When your car is declared a total loss, one term suddenly becomes the most important phrase in your vocabulary: Actual Cash Value.

So, what does "actual cash value of my car" really mean? In the simplest terms, it’s what your car was worth in the seconds right before the accident happened. It's not the price you paid for it at the dealership years ago; it's the fair market price minus all the depreciation that has occurred since.

Decoding Actual Cash Value and Why It Matters

Getting a handle on your car's Actual Cash Value (ACV) is crucial when you're navigating a total loss insurance claim. This is the yardstick nearly every insurance company uses to figure out how much to pay you when your vehicle is damaged beyond repair.

Think of it this way: you wouldn't expect to sell a two-year-old smartphone for the same price you bought it for. New models have come out, and yours has seen some use. Your car's value works exactly the same way. The insurance payout is designed to cover the value of the asset you lost, not to hand you enough cash for a brand-new car. Understanding this difference is key to setting the right expectations from the start.

The Foundation of an Insurance Settlement

The ACV is the starting point—the baseline—for any settlement offer you'll receive. It's a snapshot of your car's value in the open market just before the incident. Insurance adjusters don't pull this number out of thin air; they use a specific set of data points to calculate it.

Here’s what they’re looking at:

- Age and Mileage: This is the big one. The older the car and the higher the odometer reading, the more its value has dropped.

- Overall Condition: Was it pristine or showing its age? This covers everything from the engine and transmission to the state of the interior and any dings or scratches.

- Geographic Location: A 4×4 truck might be worth more in a snowy mountain town than in a sunny city. Location matters.

- Market Trends: Is your specific make and model in high demand right now? That can also influence its value.

A car can lose between 15% to 25% of its value in the first few years alone, a rate that thankfully slows down over time. For a more detailed look, you can find a great breakdown of how car value is calculated on paininthecarwreck.com.

The whole point of an ACV payout is to make you financially whole again—to put you back in the same financial position you were in moments before the accident. It’s what a reasonable buyer would have paid for your car.

Ultimately, wrapping your head around this concept pulls back the curtain on the insurance process. It equips you to read the adjuster's valuation report, judge whether their offer is fair, and negotiate your claim with confidence.

Quick Overview of Key Valuation Terms

Navigating an insurance claim means you'll hear a few different valuation terms thrown around. It's easy to get them mixed up, but knowing the difference is critical. This table breaks down the most common ones you'll encounter.

| Valuation Term | What It Means | When It's Used |

|---|---|---|

| Actual Cash Value (ACV) | Your car's market value right before the loss, minus depreciation. | The standard for most auto insurance policies for total loss claims. |

| Replacement Cost Value (RCV) | The cost to buy a new car of a similar make and model. | Typically an optional, add-on coverage, not standard on most policies. |

| Agreed Value | A value for the vehicle that you and the insurer agree upon when you buy the policy. | Common for classic, custom, or high-value collectible cars. |

| Trade-In Value | The amount a dealership offers to give you for your car as credit toward a new purchase. | Always lower than ACV, as the dealer needs to make a profit on resale. |

| Retail Value | The price a dealer would list your car for on their lot. | Often higher than ACV, as it includes dealer overhead and profit margin. |

Having these definitions straight will help you better understand exactly what your insurance policy covers and what to expect from a settlement offer.

How Insurers Figure Out Your Car's ACV

So, your car has been in a serious accident, and the insurance company is talking about its "Actual Cash Value." How do they land on that number? It’s not just a guess. They follow a clear, data-driven process to figure out what your vehicle was worth the moment before the crash.

