When you file a diminished value claim, you're officially asking the at-fault driver's insurance company to pay you for the hit your car's resale value took after an accident. It's a simple fact: even with flawless repairs, a car with an accident on its record is worth less. If you weren't at fault, you have a legal right to get that money back.

The Foundation of a Diminished Value Claim

When another driver is responsible for an accident, their insurance has a duty to make you "whole" again. This principle goes beyond just footing the bill for repairs. It's about restoring you to the exact financial position you were in right before the crash.

Because a car with a documented accident history is less appealing to buyers, its market value takes a permanent dip. That drop is what we call diminished value.

Let's put it in real-world terms. Imagine two identical used cars on a lot. One has a squeaky-clean vehicle history report, but the other was in a major collision and has since been perfectly repaired. Which one would you pay more for? Almost every buyer would choose the one without the accident history, or at the very least, demand a steep discount for the one that was wrecked. That price gap is exactly what your claim is trying to recover.

The Two Faces of Diminished Value

It helps to know exactly what kind of value loss you're dealing with. While there are a few technical definitions, most claims boil down to one key type: Inherent Diminished Value.

- Inherent Diminished Value: This is the automatic loss in value that happens the moment an accident is recorded on your vehicle's history. It's the most common type of claim and assumes the repairs were top-notch. You're basically saying, "Even with perfect repairs, my car is now worth less."

- Repair-Related Diminished Value: This is a separate issue. It's the additional loss in value because the repairs themselves were shoddy. Think mismatched paint, panels that don't quite line up, or lingering mechanical quirks. Proving this usually means getting another inspection and often becomes a dispute with the repair shop itself.

For the vast majority of people reading this, the focus is squarely on inherent diminished value. The accident wasn't your fault, and now your asset is worth less. Period.

Why This Loss of Value is a Big Deal

The financial fallout from an accident is more than just the repair invoice. Vehicle depreciation is a very real, measurable loss. An average car loses about 12.5% of its value each year, but a significant accident can throw that curve into overdrive.

Filing a diminished value claim isn't about getting a bonus—it's about asking the at-fault party's insurer to cover a legitimate financial loss they caused. You can find more great insights on how accidents impact car value at Diminished Value of Georgia.

The core idea is simple: You shouldn't be left out of pocket because of someone else's mistake. A diminished value claim is the tool that ensures you're fully compensated for every part of the damage to your property.

To help you see the path ahead, I've put together a quick roadmap of the claims process. Think of it as your high-level guide to what's coming.

Your Diminished Value Claim Roadmap

This table gives you a high-level overview of the claims process, giving you a quick reference for each stage.

| Phase | Objective | Key Action |

|---|---|---|

| Eligibility & Assessment | Confirm you have a valid claim and estimate the potential loss. | Verify you were not at-fault and consult a professional appraiser. |

| Documentation & Evidence | Build an undeniable case supported by official records. | Gather police reports, repair invoices, and a certified appraisal. |

| Submission & Negotiation | Formally demand payment and negotiate a fair settlement. | Send a detailed demand letter and counter any lowball offers. |

| Resolution | Secure your compensation through agreement or escalation. | Accept a fair settlement or prepare for small claims court. |

Each phase has its own set of challenges, but understanding the big picture makes the entire journey much more manageable.

Building an Unbeatable Case for Your Claim

Let's be blunt: an insurance adjuster's primary role is to protect their company's bottom line by minimizing payouts. Just telling them your car is worth less now won't get you very far. You need to build a rock-solid, evidence-based case that makes your loss impossible to ignore. This is where you pivot from being the victim of an accident to the architect of your own financial recovery.

Success comes down to one thing: documentation. Every receipt, every photo, every report is a brick in the wall of your argument. Think of it like a detective building a case—your goal is to leave absolutely no room for doubt.

