When people talk about auto insurance, you often hear terms like "liability" and "collision." But there's another crucial piece of the puzzle: comprehensive insurance. So, what is it?

Think of comprehensive coverage, sometimes just called "comp," as your car's safety net for just about everything except a collision. It’s the coverage that steps in to handle the unpredictable curveballs life throws your way—things like theft, a rogue shopping cart on a windy day, a hailstorm, or even a tree branch falling on your hood.

Essentially, it protects your vehicle from damage that happens when you're not even driving.

Breaking Down Comprehensive Insurance Coverage

Let's use an analogy. If your auto policy is a toolkit, liability coverage is the tool you use to fix the damage you cause to others. Collision coverage is the one that repairs your car after you hit another vehicle or an object, like a fence post.

So, where does comprehensive fit in? It's the multi-tool that handles almost all the other "non-driving" mishaps. It’s for the stuff that's completely out of your hands.

This type of coverage is a cornerstone of the Property and Casualty (P&C) insurance world. And it's a big deal—the global P&C market is expected to grow by EUR 1,522 billion in premiums over the next ten years. In the U.S. alone, total P&C premiums are projected to top EUR 1,800 billion by 2035. If you're interested in the numbers, you can dig into the global insurance trend data from Allianz Research.

The Core Purpose of Comprehensive

At its heart, comprehensive insurance is all about protecting your investment—your car—from random acts of chaos. It's there to make sure you aren't stuck footing a huge repair bill (or worse, the full cost of a new car) because of something you had no way of preventing.

The real value of comprehensive coverage lies in the peace of mind it provides. It’s the assurance that your investment is protected from the everyday risks that have nothing to do with your driving skills.

To simplify things, here’s a quick snapshot of what comprehensive coverage is all about.

Comprehensive Coverage at a Glance

This table breaks down the essentials of comprehensive insurance, giving you a clear picture of its role in your auto policy.

| Coverage Aspect | Brief Explanation |

|---|---|

| Main Function | Covers damage to your car from non-collision events. |

| Key Covered Perils | Theft, vandalism, fire, natural disasters, falling objects, animal collisions. |

| Typical Requirement | Often required by lenders for financed or leased vehicles. |

| Primary Benefit | Protects your car's value against unpredictable loss. |

Understanding this foundation makes it much easier to see how comprehensive stands apart from other coverages. While liability and collision are all about accidents, comprehensive is your shield against the rest of life's unexpected troubles.

What Comprehensive Insurance Actually Covers

The best way to get a feel for comprehensive coverage is to think about real-life situations. Forget the technical jargon for a moment. This is your financial safety net for all the weird, random, "other-than-collision" stuff that can happen to your car.

It’s protection for when life just… happens. Imagine waking up to find someone keyed your door overnight or smashed a window. Or picture a surprise hailstorm leaving your car looking like a golf ball. These are exactly the kinds of headaches comprehensive insurance is designed to handle.

Common Events Covered by Comprehensive Insurance

Let's dig into the specific scenarios where this coverage really shines. You'll notice a theme: none of these involve a typical crash with another car.

- Theft and Vandalism: Your car gets stolen and isn't found, or a thief breaks a window to get inside. This is classic comprehensive territory.

- Weather and Natural Disasters: Think hail, floods, windstorms, and even lightning strikes. If Mother Nature messes with your car, this is the policy that responds.

- Falling Objects: That massive tree branch that snapped off during a storm and landed on your roof? Covered. Debris falling from an overpass? Covered.

- Fire and Explosions: Whether it’s an engine fire or something external, comprehensive insurance is what helps you recover from the damage.

- Animal Collisions: Hitting a deer on a back road is a surprisingly frequent and costly event. It’s not a "collision" in insurance terms; it's a comprehensive claim.

Nature's Unpredictable Impact

With severe weather on the rise, the value of comprehensive coverage has never been clearer. There's a huge gap between the total economic damage from natural disasters and what's actually insured.

