When your insurance company tells you your car is a total loss, that gut-punch feeling is often quickly followed by a settlement offer that feels way too low. This is the exact moment an auto total loss calculator becomes your best friend. It’s your secret weapon for getting a fair shake.

Think of it as your own independent appraisal. It gives you a data-driven estimate of your vehicle's Actual Cash Value (ACV), which is the number you need before you ever start negotiating with the insurance company. It’s your first line of defense against an undervalued claim.

Why You Need a Total Loss Estimate Before You Talk to the Insurer

Walking into a negotiation with the insurance adjuster without your own numbers is like flying blind. They have their valuation, and you have… what? A feeling? An auto total loss calculator shifts the power dynamic. It gives you a realistic benchmark for your claim, so you can negotiate from a place of confidence, not confusion.

Instead of just taking the first number they throw at you, you’ll have hard evidence to back up your position. This preparation is everything. It’s about doing your homework, a bit like the process of understanding due diligence before any big financial decision. You wouldn't buy a house without an inspection, so why accept an insurance settlement without your own valuation?

Arm Yourself with Data

An independent estimate pulls back the curtain on how valuations actually work. It shows you the same key factors an appraiser looks at: your car’s make, model, year, mileage, overall condition, and—most importantly—what similar cars have recently sold for in your specific area.

Market trends play a huge role here. With the recent spike in both new and used vehicle prices due to supply chain hiccups and inflation, valuations are higher across the board. This also means the threshold for declaring a car a total loss has changed. Damage that might have been repaired a few years ago could easily total a car today.

A data-backed estimate is your leverage. It changes the conversation from, "This is our offer," to, "Here’s what my vehicle is actually worth based on real-time market data."

Take Control of the Negotiation

When you have a solid number, you can build a logical, compelling case for what you're owed. This isn't about getting angry or being difficult; it's about being prepared and professional.

You can calmly walk the adjuster through your report, point to the comparable sales, and explain exactly why their offer falls short. It shows them you've done your research and you're serious. Our guide on getting a professional https://totallossnw.com/total-loss-estimate/ can give you more tips on how to build that case effectively.

Getting Your Ducks in a Row for an Accurate Valuation

The old saying "garbage in, garbage out" is especially true when using a total loss calculator. The final number it spits out is only as reliable as the details you provide. If you're vague, you'll get a vague, easily disputed valuation. To build a rock-solid case that an insurance adjuster has to take seriously, you need to collect the right information.

This is about much more than just the basics like your VIN, make, model, and mileage. You've got to dig into the nitty-gritty details that made your car special. Was it the base model, or did you have the fully-loaded premium trim? That difference alone can mean thousands of dollars. The same goes for factory-installed options—that sunroof, premium sound system, or advanced safety package all need to be accounted for.

Essential Information for Your Total Loss Calculation

To get the most accurate number, you need to gather specific documentation. Think of this as building a complete profile of your vehicle right before the accident.

| Data Category | Specific Information Needed | Why It Matters |

|---|---|---|

| Basic Vehicle Details | VIN, Make, Model, Year, Exact Trim (e.g., LX, EX-L) | Forms the baseline value. The trim level can dramatically alter the starting price. |

| Mileage | Odometer reading at the time of the accident | Mileage is one of the biggest factors in depreciation. An exact number is crucial. |

| Vehicle Condition | Pre-accident photos, detailed notes on interior/exterior | Proves the car was in "good" or "excellent" condition, not just average. |

| Factory Options | Window sticker, original sales documents | Captures the value of sunroofs, navigation, premium wheels, etc. |

| Recent Investments | Receipts for new tires, brakes, battery, etc. | Shows recent money spent that adds tangible value and hasn't had time to depreciate. |

| Maintenance History | Service records from your mechanic or dealership | A complete history demonstrates the vehicle was well-maintained, justifying a higher value. |

Having this information on hand before you even start using a calculator will make the process smoother and the result far more credible.

Proving Your Car’s Condition and Recent Upgrades

Your vehicle's condition right before the crash is a massive piece of the puzzle. This is where your personal records become your best weapon. Don't just click "Good" from a dropdown menu—you have to prove it.