Your Essential Evidence Checklist

Before you even draft a demand letter, you have to gather your proof. I always tell my clients to get a dedicated folder—digital or physical, it doesn't matter—and keep everything in one place. Disorganization is the single biggest enemy of a successful claim.

Your evidence needs to tell the complete story of your car, from its pristine pre-accident condition to its post-repair reality. Here are the non-negotiable documents you need to track down:

- The Official Police Report: This is your foundation. It officially establishes who was at fault, a critical detail for any third-party diminished value claim.

- Complete Repair Invoices: Get the final, itemized bill from the body shop. This document proves the extent of the damage and shows that significant work was done, which is central to proving inherent diminished value.

- Pre-Accident Service Records: Were you meticulous about maintenance? Your service records prove your car was in excellent shape before the crash, which supports a higher pre-accident value.

- High-Quality Photographs: Visuals are incredibly persuasive. You'll want photos from before the accident (if possible), right after the crash, and once the repairs are finished to show the full timeline.

An insurance company will almost certainly argue that high-quality repairs made your car "as good as new." Your job is to prove that while the car may be fixed, its market value is permanently scarred because of the accident history now tied to its VIN.

The Power of Post-Repair Photography

Don't just take a few quick snaps of your repaired car. Be strategic. Take clear, well-lit photos from every angle, paying close attention to the repaired areas. Even if the work looks flawless, these photos prove the vehicle underwent major structural or cosmetic surgery.

For instance, get wide shots of the entire car, then zoom in for close-ups of the specific panels that were replaced or repainted. This visual evidence works hand-in-hand with your repair invoice, making the damage much more tangible for the adjuster who's just looking at a file on their screen.

