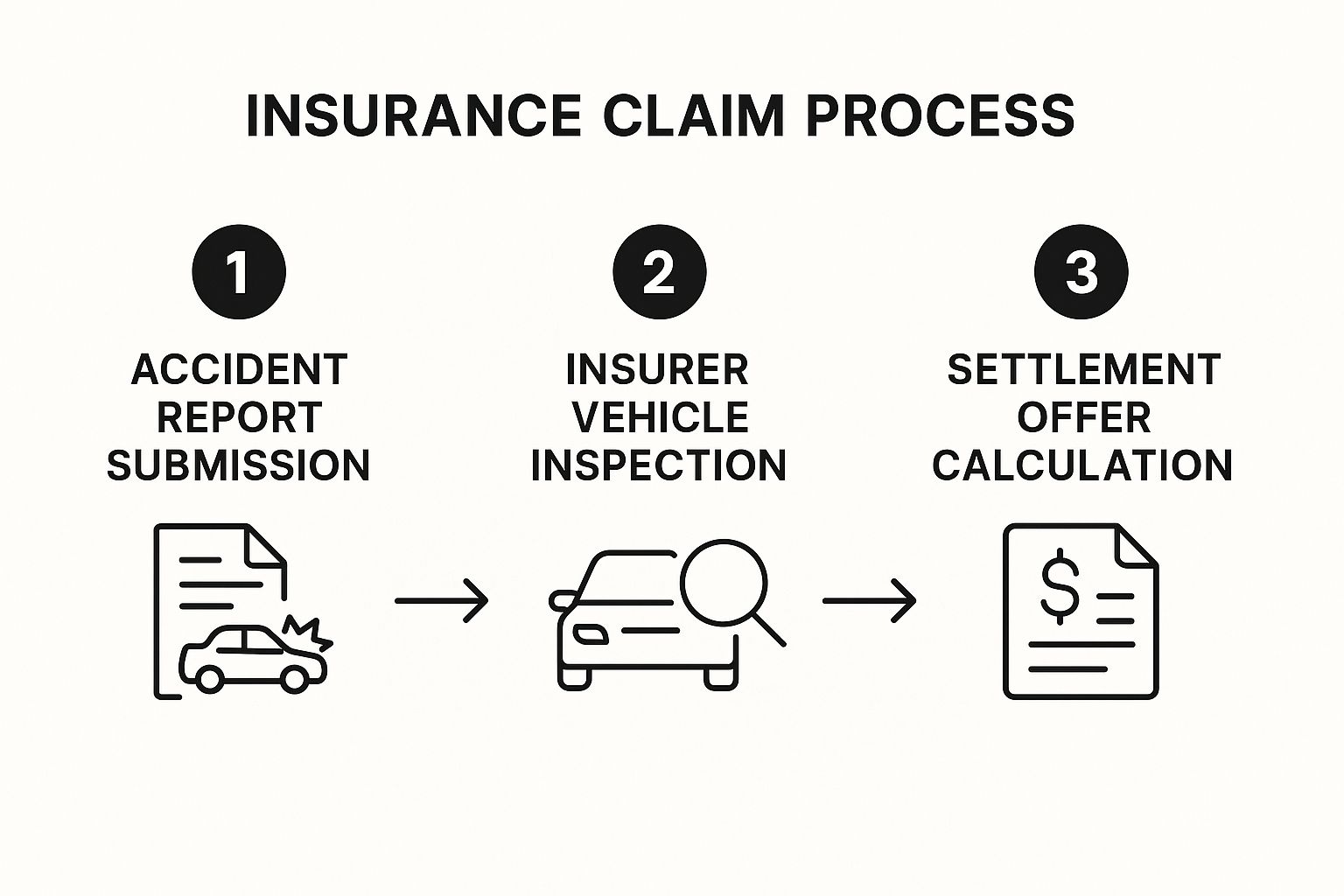

Calculating a total loss value can feel like a maze, but it’s a pretty straightforward process once you see the steps laid out. It starts the moment the accident happens and ends with that final offer in your hands. This flow chart gives you a bird's-eye view of the whole journey.

As you can see, that settlement offer is the last piece of the puzzle, built on everything that came before it—from the first report to the nitty-gritty vehicle inspection.

What to Look for Beyond the ACV

Your settlement isn’t just about the car’s raw value. In most states, the law says the insurer has to make you "whole," which means they need to cover the costs you'll face when buying a replacement car.

Look closely for these key items on your settlement sheet:

- Sales Tax: The insurer should add the sales tax you'd have to pay on a similar replacement vehicle. This is based on your local tax rate, so make sure they're using the right one.

- Title and Registration Fees: Getting a new car means paying for a new title and registration. Those fees should be part of your settlement, too.

