Ever had your car in an accident? Even after it’s been repaired to look brand new, there's a hidden financial hit you've probably taken: diminished value.

In simple terms, diminished value is the loss in your car’s resale price simply because it now has an accident on its record. Buyers are savvy, and they'll almost always pay more for a car with a clean history. That difference in value is what you’ve lost.

Understanding the Financial Impact of an Accident

Picture this: you're at a dealership looking at two identical used cars. Same make, model, year, and mileage. One has a perfect vehicle history, while the other shows it was in a major accident a year ago.

Even if the repairs on the second car are flawless, which one would you choose? Most people would pick the one with no accident history or demand a serious discount on the one that was damaged.

That discount is the heart of a diminished value claim. It’s the real-world financial loss you've suffered because of someone else's mistake. While the body shop restored your car's looks and function, they couldn't wipe its history clean.

The Scale of the Loss

The hit to your car’s value can be surprisingly large. Depending on how bad the accident was and the type of car you drive, its value can plummet by 10% to 25% of its pre-accident market price.

For instance, a 2018 Honda Accord worth $20,000 before a collision could suddenly only be worth $15,000 afterward—that’s a 25% drop. A 2017 Toyota Camry might fall from $18,000 to just $13,500. You can find more details on post-collision depreciation on meyersinjurylaw.com.

It's critical to understand that this isn't about getting extra money. Filing a diminished value claim is about being made whole—recovering the real financial loss that the at-fault driver caused.

Here's a look at how different types of vehicles might be affected.

Estimated Diminished Value by Vehicle Type

The table below gives you a general idea of the value loss a vehicle might suffer after an accident, based on its type and pre-accident value.

| Vehicle Type | Example Pre-Accident Value | Typical % Value Loss | Estimated Diminished Value |

|---|---|---|---|

| Standard Sedan | $25,000 | 10-15% | $2,500 – $3,750 |

| Luxury Sedan | $55,000 | 15-25% | $8,250 – $13,750 |

| SUV / Truck | $40,000 | 12-20% | $4,800 – $8,000 |

| Sports Car | $70,000 | 20-30% | $14,000 – $21,000 |

As you can see, luxury and sports cars often take the biggest hit because buyers in that market are particularly picky about a vehicle's history.

To get this lost equity back, you have to be proactive. The insurance company isn't going to offer this payment on their own. For a deeper look at the basics, our guide on understanding diminished value after an accident is the perfect place to start building your case.

