Let's face it, we all assume the other driver on the road has insurance. But what happens when they don't, and they're the one who hits you? That’s exactly where Uninsured Motorist (UM) coverage comes in.

Think of it as your own insurance policy stepping up to the plate to cover your expenses when the person at fault can't. It's your financial backstop against irresponsible drivers.

What Uninsured Motorist Coverage Really Means

Picture this: you're stopped at a red light, and suddenly, you're rear-ended. The other driver is clearly at fault, but they have no insurance. Without UM coverage, you'd be stuck footing the bill for your medical treatments and car repairs, a potentially devastating financial blow.

This coverage ensures you aren't left holding the bag for someone else's mistake. It’s a crucial part of the bigger picture of understanding auto insurance and building a policy that truly protects you.

The Two Main Types of Uninsured Motorist Coverage

Most UM policies are split into two distinct parts, each designed to handle different types of damage.

Here's a quick look at how the coverage breaks down.

| Uninsured Motorist Coverage at a Glance | |

|---|---|

| Coverage Type | What It Covers |

| Uninsured Motorist Bodily Injury (UMBI) | Helps pay for your medical bills, lost income if you can't work, and even pain and suffering for you and your passengers. |

| Uninsured Motorist Property Damage (UMPD) | Covers the repair or replacement costs for your vehicle if it's damaged by an uninsured driver. |

This table gives you a basic idea, but each component plays a critical role in your financial recovery after an accident.

Uninsured Motorist Bodily Injury (UMBI)

If you or your passengers are injured by a driver with no insurance, UMBI is what kicks in to cover the human cost. It helps with:

- Medical expenses, from the ambulance ride to physical therapy.

- Lost wages if you’re unable to work while recovering.

- Compensation for pain and suffering.

Uninsured Motorist Property Damage (UMPD)

While your physical well-being is the top priority, your car is important too. UMPD is there to handle the costs of getting your vehicle back on the road. It specifically covers the repairs or replacement of your car after a collision with an uninsured driver. In some states, this might overlap with or be handled by your standard collision coverage.

The scary part is just how many drivers take this risk.

More than one in seven drivers on U.S. roads might be uninsured, creating a massive gamble for everyone who follows the rules.

This isn't just a "what if"—it's a real and growing problem. A 2025 study found that approximately 15.4% of American drivers were uninsured in 2023. That number has been on the rise since 2017, making UM coverage less of a luxury and more of a necessity.

What Happens After an Accident with an Uninsured Driver?

Let's play out a scenario that’s all too common. You’re stopped at a red light, and suddenly, you feel a jolt from behind. The other driver is at fault, but when you exchange information, they drop the bomb: they have no insurance.

This is exactly where your uninsured motorist coverage springs into action. Instead of facing the nightmare of trying to sue the other driver personally—a process that can drag on for months or years with no guarantee of payment—you can turn to your own insurance policy for help.

First things first, after any accident, your priority is safety. Check for injuries, call 911 if needed, and file a police report. That report is a crucial piece of evidence. It officially documents what happened, who was at fault, and most importantly, confirms that the other driver was uninsured. Trying to file a claim without one can be an uphill battle.

Once the dust settles, you'll call your own insurance agent and let them know you need to open a claim under your uninsured motorist (UM) coverage.

Walking Through the Claim Process

Think of it this way: your insurance company essentially stands in for the insurance company the other driver should have had. While every claim is a bit different, they generally follow a similar path.

- Report the Incident: Let your insurer know you were in an accident with an uninsured driver. Have that police report number handy, as they'll need it to verify the details.

- Keep Meticulous Records: This is huge. Start a file and hang on to everything related to the accident. We're talking medical bills, receipts for prescriptions, physical therapy invoices—all of it.

- Document Lost Income: If your injuries keep you out of work, you’ll need to prove it. Keep track of the days you missed and get a letter from your employer confirming your rate of pay and lost wages.

- Handle Vehicle Repairs: For the damage to your car, your Uninsured Motorist Property Damage (UMPD) coverage (if you have it) or your collision coverage would be used to pay for the repairs.

Your UM coverage is there to cover these losses, paying out up to the policy limits you chose when you bought it.

