When your insurance company talks about a "total loss car valuation," they're talking about figuring out your car's actual cash value (ACV)—what it was worth on the open market a moment before the accident happened. This number is the foundation of your settlement offer.

It’s crucial to understand that this isn't about what you originally paid for the car or what you still owe on your loan. It's a snapshot of its market value. When the cost to repair the vehicle properly climbs higher than that value, the insurer declares it a total loss because fixing it no longer makes financial sense.

What It Means When Your Car Is a Total Loss

Hearing your insurance adjuster say your car is a "total loss" can be a shock. It’s more than just a mechanical assessment; it's a financial turning point that often feels confusing, and frankly, a little unfair. But the logic behind it is actually quite straightforward.

Think of it like a major home repair. If a storm causes $50,000 in damage to a house worth $300,000, you’d obviously fix it. But what if that same storm caused $250,000 in damage to a house only valued at $200,000? At that point, it’s a total loss. Spending that much on repairs just wouldn't be a sound investment.

A total loss car valuation works on the exact same principle. Your vehicle gets this designation when the estimated repair bill is higher than its pre-accident market value, a figure the industry calls its Actual Cash Value (ACV).

The Financial Equation of a Total Loss

This isn't just a gut feeling on the adjuster's part; it's a simple, though sometimes frustrating, calculation. Each state sets a "total loss threshold," which is a specific percentage of the car's ACV. If the estimated cost of repairs hits or goes over that percentage, the insurance company is legally required to declare it a total loss.

A "total loss" is a purely economic decision. It simply means that the cost to safely and properly repair your vehicle is more than what the vehicle was worth right before the crash.

Grasping this core concept is your first step to taking control of the claims process. It helps you shift your focus away from the visible damage and onto the real question at hand: what was my car truly worth? This is where the valuation process really begins.

Why Are More Cars Being Totaled These Days?

If it seems like you’re hearing about total losses more often, you’re not imagining things. One of the biggest reasons is the increasing age of the cars we drive. The average vehicle on U.S. roads is now a record 12.6 years old.

As cars get older, their Actual Cash Value drops significantly. At the same time, the cost of modern parts and skilled labor doesn't get any cheaper. This growing gap means even a moderate accident can result in a repair estimate that easily surpasses an older car's low value, pushing it into total loss territory. You can read more on this trend in reporting from the Claims Journal.

To put it all in perspective, here’s a quick breakdown of how an insurer looks at the two possible outcomes for your damaged car.

Total Loss vs Repairable Damage At a Glance

The following table offers a clear, side-by-side comparison to help you quickly understand why one car gets repaired while another is declared a total loss.

| Scenario | Repairable Damage | Total Loss |

|---|---|---|

| Financial Logic | Repair costs are less than the car's Actual Cash Value (ACV). | Repair costs exceed a specific percentage of the car's ACV. |

| Vehicle Outcome | The car is repaired and returned to you with its original title. | The car is not repaired; the insurer takes ownership. |

| Your Payout | The insurance company pays the body shop for the approved repairs. | The insurance company pays you the car's pre-accident ACV. |

Ultimately, whether your car is repaired or totaled comes down to this simple financial comparison. Both paths lead to very different outcomes for you and your vehicle.

How Insurers Calculate Your Car's Actual Cash Value

When your car is declared a total loss, the insurance company's first job is to land on one key number: the Actual Cash Value (ACV). This isn't what you originally paid for the car, nor is it what you still owe on your loan. Simply put, the ACV is what your vehicle was worth on the open market in the moments right before the crash.

Imagine trying to sell your car the day before the accident. The ACV is the realistic price a buyer in your local area would have likely paid for it in its exact pre-accident condition. It’s a snapshot in time meant to reflect true market value.

But how do they figure that out? Insurers don’t just pull a number out of a hat. They rely on sophisticated, third-party valuation services that are the data powerhouses of the industry.

The Role of Third-Party Valuation Companies

More often than not, your insurer will use data from specialized companies like CCC Intelligent Solutions or Mitchell International. These firms are the industry standard, maintaining massive databases of vehicle sales information that essentially act as the engine for calculating your car's value.