- Service Records: A meticulously kept maintenance log is gold. It shows the adjuster you took great care of the vehicle, which justifies a higher valuation compared to a car with a questionable history.

- Recent Purchases: Did you just drop $1,200 on a set of high-end tires a month before the accident? Or maybe you replaced the battery? Find those receipts. That's real, provable value an adjuster might otherwise ignore.

- Pre-Accident Photos: If you happen to have any photos of your car looking clean and damage-free before the wreck, they are incredibly powerful. They can instantly shut down any attempt to devalue your car by claiming pre-existing wear and tear.

The entire goal here is to remove any ambiguity. You want to give the insurance company zero room to devalue your vehicle based on assumptions. Every receipt, photo, and service record you provide makes your valuation stronger and much harder to dispute.

Think of yourself as an attorney building a case for your car. The more organized and detailed your evidence is, the more precise the calculator's estimate will be. This isn't about guessing what your car was worth—it's about proving it with cold, hard facts.

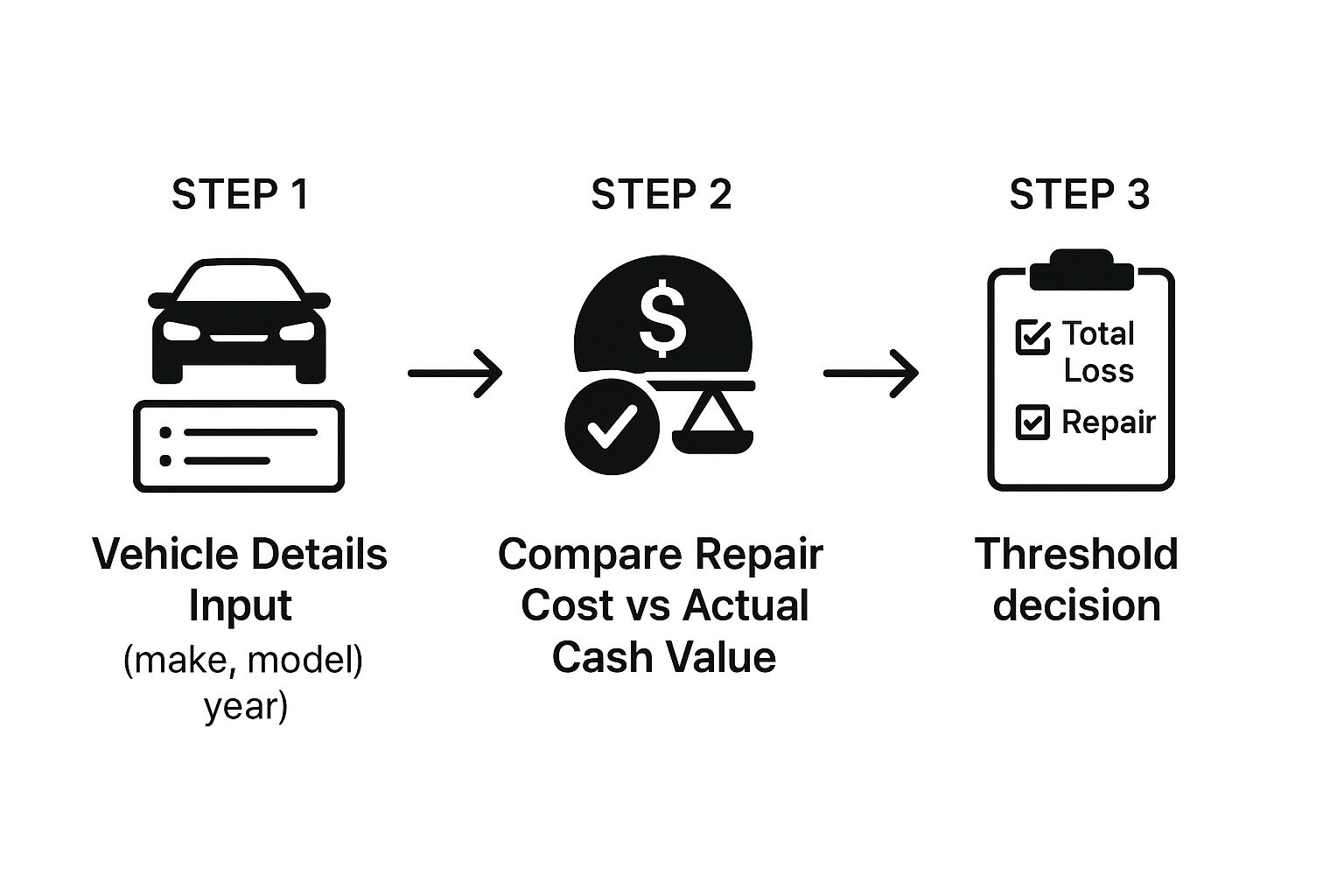

How Insurers Actually Calculate a Total Loss

When an insurance adjuster looks at your damaged car, they aren't just guessing. They're using a specific formula to decide whether to fix it or write it off as a total loss. Getting a handle on this formula is your best defense against a lowball offer.

The entire decision boils down to one simple equation: (Cost of Repairs + Salvage Value) > Actual Cash Value (ACV). If the price to fix your car, plus what they can get for it at a salvage auction, is more than what your car was worth right before the crash, it’s a goner.

What Goes Into the Total Loss Formula?

The number that causes the most arguments in this whole process is the Actual Cash Value (ACV). This isn't just a quick peek at a generic "Blue Book" number. A proper ACV is based on what similar cars have recently sold for right in your local area. They're looking for the same make, model, year, and trim, with comparable mileage and overall condition.

It’s all relative. A newer truck with $15,000 in damage might be an easy "repair" decision if its ACV is $40,000. On the other hand, an older car with an ACV of $7,000 could easily be totaled by just $5,000 in repairs, once you add in its scrap value. For a more detailed look at the math, you can check out our guide on calculating a total loss vehicle.

Don't forget, the insurance company wants to close your claim as cheaply as possible. Your job is to make sure their ACV number reflects what your car was really worth on the market—not just a number that works for their bottom line.

This flowchart gives you a pretty clear picture of the decision-making process from the insurer's perspective.