Between 2014 and 2023, global economic losses from these events hit nearly US$2.35 trillion, but insured losses were only about US$944 billion. That leaves a staggering 60% protection gap. It’s a powerful reminder of why having the right coverage matters.

A comprehensive claim almost always feels like a bolt from the blue. Your car is fine one minute, and the next, a completely random event leaves you facing a huge repair bill. That's the whole point of this coverage—to absorb the financial shock of the unexpected.

If one of these events is severe enough to total your car, you'll need to navigate the claims process carefully. It really helps to understand the total loss appraisal process so you can be sure you're getting a fair settlement. A big part of that is knowing https://totallossnw.com/what-is-actual-cash-value-of-my-car/ and how your insurer calculates it.

Understanding What Your Policy Excludes

While comprehensive coverage is incredibly broad, knowing its limits is just as important as knowing what it covers. You don't want to be caught off guard when you file a claim, only to discover something isn't included.

Think of it like this: comprehensive insurance is your car's protection against the unexpected chaos of the world—things that happen to your car, not things that happen because you're driving it.

The biggest and most important exclusion to remember is that comprehensive does not cover collision damage. If you run into another vehicle, a mailbox, or a guardrail, that’s a job for collision coverage, not comprehensive. They are two separate parts of your policy designed for completely different scenarios.

Likewise, this coverage is for sudden, accidental events, not the slow march of time. Normal wear and tear, like your tires getting thin or your paint fading, isn't covered. Mechanical breakdowns, like a failing transmission or a bad alternator, are also outside the scope of comprehensive insurance.

What Is Not Covered By Comprehensive Insurance

Let's get specific. Knowing these common exclusions ahead of time can save you a lot of frustration down the road.

-

Personal Belongings: Imagine a thief smashes your car window. Comprehensive coverage will absolutely pay to replace the broken glass. However, it won't cover the laptop or gym bag they stole from your back seat. Those items fall under your homeowners or renters insurance policy.

-

Custom Parts and Equipment: Did you upgrade your ride with some pricey custom rims or a booming sound system? Your standard policy is designed to cover the car as it came from the factory. To protect those aftermarket additions, you’ll need to add a special endorsement to your policy.

-

Diminished Value: After an accident and repairs, your car is often worth less than it was before, simply because it now has an accident history. This loss in resale value is called diminished value, and it's almost never covered by a standard policy. Understanding the nuances of diminished value laws and how they affect your claim is key if you find yourself in this situation.

Your Out-of-Pocket Cost: The Deductible

One last crucial piece of the puzzle is your deductible. This is the amount you agree to pay out of your own pocket for a claim before your insurance company starts paying.

Think of your deductible as your share of the repair cost. If a hailstorm causes $2,500 in damage to your car and you have a $500 deductible, you pay the first $500. Your insurer then picks up the remaining $2,000.

Choosing a higher deductible, like $1,000 instead of $500, will usually lower your monthly premium. But it also means you're on the hook for a bigger chunk of the cost if something happens. It’s a classic trade-off between saving money now and potentially paying more later.

Decoding Comprehensive, Collision, and Liability

Trying to make sense of an auto insurance policy can feel like you’re reading a foreign language. You see words like comprehensive, collision, and liability thrown around, and it's easy for them all to just blur together. But each one has a very specific, very important job to do when it comes to protecting you and your finances.

Think of your car insurance policy as a team of specialists. You wouldn't ask a plumber to fix your wiring, and you wouldn't want your collision coverage to handle a hailstorm. Each part of your policy is designed for a specific type of problem, and understanding their roles is key to making sure you don't have a surprise gap in your protection when you need it most.

Let's break them down, one by one.