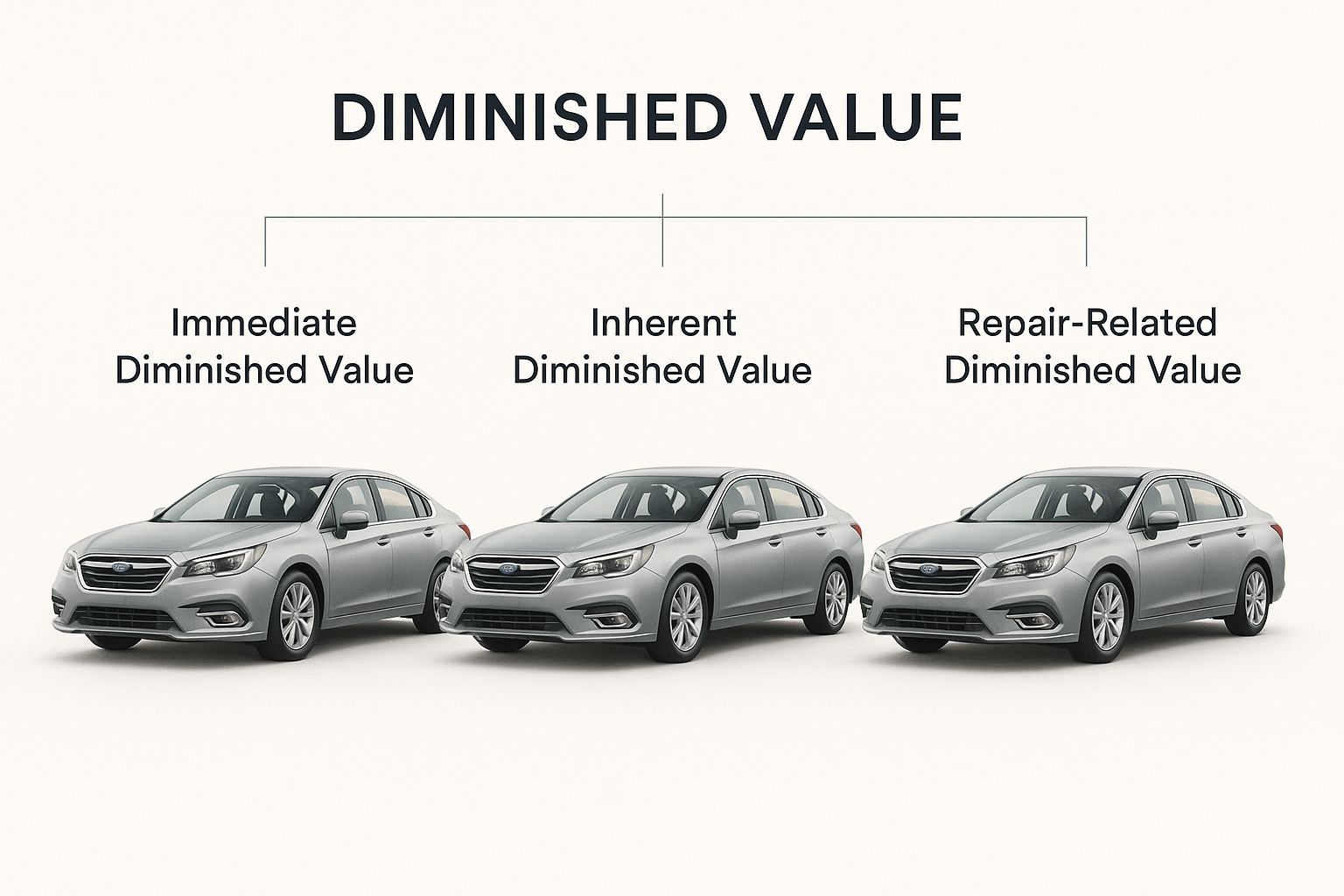

The Three Flavors of Diminished Value

When you start digging into a diminished value claim, you'll quickly realize it’s not just one simple concept. The loss your car suffers actually breaks down into three distinct types. Figuring out which one—or ones—apply to your situation is the key to building a solid claim that an insurance company will take seriously.

Each category points to a different reason why your car isn't worth what it used to be.

Let's unpack what Inherent, Repair-Related, and Immediate diminished value really mean for you and your vehicle.

Inherent Diminished Value

This is the big one—the most common and unavoidable type of value loss. Inherent Diminished Value is the automatic drop in your car’s resale value just because it now has an accident on its record. Period.

Even if the repairs are flawless and done by a world-class technician, the vehicle is forever branded. A savvy buyer will always choose an identical car with a clean history over yours, or at least, they won't pay the same price for it.

Think of it like a beautifully restored antique vase that was once broken. No matter how perfect the repair, it will never be worth as much as a pristine, undamaged original. The accident history alone creates a stigma that lowers what people are willing to pay. This is the fundamental loss most diminished value claims are built on.

Repair-Related Diminished Value

Sometimes, the repairs themselves are part of the problem. Repair-Related Diminished Value comes into play when the body shop's work is just not up to snuff, leaving behind obvious signs of the accident.

This can show up in several ways:

- Mismatched paint that doesn't quite blend with the factory finish.

- Uneven panel gaps around the doors, hood, or trunk.

- Cheaper aftermarket parts were used instead of original factory (OEM) parts.

- Lingering mechanical problems—the car just doesn't drive or feel the same.

This kind of value loss is a direct result of poor craftsmanship. If you're dealing with this, you can often claim it on top of the inherent diminished value.

Here's the bottom line: even with absolutely perfect repairs, you are still owed for the inherent diminished value. The quality of the work just determines whether you can also claim for repair-related losses.

Immediate Diminished Value

Finally, there’s Immediate Diminished Value. This is the difference in your car's market price right after the crash but before any repairs have been done. It's essentially what your car is worth in its wrecked, undrivable state.