As you can see, that moment where repair costs are weighed against the car's value is the make-or-break point.

Why Are Repair Costs So High Right Now?

It’s not always just about the visible damage. Global issues can have a massive impact on repair costs, pushing more cars into the "totaled" category. Tariffs on imported auto parts are a perfect example.

Since about 60% of replacement parts in the U.S. come from other countries, these extra costs get passed straight into your repair estimate, making it much easier for a vehicle to hit that total loss threshold.

Knowing the potential repair bill is key. If you want to get a rough idea of what a body shop might charge, a tool like an Automotive Repair Estimator can give you a starting point. This helps you anticipate which way the insurance company might be leaning with your claim.

How to Use Your Results to Negotiate a Better Settlement

Getting an independent estimate from a total loss calculator is a great first step, but it’s just that—a first step. The real work begins when you use that information to build a solid case for a better settlement from the insurance company. This isn't about getting angry or argumentative; it's about having a calm, fact-based conversation with the adjuster.

Your starting point is a side-by-side comparison. Pull up the insurance company's offer and your independent report and go through them line by line. You’re looking for the specific points where they diverge. Maybe they dinged your car's condition, rating it "fair" when all your service records show it was meticulously maintained and easily qualifies as "excellent." Or perhaps the "comparable" vehicles they used to set the price were from a different city where cars just sell for less. These are the gaps you need to close.

Assembling Your Counter-Offer

Once you've spotted the discrepancies, it's time to gather your evidence and put together a professional counter-offer. Simply telling the adjuster their number is too low won't get you far. You have to show them why.

I always advise clients to create a small "negotiation packet." It makes you look organized, serious, and prepared. Here’s what should be in it:

- A Simple Cover Letter: Start with a brief, clear summary. State your proposed settlement figure and explain why your number is more accurate, referencing the documents you’ve included.

- Your Independent Valuation Report: This is your primary piece of evidence. Include the full report.

- Proof of Value: This is where you add everything else that proves your car's worth. Think recent receipts for new tires, service records from the last year, or photos of the car taken right before the accident that show its fantastic condition.

- Local Market Comps: This is crucial. Find a few online listings for the exact same year, make, and model in your local area. This demonstrates the real-world cost to replace your vehicle right now, right where you live.