Uninsured vs. Underinsured: A Critical Distinction

People often confuse Uninsured Motorist (UM) coverage with its cousin, Underinsured Motorist (UIM) coverage. They sound similar and are often sold together, but they tackle two very different—and equally frustrating—problems.

Uninsured Motorist (UM): Kicks in when the at-fault driver has zero insurance.

Underinsured Motorist (UIM): Kicks in when the at-fault driver has insurance, but their policy limits are not high enough to cover your bills.

Here’s a real-world example. Imagine your medical expenses and lost wages total $75,000. The driver who hit you has insurance, but only the state minimum of $25,000. Their insurance pays out the full $25,000, but you're still left with a $50,000 gap. This is precisely where your UIM coverage would step in to help cover the rest, protecting you from a major financial hit.

The Hidden Costs of Uninsured Drivers

Ever look at your auto insurance bill and wonder why it keeps creeping up, even though you haven't had so much as a parking ticket? A big piece of that puzzle is the surprising number of uninsured drivers out there on the road with you every single day.

This isn't some far-off problem; it hits you directly in the wallet. The whole idea of insurance is based on a concept called risk pooling. Think of it as a giant community fund where all the premiums from insured drivers go, ready to pay out when someone has an accident.

But when a driver with no insurance causes a crash, they have no insurance company to tap into. The money to fix your car and cover your injuries has to come from somewhere. That "somewhere" is often your own insurance company, which drains that shared pool and ultimately raises rates for everyone who is playing by the rules.

The Ripple Effect on Your Premiums

It’s a simple economic reality: when times are tough, more people gamble by driving without insurance. In 2022, a staggering 14% of U.S. drivers were uninsured. In some states, that number jumps to nearly one in four drivers on the road. This isn't just a statistic; it's a financial risk you face every time you get behind the wheel.

This is why having uninsured motorist coverage is less of a luxury and more of a necessity. It’s not just about one potential accident; it's your personal defense against a widespread problem that can seriously threaten your financial health.

Your uninsured motorist coverage acts as a firewall, shielding your finances from the irresponsible choices of others and ensuring one accident doesn't derail your financial future.

Protecting Your Vehicle's Value

Getting your car repaired is only half the battle. After an accident, even with perfect repairs, your car's resale value takes a nosedive. This drop in market value is called diminished value, and it's a very real loss. When the at-fault driver is uninsured, figuring out how to file a diminished value claim becomes absolutely critical to getting back the money you've lost.

This is where the true value of UM coverage really shines. It's designed to step in and fill the gaps when the other driver can't, making sure you aren't stuck paying for:

- Your own medical bills after an accident that wasn't your fault.

- Lost wages if you're injured and can't work.

- Vehicle repairs that would otherwise have to be paid out of your own pocket.

Navigating Your State's UM Coverage Rules

When it comes to uninsured motorist coverage, there isn’t a one-size-fits-all rule. What’s required in one state can be completely different just a few miles down the road. This patchwork of laws can feel confusing, but it really boils down to three main approaches states take.

Some states make uninsured motorist (UM) coverage mandatory. They’ve looked at the numbers and decided the risk of getting hit by an uninsured driver is high enough to require everyone to carry this protection. Then you have states where UM coverage is optional, but insurers must offer it to you. This is a common setup, and if you decide against it, you usually have to formally reject it in writing.

Finally, a handful of states leave the decision entirely in your hands, with no specific requirements at all.

Why Your Local Rules Matter

Understanding your state's approach is more than just a legal box to check—it’s a direct reflection of the risk you face every time you get behind the wheel. The stricter the rules, the more likely it is that there's a significant problem with uninsured drivers in that area.

While car insurance is a global industry, the need for this specific coverage is intensely local. For instance, in 2022, Washington D.C. had a staggering 25% of its drivers on the road without insurance. Compare that to states like Wyoming and Maine, where the rate hovered around a much lower 6%. If you're curious about how these numbers influence insurance trends, diving into the latest car insurance facts and figures can be pretty eye-opening.

To give you a better idea of how this plays out, let's look at a few examples.