They gather a staggering amount of real-world data, including:

- Dealer asking prices: What cars like yours are listed for at local dealerships.

- Private party sales: Transaction data from people selling cars themselves.

- Auction results: The prices similar vehicles fetch at wholesale auctions.

By crunching millions of data points specific to your geographic area, these systems create a baseline value for your car's year, make, and model. This data-first approach is meant to standardize the process and remove subjective guesswork from the initial offer.

The basic formula for ACV is pretty straightforward: Market Value minus Depreciation. Where things get complicated is in how those two pieces are calculated—and that's where valuation reports and "comparable vehicles" enter the picture.

Knowing this is your first step to a fair settlement. The insurer isn't inventing a value; they're starting with a detailed report generated by one of these major data providers.

How a Baseline Value Is Established

The process starts with a valuation report that identifies several “comparable” vehicles, or “comps,” that have recently sold near you. These are supposed to be cars as identical to yours as possible. From there, an adjuster makes specific dollar adjustments to that baseline value based on what made your car unique.

Let's say the system finds three 2019 Honda CR-Vs that sold in your zip code. The report will then tweak that average value up or down. Did your car have exceptionally low mileage? That's a positive adjustment. Did it have some old dents, a stained interior, or worn-out tires? That's a negative adjustment. You can find an excellent deep dive into this topic by understanding the Actual Cash Value for your car.

To add another layer of data, insurers often cross-reference other industry reports. For example, they might look at MMR car values, which track wholesale pricing from major auto auctions, giving them a sense of what a dealer would pay for your car.

This initial valuation report is the single most important document you'll see in your claim. It’s the foundation for the insurance company's settlement offer, and it’s where you'll need to focus your attention. The adjustments—or lack thereof—are where most lowball offers come from and where you have the most room to negotiate for a fair payout.

Key Factors That Influence Your Car's Final Value

When the insurance company hands you their initial valuation report, it's crucial to remember that this isn't the final word. Think of it as their first offer—a starting point calculated from broad, generic data. The real, fair number is found by adjusting that baseline up or down based on the unique, specific details of your car. This is where you can make a real difference in your total loss settlement.

These adjustments are the heart of the appraisal process. They account for everything from the meticulous care you took of your vehicle to the premium features that made it stand out. By getting a handle on what appraisers look for, you can start building a rock-solid case for what your car was truly worth right before the accident.

Positive Adjustments That Increase Value

Certain features and a car's overall condition can give your settlement offer a significant boost. It's on you to prove these positive factors existed before the crash.

- Exceptionally Low Mileage: If your car has way fewer miles on the odometer than the average for its model year, it's more valuable. A vehicle with only 30,000 miles is naturally worth more than an identical one with 90,000 miles.

- Excellent Pre-Accident Condition: Was your car's interior and exterior in fantastic shape? If you have photos, they're worth their weight in gold now. A clean, well-cared-for car fetches a higher price than one with the usual dings, scratches, and wear.

- Premium Trim Levels and Options: A top-tier "Limited" or "Platinum" model is in a different league than the base model. You need to make sure the valuation report correctly identifies your car’s specific trim and accounts for all its factory options—things like a sunroof, leather seats, or an upgraded sound system.

- Recent Major Upgrades: Did you just spend $1,200 on a set of brand-new tires a month before the accident? Maybe you invested in a new suspension or a high-end stereo. These are tangible improvements that add real value, but you have to provide the receipts to get credit for them.

While your insurer is looking at the market, the physical condition of your car plays a huge role. Learning about strategies for car longevity often means you've preserved your vehicle's value without even realizing it. Every receipt for a recent, major purchase is another piece of evidence in your corner.

Negative Factors That Decrease Value

Just as positive factors can raise your offer, you can be sure the insurer will be looking for anything that might lower it. It's smart to know what they'll be scrutinizing so you can be prepared.

Common reasons for downward adjustments include:

- High Mileage: A car with mileage well above the average for its age will almost always have its value reduced.