Presenting a well-organized packet like this changes the entire dynamic. The conversation shifts from a battle of opinions to a review of the facts. If you want a deeper dive into tactics, our guide on how to negotiate a total loss settlement is packed with proven strategies.

When you get on the phone with the adjuster, your tone makes all the difference. Instead of an accusatory, "Your offer is wrong," try a more collaborative approach: "I’ve gathered some additional information that I think supports a higher valuation, and I'd love to walk you through it."

This simple change in language positions you as a reasonable partner trying to get to a fair number, not an opponent. Walk the adjuster through your documents, point out the facts, and let your preparation do the talking. When you turn hard data into a logical argument, you dramatically improve your odds of getting the fair settlement you actually deserve.

Hidden Factors That Impact Your Car's Totaled Value

https://www.youtube.com/embed/CtVJRaA8wFA

Ever wonder why two cars that look identical on paper can have wildly different total loss values? It’s because insurance adjusters dig into details that go way beyond just the make, model, and year. These subtle, often overlooked factors can make a huge difference in your final settlement.

One of the biggest wild cards is simply where you live. Your geographic location plays a massive role in determining your car's Actual Cash Value (ACV). A rugged 4×4 truck, for instance, is going to be worth a lot more in a snowy, rural area where it's in high demand than it would be in a warm, coastal city. The insurer’s valuation is always pegged to your local market conditions.

Condition and Upgrades Matter More Than You Think

This is where your diligence as a car owner really pays off. The adjuster will assess your vehicle's pre-accident condition, and this is your chance to prove it was a cut above the rest. Don't let them just slap an "average" label on it.

Your maintenance records are your best evidence. They provide solid proof of the care you've invested. The same goes for any recent upgrades—they add real, tangible value.

- New Tires: Did you just drop $1,000 on a new set of tires? Make sure they see the receipt.

- Recent Repairs: A brand-new battery or a full brake job is an asset that hasn't had time to depreciate.

The key is to build a compelling case for your car's specific worth. You want to give the adjuster no choice but to look beyond a generic "book value" and acknowledge the true, higher value of your vehicle.

It's also helpful to understand the various factors that lower car insurance costs, as this gives you a peek into how insurers think about vehicle risk and value. This is more relevant than ever, especially since the average age of cars on U.S. roads has hit 12.6 years. With older vehicles sticking around longer, more of them are being declared total losses after accidents.

What Happens Next? Answering Your Top Total Loss Questions

Getting that total loss valuation number is a huge step, but it often kicks off a whole new set of questions. The process can be a maze of confusing terms and high-stakes decisions. Let's walk through a couple of the most common hurdles car owners run into.

What if I Still Owe Money on My Car Loan?

This is one of the toughest situations to be in. Your car is declared a total loss, but you're still on the hook for loan payments. If the insurance company's settlement offer for the Actual Cash Value (ACV) is less than what you owe the bank, that leftover amount is unfortunately your responsibility. This is what's known as being "upside down" on your loan.

This is exactly why Gap Insurance exists. If you have this coverage, it's designed to step in and pay off that remaining loan balance after your main insurance policy pays out the car's value. Without it, you could be stuck making payments on a car you can't even drive anymore.

Can I Actually Keep My Totaled Car?

It might sound strange, but yes, you usually can. In most states, you have the option to "retain salvage."

If you go this route, the insurance company calculates your payout a bit differently. They'll pay you the car's ACV minus its salvage value. That salvage value is simply the amount they would have pocketed by selling your wrecked car to a salvage yard.

Choosing to retain salvage means you get a smaller check from the insurer and a car with a "salvage title." This is a permanent brand on the vehicle's history, making it incredibly difficult to insure or sell later on.

Before you decide, be realistic about the costs. You'll have to pay for all the repairs to make the car safe and roadworthy, and it has to pass a rigorous state inspection to earn a "rebuilt" title. This path really only makes sense if you have the mechanical know-how to handle the repairs yourself.

At Total Loss Northwest, we know how to navigate these tough decisions because we've helped countless drivers through them. If you're staring at a lowball settlement offer, we can help you fight for the fair, accurate value you're owed. Find out how we can help at https://totallossnw.com.