While it's a real concept, it's rarely the focus of a claim. Why? Because the goal is almost always to calculate the value loss after the vehicle has been put back together and is ready to be sold.

It's a surprising fact, but while 4.54% of insured drivers filed collision claims in 2022, a huge number of them never knew these categories existed. As a result, they missed out on money they were rightfully owed. You can see how different states handle these claims to understand your specific rights.

How Insurance Companies Calculate Diminished Value (And How It’s Really Determined)

When you file a claim for vehicle diminished value after an accident, the at-fault driver's insurance company isn't just pulling a number out of thin air. They have a playbook, and it’s designed to pay out as little as possible. Knowing how they operate is the first step to getting the fair compensation you deserve.

Most major insurers lean on a convenient, in-house formula to come up with their initial offer. The most infamous of these is widely known as "Rule 17c," which stems from a Georgia court case that set a precedent. While it's not a law, many companies have adopted its basic structure as their go-to calculation method because it reliably produces low numbers.

The Insurer's Favorite Tool: The 17c Formula

The 17c formula is a simple, multi-step calculation designed to minimize the payout. It starts by setting an arbitrary cap on your car’s lost value and then whittles that number down even further.

Here’s a look at how it generally works:

- Step 1: Set a Maximum Value. The formula begins by capping the total possible diminished value at 10% of your vehicle's fair market value right before the accident. So, for a $30,000 car, they start with a maximum of $3,000.

- Step 2: Apply a Damage Multiplier. Next, they reduce that number based on the severity of the damage. They'll use a modifier, like 0.25 for minor cosmetic damage or 1.00 for major structural issues, and multiply it against the 10% cap.

- Step 3: Apply a Mileage Multiplier. Finally, they apply another modifier for your car's mileage, which further reduces the payout. A car with 100,000 miles will get a much larger reduction than one with 10,000 miles.

The core problem with this approach is that it's a blunt instrument. The 17c formula completely ignores critical factors like your car's make and model, local market conditions, and the specific stigma attached to its new accident history. The result is almost always a lowball offer.

The Expert Appraiser's Method: A Real-World Approach

A certified, independent appraiser throws the insurer’s formula out the window. Their entire process is grounded in real-world market data, reflecting what an actual buyer would pay for your repaired car versus an identical one with a clean history. This method is far more nuanced, accurate, and almost always results in a higher, more realistic valuation.

An independent appraiser’s valuation is built on solid evidence:

- A Hands-On Inspection: They start by physically examining the vehicle, scrutinizing the quality of the repair work. They look for subtle flaws like mismatched paint, inconsistent panel gaps, or the use of cheaper aftermarket parts.

- Deep Market Analysis: They dive into local sales data, comparing recent sales of vehicles just like yours—some with clean histories and some with accident records. This shows the real financial impact of the damage history.

- Gathering Professional Opinions: The appraiser will often contact sales managers at several local dealerships. They'll ask them directly, "How much less would you offer for this specific car now that it has this accident on its record?" This provides boots-on-the-ground proof of the value loss.

This comprehensive process creates a detailed report based on market reality, not a self-serving equation. It tells the true story of your vehicle diminished value after an accident.

While a professional appraisal is the only way to build a strong claim, you can get a ballpark figure to start. Using a diminished value claim calculator can give you a preliminary estimate of what your claim could be worth.

What Really Drives Your Claim Amount?

Figuring out a vehicle's true diminished value after a wreck isn't as simple as checking its pre-accident book value. A handful of key variables come together to determine the final number, and getting a handle on them is the first step to building a strong claim and knowing what to expect.

Let's start with the basics: your car's age and mileage. It’s no surprise that a newer, low-mileage car will take a much bigger hit in value compared to an older vehicle with a lot of miles already on the clock. Why? Buyers in the "nearly-new" market are paying a premium for a car that's practically perfect, so an accident history is a massive turn-off.

The same logic applies to luxury and high-performance models. Someone in the market for a top-of-the-line sedan or a sports car is looking for perfection, and an accident record—no matter how expertly repaired—is a permanent black mark in their eyes.