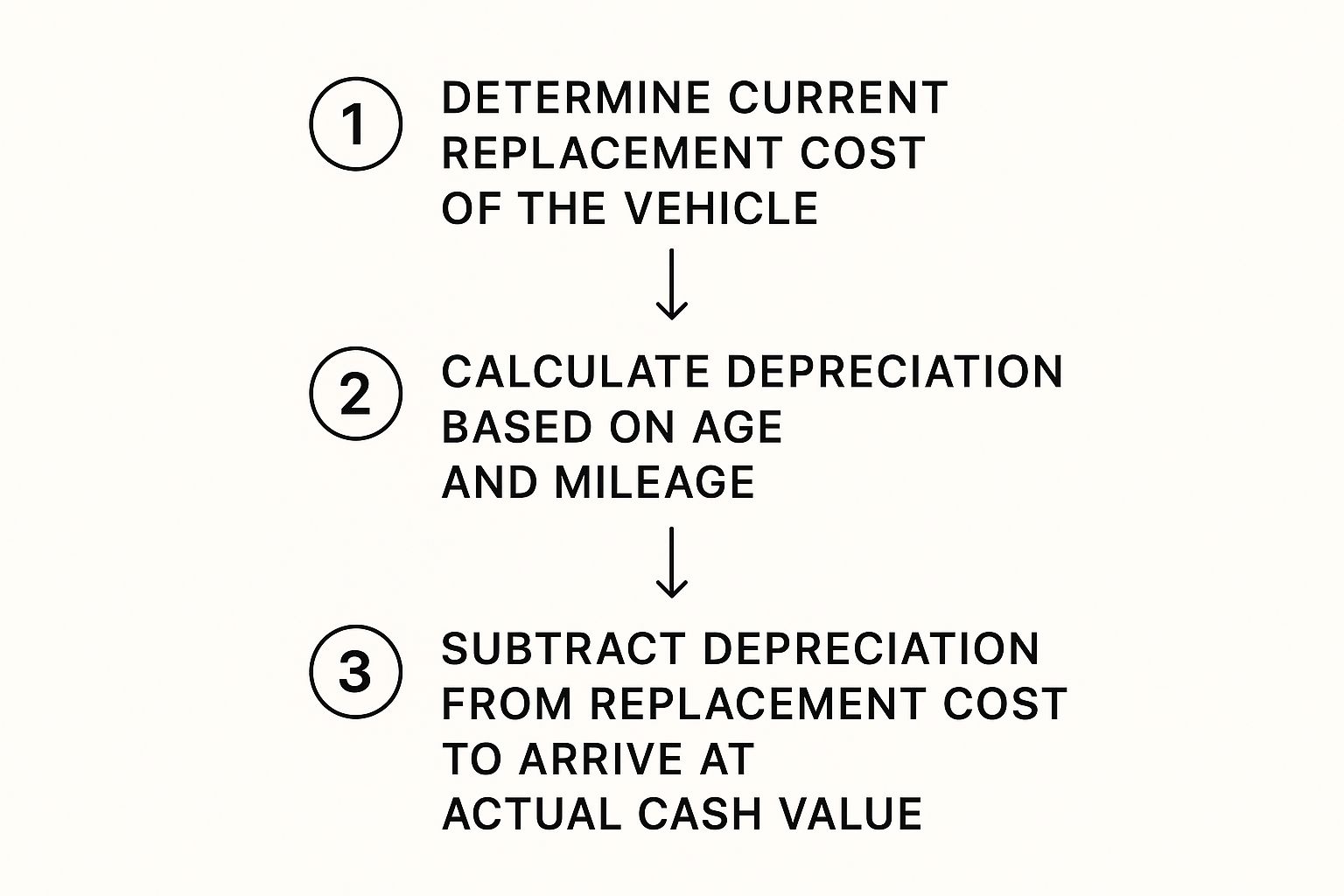

At its heart, the calculation is pretty straightforward. It all comes down to a simple formula:

Actual Cash Value (ACV) = Replacement Cost – Depreciation

Looks simple, right? But the magic is in understanding what those two terms really mean. Let’s break them down.

The Two Key Pieces of the ACV Puzzle

First up is replacement cost. This isn't what you originally paid for your car, and it's definitely not the price of a brand-new one off the lot. Instead, it’s what it would cost today to buy a used car that's the same make, model, and year as yours, and in similar shape. Insurance companies have massive databases they use to see what comparable cars are selling for in your local area to set this starting number.

Then comes depreciation. This is simply the value your car has lost over the years. Think of it as the cost of age, mileage, and all the little dings and scratches that come with normal use. Every mile you drive and every year that passes chips away at a car's value. By subtracting this accumulated depreciation from the replacement cost, the insurer gets the final ACV.

This infographic lays out the step-by-step process nicely.

As you can see, it’s a logical flow. They start with a baseline value and then adjust it down for wear and tear, which gives them the car's true market value right before the loss.

A Real-World ACV Example

Let's walk through an example to make it crystal clear. Say you bought a new Toyota Camry three years ago for $25,000. Because of market shifts, a similar three-year-old Camry today might actually cost $27,000 to buy—that’s your replacement cost.

