The second your car is involved in a collision, its value takes a permanent hit. It doesn't matter how perfectly it's repaired; the fact that it was in an accident is now a permanent part of its history, and that history costs you money.

This immediate drop in market price is what we call diminished value. It’s the invisible damage that even the best body shop can’t fix.

How An Accident Immediately Impacts Your Car's Value

Put yourself in a car buyer's shoes for a moment. You're looking at two identical cars—same make, model, year, and price. The only difference? One has a clean vehicle history report, and the other shows it's been in a wreck. Which one do you choose? It’s a no-brainer.

That hesitation from buyers is exactly what creates diminished value. It's a real, quantifiable financial loss that you shouldn't have to shoulder when the accident wasn't your fault.

Even after meticulous repairs, the accident is a permanent blemish on the car's record. This single fact can slash a vehicle's worth by 10% to 30% of its pre-accident value. For a car that was worth $25,000, that’s a direct loss of anywhere from $2,500 to $7,500 out of your pocket.

Understanding The Types of Value Loss

The total loss in value isn't just one simple number; it’s actually a combination of different issues. Getting a handle on these distinctions is your first step toward building a solid case when you file a claim with the insurance company.

There are two main types of diminished value you'll run into:

- Inherent Diminished Value: This is the automatic, most common form of value loss. It happens simply because the car now has an accident on its record, making it less desirable than a comparable car with no accident history.

- Repair-Related Diminished Value: This loss is caused by subpar repairs. If the shop uses cheap aftermarket parts instead of OEM (Original Equipment Manufacturer) ones, or if the paint doesn't quite match, or if the frame isn't perfectly aligned, your car’s value takes another nosedive.

The bottom line is this: no repair, no matter how flawless, can scrub the accident from your car's permanent record. This guide is designed to help you understand, calculate, and ultimately recover the value your car has lost, giving you a clear plan to fight for the fair settlement you deserve.

Understanding the Hidden Cost of Diminished Value

When your car is damaged in an accident, the most obvious cost is the repair bill. But there’s another, often more significant financial hit that most people miss: diminished value.

Think about it from a buyer's perspective. You're looking at two identical used cars—same make, model, year, and mileage. One has a squeaky-clean vehicle history. The other has a reported accident, even if it was repaired flawlessly. Which one are you going to pay more for?

That difference in price, purely because of the accident history, is the core of diminished value. It's the instant, permanent drop in your car's resale value, and it happens the second that collision becomes part of its permanent record.

Even with top-notch repairs, a vehicle with an accident on its record can sell for 10% to 30% less than one without. This "invisible" damage is a real financial loss, and it's where insurance negotiations can get very tough. Understanding exactly what you've lost is the first step to getting it back.

The Three Types of Diminished Value

To build a solid claim, you need to be specific about the kind of value your car has lost. It's not just one big number; it’s a concept that breaks down into three distinct categories that appraisers and insurers will scrutinize.

-

Inherent Diminished Value: This is the most common and unavoidable type. It’s the automatic drop in value that occurs the moment an accident is reported, no matter how perfect the repairs are. The stigma of having a "damage history" permanently makes your car less attractive to potential buyers.

-

Repair-Related Diminished Value: This loss comes directly from the quality of the repair work itself. Think mismatched paint, aftermarket parts used instead of original factory ones (OEM), or subtle frame issues that only a trained eye can spot. Shoddy repairs compound the initial value loss.

-

Insurance-Related Diminished Value: This one is a bit less common but far more severe. It happens if an insurer initially declares a vehicle a total loss, but it's later repaired and put back on the road with a branded title (like "salvage" or "rebuilt"). That brand on the title is a permanent red flag that kills its market value.

It's crucial to know which type of diminished value applies to your situation. While every accident causes inherent diminished value, finding evidence of poor repairs can give you powerful leverage in your negotiation.