Damage, Repairs, and Stigma

The single most important factor, however, is the severity of the damage itself. There's a world of difference between a minor fender bender and something that compromises the car's core structure.

- Cosmetic Blemishes: Things like scratches, small dents, or a scraped bumper cover will lead to a smaller diminished value claim. These are considered minor, less invasive repairs.

- Structural Damage: This is the big one. If the vehicle’s frame or unibody was bent, twisted, or welded, the value plummets. This type of repair leaves a permanent stigma that scares off a huge number of potential buyers.

- Airbag Deployment: Deployed airbags are an immediate red flag. To any future buyer, it screams "major impact," instantly and significantly dropping the car's perceived worth.

Of course, the quality of the repair work matters, too. While even the best repairs can't completely erase the value loss, exceptional quality auto repair services can certainly soften the blow. On the flip side, sloppy work with mismatched paint, cheap aftermarket parts, or lingering issues will only make your financial loss worse.

The Influence of the Open Market

It’s not just about your car. The world outside the garage plays a huge part in your claim. Local supply and demand, what’s popular in your area, and even the time of year can all affect your car’s resale value and, in turn, its diminished value.

For instance, if used cars are in high demand and there aren't many available, the value loss might be less severe simply because buyers have fewer options. You can find more details on how market factors affect claims on diminishedvalueofgeorgia.com.

An independent appraiser’s job is to weigh all of these factors—your vehicle's stats, the extent of the damage, and real-time market data—to build a complete picture. Their detailed report is the hard evidence you need to challenge an insurance company's initial lowball offer and fight for the full amount you're owed.

How to File Your Diminished Value Claim

Knowing your car has lost value is one thing; actually getting that money back from an insurance company is a whole different ball game. Filing a claim for your vehicle diminished value after an accident isn't complicated, but it does require a methodical approach. Let's walk through the steps you need to take.

First things first, you have to be eligible. In almost every state, you can only file a diminished value claim against the at-fault driver's insurance policy. This is key—the accident can't have been your fault. If the other driver was ticketed or officially found responsible for the crash, you're good to go.

Step 1: Build Your Case With Evidence

A diminished value claim is only as strong as the proof you have to back it up. Before you even think about picking up the phone to call the insurance company, you need to assemble a complete file with all your paperwork. You're essentially building a case, and solid evidence makes it very difficult for an insurer to dismiss your claim.

To build a strong foundation, you'll need a collection of key documents. Think of this as your evidence toolkit—each piece tells a part of the story and validates your financial loss.

Essential Documents for Your Diminished Value Claim

| Document/Evidence | Why It Is Important | Where to Get It |

|---|---|---|

| Police/Accident Report | Officially establishes fault, which is crucial for eligibility. | The law enforcement agency that responded to the accident. |

| Repair Invoices & Estimates | Shows the full extent of the damage and the complexity of the repairs performed. | The auto body shop that repaired your vehicle. |

| Pre- & Post-Repair Photos | Visual proof of the damage and the quality of the repair work. | Your phone (from the scene) and the body shop. |

| Proof of Ownership | Confirms you are the legal owner of the vehicle. | Your vehicle's title and registration documents. |

| Independent Appraisal Report | Provides an unbiased, expert calculation of the diminished value. | A licensed, independent auto appraiser. |

Having these documents organized and ready to go shows the insurance company that you're serious and well-prepared from the very start.

Step 2: Get a Professional, Independent Appraisal

This is, without a doubt, the most important step in this entire process. Do not rely on the insurance company to tell you what your car's diminished value is. Their main goal is to pay out as little as possible, so they often use internal formulas that are designed to benefit their bottom line, not yours.

Hiring a licensed, independent auto appraiser is absolutely essential. A true expert will dig into real-world market data, assess the quality of the repairs, and consider the specifics of your vehicle to produce a detailed, data-driven report. This report becomes the cornerstone of your claim.

An independent appraisal report is your single most powerful negotiating tool. It swaps the insurer's self-serving number for a professional valuation grounded in market reality, giving your claim the credibility it needs to succeed.