- Pre-Existing Damage: Unrepaired dents, deep scratches, or mechanical problems that were there before the total-loss accident will be deducted from the car's value.

- Excessive Wear and Tear: Stained seats, worn-out tires, or a badly faded paint job will all lead to what the industry calls "conditioning adjustments."

- Prior Salvage or Rebuilt Title: If your car has a salvage or rebuilt title in its history, its value is automatically slashed by a huge margin—often 20-40%—compared to a similar vehicle with a clean title.

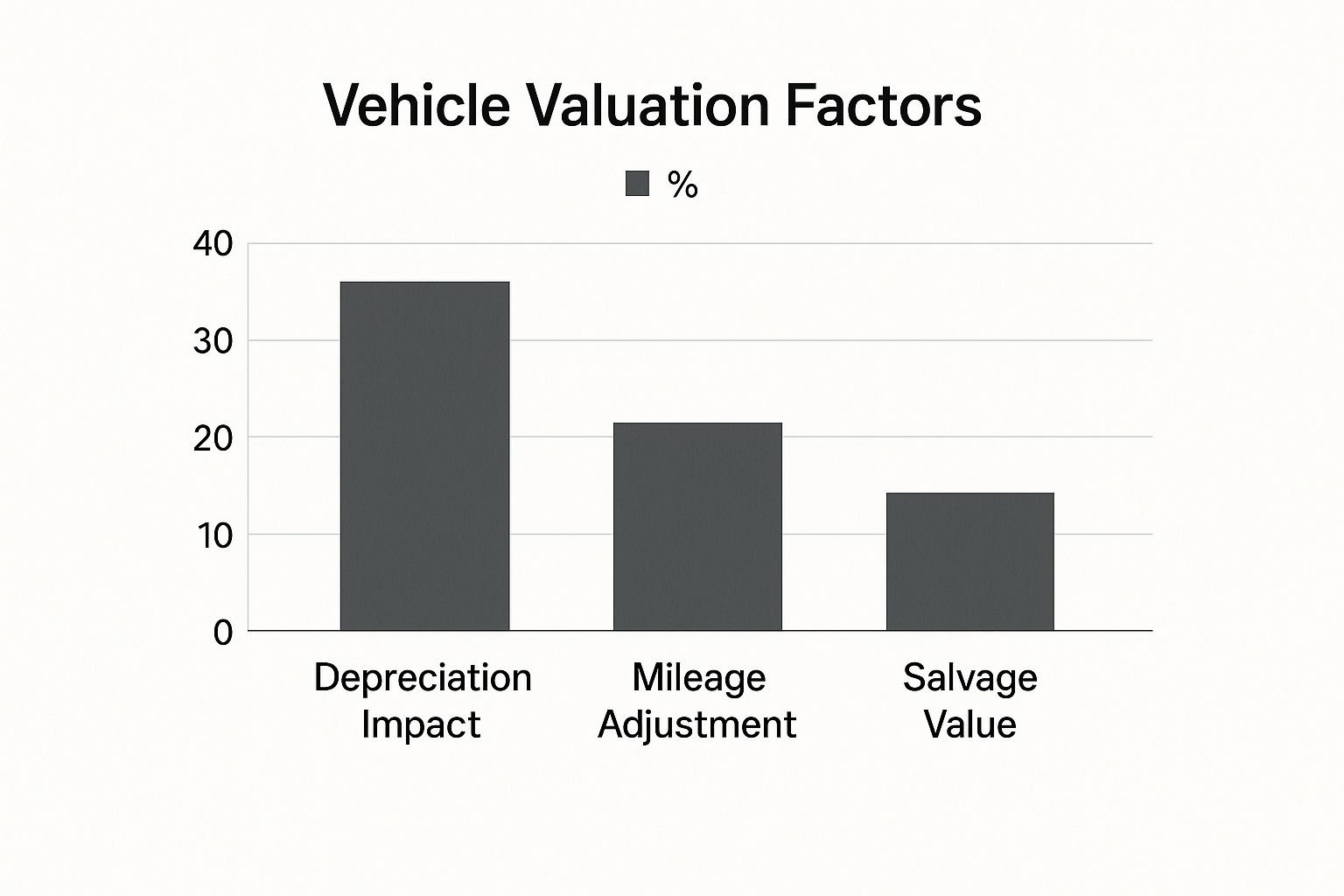

This image really drives home how several different elements come together to create that final number. It shows that a car's history and mileage are just as important as its base market price.