Getting a handle on these concepts is the foundation for figuring out what your car is actually worth now. While this section is about the loss in value, you can learn how insurers calculate your car's pre-accident worth by reading our guide on calculating the actual cash value of your car. This gives you the complete picture of the valuation puzzle.

Factors That Determine Post-Accident Depreciation

Not every fender bender has the same financial fallout. The true value of your vehicle after an accident isn't a random number; it's calculated based on a specific set of factors that appraisers and potential buyers look at very closely. Getting a handle on these elements is the first step toward understanding what your car is now worth—and fighting for a fair settlement.

Think of it this way: a small scratch on a bumper is a minor headache, but a bent frame is a serious, long-term problem. The market sees these differences in the same light, assigning a much bigger loss in value to more significant incidents.

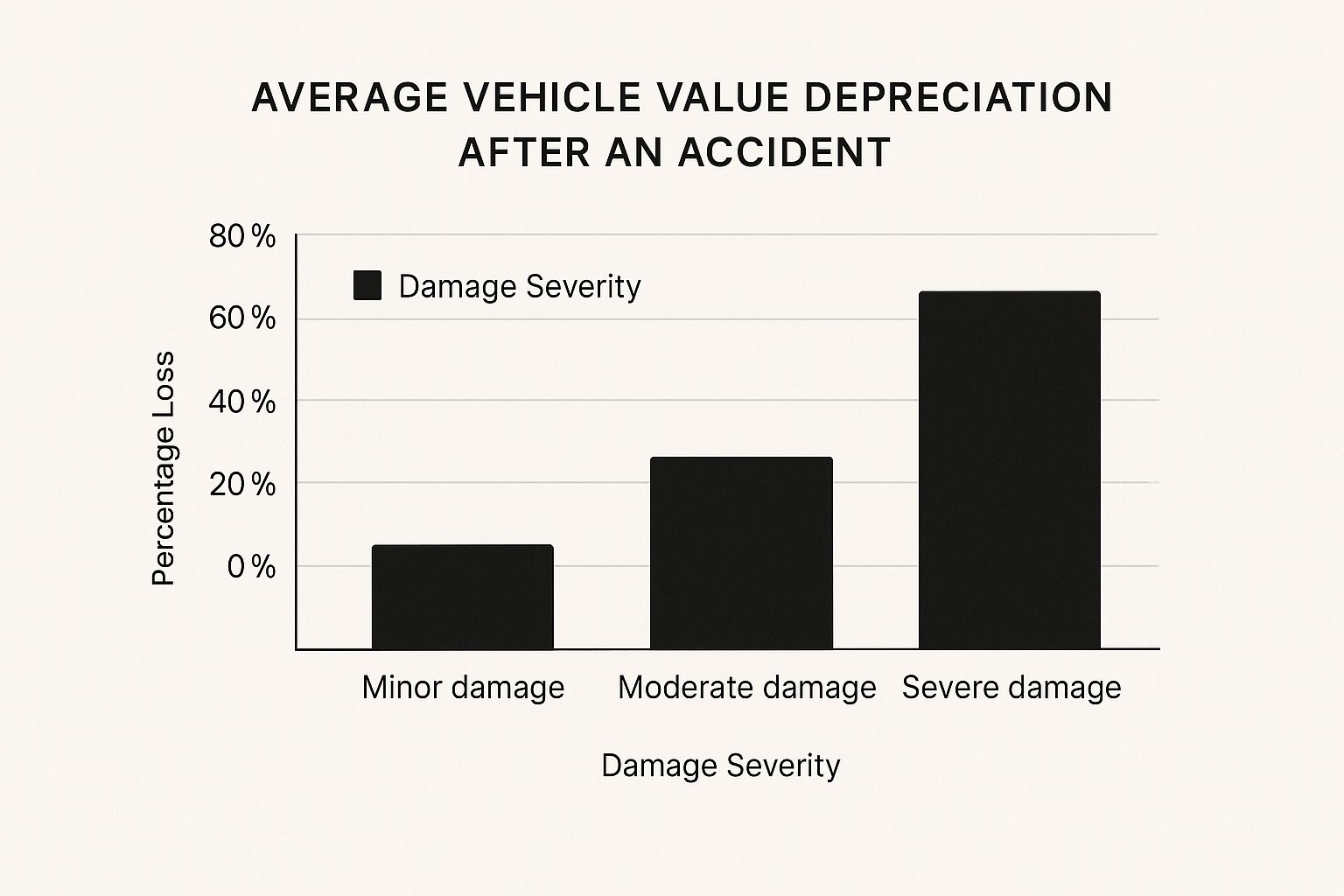

Severity of Damage

The single most important factor is just how badly your car was damaged. This goes way beyond what you can see on the surface. Appraisers and insurers have a system for categorizing damage to figure out how it affects the car's long-term safety and integrity.

There’s a huge gap between a cosmetic scuff and real structural harm.

- Cosmetic Damage: This is the stuff you see, like scratches, dings, and chipped paint. While it might look ugly, it doesn't impact how the car drives or its safety, so it causes the least amount of diminished value.

- Mechanical Damage: Here, we're talking about damage to the engine, transmission, or suspension. These repairs are a lot more involved and can leave potential buyers worried about future reliability, leading to a moderate drop in value.

- Structural Damage: This is the worst-case scenario. It means the vehicle's frame or unibody has been compromised. Even if the repairs are flawless, a history of frame damage is a massive red flag, causing the biggest hit to its value.

A good rule of thumb: any accident where the airbags go off is almost always considered severe. It’s a clear signal of a major impact and immediately raises questions about the vehicle's structural integrity, causing a substantial drop in resale value.

Quality of Repairs