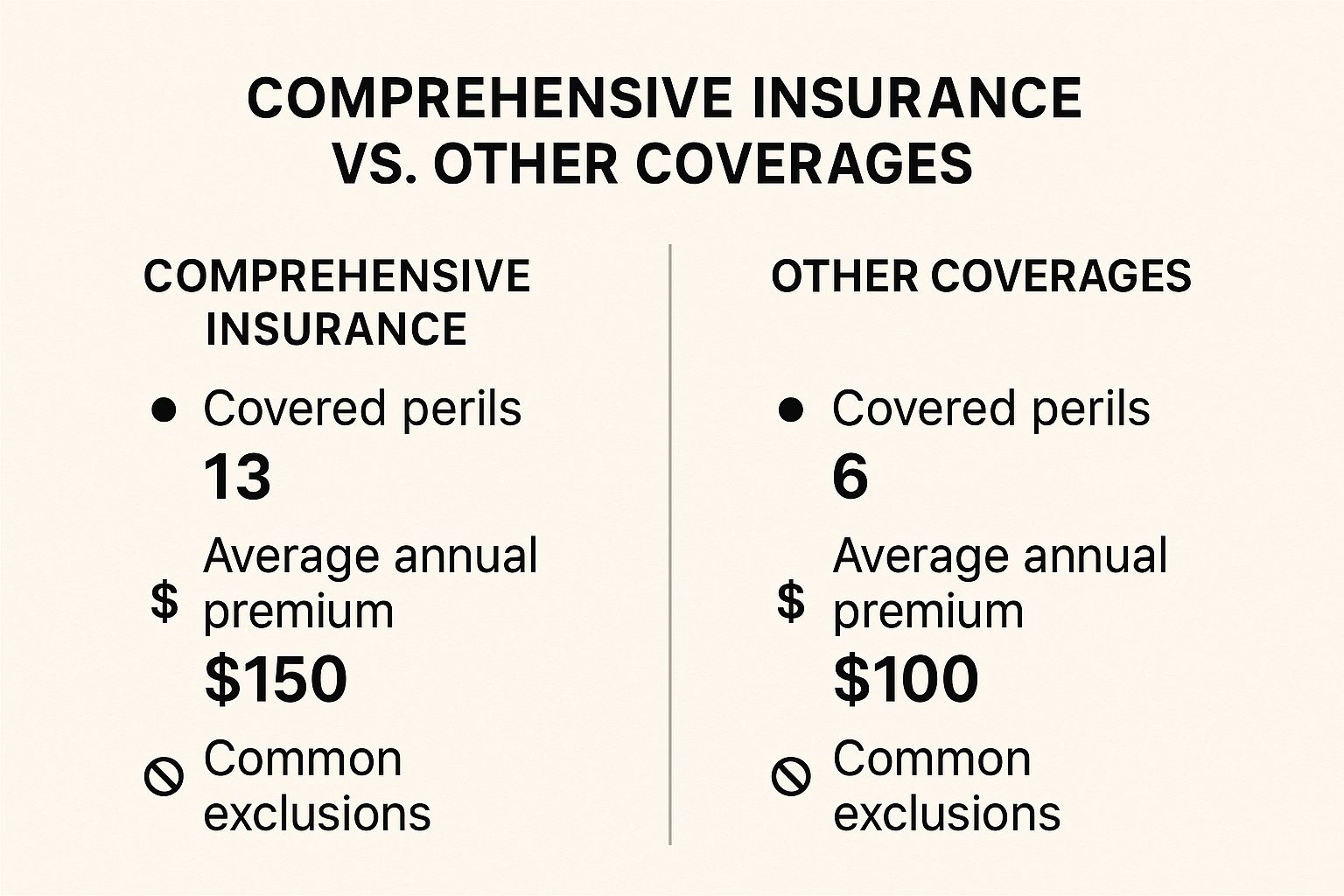

The image below gives you a quick snapshot of how these coverages differ, especially when it comes to the specific events they cover, how they impact your wallet, and what they don't cover.

As you can see, comprehensive coverage is your go-to for a lot of non-crash incidents, but it's only one piece of the puzzle.

The Three Pillars of Auto Coverage

The best way to get a grip on what is comprehensive insurance coverage is to see how it stands next to the other major players.

-

Liability Insurance: This is the absolute bedrock of any policy and it’s required by law in almost every state. Its job is straightforward: it pays for the damage you cause to other people or their property. If you're at fault in an accident, your liability coverage handles the other driver's medical bills and car repairs. It does nothing for your own car or your own injuries.