Over those three years, however, your car has racked up miles and shown some wear, leading to $10,000 in depreciation.

So, the math looks like this: $27,000 (Replacement Cost) – $10,000 (Depreciation) = $17,000 (ACV). This $17,000 is the amount your insurance company would offer you as a settlement, before taking out your deductible.

The Tools and Data Behind the Scenes

Insurance adjusters aren't just pulling these numbers out of thin air. They lean on powerful, third-party valuation services to get it right. These platforms are the industry go-to for pinning down a vehicle's value.

You'll often hear about a couple of major players:

- CCC ONE: This is a huge one. It taps into a giant database of vehicle sales to generate incredibly detailed valuation reports.

- Mitchell: Another industry leader, Mitchell's software crunches local market data, vehicle condition reports, and specific features to calculate a precise ACV.

These tools give the adjuster a starting value for a "clean" version of your car. From there, the adjuster fine-tunes the number. They'll make adjustments up or down based on your car's actual mileage, its documented condition, and any special options it might have. You can dive deeper into the nitty-gritty of the details of the actual cash value formula on our site.

This blend of high-tech software and a hands-on review by an adjuster is how they arrive at the final number for your specific car.

The Key Factors That Influence Your Car's Value

Figuring out your car's Actual Cash Value isn't as simple as plugging numbers into a formula. It's more like piecing together its entire life story. Every mile on the odometer, every oil change, and even the city you park it in all play a role in the final number.

Think of it like a home appraisal. The appraiser doesn't just glance at the square footage; they check the roof's age, the quality of the kitchen, what the neighborhood is like, and what similar homes nearby have sold for. Insurance adjusters do the same thing with your car, digging into a specific set of factors to figure out what a reasonable person would have paid for it just moments before the accident.

Let's break down exactly what they're looking at.

The Big Three: Age, Mileage, and Condition

These three factors are the bedrock of any vehicle valuation. They are the biggest drivers of depreciation and give the adjuster a starting point for calculating your car's ACV.

-

Age: This one’s pretty straightforward. A car's value naturally drops as it gets older and new models with better tech and features hit the showrooms. All else being equal, a 2022 model will always be worth more than an identical 2018 model.

-

Mileage: The odometer is a direct report card on how much work the car has done. High mileage means more potential wear on the engine, transmission, and suspension, which pulls the market value down. A car with surprisingly low mileage for its age is a gem, suggesting it's been well-preserved and can command a higher price.

-

Pre-Accident Condition: This is where the little details make a huge difference. Adjusters look past the age and mileage to grade the vehicle’s overall shape, usually on a scale from poor to excellent. They’re inspecting everything: the engine's mechanical health, the cleanliness of the interior, the shine of the paint, and any old dings, scratches, or rust.

A car with a stack of service records, a spotless interior, and perfect paint will be valued much higher than another vehicle of the same year and mileage that’s been clearly neglected.

To illustrate just how much condition matters, let's look at a hypothetical example. A car with a base market value might see its final ACV swing dramatically based on its overall state.

Impact of Condition on Actual Cash Value

| Vehicle Condition | Description | Potential ACV Adjustment |

|---|---|---|

| Excellent | Showroom quality. No mechanical issues, flawless interior, perfect paint. All records available. | Can increase value by 10-20% or more. |

| Good | Minor cosmetic flaws (e.g., small scratches). Clean interior, runs well with no known issues. | This is the baseline; little to no adjustment. |

| Fair | Visible cosmetic damage (dents, rust). Some mechanical issues may be present. Interior shows wear. | Can decrease value by 15-25%. |

| Poor | Significant mechanical problems. Major cosmetic damage, rust, or a heavily worn interior. | Can decrease value by 40% or more. |

As you can see, two cars that look identical on paper (same year, make, model) can have vastly different values based on how they were cared for.

Location and Market Demand

Believe it or not, your car’s zip code has a real impact on its value. It all comes down to simple supply and demand, and what’s popular in one part of the country might not be in another.

A convertible, for example, is going to fetch a much higher price in sunny Southern California than it will in snowy Upstate New York. On the flip side, an all-wheel-drive SUV is a hot commodity in a mountain town with harsh winters, which boosts its local market value. An adjuster in Seattle will value a Subaru Outback completely differently than an adjuster in Miami, simply because the local buyers have different needs.