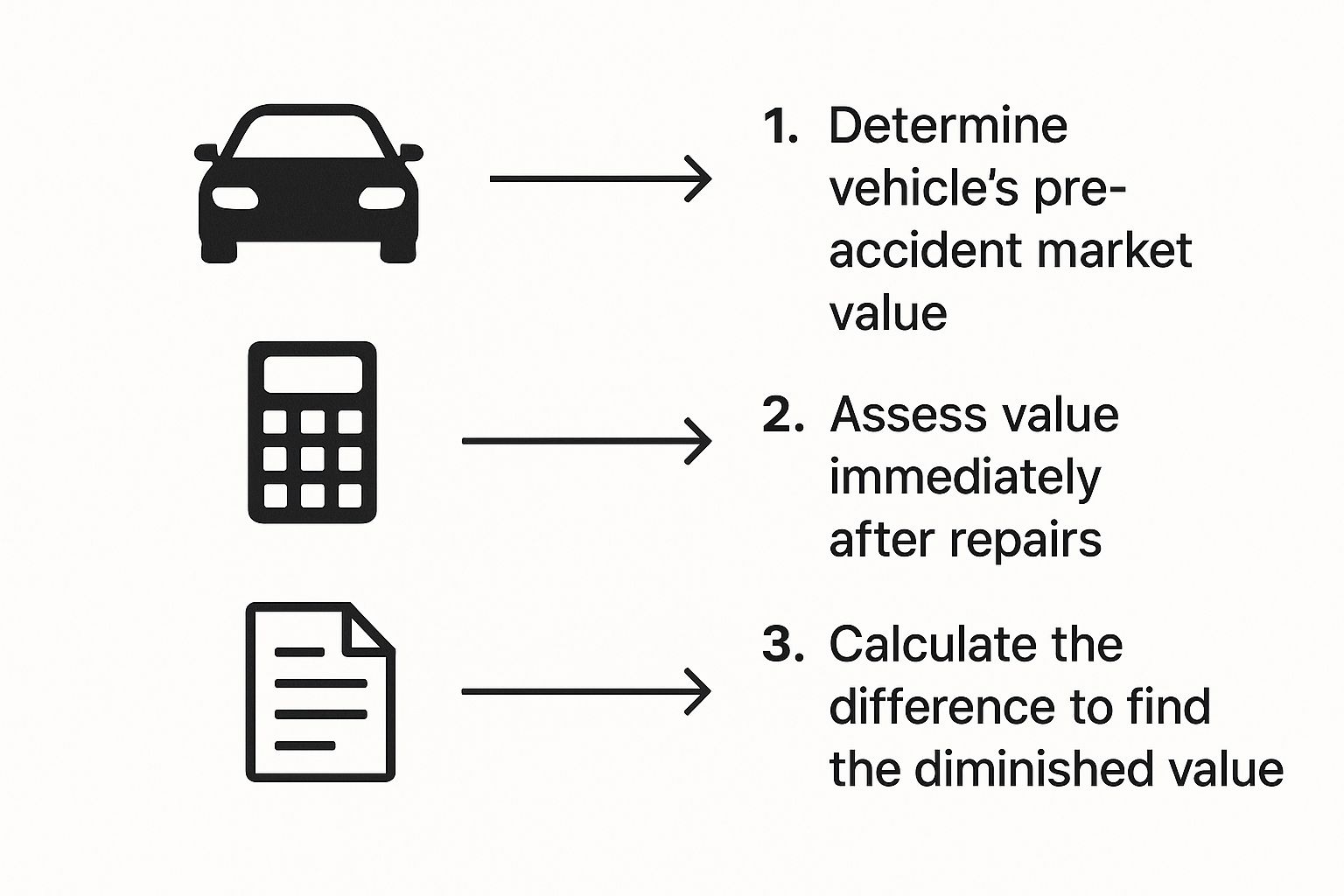

This simple graphic breaks down the core calculation at the heart of your claim.

As you can see, diminished value isn't some arbitrary number. It’s a specific financial loss calculated by subtracting the car's post-repair market value from what it was worth moments before the collision.

The Cornerstone of Your Claim: The Independent Appraisal

While all those other documents are crucial supporting evidence, the independent diminished value appraisal is the undisputed star of the show. It is the single most important document you will submit. The insurance company's own valuation will almost always favor them, often using flawed formulas like 17c that spit out insultingly low numbers.

Getting an independent appraisal from a certified expert provides an unbiased, market-based assessment of your actual loss. It’s a detailed report from a professional who lives and breathes vehicle valuation.

A truly credible appraisal report will always include:

- Vehicle Information: A deep dive into your vehicle—year, make, model, trim, options, and its documented pre-accident condition.

- Market Analysis: A real-world comparison of your vehicle to similar ones on the market, establishing its fair market value before the accident.

- Damage Assessment: A thorough review of the repair orders to understand the severity of the damage.

- Final Valuation: A clear, calculated diminished value figure, backed by professional logic and industry standards.

Submitting a claim without a professional appraisal is like showing up to court without a lawyer. You’re putting yourself at a massive disadvantage. An adjuster can easily brush off your personal opinion, but they can't so easily dismiss a detailed report from a certified professional. It forces them to negotiate based on facts, not their own self-serving formulas.

How to Write a Demand Letter That Gets Results

You’ve done the legwork. You have your appraisal and all your documents lined up. Now it's time to formally ask for your money. This is done with a diminished value demand letter, and it’s the most critical piece of communication you'll send.

This letter isn’t just a simple note asking for a check. It’s a professional, evidence-backed document that methodically lays out your case, presents the facts, and states exactly what you’re owed. Think of it as the opening argument in your negotiation.

A powerful, well-organized letter tells the insurance adjuster you're serious and have done your homework. A sloppy or emotional one, on the other hand, is an easy excuse for them to dismiss your claim. Your goal is to be firm, factual, and completely impossible to ignore.

The Essential Components of Your Letter

Your demand letter needs to be clean and logical. Forget long, rambling paragraphs; get straight to the point. Every section should build on the last, guiding the adjuster to the only reasonable conclusion: your claim is valid and your requested amount is fair.