Right after the severity of the damage comes the quality of the repair work. How your vehicle is put back together directly impacts what it's worth. The goal is always to return the car to its pre-accident condition, but the parts used to do it make all the difference.

Using Original Equipment Manufacturer (OEM) parts is absolutely critical. These are the exact same parts your car was built with at the factory. Cheaper, aftermarket parts often don't fit perfectly, can wear out faster, and might even compromise safety features. Any smart buyer will pull the repair records, and seeing a history of non-OEM parts will drag down the vehicle’s value.

Vehicle Age and Pre-Accident Condition

Finally, what your car was like before the crash plays a big part. A newer, low-mileage car in mint condition simply has more value to lose. Because of this, it will take a much bigger percentage-based hit than an older car with high mileage and some existing wear and tear.

A car's history and even its brand reputation matter. As a general guideline, minor accidents might knock 5-10% off a car's value, while major ones could cause a 10-15% decrease. Luxury brands often see an even steeper drop, sometimes as high as 25-30%, because of higher repair costs and buyer expectations. You can find more data on how accidents impact car trade-in values at meyersinjurylaw.com.

All these factors—damage, repairs, and pre-accident condition—come together to paint the full picture of your car's diminished value.

How Your Car's Brand Affects Its Resale Value

The badge on your car's grille is more than just a brand name; it's a huge factor in determining the value of your vehicle after an accident. Not all makes and models take the same hit after a collision, and knowing why is crucial for setting realistic expectations for your settlement.

Think of it this way: a high-end luxury watch with a deep scratch will lose a much bigger chunk of its value than a durable, everyday digital watch with the same exact scratch. The luxury item is held to a higher standard of perfection. Any flaw, even one that's been professionally repaired, leaves a bigger dent in what people are willing to pay for it. The same logic applies to cars.

The Luxury Car Problem

High-end and luxury vehicles, especially German brands, often suffer the steepest drop in value. Why? It comes down to the sheer cost and complexity of their repairs. Buyers are naturally skeptical that even the most skilled body shop can perfectly restore sophisticated electronics or precisely align a high-performance chassis after a major impact.