If these costs are missing, you need to flag it for the adjuster right away. These are standard parts of a total loss payout, and they can add hundreds, sometimes thousands, of dollars to your check. Leaving them out is a classic way for adjusters to present a low initial offer.

I’ve seen this happen countless times. An insurer offers a $22,000 ACV but conveniently "forgets" the 7% local sales tax. That’s $1,540 you’d miss out on if you didn’t know to ask. Always, always check for taxes and fees.

The Role of Salvage Value and Owner Retention

The salvage value is what the insurance company thinks it can get by selling your wrecked car at a salvage auction, usually to a place like Copart or IAAI. This money helps them recoup some of what they paid you.

Normally, the insurance company takes your car, sells it for salvage, and you never have to think about it again. But sometimes, you have the option to keep your car, a choice known as owner retention. If you go this route, the insurer will simply subtract the salvage value from your settlement check.

Let's say your car's ACV is $10,000 and the adjuster determines its salvage value is $1,500. If you choose to keep it, you'll get a check for $8,500 and the keys to your damaged car, which will now have a salvage title. This really only makes sense if the car holds a lot of sentimental value, or if you're a mechanic with the skills and a plan to fix it properly.

Building Your Case for a Higher Payout

When the insurance adjuster calls with their first settlement offer, your instinct should be skepticism, not acceptance. That initial number is almost always generated by software using data that benefits the insurance company, not you.

This isn't about starting a fight. It's about building a solid, fact-based case that gives the adjuster a reason to increase their offer. The best way to do that? Become an expert on what your car was really worth right before the accident. Your own research is the most powerful tool you have to counter a lowball offer.

Find Your Own Comparable Vehicles

The insurance company used "comparable vehicles," or comps, to arrive at their number. Now, it’s your turn to do the same, but better. Don't just pull a generic value from a single pricing guide. You need to find real cars for sale, right now, in your local area.

Start digging on sites like Autotrader and Cars.com—even Facebook Marketplace can be a goldmine. The key is to get as specific as possible.

- Year, Make, and Model: That’s the easy part.

- Trim Package: This is where the money is. An EX-L model is a completely different vehicle than a base LX. Match the trim exactly.

- Mileage: Find comps with mileage within 10-15% of your car's odometer reading.

- Condition: Look for cars in similar pre-accident condition.

Be sure to save screenshots of every good match. Capture the asking price, the VIN, the options list, and the dealer's contact information. Finding just three to five solid, local examples priced higher than the insurer’s offer is compelling proof that their valuation doesn't reflect what it will actually cost you to replace your car.

Assemble Your Evidence Package

Your comps are the main event, but you also need supporting evidence. You have to prove your car was well-maintained and had features that the adjuster’s automated report probably missed. It’s time to play detective and gather every receipt and record you can find.

Create a file—digital or physical—with documentation for any recent work or upgrades. Think about things like:

- New Tires: Did you just spend $800+ on a set of new Michelins a few months back? That’s real, added value.

- Major Service: That 30,000-mile service you just paid for or the recent brake job adds tangible worth.

- Aftermarket Upgrades: A remote starter, an upgraded stereo, or custom wheels all count. If you paid for it, document it.

Think of it this way: you are building a counter-report to theirs. A well-organized package with pre-accident photos, maintenance records, and strong local comps makes it incredibly hard for an adjuster to stick to their initial low number.

Broader market trends can also be a factor. For example, recent global auto sales have seen significant shifts. When new car sales volumes drop—like the 13% decline seen in the U.S. not long ago—the supply of quality used cars tightens, which naturally drives up their value. You can read more about how global auto market shifts affect values. Pointing this out shows you've done your homework.

If you want to bring in the heavy artillery, getting a professional total loss vehicle appraisal provides a certified, independent report that can significantly strengthen your position.

Proven Tactics for Negotiating Your Settlement

Once you've put together all your evidence, the real work begins. This is where you actually start negotiating for a better total loss payout. It’s the part of the process where you can truly impact the final number, and success isn't about getting loud—it's about being professional, prepared, and persistent.

The first conversation you have with the adjuster really sets the tone for everything that follows. Make sure you lead with your research, not your frustration. So, instead of blurting out, "Your offer is way too low," you'll get a lot further with a more constructive approach.

Try something like this: "I've had a chance to review the valuation report, and I appreciate the work you put into it. Based on my own research into the local market, however, comparable vehicles are selling for a bit more. I just sent you an email with three examples I found."

See the difference? This approach instantly shows you're organized and basing your position on facts, not feelings. You aren't just complaining; you're presenting a documented, well-reasoned counteroffer.

Countering Common Adjuster Responses

Insurance adjusters are professional negotiators. It’s their job. Over the years, they develop a handful of go-to responses to push back on claims for a higher value. Knowing what they're likely to say is half the battle.

