So, you’ve just been told your car is a "total loss." What does that even mean, and what comes next?

A total loss adjuster is essentially your personal advocate in this situation. They are an independent expert you hire to figure out your vehicle's true pre-accident value, ensuring the insurance company’s settlement offer is fair and accurate.

Your Car Is Totaled—What Really Happens Next

Hearing your car is "totaled" can be a gut punch. It’s the insurance company's way of saying it costs more to fix your car than it’s worth. This is the exact moment a total loss adjuster can step in and make a huge difference in how much money you get back.

Think of it this way: the insurance company has its own team of adjusters. Their job is to settle the claim, often as quickly and cost-effectively as possible for their employer.

An independent total loss adjuster, on the other hand, works for you. Their only job is to dig deep and determine your car’s actual cash value (ACV) right before the accident, without any bias.

The Typical Total Loss Journey

Knowing the process helps you see where things can go wrong—and where an expert can help. While every claim is a little different, the path is usually pretty similar.

Here’s what you can generally expect:

- Initial Damage Assessment: The insurance company's adjuster looks at the damage and estimates how much it will cost to fix.

- Total Loss Declaration: If the repair costs hit a certain point—often 70-80% of the car’s value—they’ll declare it a total loss.

- Settlement Offer: The insurer then gives you a settlement offer based on their calculation of your vehicle's ACV.

- Negotiation Phase: This is your chance to push back if the offer seems low. Bringing in your own total loss adjuster is a powerful move here.

An adjuster's valuation can make a significant difference in your final payout. Understanding their job is not just helpful—it's essential for protecting your financial interests and ensuring you receive a fair settlement.

A good adjuster often uncovers value that the insurance company’s automated systems miss. Think recent upgrades, a pristine maintenance record, or high local market demand for your specific model. All of these details add up and can directly increase the money you get in your pocket.

Who's Who in Your Claim?

It's easy to get confused by all the different people involved in a total loss claim. This quick breakdown clarifies who does what.

Key Players in a Total Loss Claim

| Role | Primary Responsibility |

|---|---|

| You (The Policyholder) | Reporting the claim, providing documentation, and negotiating the final settlement. |

| Insurance Company Adjuster | Works for the insurer to assess damage, determine fault, and calculate the company's settlement offer. |

| Independent Total Loss Adjuster | Hired by you to conduct an unbiased valuation of your vehicle and advocate for a fair settlement. |

| Body Shop/Mechanic | Provides the professional estimate for the cost of repairs. |

Ultimately, having an expert on your side who is focused solely on your interests can level the playing field.

The Adjuster's Role in Your Insurance Claim

https://www.youtube.com/embed/J8FTmAH0EIs

So, what does a total loss adjuster actually do? Think of them less as a number-cruncher and more as a financial detective for your vehicle. Their main job is to build an ironclad, evidence-based case for what your car was really worth right before it was totaled. This goes way beyond a quick glance at a price guide. It's a deep dive.

They'll dig into everything. We're talking about vehicle condition reports, recent maintenance you've paid for, and every single aftermarket upgrade—whether that’s a new set of tires or that custom sound system you installed last year. These are the little details that the insurance company's automated software almost always misses.

A good adjuster also knows that a car's value isn't the same everywhere. That popular truck model you own might be worth a lot more here in the Pacific Northwest than it would be in Florida. They research local market sales data to make sure your valuation is based on what people are actually paying in your area, which can make a huge difference in your final payout.

The Two Types of Adjusters

You'll always deal with an adjuster in a total loss claim, but it’s critical to know who they're working for. The difference is simple, but the financial impact on you is anything but.

-

The Insurer's Adjuster: This person works for the insurance company. Their goal is to settle the claim efficiently and according to company policy, which usually means sticking to the value their internal software spits out—a number designed to keep their costs down.

-

Your Independent Adjuster: This is a total loss adjuster you hire to represent you and only you. Their loyalty is 100% to you, and their entire focus is on fighting for the highest possible fair market value for your vehicle.

This conflict of interest is exactly why so many people decide to get their own expert. An independent adjuster isn't just helpful; they level the playing field. For more on this, check out our guide on how to deal with insurance adjusters for tips on handling those conversations.

Think of it this way: The insurance company's adjuster is playing for their team, and their goal is to protect their company's bottom line. An independent adjuster is the star player on your team, dedicated to getting you the win.

Building Your Case with Evidence

An independent adjuster doesn't just pull a higher number out of thin air—they prove it. They assemble a comprehensive report that breaks down every single factor that adds value to your vehicle.

This report will typically include:

- Comparable Vehicle Analysis: They find actual, recently sold vehicles in your local market that are a true match to yours in terms of trim, mileage, and condition.