This "perception gap" is where the real value loss happens. The very things that make these cars so desirable in the first place—their advanced technology, premium materials, and precision engineering—also make them more susceptible to severe depreciation after an accident.

This chart shows just how directly the severity of the damage impacts the loss in value.

As you can see, the financial hit climbs quickly as you move from minor cosmetic scrapes to serious structural harm.

Brand Reputation and Real-World Data

The numbers don't lie. German luxury brands like BMW and Mercedes-Benz consistently suffer the most. A BMW might see its value drop by 25-35% after just a minor accident. If the damage is severe, that figure can jump to 40-50%.

On the other hand, brands known for reliability and affordable parts, like Honda or Toyota, tend to fare much better. Their post-accident value drops are often in the 10-20% range. The simple reason is that the high cost of OEM parts and the need for specialized labor on luxury cars makes future buyers nervous about hidden problems, pushing resale prices way down. You can learn more about how different car brands fare after an accident at appraisalengine.com.

In short, a brand's reputation for durability and affordability acts as a buffer against post-accident value loss. While a luxury car loses value based on its compromised perfection, an economy car retains more of its worth because its primary value is tied to practical reliability.

How to Calculate Your Vehicle's Diminished Value

Knowing your car has lost value after a wreck is one thing. Being able to put a credible, defensible number to that loss is a completely different challenge.

Insurance companies won't just take your word for it. They need a figure they can plug into their own system, and more often than not, they lean on a specific formula to calculate a starting point for the value of your vehicle after an accident.

Breaking Down the Rule 17c Formula

One of the go-to methods for insurers is something called the "17c formula." While it's riddled with problems, understanding how it works gives you a crucial peek behind the curtain at what the insurance adjuster is likely thinking. Think of it as their opening offer in a negotiation.

The Rule 17c calculation is a multi-step process that chips away at your car's pre-accident value. It’s designed to produce a conservative estimate, which is exactly why it's so popular with insurance carriers.

Here’s a quick look at how they come up with their number.

| Step | Calculation | Example Value |

|---|---|---|

| 1. Find Market Value | Determine the vehicle's value right before the crash. | $30,000 |

| 2. Apply 10% Cap | The formula sets a maximum DV at 10% of the vehicle's value. | $3,000 |

| 3. Damage Multiplier | Multiply the base amount by a damage severity factor (0.0 to 1.0). | $3,000 x 0.75 = $2,250 |

| 4. Mileage Multiplier | Multiply again by a mileage factor (0.0 to 1.0). | $2,250 x 0.80 = $1,800 |

As you can see, this formula starts with a low ceiling and only goes down from there. It's a structured way for an insurer to minimize their payout, not to accurately reflect what a real buyer in the open market would deduct for that accident history.

Why Their Formula Is Just a Starting Point

The 17c formula's biggest flaw is that arbitrary 10% cap. In the real world, a serious collision can easily slash more than 10% off a car’s resale value, especially on newer or high-end models.

The damage and mileage multipliers are also highly subjective. An adjuster can easily tweak those numbers to push the final payout even lower. This is why you should never accept their initial calculation at face value.

This formula provides a number, but it almost never captures the true market loss. It’s a tool insurers use to control costs, not to reflect what an informed buyer would actually pay for a car with an accident history.

Let's put this in perspective. Normal depreciation is already brutal. Some family cars can lose 43% of their value in just three years without any accidents. Certain luxury sedans can plummet by over 66% in the same timeframe. An accident record just pours gasoline on that fire, as explained in this research on how accidents compound vehicle depreciation.

Because of all these moving parts and the insurer's built-in bias, relying on their math is a mistake. An online tool, like our diminished value claim calculator, can give you a much better ballpark figure.

Ultimately, though, the best way to fight back against a lowball offer is with an independent, expert appraisal. A professional report gives you the evidence you need to challenge their numbers and argue for the full amount you’re rightfully owed.