Factors Impacting Your Final Settlement Offer

The table below breaks down the most common factors that influence the Actual Cash Value (ACV) your insurer will offer. Being aware of these can help you anticipate the insurance company's position and build a stronger counter-argument.

| Factor | Potential Impact on Value | Example |

|---|---|---|

| Mileage | Increase or Decrease | Significantly lower-than-average mileage boosts value; higher mileage reduces it. |

| Trim Level | Increase or Decrease | A "Limited" or "Touring" trim is worth more than a base "LX" model. |

| Condition | Increase or Decrease | A pristine interior and exterior increase value; dents or stains decrease it. |

| Upgrades | Increase | Documented recent upgrades, like new tires or a stereo, add value. |

| Title History | Decrease | A prior "salvage" or "rebuilt" title will significantly lower the car's worth. |

| Maintenance | Increase | A complete and documented service history can prove excellent care. |

Ultimately, your settlement isn't a fixed price tag; it's a negotiation. The more proof you have to back up your car's true condition and features, the more power you have to secure a fair payout. For a deeper dive into this concept, check out our guide on what is fair market value and how it's calculated in an insurance claim.

How to Analyze the Insurance Valuation Report

When the insurer’s total loss valuation report finally arrives, it’s time to get to work. This document is the bedrock of their settlement offer, and knowing how to pick it apart, line by line, is your single biggest advantage. It's what separates a passive victim from an informed negotiator who can argue effectively for a fair payout.

You have to think of this report as the insurance company’s opening bid, not the final word. It's packed with data, adjustments, and assumptions—and every single one of them is up for debate. Your job is to fact-check their work and make sure the story they're telling actually matches your car's real, pre-accident value.

Scrutinizing the Comparable Vehicles

At the heart of any total loss valuation is a list of "comparable vehicles," often called "comps." These are supposedly similar cars that have recently sold, which the insurance company's system uses to create a baseline value for your vehicle. The entire settlement hinges on these comps being accurate.

Here’s exactly what you need to look for—the common red flags:

- Mismatched Trim Levels: This is a classic. Did they compare your top-tier "Limited" model with all the bells and whistles to a stripped-down, base "LX" version? This one mistake can cost you thousands.

- Significant Mileage Differences: The comps must have mileage that's in the same ballpark as your car's. A vehicle with 90,000 miles on the clock is simply not a fair comparison for your meticulously maintained car with only 50,000 miles.

- Geographic Distance: Comps should come from your local area. A car sold 200 miles away or in a different state might have a completely different market value. If it's not local, challenge it.

A fair total loss car valuation depends on truly comparable vehicles. If the "comps" are lower-end models, have higher mileage, or are from a different market, the entire valuation is built on a flawed foundation.

Decoding Condition Ratings and Adjustments

Once a baseline value is set using the comps, the report will add or subtract money based on your car's condition, optional features, and mileage. This is where things get subjective, and you need to pay close attention.

Insurers often use a generic condition scale (like poor, fair, good, excellent) and might default your car to "average" without considering its actual, real-world condition. If you kept your car in pristine shape, "average" is an insult that costs you money.

Go through every single adjustment. Did they credit you for the set of brand-new tires you put on last month? Did they miss the premium sound system or the factory sunroof? On the flip side, if they made a negative adjustment for "prior damage," make sure it's legitimate and not just a standard deduction they apply to every claim.

The broader car market also influences these numbers. For example, recent data showed that the biggest value increase was for newer vehicles (0-3 years old), which saw their average total loss market value jump by 0.96% in a single quarter. This was fueled by buyers wanting newer models during a period of price uncertainty. You can learn more about how these trends impact on total loss valuations. It’s a good reminder that market dynamics can, and do, affect your specific car’s value.