State UM Coverage Requirements and Risk Levels

This table shows how different state requirements often correlate with the percentage of uninsured drivers on the road.

| State Example | Coverage Requirement | Approx. Uninsured Driver Rate |

|---|---|---|

| New York | Mandatory | ~6.1% |

| Florida | Optional (must be offered/rejected) | ~20.4% |

| Virginia | Can pay a fee to drive uninsured | ~10.5% |

As you can see, a state like Florida, where the coverage is optional, has a significantly higher rate of uninsured drivers compared to New York, where it's required. This underscores why knowing your local landscape is so important when deciding on coverage.

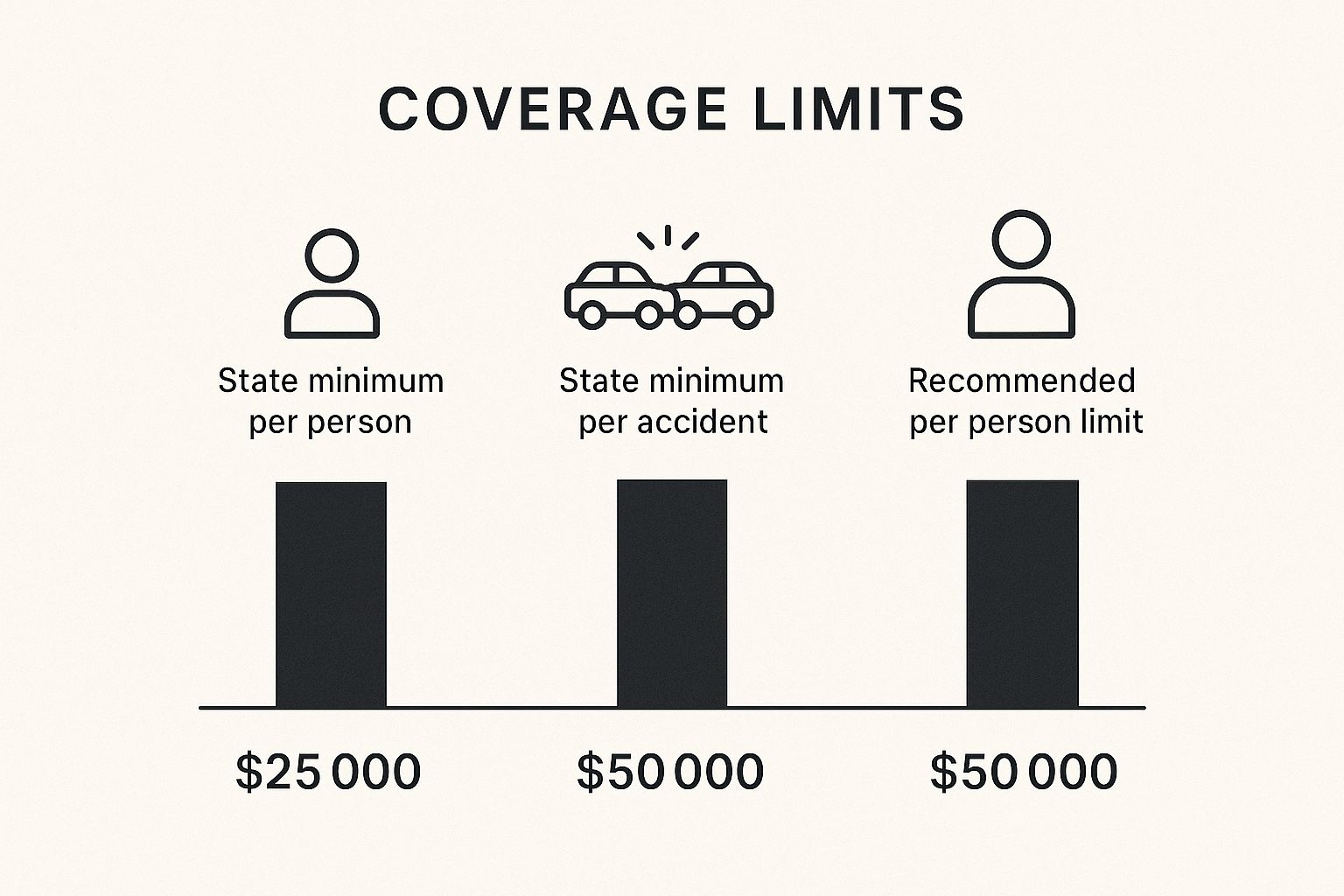

This image really drives home the point that what's legally required is often far less than what you actually need for solid financial protection.