Make sure these key ingredients are front and center:

- Your Information and Claim Details: Start with the basics—your full name, address, and the date. But most importantly, include the insurance claim number, the date of the accident, and the name of the at-fault driver. This gets your file pulled up instantly.

- A Clear Statement of Purpose: Your very first sentence should be direct. State that this letter is a formal demand for compensation for your vehicle's inherent diminished value caused by the collision. No fluff.

- A Brief, Factual Accident Summary: A quick recap of what happened is all you need. Who, what, where, and when. You aren't rewriting the police report, just providing a sentence or two to establish the facts and confirm their insured's liability.

- The Demand for a Specific Amount: This is the heart of the letter. Clearly state the exact dollar amount of diminished value you are demanding. Crucially, you need to reference your independent appraisal report as the source for this number.

A common mistake I see is people sounding apologetic or unsure in their writing. Your language needs to be confident and assertive, but not aggressive. You aren't asking for a favor—you're demanding rightful compensation for a documented financial loss.

Phrasing That Presents a Logical Argument

The words you choose really matter. You want to present your case as a logical, fact-based conclusion, not an emotional plea. This approach makes it much harder for an adjuster to poke holes in your argument. For a deeper dive into crafting the perfect message, our guide on how to write a powerful insurance demand letter has even more examples and strategies.

For instance, don't say, "I feel my car is worth less now." That’s an opinion. Instead, use authoritative language backed by your evidence.

Here’s how to phrase it effectively:

"The enclosed certified appraisal from a licensed and independent auto appraiser has determined the inherent diminished value to be $4,750. This figure represents the permanent loss of market value my vehicle sustained as a direct result of the collision caused by your insured."

See the difference? This sentence states the exact amount, cites a professional source (your appraisal), and legally connects the financial loss directly to their client's actions. It turns your "feeling" into a documented, hard-to-refute fact.

The Final Steps: Submission and Proof

Once your letter is polished and ready, gather copies of your supporting documents—never send the originals! This includes your appraisal report, the final repair invoice, and the police report.

Now, you have to send it the right way. Don't just pop it in a mailbox or fire off an email.

You must send your complete demand letter package via Certified Mail with a return receipt requested.

This step is absolutely non-negotiable. Certified Mail gives you a legal paper trail with a tracking number, proving you sent it. The return receipt is a physical postcard that the insurance company signs and mails back to you. This is your undeniable proof they received your demand.

Taking this one simple step shuts down the all-too-common adjuster excuse of, "I never received your letter," which is often used to create delays. It signals you're a professional who is serious about pursuing this claim through all necessary channels.

Negotiating with Insurance Adjusters Like a Pro

Alright, you’ve gathered your evidence and sent your demand letter. Now comes the part that can feel intimidating: the negotiation. This is where the rubber meets the road, but don't sweat it. You've done the prep work. You have the facts, the documents, and a professional appraisal in your corner.

Expect the insurance adjuster’s first response to be a quick dismissal or a ridiculously low offer. This is completely normal, so don't let it throw you. It’s their standard opening play. Their job is to pay out as little as possible, and most people they deal with are unprepared. Your professional approach and solid evidence will make you stand out immediately.

Understanding the Adjuster's Playbook

Insurance adjusters are trained negotiators. They have a playbook of tactics designed to make you second-guess your claim or just give up. Knowing what to expect is the best way to stay one step ahead.

One of the most common things you'll hear about is a flawed calculation called the "17c formula." This is a completely arbitrary formula created by insurers to produce an insultingly low number. It usually starts by capping the loss at 10% of the car's pre-accident value and then hits it with vague "modifiers" for damage and mileage to slash it even further.

When an adjuster brings up the 17c formula, your response should be simple and direct.

"The 17c formula is just an internal tool created by insurance companies and has no real standing in the marketplace. My claim is based on a certified, independent appraisal using real-world market data, which is the industry standard for determining fair market value."