Here’s a look at what you might hear and how you can respond effectively:

-

"Those cars you sent have lower mileage." A perfectly valid point, but one you should be ready for. Your reply: "I've already accounted for that. According to industry mileage adjustment charts, my car's higher mileage would only justify a $300 adjustment, not the $2,500 gap between our valuations."

-

"We can't use dealer asking prices, only actual sales prices." This is a classic tactic. You can counter with: "I understand your point, but asking prices establish the current fair market value for a buyer in our area. That's the amount I'd have to pay to replace my vehicle today, which is exactly what an ACV settlement is supposed to cover."

-

"Our system sets the value automatically." Many adjusters lean on their software (like CCC ONE) as the final word. Gently push back: "I realize that software is a helpful tool, but it’s only as good as the data it’s using. In this case, it seems to have overlooked my car's premium technology package and the brand-new set of tires I bought back in May."

Always remember, the adjuster's primary goal is to close your claim quickly and for the lowest cost possible. Your goal is to make sure that settlement is fair and accurate. Your documentation is the only tool you have to bridge that gap.

What to Do When You Reach a Stalemate

So what happens if the adjuster just won't budge, even after you've presented solid evidence? Don't give up. Now is the time to bring up the appraisal clause in your auto insurance policy. This is a powerful, and often overlooked, tool for policyholders.

This clause gives both you and your insurance company the right to hire your own independent, certified appraisers. These two appraisers then work to determine the vehicle's true value. If they can't agree, they select a neutral third appraiser (called an umpire) to make the final call. The resulting decision is binding for everyone. Simply mentioning your intent to invoke this clause can often prompt the insurer to make a more reasonable offer just to avoid the extra time and expense. If you want to dive deeper, you can learn all about how to negotiate a total loss settlement in our dedicated guide.

Once you finally agree on a number, the last few steps are pretty straightforward. You'll want to carefully review all the final paperwork before you sign over your title. Most importantly, confirm the settlement check matches the agreed-upon amount down to the penny, including all the necessary taxes and fees.

Common Questions About Total Loss Claims

Once an insurance company declares your car a total loss, the questions don't stop. In fact, that's often when the most confusing part begins. Figuring out what happens next can be just as daunting as understanding the settlement calculation itself. Let's walk through some of the most common things people ask after getting the bad news.

"Can I Keep My Totaled Car?"

This is probably the first question that pops into most people's heads, especially if they have an emotional or mechanical attachment to their vehicle. The short answer is yes, you usually can. This option is called owner retention.

Here's the catch: the insurance company will pay you the car's actual cash value (ACV) minus its salvage value. If you take this deal, your state's DMV will issue the vehicle a salvage title. This is a permanent brand on the car's history, letting any future owner know it was once written off as a total loss. To make it road-legal again, you'll have to get it professionally repaired and pass a strict state inspection, which can be a real headache and a major expense.

"How Long Does a Total Loss Claim Take?"

It's tough to be patient when you're suddenly without a car, but these claims don't get sorted out in a day or two. The timeline can swing pretty wildly, but you can generally expect a straightforward claim to take anywhere from two to four weeks from the day you file to the day you get paid.

What can slow things down? A few things:

- The Adjuster's Schedule: How quickly can they get out to inspect the car and run the numbers?

- Negotiations: If you push back on their initial offer (and you often should), the back-and-forth adds time.

- Your Lender: If you have a car loan, the insurer has to work with your bank to process the payout, which can add days to the process.

A clean, undisputed claim where all the paperwork is in order will always be on the faster end of that timeline.

"What If I Owe More Than the Car Is Worth?"

This is the scenario every car owner dreads. It’s called being "upside-down" on your loan, and it’s a tough spot to be in. It happens when your settlement offer is less than what you still owe the bank. For example, if you owe $18,000 on your loan but the insurer’s final ACV is only $15,000, you’re on the hook for that $3,000 gap.

This is exactly what Guaranteed Asset Protection (GAP) insurance is for. If you bought GAP coverage when you financed the car, it’s designed to cover that exact difference, saving you from a significant out-of-pocket hit.

Without GAP insurance, you are still legally required to pay off the remainder of your loan to the lender, even though you don't have the car anymore. It’s a good idea to dig through your original purchase paperwork to see if you have this coverage.

Another thing to keep in mind is your insurance premium. If the accident was your fault, you should brace for a rate increase at your next renewal. If you weren't at fault, your rates shouldn't be affected, but this can depend on your specific insurer and state regulations.

If you're in Washington or Oregon staring at a lowball total loss offer, don't just accept it. At Total Loss Northwest, our certified appraisers create an ironclad case using real market data to ensure you get the fair settlement you're owed. We know how to invoke the appraisal clause and fight for you. Learn more about how we can help at totallossnw.com.