- Documentation of Upgrades: They present receipts and records for any recent work, maintenance, or high-value features you've added.

- Condition Substantiation: They use your maintenance records and pre-accident photos to document that your vehicle was in exceptional shape.

This evidence-based strategy shifts the conversation from a subjective argument to a factual negotiation. It makes it much, much harder for the insurer to stand by a lowball offer.

How Your Vehicle's True Value Is Determined

When an insurance company declares your car a total loss, their settlement offer all comes down to a single term: Actual Cash Value (ACV). This isn't some arbitrary number. In theory, it’s supposed to represent what your vehicle was worth on the open market right before the accident occurred.

The trouble is, the way insurance companies arrive at that number is often where the conflict starts. They usually lean on valuation software that pulls in and averages data from a wide range of sources. While that might sound fair on the surface, these automated systems often completely miss the details that made your car special. A seasoned total loss adjuster knows a car's real value is hidden in the nuances the software was never programmed to see.

Beyond the Blue Book Value

Think of guides like Kelley Blue Book (KBB) or NADA as a starting point, not the final word. They're great for getting a general idea, but they can't possibly capture every detail that affects a specific car’s value in your local area.

An expert adjuster doesn't just glance at a guide; they build a case. They put together a detailed valuation report grounded in real-world evidence, not just generalized data from a computer program.

Here’s what that deeper dive looks like:

- Local Market Comparables: This is key. An expert finds actual cars—the same year, make, model, trim, and condition—that recently sold right in your neighborhood. This is infinitely more accurate than relying on some national average that has nothing to do with your local market.

- Pre-Accident Condition: Did you keep your car in mint condition? An adjuster will use your maintenance records, recent repair invoices, and photos to prove it. The insurer’s software almost always defaults to "average" condition, which can cost you thousands.

- Upgrades and Special Features: That brand-new set of tires, the premium sound system you installed, or the rare factory sports package—all of it adds value. Every single high-value addition needs to be documented and accounted for.

The real goal is to paint a complete and accurate picture of your specific vehicle's worth. A proper valuation digs into every single detail that makes your car stand out from a generic entry in a pricing guide. This ensures the compensation you receive reflects its true, provable value.

The Impact of Rising Repair Costs

There’s another major factor pushing more cars into the total loss category: the skyrocketing cost of repairs. Today’s vehicles are rolling computers, loaded with expensive sensors, cameras, and advanced electronics. What looks like a simple fender-bender can easily lead to a repair bill that’s astronomical.

For instance, industry reports show the average cost of repair hit over $4,730 in 2024. When you factor in climbing labor rates and parts inflation—which jumped more than 4% in early 2025—it becomes clear why insurers are quicker to total a vehicle. If you want to see the numbers for yourself, you can check out the latest report on insurance and collision repair industry data.

This trend makes getting an accurate ACV appraisal more critical than ever. As insurance companies write off more cars to sidestep massive repair bills, you have to be confident that their settlement offer is fair. Understanding how a professional valuation is built is the first step, and you can see a breakdown in our guide on creating a proper total loss estimate.

Challenging a Low Settlement Offer

It’s a frustrating moment for any car owner: the insurance company declares your car a total loss, and then slides an offer across the table that feels like a slap in the face. It’s easy to feel cornered, but here's the most important thing to remember: their first offer is just that—an offer. It's not the final word; it's the opening line of a negotiation.

So, why the lowball offer? It's rarely personal. Insurers often rely on automated valuation systems that can be flawed. These platforms might pull outdated comparable sales, fail to account for the brand-new tires you just bought, or completely overlook your car's pristine condition. Their system spit out a number. Now, it's your turn to show them why that number is wrong.

Turning a Dispute into a Negotiation

The secret to getting a better settlement is to approach this as a negotiation, not a fight. Anger and frustration won't get you far, but solid, well-organized evidence will. Your goal is to build a logical, fact-based case that clearly demonstrates your vehicle's true worth, making it nearly impossible for the insurer to stick to their initial, low valuation.

Think of yourself as an attorney building a case. Every piece of paper that supports a higher value for your car is a piece of evidence.

Start gathering your documentation:

- Maintenance Records: A thick file of regular oil changes and service appointments proves your car was meticulously cared for, justifying a condition rating far above "average."

- Receipts for Upgrades: Did you add a premium sound system, custom wheels, or a tow package? Those receipts are proof of added value.

- Recent Repair Invoices: A new transmission or a set of expensive tires installed a month before the accident adds significant, measurable value to your vehicle.