Step 3: Submit Your Demand and Negotiate

With your arsenal of evidence and your professional appraisal report in hand, it's time to make your move. You'll need to draft a formal demand letter and send it to the at-fault driver's insurance adjuster. This letter should be clear and concise, stating that you are officially making a diminished value claim, and it must include a full copy of your appraisal.

Once they receive it, the insurance company will review your submission and come back with an offer. Be ready for it—their first offer will almost certainly be low. This is just standard procedure, so don't get discouraged.

Your job is to respond professionally, pointing to specific data from your appraisal report and calmly restating the very real financial loss you've incurred. Negotiation is just part of the process. For a more detailed walkthrough, you can learn more about how to file a diminished value claim to get fully prepared for the road ahead.

So, you’ve decided to file a claim for your vehicle diminished value after an accident. Getting what you're owed means stepping into the ring with two opponents: your state's laws and the at-fault driver's insurance company. You need a strategy for both.

Think of state laws as the rules of the game. They vary wildly, and what works in one state might not fly in another.

https://www.youtube.com/embed/A8n4Jc9QRqY

The most important rule? In most places, you can only file a diminished value claim against the insurance company of the driver who caused the accident. Very few states, like Georgia, are the exception, allowing you to file a claim against your own insurance policy. Knowing this distinction is step one.

The Insurance Company's Playbook

Once you've cleared the state law hurdle and filed your claim, get ready for the pushback. Insurance companies have a well-rehearsed script designed to shut your claim down or pay you as little as possible. Being prepared for their common tactics is your best defense.

You'll almost certainly hear one of these lines:

- "Our repairs restored the vehicle to its pre-accident condition." This is their go-to argument. Sure, the car might look and drive great, but quality repairs can't erase the accident from the vehicle's history report, and that’s what spooks future buyers.

- "We don't pay for diminished value." Don't fall for this bluff. In most states, if their driver was at fault, the law says they have to make you whole. That includes compensating you for the loss in your car's market value.

- "According to our formula, your diminished value is only $X." They’ll pull out a number generated by a tool like the infamous 17c formula, which is notorious for spitting out ridiculously low figures. It's a calculation designed to protect their bottom line, not fairly compensate you.

Remember this: The insurance company's initial offer is just that—an offer. It’s the start of a negotiation, not the end of the conversation. They’re counting on you to be intimidated or just give up.

This is where your independent appraisal report becomes your most powerful tool. It cuts through their arguments and biased formulas with a professional, data-backed assessment of what you're truly owed for your vehicle diminished value after an accident. It gives you the leverage you need to counter their lowball offer and demand fair compensation.

Got Questions? We've Got Answers

Even when you understand the basics, the world of diminished value can feel a little murky. Let's clear up some of the most common questions that pop up when you're trying to file a claim.

Can I File A Claim If I Caused The Accident?

This is a big one, and unfortunately, the answer is usually no. Diminished value is something you claim from the at-fault driver's insurance, making it a third-party claim.

Your own policy is designed to cover repairs, not the drop in resale value. While there are a few rare exceptions—Georgia, for instance—the vast majority of states won't let you file a first-party diminished value claim against your own insurance.

Is There a Deadline to File My Claim?

Yes, and you absolutely don't want to miss it. Each state sets its own statute of limitations for property damage claims, and diminished value falls right into that category.

Generally, you'll have somewhere between two and six years from the date of the accident to file. It's critical to look up your state's specific laws and get the ball rolling as soon as you can.

Waiting too long isn't an option. If you miss the statute of limitations deadline, you legally lose your right to recover that money, no matter how solid your claim is.

Do I Need to Hire a Lawyer?

For many claims, probably not. A detailed report from a credible, independent appraiser is often all the muscle you need to prove your case and negotiate a fair settlement with the insurance company.

However, if you're dealing with a high-value car, a complex accident, or an insurer that's just stonewalling you, bringing in an attorney can be a smart move. They can add a lot of weight to your claim and show the insurance company you mean business.

Don't let the insurance company dictate what your vehicle is worth. The team at Total Loss Northwest provides certified, independent appraisals to ensure you get the fair settlement you're legally owed. We fight for you. Learn more and start your claim at https://totallossnw.com.