They'll even consider things like regional climate. A car from a dry place like Arizona is far less likely to have rust issues than one from the "Salt Belt," where winter road treatments can wreak havoc on a vehicle's undercarriage.

Insurance companies rely on trusted third-party valuation tools like Kelley Blue Book, Edmunds, and NADA Guides to establish a vehicle's baseline ACV. These platforms analyze make, model, year, mileage, condition, and location. State regulations also play a part, often requiring a vehicle to be declared a total loss when repair costs exceed 70-80% of its ACV. You can learn more by exploring how insurance companies value cars in their claims process.

Documented History and Recent Repairs

Your car’s vehicle history report is basically its resume, and a clean one can add serious value. A car with a clean title and no accident history is far more appealing to a buyer than one with a collision record or a salvage title. Adjusters will always pull this report to look for red flags.

On the other hand, you can sometimes get a bump in value from recent, major repairs—but only if you have the receipts to prove the work was done.

Examples of Value-Adding Repairs:

- A newly replaced engine or transmission

- A brand-new set of high-quality tires

- A recent major service, like a timing belt replacement

- A complete brake system overhaul

These investments prove the car was well-maintained and that key components had plenty of life left in them. Just keep in mind that most aftermarket add-ons, like a custom stereo or fancy wheels, rarely add to the ACV in an insurer's eyes unless you have specific custom parts coverage. Their focus is almost always on the car's mechanical soundness and factory-equivalent condition.

ACV vs. Replacement Cost vs. Stated Value: What's the Difference?

When your car is declared a total loss, the type of insurance coverage you have is what drives the entire settlement process. Not all policies are created equal, and the valuation method your insurer uses will make a huge difference in the check you receive.

The three main ways insurers value a totaled vehicle are Actual Cash Value (ACV), Replacement Cost Value (RCV), and Stated Value.

Let's use an analogy. Think of it like a smartphone. ACV is what you could sell your two-year-old phone for on the open market today. RCV is what it would cost to walk into a store and buy this year's brand-new model. Stated Value is like a rare, first-generation iPhone in its original box—its value is a specific, agreed-upon amount based on its collectibility.

Knowing which coverage you carry is the first step. It sets the stage for what you can realistically expect from your settlement. Let's break down how each one really works.

Actual Cash Value: The Industry Standard

For the vast majority of us, Actual Cash Value is the default setting on our auto insurance policies. As we've covered, ACV is simply your car's fair market value the second before it was wrecked. It’s the sticker price minus all the depreciation from age, mileage, condition, and general wear and tear.

This is the most common and affordable type of coverage out there. It’s built to give you a payout that reflects what your car was actually worth at the time of the loss, not what you first paid for it. For most daily drivers, ACV strikes a practical balance between the monthly premium and the protection you get. You can get a much deeper look into what fair market value is and see how it’s the foundation for any ACV calculation.

Replacement Cost Value: The New Car Option

Replacement Cost Value (RCV) is a completely different animal. It's an optional endorsement you can add to your policy, and it does exactly what the name implies. Instead of cutting you a check for your old car's depreciated value, an RCV policy gives you enough money to buy a brand-new vehicle of the same make and model.

This coverage isn't for everyone; it's typically only offered for cars that are just a few years old. While it does mean a higher premium, it offers incredible peace of mind by closing the gap that depreciation creates. If your two-year-old car gets totaled, RCV means you can head right back to the dealership and get the current year's model without having to dig into your savings.

The Bottom Line: ACV pays you what your used car was worth. RCV pays you to replace it with a new one. Simple as that.

Stated Value: The Collector's Choice

Finally, we have Stated Value coverage. This is a specialized policy for vehicles where the normal rulebook for valuation just doesn't work—think classic cars, custom-built hot rods, or heavily modified trucks.

Here’s the process: when you take out the policy, you and the insurance company agree on a specific, fixed value for the car. That becomes the "stated value." If the car is totaled, that's the amount you get paid, period. It requires a professional appraisal and plenty of documentation to justify the car's worth, but it’s the only way to ensure a unique, high-value vehicle is properly protected.

Let's put it all together with an example.

Scenario: A 2-year-old SUV, originally purchased for $40,000, is totaled.