Steps to Filing a Successful Diminished Value Claim

Getting back the value your vehicle lost after an accident isn't as simple as asking the insurance company for a check. You have to build a rock-solid, evidence-based case that leaves no room for them to argue. It's all about proving your loss with undeniable facts.

The very first thing you need to do is become a master of documentation. Start gathering every single piece of paper related to the accident and the subsequent repairs. This paperwork is the foundation of your entire claim and tells the complete story of what your car went through.

Gather Your Essential Documents

Before you even pick up the phone to call the insurance company, get your evidence organized. An incomplete file is an open invitation for a denial. You'll want clear, readable copies of everything.

Here’s a quick checklist of what you'll need to pull together:

- The Official Police Report: This is your official record of the accident and, most importantly, who was at fault.

- All Repair Estimates and Invoices: These documents detail the full scope of the damage and what it cost to fix.

- Proof of OEM Parts: If you insisted on Original Equipment Manufacturer parts, get that in writing from the body shop. It’s a key detail in showing the quality of the repair work.

- Before and After Photos: Nothing tells the story like pictures. Document the initial damage and the final, repaired state of your car.

The cornerstone of a winning diminished value claim is an independent, third-party appraisal report. An insurer's internal assessment is designed to minimize their payout; a report from a certified professional is your most powerful tool for proving your car's true market value loss.

Draft a Compelling Demand Letter

With all your documentation in order, it's time to write a formal demand letter to the at-fault driver's insurance company. This isn't just a casual note—it's a professional document that lays out your case with clarity and confidence.

In your letter, you should state your car’s pre-accident value, the specific amount of diminished value you’re claiming, and refer directly to the evidence you’ve enclosed, especially your independent appraisal. For a more detailed guide, you can learn more about how to file a diminished value claim and see exactly what this process looks like.

Finally, brace yourself for a little back-and-forth. An insurer's first offer is rarely their final one. The key is to be polite but firm. Keep pointing back to your professional appraisal and documentation. A well-supported claim gives you the high ground you need to secure a fair settlement for the value your car has truly lost.

Common Questions About Your Car's Value After a Wreck

After an accident, the questions start piling up almost as fast as the repair bills. What is my car worth now? Who is supposed to pay for the drop in value? Getting clear, straightforward answers is the first step toward making sure you're treated fairly.

Let's tackle some of the most common things people ask when dealing with post-accident value.

Who Actually Pays for a Diminished Value Claim?

This is the big one. In almost every state, the responsibility falls squarely on the at-fault driver's insurance company. Their driver caused the accident, and that negligence caused your car to lose a chunk of its resale value.

To get that money back, you'll need to file what's called a "third-party claim" directly against their insurance policy.

Can I Just File a Claim With My Own Insurance?

It's a logical question, but the answer is usually no. Most standard auto insurance policies are written to cover the cost of repairs and get your car back on the road—that's it. They aren't designed to compensate you for the market value it lost simply because it now has an accident history.

Think of it like this:

- Third-Party Claim (Their Insurance): This is your path for diminished value. You're going after them because their client caused your financial loss.

- First-Party Claim (Your Insurance): This is for fixing the bent metal. Your policy's job is to restore the car's physical condition, not its market reputation.

While a handful of states have exceptions, for the vast majority of drivers, the only way to recover diminished value is to pursue the at-fault party's insurer.

What About Leased Cars? Does Diminished Value Still Matter?

Yes, absolutely. In fact, it might matter even more. When you turn in a leased vehicle, the leasing company inspects it with a fine-tooth comb. An accident on its record will tank its value, and you can bet they'll hold you financially responsible for that loss.

If you don't file a diminished value claim after an accident in a leased car, you could be blindsided by hefty penalties and fees when your lease is up.

Don't let an insurance adjuster tell you what your car is worth. At Total Loss Northwest, our certified appraisers dig into the details to build a case for the fair and accurate settlement you deserve. We provide the expert reports needed to push back against low offers on your diminished value or total loss claim. Learn more about how we can help you at totallossnw.com.