The initial settlement offer is just a starting point based on an algorithm's assumptions. Your job is to replace those assumptions with cold, hard facts that paint an accurate picture of your vehicle's true market value.

The Strategic Advantage of an Expert

You can absolutely gather all this evidence on your own, but this is where a total loss adjuster becomes your professional advocate. They live and breathe this stuff. They know exactly what documentation insurers find persuasive and how to present it for maximum impact.

More importantly, they have access to industry-grade tools and market data that you can't find with a quick Google search. This allows them to locate truly comparable vehicles that support a much higher valuation for your car.

Hiring an independent expert instantly levels the playing field. They take over the stressful phone calls and back-and-forth emails, freeing you from the emotional drain of the negotiation. Their involvement shifts the conversation from an emotional plea to a data-driven business transaction.

For a deeper dive into the tactics involved, our guide on how to negotiate a total loss settlement provides more strategies. Ultimately, bringing in an adjuster sends a clear signal to the insurance company: you're serious about getting a fair payout. This alone can often speed up the process and lead to a much more reasonable counteroffer.

So, Why Hire Your Own Total Loss Adjuster?

After a total loss, your insurance company will assign an adjuster to your claim. They're usually professional and efficient, but it's vital to remember who signs their paycheck. Their job is to settle the claim according to their company's guidelines and financial interests, which don't always align with getting you the maximum payout.

Hiring your own independent total loss adjuster completely flips the script. Suddenly, you have a seasoned pro in your corner whose only loyalty is to you. It levels the playing field, transforming you from an individual against a massive corporation into a well-represented claimant with an advocate fighting for your best interests. Their entire focus is getting you the highest possible fair settlement for your vehicle—not a penny less than what you're owed.

Get the Payout You Actually Deserve

The single biggest reason to hire your own adjuster is the massive impact it can have on your final settlement. An independent expert goes far beyond the automated, one-size-fits-all valuation software that insurance companies use. They roll up their sleeves and build a powerful, evidence-backed counter-valuation from the ground up.

They do this by:

- Digging into the local market: They find real, recent sales of comparable vehicles right in your area to establish a true, boots-on-the-ground market value.

- Valuing every single upgrade: That new sound system you installed? The premium all-weather tires? They meticulously itemize and assign value to every single aftermarket addition.

- Proving your vehicle's real condition: They use your maintenance records, recent repairs, and detailed photos to argue for a "good" or "excellent" condition rating, pushing back against the insurer's default "average" classification.

When you present this kind of detailed, fact-based report, it becomes incredibly hard for the insurance company to stick to its initial lowball offer. The difference can often mean thousands of extra dollars in your pocket.

Take the Stress and Hassle Off Your Plate

Let's be honest: dealing with a total loss claim is a nightmare. It's a seemingly endless cycle of phone calls, tracking down paperwork, and arguing your case over and over again. It’s draining and time-consuming when you're already dealing with the stress of losing your vehicle.

An independent adjuster lifts this entire burden from your shoulders.

Think of it this way: when you hire an adjuster, you're not just paying for their expertise—you're buying back your time and peace of mind. They take over the fight, handling the frustrating negotiations and mountains of paperwork so you can focus on getting back to your life.

They become your single point of contact, managing all communication with the insurer, presenting the valuation evidence, and handling the entire negotiation process. You get to stay in the loop without having to live in the trenches of the claim battle.

Understanding the Competing Agendas

The effectiveness of an independent adjuster boils down to a simple conflict of interest. The adjuster sent by your insurance company has a fundamentally different goal than an adjuster you hire yourself. Their roles and motivations are worlds apart.

To make it crystal clear, let's compare them side-by-side.

Insurer's Adjuster vs. Your Independent Adjuster

| Aspect | Insurer's Staff Adjuster | Your Independent Adjuster |

|---|---|---|

| Loyalty | To the insurance company | To you, the policyholder |

| Objective | Settle the claim efficiently and cost-effectively | Maximize your settlement payout |

| Valuation Method | Relies on company software and national data | Uses local market research and detailed evidence |

| Focus | Speed and adherence to company policy | Accuracy and securing your full vehicle value |

As you can see, their objectives are simply not the same. One is focused on closing the file for their employer, while the other is focused on maximizing the outcome for their client—you.

A Smart, Risk-Free Financial Move

Most people assume hiring an expert is expensive, but that's not how it works here. The vast majority of independent adjusters operate on a contingency fee basis.

This means you pay absolutely nothing out of pocket. Their fee is just a small, pre-agreed percentage of the extra money they get for you above the insurance company’s initial offer.