Negotiating a Fairer Total Loss Settlement

So, you’ve looked over the insurance company’s report and spotted the problems. The natural reaction is frustration, maybe even anger. But the next step isn’t a heated phone call—it’s strategy. Think of negotiating your total loss settlement less like a confrontation and more like building a calm, logical case for why your vehicle is worth more than their opening bid.

You've peeked behind the curtain and now see how the total loss car valuation game works. The insurer made their first move using their preferred data. Now, it's your turn to counter with your own research and close the gap between their lowball offer and your car's true Actual Cash Value.

Step 1: Build Your Counter-Valuation

Before you even think about calling the adjuster, you need to construct your own valuation from scratch. This isn't about feelings; you can't just say, "I think it's worth more." You need to prove it with hard data, and this independent research is the bedrock of your entire negotiation.

A great place to start is with the same tools everyone has access to. Head over to consumer sites like Kelley Blue Book (KBB) and Edmunds. Be brutally honest when you enter your car’s exact year, make, model, trim, mileage, and condition. Print those reports out. While insurers might dismiss them as "not what we use," they do establish a widely recognized market value range that’s hard to ignore.

Step 2: Find Your Own Comparable Vehicles

This is where you gain the most leverage. The insurance company found comps that supported their low number; now you need to find ones that support reality. Your mission is to scour local dealership websites and online marketplaces like Autotrader or Cars.com for vehicles that are a mirror image of yours.

Zero in on cars with:

- The exact same trim level and options package.

- Similar or, even better, slightly lower mileage.

- A clean title history (no salvage or rebuilt titles).

- Listings from within a 50-75 mile radius of your home, reflecting your local market.

Find at least three to five solid examples. Save and print the entire listing for each one. The asking price on these vehicles is your most powerful piece of evidence, because it shows exactly what it would cost to replace your car today.

Step 3: Assemble Your Evidence Package

Once your research is done, it's time to organize it. Don't just stuff a bunch of papers in an envelope. You need to present your case professionally, making it incredibly easy for the adjuster to follow your logic and, ultimately, agree with you.

A well-organized evidence binder is far more effective than an angry phone call. It shows you've done your homework and are serious about getting a fair total loss car valuation.

Your package should contain:

- A Cover Letter: Keep it short and professional. State that you're rejecting their initial offer and present your own valuation based on the evidence you've gathered.

- Your Research: Include the copies of your KBB and Edmunds valuation reports.

- Your Comps: Add the printed-out listings of the comparable vehicles you found.

- Proof of Value: Dig up all your maintenance records, receipts for recent work (like new tires, brakes, or a battery), and any proof of aftermarket upgrades.

- Photographs: If you have any pre-accident photos that show off your car's excellent condition, include them.

Step 4: Invoking the Appraisal Clause

What if you present your case and the insurer still won't budge? If you've hit a wall and are still far apart on the value, you have one last, powerful tool in your toolbox: the appraisal clause.

This clause, buried in most auto insurance policies, gives you the right to hire a certified independent appraiser. It triggers a formal process where your appraiser and the insurer's appraiser each determine the car's value independently. If they can’t come to an agreement, they bring in a neutral, third-party "umpire" who makes a final, binding decision. This process completely sidesteps the insurance company’s biased software and forces a resolution based on real-world evidence.

Our detailed guide offers more insight into how to negotiate a total loss settlement and explains exactly when it's time to bring in an expert.

You’ve done the hard work. You've negotiated with the adjuster and finally landed on a settlement figure you can live with. Now, what happens? Getting from an agreed-upon number to cash in hand involves a few final, but crucial, steps.

This last part of the process is all about the paperwork, signing over your wrecked car, and getting paid. Think of it as the final sale of your vehicle—only the buyer is the insurance company.

The Paperwork and Title Transfer

Once you agree to the settlement, the insurance company will send you a final packet of documents. You'll likely see a settlement agreement that officially states the final payout amount and forms to transfer ownership of the car. Read every single word before you sign.

You’ll need to hand over the physical title to your car. The adjuster will show you where to sign as the "seller." Don't be shy about asking questions here; a mistake on the title can cause annoying delays.