-

Collision Insurance: This one is all about your car. It pays to fix or replace your vehicle after it's damaged in a crash, whether you hit another car, a pole, or a guardrail. It kicks in regardless of who was at fault in the accident.

-

Comprehensive Insurance: Think of this as your "life happens" coverage. It steps in to cover damage to your car from almost everything other than a collision. We're talking about things like theft, vandalism, fire, falling trees, hailstorms, and hitting a deer.

Here's a simple way to keep them straight: Ask yourself, "What damaged the car?" If your car hit something, that’s a job for collision. If you hit someone or something and caused damage, that’s liability. If something else entirely—like a thief or a storm—damaged your car, that’s almost always comprehensive.

Comprehensive vs. Collision vs. Liability: A Side-by-Side Comparison

Putting these three coverages in a direct comparison really makes their distinct roles click. The table below lays it all out, showing exactly what each one covers, its main purpose, and whether it's typically required.

| Coverage Type | What It Covers | Primary Purpose | Is It Required? |

|---|---|---|---|

| Liability | Bodily injury and property damage you cause to others. | To protect others from your actions and fulfill legal requirements. | Yes, by state law (in nearly all states). |

| Collision | Damage to your own vehicle from a crash with another car or object. | To repair or replace your car after an accident you are involved in. | No, by law. Yes, usually by a lender if you have a loan or lease. |

| Comprehensive | Damage to your own vehicle from non-collision events like theft, fire, or weather. | To protect your investment from unpredictable, external events. | No, by law. Yes, usually by a lender if you have a loan or lease. |

At the end of the day, these coverages aren't competing against each other—they're designed to work together as a team. Liability protects your assets from lawsuits, while collision and comprehensive work in tandem to protect the value of your vehicle itself. When you hear someone talk about having "full coverage," they're usually referring to a policy that includes all three, giving them a strong financial shield against almost anything the road can throw at them.

How Insurers Determine Your Premium Costs

Ever get your insurance bill and wonder, "Where on earth did they get this number?" Calculating your premium for comprehensive coverage isn't just pulling a figure out of thin air. It’s a sophisticated risk assessment, where insurers act a bit like detectives, piecing together clues about you, your car, and your neighborhood to figure out how likely you are to file a claim.

Think of it as your own personal risk score. A shiny new luxury SUV packed with expensive tech will naturally cost more to insure than a 10-year-old sedan. Why? The potential repair and replacement costs are worlds apart. That's one of the biggest pieces of the puzzle.

But what your car is worth is just the beginning.

Key Factors That Influence Your Rate

Insurance companies look at a whole host of factors to build your premium. While each has its own unique formula, the main ingredients are pretty consistent across the board. Knowing what they are helps demystify your bill.

- Your Vehicle's Make and Model: This goes way beyond the sticker price. Insurers dig into theft statistics for certain models, the cost of replacement parts, and the car's safety record. If you drive a car that’s a frequent target for thieves, expect that to be reflected in your rate.

- Your Geographic Location (ZIP Code): Where you live and park your car is a huge deal. If you're in a city with high rates of vandalism and theft, or a region prone to hailstorms and flooding, your comprehensive premium will be higher to account for that increased risk.

- Your Chosen Deductible: This is the amount you agree to pay out-of-pocket before your insurance coverage starts paying. Opting for a higher deductible, say $1,000 instead of $500, tells the insurer you’re willing to shoulder more of the initial cost. In return, they'll almost always lower your premium.

If your car ends up being severely damaged in a covered incident, knowing how the insurer calculates its value is critical. Getting a proper total loss estimate is key to ensuring you get a fair settlement.

Broader Market and Regional Trends

It’s not all about you, though. Big-picture economic forces and regional patterns also have a say in what you pay. For example, trends in the global insurance market can nudge rates up or down for everyone.

In the second quarter of 2025, overall global insurance rates actually dipped by about 4%. But here in the United States, things looked different. Thanks to our significant exposure to natural disasters, many rates stayed flat or even ticked upward for coverages that affect comprehensive insurance costs. It’s a perfect example of how local risk can easily trump global pricing trends. You can dive deeper into these global insurance market dynamics from Marsh.