This kind of response immediately shuts down their flawed logic and pulls the conversation back to your credible evidence. You're not just arguing; you're explaining why their method is irrelevant and why yours is the correct one. For more in-depth strategies, our complete guide on how to negotiate a diminished value claim has a ton of extra talking points.

Managing Communication and Staying in Control

How you communicate is just as important as what you say. Your main goal is to create a clear, documented paper trail of every single interaction. This keeps the adjuster accountable and protects you.

- Follow Up Every Call with an Email: After you hang up the phone, send a quick email summarizing the conversation. Something like: "Per our call today, you offered $500 for my diminished value claim. As I mentioned, this offer is unacceptable as it doesn't reflect the documented loss of $4,500 detailed in my appraisal."

- Stay Professional and Calm: Emotion is the adjuster's best friend. Getting angry or frustrated only works against you and can damage your credibility. Let the facts of your case—the appraisal and the repair invoices—do the talking for you.

- Never, Ever Accept the First Offer: The first offer is a test. It’s designed to see if you'll go away cheaply. A polite but firm "no" is all you need to say.

It also helps to know what's happening in the broader auto insurance world. In the U.S., things like falling used car values and more complex vehicle repairs have led to a 1% year-over-year increase in total loss claims. At the same time, insurance deductibles have shot up by 47% between 2019 and 2024. This makes people focus more on getting every dollar they're owed, especially from claims like diminished value. Keeping these trends in mind—from depreciation rates to the changing insurance landscape—makes your claim stronger and more relevant. You can find more insights on these insurance industry trends on cccis.com.

Countering Low Offers with Evidence

When the adjuster comes back with a lowball offer, your job is to calmly dismantle their reasoning with your documentation. Don't just say, "That’s not enough." Point back to your evidence to show them why.

Here's a real-world example of how that conversation might go:

Adjuster: "We've reviewed your claim and we can offer you $800 for your diminished value."

Your Response: "Thanks for the offer, but it doesn't line up with the market evidence. My certified appraisal puts the loss at $4,200. The repair invoice shows over $9,000 in damages, including structural frame alignment and replacing three major body panels. A car with that level of documented structural repair always takes a significant hit on its resale value, which my appraiser professionally calculated. Can you please show me the specific market data you used to get to your $800 figure?"

This response does three powerful things:

- It firmly rejects their offer without being emotional.

- It re-anchors the negotiation back to your solid number.

- It puts the ball in their court to justify their low offer with facts—which they usually can't do.

By constantly steering the conversation back to your independent appraisal and the specific, ugly details of the repair, you stay in control. You're turning what could be a stressful argument into a structured, evidence-based discussion where your position is clearly the stronger one.

What to Do When the Insurance Company Won’t Budge

So, you’ve built a rock-solid case with all the right documents, but the insurance adjuster is playing hardball. It’s a frustratingly common scenario, but it’s definitely not the end of the line. Knowing how to push back is the key to getting what you're owed.

When an insurer stalls, lowballs you without a good reason, or flat-out denies your claim, they might be operating in bad faith. These are huge red flags. Don't give up—this is when you need to escalate.

Your First Move: File a Complaint with the Department of Insurance

Before you even think about lawyers, there's a powerful and free tool at your disposal: your state's Department of Insurance (DOI). This is the government body that regulates insurers and protects people like you from unfair practices.

Filing a complaint officially puts the insurance company on notice. Once you file, they are legally required to respond directly to the DOI, which usually means a senior-level claims manager gets involved. Suddenly, they have a strong incentive to resolve your claim fairly to avoid regulatory trouble.

To make your complaint effective, be ready with all your paperwork:

- The police report showing the other driver was at fault.

- Your independent diminished value appraisal.

- A copy of your demand letter.

- Records of every call and email with the adjuster.

This simple step can often break the deadlock without costing you a dime.

Next Up: Small Claims Court

If the DOI complaint doesn’t get you a fair offer, your next stop is small claims court. This is exactly what it's designed for—letting regular people resolve financial disputes without the headache and cost of a major lawsuit.