- ACV Policy: After accounting for depreciation, the insurer determines its actual cash value is $28,000. That's the settlement you'll receive (minus your deductible).

- RCV Policy: A brand-new, current-year model of that same SUV now costs $43,000. Your settlement will be for that amount, letting you buy a new replacement.

- Stated Value Policy (Hypothetical): If this was a rare, collectible model, you might have agreed to a stated value of $50,000 when you bought the policy. That's the amount you'd be paid.

Ultimately, knowing your car's actual cash value is just one piece of the puzzle. The type of policy you chose to buy is what truly determines your financial outcome after a total loss.

Navigating a Total Loss Declaration

Hearing an insurance adjuster tell you your car is a "total loss" is a gut-punch moment for any driver. It’s confusing, stressful, and leaves you wondering what comes next. What it means, in simple terms, is that the insurance company has decided it would cost more to fix your car than it’s actually worth.

This isn't just a judgment call; it's based on a formula. Your car hits its total loss threshold when the cost to repair it (plus what it would sell for as salvage) exceeds its pre-accident Actual Cash Value (ACV). Every state sets its own rules, but a common benchmark is when repair costs hit 70-80% of the car's ACV.

At that point, the insurer sees fixing the vehicle as a bad investment. Instead of paying for repairs, they'll write you a check for the car's value and take ownership of it. This declaration kicks off a whole new phase of your insurance claim.

What the Adjuster Does Behind the Scenes

After an accident, the adjuster's first move is to play detective with your car. They’ll do a detailed inspection, documenting every dent, scratch, and broken part to create a comprehensive repair estimate. This is a meticulous process designed to calculate the true cost of bringing your vehicle back to its pre-accident state.

Next, they take your car's vital stats—make, model, year, mileage, and overall condition—and plug them into a third-party valuation service. This is how they determine the ACV, answering the big question: "What was my car worth right before the crash?". If the repair estimate crosses that state-mandated total loss threshold, you’ll get the official call with their decision and a settlement offer based on the ACV.

Decoding Your Settlement Offer

Once your car is officially a total loss, the insurance company will present you with their settlement offer. This is the amount they're prepared to pay you for the vehicle. If you own your car free and clear, the money comes straight to you once you sign over the title.

But things get a bit more complicated if you have an auto loan or lease.

By law, the insurance company must pay your lender first. The settlement check goes directly to the lienholder (the bank or credit union) to clear your outstanding loan balance.

If the ACV payout is more than what you owe, you get to pocket the difference. The real problem arises when the ACV is less than your loan balance, leaving you on the hook for the remaining amount on a car you can no longer drive.

Your Rights and Options After the Declaration

Even when your car is declared a total loss, you aren't powerless. The most common route is to accept the settlement, sign the title over, and let the insurance company take the vehicle. They’ll usually sell it for scrap or parts at a salvage auction.

However, you often have another choice:

- Keep the car. This is known as "retaining the salvage." If you go this route, the insurer subtracts the car's salvage value from your ACV payout and gives you the rest. You'll get the car back with a salvage title, but you're now responsible for all repairs and navigating the tricky process of getting it re-titled and insured again.

The Lifesaving Role of GAP Insurance

What happens if your car’s ACV is less than what you owe on your loan? This scary scenario is known as being "upside down" or "underwater" on your loan, and it’s where Guaranteed Asset Protection (GAP) insurance proves its worth.

GAP insurance is an optional add-on that covers the "gap" between your ACV settlement and your remaining loan balance.

Let’s say your car's ACV is $15,000, but you still owe $18,000 on your loan. Your standard policy will only pay the lender $15,000. Without GAP insurance, you'd have to find a way to pay that extra $3,000 yourself. With it, the GAP policy steps in and covers that difference, saving you from a major financial headache.

How to Negotiate a Fairer ACV Settlement

When the insurance company sends over their settlement offer for your totaled car, don't just take it at face value. That initial number isn't a final decision—it's an opening offer. Think of it as the start of a conversation. If you have a gut feeling that they've lowballed the actual cash value of your car, you're well within your rights to push back with a counteroffer.

The trick is to be prepared. You need to shift from just accepting their number to actively proving your car was worth more. This isn't about getting emotional; it's about being organized, doing your homework, and approaching the discussion like a professional.