Ultimately, your comprehensive premium is a reflection of calculated risk. It blends your personal profile with broader environmental and market data to arrive at a price that balances the insurer's potential payout against the coverage you receive.

Is Comprehensive Insurance a Smart Choice for You?

Alright, you understand what comprehensive coverage is, but the big question remains: do you actually need it? There's no one-size-fits-all answer here. It really comes down to weighing the monthly cost against your personal risk.

Making the right call means getting real about your car and your financial situation. A quick self-assessment is the best way to figure out if it’s the right move for you.

Questions to Ask Yourself Before Deciding

Think through these points honestly. Your answers will tell you whether that premium is a smart investment or just an extra bill you don't need to pay.

-

Do you have a car loan or lease? If so, this decision is probably already made for you. Lenders and leasing companies almost universally require you to carry both comprehensive and collision coverage. They need to protect their investment until you’ve paid off the vehicle, plain and simple.

-

What is your car’s actual cash value (ACV)? Is your ride fresh off the lot, or is it an older car with a lot of miles on the clock? A good rule of thumb is to think about dropping comprehensive coverage if the annual premium is more than 10% of your car’s value. For example, if your car is only worth $2,000 and the coverage costs you $250 a year, it might not make much financial sense.

-

Could you afford a major repair or replacement? This is the bottom line. If your car was stolen tomorrow or flattened by a fallen tree, could you come up with the cash to fix it or buy another one without derailing your finances? If the answer is no, comprehensive coverage is your financial safety net.

The decision boils down to a simple trade-off: paying a predictable premium for peace of mind versus accepting the unpredictable risk of a large, sudden expense.

Ultimately, choosing comprehensive insurance is a strategic financial decision. If you own a new, valuable, or financed car, it's pretty much a no-brainer. But if you're driving an older, paid-off vehicle and have a healthy emergency fund, the cost might not be worth the benefit. Weigh these factors carefully, and you can make a confident choice that protects both your car and your wallet.

Answering Your Lingering Questions

Even with the big picture in place, a few common questions always seem to come up. Let's tackle them head-on so you can feel confident about your coverage choices.

Does Comprehensive Cover a Rental Car?

This is a great question, and the answer is typically no—at least not automatically. Comprehensive coverage itself is for damage to your car.

The coverage that helps pay for a rental while your car is in the shop after a claim is a separate, optional add-on often called rental reimbursement. It's usually a small extra cost on your policy, but you have to specifically add it. Always double-check your policy documents or just ask your agent to be sure.

Will a Comprehensive Claim Raise My Rates?

Probably not, but it's not a simple "no." Insurers view comprehensive claims very differently than at-fault accident claims. Since things like hail storms, falling trees, or theft are completely out of your control, a single claim is unlikely to cause a rate hike.

Where you might see an issue is if you file several comprehensive claims in a short period. An insurer might see this pattern as a sign of higher risk and could adjust your premium when it's time to renew. It really comes down to your insurer's specific rules and your claims history.

Key Takeaway: A single comprehensive claim probably won't hurt your rates, but multiple claims might. It's not treated the same as an accident you caused.

Can I Get Comprehensive Without Collision?

Absolutely. In fact, this is a very common strategy for owners of older, paid-off cars.

Think about it this way: if your car's market value is low, paying a hefty premium for collision coverage might not make financial sense anymore. But you still want to be protected if your car gets stolen or a tree branch falls on it. Keeping comprehensive gives you that peace of mind against non-accident events without the higher cost of collision.

Dealing with an insurance company after a major accident or total loss can be a real headache. You just want what's fair, but often the settlement offer feels frustratingly low. At Total Loss Northwest, we step in to make sure you get the true market value for your vehicle. If you're stuck with a lowball offer, our certified independent appraisers can invoke the Appraisal Clause on your behalf to fight for the fair settlement you rightfully deserve. Find out how we can help at https://totallossnw.com.