The monetary limits for small claims court vary by state but typically range from $5,000 to $25,000, which is more than enough to cover most diminished value claims.

The process is straightforward. You'll file a simple form, pay a small filing fee, and then have the insurance company served. In court, a judge will review your evidence—and this is where your professional appraisal report and organized documents become incredibly convincing.

I've seen it happen time and again: just filing the lawsuit is enough to get the insurer’s attention. Their legal team knows that going to court is a hassle, and they’ll often come back with a much better offer once they see you’re serious.

Knowing When to Call a Lawyer

While you can absolutely handle the DOI and small claims court on your own, some situations really do call for an attorney. If your claim involves a high-end luxury vehicle, a classic car, or if you were also seriously injured in the accident, it’s time to bring in a professional.

A lawyer who specializes in diminished value claims will take over all the negotiations and legal filings. They work on a contingency fee, which means they only get paid if you do, taking a percentage of the settlement. There are no upfront costs to you.

The claims process is always evolving. Experts see a future where technology helps streamline these negotiations, making it faster to get paid. You can learn more about the future of diminished value claims and AI on appraisalengine.com. But for now, knowing when to escalate—and when to call in a pro—is your most effective strategy.

Common Questions on Diminished Value Claims

Even with a solid game plan, you're bound to have questions as you navigate your diminished value claim. Let's walk through some of the most frequent ones I hear to clear things up and get you moving forward with confidence.

Can I File a Diminished Value Claim in Any State?

The short answer is: almost always, yes—if you're filing against the other driver's insurance. Nearly every state allows you to pursue a third-party claim against the at-fault driver’s policy. The logic is simple: their driver caused your financial loss, so their insurance is on the hook.

Where it gets complicated is with first-party claims, which are claims you file against your own insurance company. Most states don't allow this. Georgia is a notable exception, letting you file a first-party claim, but usually only if the at-fault driver was uninsured. For a deeper dive, our guide to understanding diminished value after an accident has more specifics.

Because state laws can be nuanced, I always recommend a quick check with your state’s Department of Insurance to confirm the latest rules.

Will Filing This Claim Raise My Insurance Rates?

This is a big one, and it’s a valid concern. But I can tell you definitively: no. Filing a diminished value claim against the at-fault driver's insurance will not raise your rates.

Insurance rate hikes are triggered when you cause an accident. This claim isn't that. You're simply recovering a financial loss caused by someone else's mistake, so your insurance company isn't even involved in the payment. You're just holding the other party's insurer accountable for all the damage they caused.

Think of it this way: The at-fault driver's policy is responsible for making you "whole" again. That includes both repairing your vehicle and compensating you for the permanent loss in its market value. Your policy is not part of that equation.

What if My Car Is Leased or Still Has a Loan on It?

You can, and absolutely should, file a claim even if you're leasing or financing. The loss in your car's value is a real hit to its equity, and that impacts you directly, regardless of who technically holds the title.

Here’s how it breaks down:

- For Financed Vehicles: That diminished value check helps you fight back against the negative equity an accident creates. Suddenly owing more on your loan than your wrecked-and-repaired car is actually worth is a tough spot to be in. The settlement you recover helps close that gap.

- For Leased Vehicles: Remember that lease agreement? You're on the hook for the car's condition when you turn it back in. An accident on its record almost guarantees you'll face penalties and excess wear-and-tear fees from the leasing company. That diminished value payment gives you the cash to cover those charges so you aren't blindsided later.

Don't let a loan or lease agreement scare you off. The financial damage is yours, and you have the right to recover it.

Navigating the world of diminished value can feel like an uphill battle, but you don't have to go it alone. If you're getting stonewalled by an adjuster or just need a rock-solid appraisal to prove your loss, Total Loss Northwest is here to help. We specialize in expert, independent auto appraisals that give you the leverage to get the fair settlement you deserve. Visit us online to get started.