It’s a win-win. They are highly motivated to fight for every last dollar because they only get paid if they succeed in increasing your settlement. For you, it’s a risk-free investment that puts a professional negotiator on your team, often leading to a final payout that dwarfs the cost of their fee.

The Future of Total Loss Claims and Valuation

The world of total loss claims is anything but static. It's constantly being reshaped by everything from global economic turbulence to new technology. For a total loss adjuster, keeping up isn't just good practice—it's absolutely critical for getting clients the fair settlement they deserve.

Think about it: international supply chain hiccups can send repair costs and parts availability into a tailspin. These are factors happening thousands of miles away that directly impact the value of your wrecked vehicle. It makes pinning down an accurate number more challenging than ever.

At the same time, Artificial Intelligence (AI) is elbowing its way into the claims process. Insurance companies are leaning on AI tools for quick, photo-based damage estimates, selling it as a faster, more efficient way to handle claims. But here's the catch: these automated systems often miss the details. They can't always see the subtle signs of damage or appreciate the unique features that a trained human eye would catch in a heartbeat.

Technology and the Human Element

This push toward automation doesn't make the human adjuster obsolete. Far from it. It actually makes their expertise more valuable. While AI is great at crunching numbers to spit out a baseline valuation, it completely lacks the seasoned judgment and investigative instinct of a real professional.

An expert adjuster is the essential reality check on the machine. They dig into the data, question the AI’s assumptions, and build a compelling case based on solid, real-world evidence. That’s something an algorithm just can't do. The future of fair claims isn't about choosing between tech and people; it's about blending data-driven insights with human-led analysis.

The real value of a top-notch total loss adjuster today is their ability to stand at the crossroads of technology and reality. They take the black-and-white data from an automated report and paint the full-color picture of what a vehicle is actually worth, protecting their clients from the blind spots of technology.