Once you sign that title and send it in, the car officially belongs to the insurance company. They'll then handle towing it from the body shop or storage yard to a salvage auction.

What If You Still Have a Car Loan?

This is a really common situation and it's important to understand how it works. If you have a loan on the car, the insurance company won't send the check directly to you. Instead, the payment goes straight to your lender (the bank or credit union) first.

The settlement money is used to pay off your outstanding loan balance. If the payout is more than what you owe, your lender will cut you a check for the leftover amount.

But what if you're "upside down" and owe more than the car is worth? You are still on the hook for that remaining balance. This is exactly what GAP (Guaranteed Asset Protection) insurance is for. If you purchased it, it will step in to cover that difference. The whole system is set up to make the lender whole before you see a dime.

Common Questions After a Total Loss

Even with a good grasp of the total loss process, a few nagging questions always seem to surface. Let's tackle some of the most common ones I hear from clients. Getting these sorted out can make a huge difference in how you navigate the final, often tricky, stages of your claim.

It's easy to feel lost when you're dealing with things like car loans or figuring out what to do with the wreck. Having clear, straightforward answers helps you make smart decisions without feeling rushed or pushed around by the insurance company.

What Happens if I Owe More on My Loan Than the Car is Worth?

This is a tough spot to be in, and it's surprisingly common. It’s often called being "upside-down" or having "negative equity." The core of the problem is that the insurance company's settlement is based on your car's Actual Cash Value (ACV), not what you owe on your loan. If there's a shortfall, you're legally on the hook for that difference.

This is the exact scenario GAP (Guaranteed Asset Protection) insurance was designed for.

- If you have GAP Coverage: You're in luck. This optional policy covers the "gap" between the ACV payout and your remaining loan balance. It pays off the lender directly, saving you from a potentially massive out-of-pocket expense.

- If you don't have GAP Coverage: Unfortunately, you'll have to pay the lender the remaining balance yourself after the insurance settlement money is applied to the loan.

Can I Keep My Totaled Car?

Yes, in most states, you can. The official term is "owner retention," and while it might sound like a good idea, you need to go into it with your eyes wide open. It’s a path loaded with complications and long-term consequences.

Here's how it works: the insurance company pays you the car's ACV, but they subtract its salvage value. The salvage value is what they would have gotten by selling the wreck to a salvage yard. Your car is then given a "salvage title," which permanently brands it as a vehicle that was once declared a total loss.

Choosing to keep your totaled car means accepting a lower payout and taking on the complex, often expensive task of making it roadworthy again. The resulting "rebuilt" title will permanently reduce its future resale value.

To get it back on the road legally, you have to complete all the repairs your state requires, pass a pretty tough safety inspection, and then apply for a new "rebuilt" title. It can be a long and expensive journey.

How Long Does a Total Loss Settlement Usually Take?

There's no single answer here—the timeline for a total loss claim can really vary. Generally, you can expect the process to take anywhere from a few weeks to over a month. The speed depends on everything from how clear the accident report is to how complicated it is to value your specific car.

A typical timeline often breaks down like this:

- Initial Inspection & Declaration (7-10 days): The adjuster examines the vehicle and officially declares it a total loss.

- Valuation & Offer (3-7 days): The insurer crunches the numbers and sends you their initial valuation report and settlement offer.

- Negotiation or Appraisal (1-3 weeks): This is the biggest variable. If you negotiate or have to invoke the appraisal clause, it will naturally extend the timeline.

- Payment Processing (1-2 weeks): Once you've agreed on a number, it still takes time to get the final paperwork processed and the check cut.

The best thing you can do to keep things moving is to get all your documents to the adjuster quickly and stay in regular contact with them.

If you’re in Washington or Oregon and staring at a lowball offer for your totaled vehicle, you don’t have to just take it. At Total Loss Northwest, we're certified independent appraisers who fight to get our clients the true market value they're owed. We use the appraisal clause in your policy to force a fair, evidence-based valuation. Don't leave your money on the table—visit us at Total Loss Northwest and get the expert help you need.