Your Step-by-Step Negotiation Playbook

You're essentially building a case for your car's true value. Your opinion, unfortunately, doesn't carry much weight on its own. What does? Hard evidence. A successful negotiation is built on solid proof that an adjuster can't simply ignore.

Here’s a simple plan to get you started:

- Get the Valuation Report: The very first thing you should do is ask the adjuster for a full copy of their valuation report. This document, often from a third-party like CCC ONE, breaks down exactly how they landed on their ACV number.

- Go Over It with a Fine-Tooth Comb: Read every single line of that report. Are they listing the correct trim level? Did they miss any of your car's optional features? Is the mileage accurate? Pay close attention to the condition rating—if they marked your car as "Fair" when it was in excellent shape, that's a major point of contention.

- Collect Your Proof: Now it's time to build your counter-argument. Dig up every maintenance record, receipt for new tires, and photo you have that shows your car was well-cared-for and in great condition before the accident.

An insurer's valuation is based on data, but that data might not tell the whole story of your specific vehicle. Your job is to provide the missing chapters with concrete proof of its superior condition and maintenance.

Building Your Case with Comparable Vehicles

One of the most effective negotiation tactics is to find comparable vehicles—or "comps." These are real, for-sale listings for cars of the same make, model, and year as yours, right in your local area.

The goal is to find a few examples from local dealerships (private party sales are less reliable) that have a higher asking price than the insurer's offer. Look for cars with similar mileage and features. Save screenshots or print the listings to use as concrete evidence.

When you talk to the adjuster, you can say something firm but polite, like:

- "I've found three similar vehicles for sale at local dealerships, and they are all listed for significantly more than my settlement offer. This suggests my car's local market value is higher than your report indicates."

Bringing this kind of local market data to the table changes the entire conversation. You're no longer debating opinions; you're discussing facts. For a more detailed breakdown of this strategy, our guide on how to negotiate a total loss settlement walks you through every step.

Just remember, a strong negotiation is always backed by strong evidence.

Your Top Questions About Car ACV, Answered

When your car is declared a total loss, the questions start piling up fast. It's a confusing process, and getting straight answers is the first step toward getting back on the road. Let's tackle some of the most common things people ask about their car's actual cash value.

Is There Anything I Can Do to Increase My Car’s ACV?

Absolutely. While you can't turn back the clock on your car's age or mileage, you can definitely fight for a higher ACV by proving your vehicle was in better-than-average shape before the accident. The insurance company's first offer is often based on the assumption that your car was just… average. Your job is to prove it was exceptional.

To do that, you need to build a case with solid proof. Here's what works:

- A full stack of maintenance records: Nothing speaks louder than a detailed history of regular oil changes, tire rotations, and all the scheduled service milestones.

- Receipts for big-ticket items: Did you recently replace the transmission? Get new high-quality tires? Those receipts are gold because they add real, provable value.

- Photos from before the accident: If you have pictures showing a spotless interior or a gleaming, dent-free exterior, use them! They can directly challenge an adjuster's low rating on your vehicle’s condition.

What if the ACV Isn’t Enough to Pay Off My Car Loan?

This is a tough, and unfortunately common, situation. It's often called being "upside down" or "underwater" on your loan. If the insurance company's ACV payout is less than what you still owe, the check goes straight to your lender, and you're on the hook for the remaining balance.

This is the exact problem Guaranteed Asset Protection (GAP) insurance was created to solve. If you have GAP coverage, it steps in and pays the difference between your ACV settlement and your remaining loan balance, saving you from a potentially massive out-of-pocket expense.

Will My Aftermarket Upgrades Increase the ACV?

In most cases, a standard policy won't give you a dime for them. Your fancy custom wheels, upgraded stereo, or new exhaust might make the car more valuable in a private sale, but insurers calculate ACV based on the car as it came from the factory.

The one way around this is to have a special add-on to your policy, usually called Custom Parts and Equipment (CPE) coverage. This endorsement specifically insures the value of your modifications. If you've invested in upgrading your vehicle, you need to tell your insurance agent before an accident happens to make sure you're covered.

At Total Loss Northwest, we live and breathe this stuff. Our entire focus is making sure you get a fair, accurate settlement. If you feel the insurer's offer is lowballing you, our certified independent appraisers can invoke the Appraisal Clause in your policy. We’ll build an evidence-based report that forces them to re-evaluate. Don't settle for less than your car was worth—see how we can help at https://totallossnw.com.