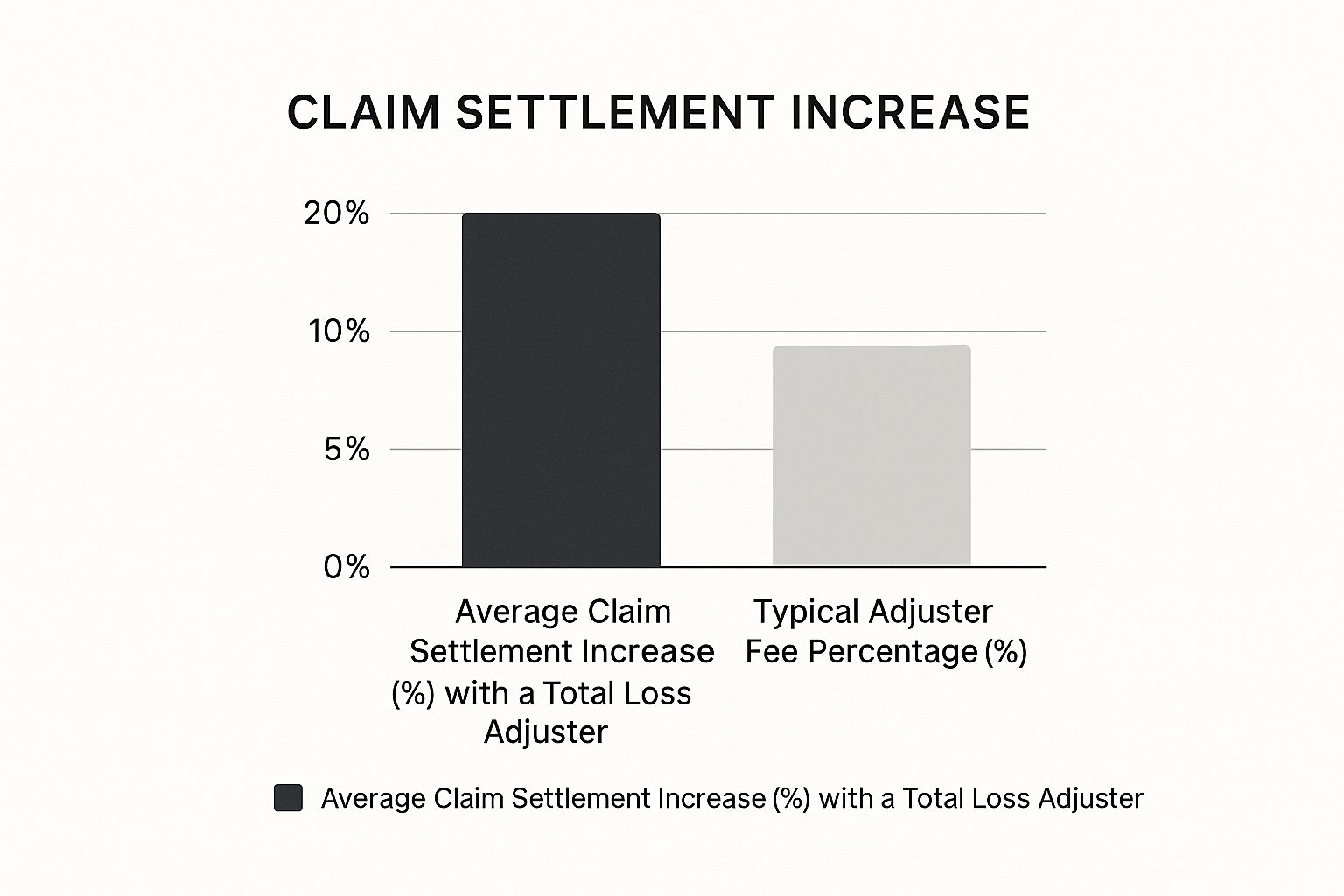

The infographic below really drives home the financial benefit of bringing a professional into the mix.

As you can see, the increase in the settlement amount an adjuster can secure typically dwarfs the fee they charge for their service.

Macroeconomic Pressures on Valuations

The puzzle of vehicle valuation gets even more complicated when you factor in major economic and environmental trends. In 2024 alone, climate-related disasters caused $368 billion in property damage, putting immense strain on the entire insurance industry.

On top of that, new trade policies have tacked on over $3 billion to material costs. All this creates a volatile market where vehicle values are constantly shifting. The global AI claims market, which hit $514 million in 2024, is one way the industry is trying to manage this complexity, but it also highlights just how much expert oversight is needed. If you want to dive deeper, the 2025 Loss Adjusting Insights Report from Sedgwick is a great read on how these global forces are affecting property claims.

In this ever-changing landscape, a total loss adjuster does more than just value a car. They have to understand the entire, intricate web of factors that influence that value. Their ability to connect the dots between market data, tech reports, and economic pressures is what ensures your settlement reflects today's reality, not yesterday's out-of-date numbers. When it comes to getting a fair outcome, their expertise is still the most powerful tool you have.

Got Questions? We've Got Answers

When your car is declared a total loss, it's natural to have a million questions running through your mind. It's a confusing process. Here are some straightforward answers to the questions we hear most often.

How Much Does it Cost to Hire a Total Loss Adjuster?

This is usually the first thing people ask, and the answer is better than you think. Most people assume hiring an expert is expensive, but it's structured to be completely risk-free for you.

Nearly all independent adjusters work on a contingency fee. This means you pay zero out of pocket. Their fee is simply a small, agreed-upon percentage (typically 10% to 20%) of the extra money they get for you—that is, the amount above the insurance company's first lowball offer.

It’s simple: if they don't increase your settlement, you don't owe them a dime.

Can't I Just Handle the Negotiations Myself?

You certainly can, and many people try. You have every right to negotiate directly with your insurance company. The real question is whether you should.

Hiring a total loss adjuster gives you a professional in your corner. Think of it like going to court; you could represent yourself, but you'd be at a huge disadvantage against a seasoned lawyer. Adjusters bring specialized knowledge, years of negotiation experience, and access to the same professional valuation tools the insurers use—software the public can't get.

Hiring an adjuster isn't just about getting more money. It's about leveling the playing field. They take the stress and emotion out of the equation, handling the difficult conversations and building a case based on cold, hard facts. It turns a frustrating argument into a professional negotiation.

What Paperwork Should I Have Ready for My Claim?

The more proof you have, the stronger your case will be. Your vehicle's real value is in its history and condition, and paperwork is how you prove it.

To help your adjuster build the best possible argument for your car's value, start gathering these items:

- The Vehicle's Title: This is non-negotiable proof that you are the legal owner.

- Maintenance Records: A full service history is powerful. It shows your car was well-cared-for, which directly translates to a higher value.

- Receipts for Upgrades & New Parts: Did you buy new tires a month before the crash? Install a new sound system? Receipts prove you invested in the vehicle, and that value should be recovered.

- Photos from Before the Accident: A picture is worth a thousand words. Clear, recent photos showing your vehicle in great shape can completely shut down an insurer's attempt to claim it was in poor condition.

Having these documents on hand allows your appraiser to hit the ground running and build an undeniable case for what your vehicle was truly worth.

At Total Loss Northwest, we live and breathe this stuff. Fighting for the fair and true value of your vehicle is what we do. If you're staring at a settlement offer that just doesn't feel right, let our certified appraisers take over. Visit us at https://totallossnw.com and get the payout you're legally owed.