The key takeaway here is that state minimums are just the starting line. Recommended coverage levels are designed to provide a much more realistic safety net against the very real costs of an accident. No matter what your state’s laws say, it’s always a smart move to assess your own risk and make sure you’re truly protected.

Choosing the Right Amount of UM Coverage

Figuring out how much uninsured motorist (UM) coverage to buy can feel a bit like throwing a dart in the dark. But getting this number right is one of the most critical decisions you'll make for your financial security. The right amount isn't arbitrary; it's a safety net designed to protect everything you've worked for if you're in a serious crash with the wrong driver.

A common piece of advice you’ll hear is to match your UM limits to your liability coverage. So, if you have $100,000 in liability protection per person, you should aim for at least $100,000 in UM coverage. This creates a kind of mirror effect—you're giving yourself the same level of protection you're required to give to others. It’s a solid starting point.

Calculating What You Really Need

But just matching your liability limits might not cut it. The best way to land on the right number is to take a quick look at your own financial picture. Ask yourself what would happen if a serious accident took you off your feet for a while.

-

Your Health Insurance: First, what’s your deductible and out-of-pocket maximum? If you have a high-deductible plan, you could be on the hook for thousands of dollars in medical bills right away.

-

Your Income: How much money would your family lose if you couldn't work for weeks or even months? UM coverage is designed to step in and cover that lost income.

-

Your Assets: Think about your savings, investments, and even the equity in your home. The right coverage prevents you from having to drain these accounts just to pay for someone else’s mistake.

Choosing your UM limits is about creating a financial safety net that can withstand the true cost of an accident, not just meeting a minimum requirement.

Remember, the aftermath of an accident brings more than just medical bills and repair costs. For example, understanding diminished value laws is essential because your car's resale value plummets even after a perfect repair job. Your UM coverage needs to be robust enough to handle these hidden financial hits so you can get back on your feet without wiping out your savings.

Common Questions About Uninsured Motorist Coverage

Even when you grasp the basics of uninsured motorist coverage, real-world accidents can bring up tricky questions. Let's walk through some of the most common gray areas so you can feel confident about how this protection really works.

Does UM Coverage Apply to Hit-and-Run Accidents?

Yes, absolutely. In most states, your uninsured motorist coverage is specifically designed to step in after a hit-and-run. Because the at-fault driver fled and can't be identified, they are treated as an uninsured driver for claim purposes.

Your Uninsured Motorist Bodily Injury (UMBI) coverage will help handle medical expenses for you and anyone in your car. When it comes to fixing your vehicle, either your Uninsured Motorist Property Damage (UMPD) or your regular collision coverage would be the part of your policy that applies.

A hit-and-run is one of the clearest examples of why UM coverage is so essential. Without it, you could be left with all the bills from an accident you didn't cause, with no at-fault party to hold accountable.

Is Uninsured Motorist Coverage Worth the Extra Cost?

When you consider that more than one in seven drivers on the road could be uninsured, adding this coverage is one of the smartest, most affordable ways to protect yourself. The small bump in your premium can be the difference between a manageable situation and a financial disaster.

Without it, you're on the hook for every dollar of your medical bills and car repairs. If the driver who hit you has no insurance, they probably don't have many assets either, which means suing them is often a dead-end street. Trying to navigate a total loss settlement negotiation is hard enough; doing it when the other driver is uninsured is a complete nightmare.

What Is the Difference Between Uninsured and Underinsured?

This is probably the most common point of confusion, and the difference is crucial. Insurers often sell these coverages together, but they solve two very distinct problems.

- Uninsured Motorist (UM): This is for when the driver who hits you has no insurance coverage at all.

- Underinsured Motorist (UIM): This kicks in when the at-fault driver does have insurance, but their policy limits are too low to pay for all of your medical bills and damages.

Think of UIM coverage as a safety net that closes the gap between what the other driver's cheap policy pays out and what you actually need to recover.

If you've been in an accident and are facing a lowball settlement offer for your vehicle, Total Loss Northwest is here to help. We are certified appraisers who fight to get you the true market value you're owed. Don't let the insurance company dictate your settlement—visit us online to ensure you get a fair and accurate appraisal.