So, you’ve just been told your car is a “total loss.” That phrase can be a real gut punch. It immediately brings to mind images of a completely mangled vehicle, but the reality is often less about the car's appearance and more about simple economics.

Think of it this way: if you had an old laptop and the screen broke, you'd have to decide if it's worth fixing. If a new screen costs $400 but the whole laptop is only worth $300, you’d probably just buy a new one. It's the same logic insurance companies use.

When your car is totaled, the insurer is essentially saying that the cost to safely and properly repair it is more than what the car was worth right before the accident. They'll pay you its pre-accident fair market value, often called the Actual Cash Value (ACV), minus your deductible. In return, they usually take possession of the damaged car, and you can use that settlement money to find a new ride.

Your Car Is Totaled What Happens Now

Hearing the words "total loss" from an adjuster officially kicks off the claims process. This is your cue to get organized, because what you do next can have a big impact on your final settlement. The better prepared you are for that first real conversation with the adjuster, the smoother things will go.

Before you get on the phone, take a few minutes to gather some key information. Having this ready shows the adjuster you're on top of things and helps set a professional, cooperative tone for your negotiations.

The First Steps After a Total Loss Declaration

Once the car has been officially declared a total loss, the clock starts ticking. Your next move is to prepare for the conversation with the insurance adjuster. Don't go into it cold!

Try to have this information at your fingertips:

- Your Car's Full Details: Be ready with the exact year, make, model, trim package, and current mileage. Every little detail matters.

- Proof of Upgrades: Did you just buy new tires? A new battery? Have a major service done? Get those receipts together. Recent investments can add value.

- Loan/Lender Info: If you're still paying off the car, you'll need your lender's contact information and your loan account number. The insurance company will need to coordinate with them.

It's helpful to know that you're not alone in this situation. Total losses are becoming more common than ever.

The total loss frequency for the year recently hit an all-time annual high of 22.2%. This is happening largely because modern cars are packed with sensors and complex technology, making repairs far more expensive than they used to be. You can find more details in recent industry reports on Autobody News.

Feeling empowered starts with understanding the road ahead. Knowing what to do when your car is totaled is the best way to make sure you're treated fairly and get the settlement you deserve. This initial phase is your best opportunity to show you're an informed and proactive owner.

Key Terms in a Total Loss Claim

Navigating a total loss claim can feel like learning a new language. To help you get comfortable with the lingo, here's a quick reference guide for the essential terms you'll hear from your adjuster.

| Term | What It Means For You |

|---|---|

| Actual Cash Value (ACV) | This is the amount your car was worth right before the crash. It's the starting point for your settlement offer, calculated based on its age, condition, mileage, and market data. |

| Total Loss Threshold | A percentage set by your state. If repair costs exceed this percentage of the car’s ACV, the insurer must declare it a total loss. |

| Deductible | The amount you agreed to pay out-of-pocket for a claim when you bought your policy. Your insurer will subtract this from your final settlement check. |

| Salvage Value | The amount the insurance company can get by selling your damaged car for parts or scrap. They factor this into their calculations. |

| Settlement | The final amount of money the insurance company agrees to pay you for your totaled vehicle. This is the number you'll be negotiating. |

| Gap Insurance | Optional coverage that pays the difference between your ACV settlement and the amount you still owe on your auto loan. It's a lifesaver if you're "upside down" on your loan. |

Understanding these terms is the first step in taking control of the process. They are the building blocks of your entire claim, and knowing what they mean will help you have more productive conversations with your insurance company.

How Insurers Decide a Car Is a Total Loss

When an adjuster comes to inspect your car, they aren't just looking at the crumpled fender or smashed headlight. They're doing the math. It’s a cold, hard calculation to see if repairing your vehicle makes financial sense for the insurance company. This decision has nothing to do with emotion or how bad the damage looks—it's all about the numbers.

At the heart of it is what's known as the Total Loss Formula. The insurer weighs two key figures against each other: the cost to repair the vehicle plus its potential value as scrap, versus its pre-accident Actual Cash Value (ACV). If the cost of repairs and scrap gets too close to, or surpasses, the ACV, they'll declare it a total loss.

It's a business decision, plain and simple. Think of it like a landlord deciding whether to gut-renovate an old apartment. If the renovation costs more than the apartment is worth, it makes more sense to sell it as-is and cut their losses.

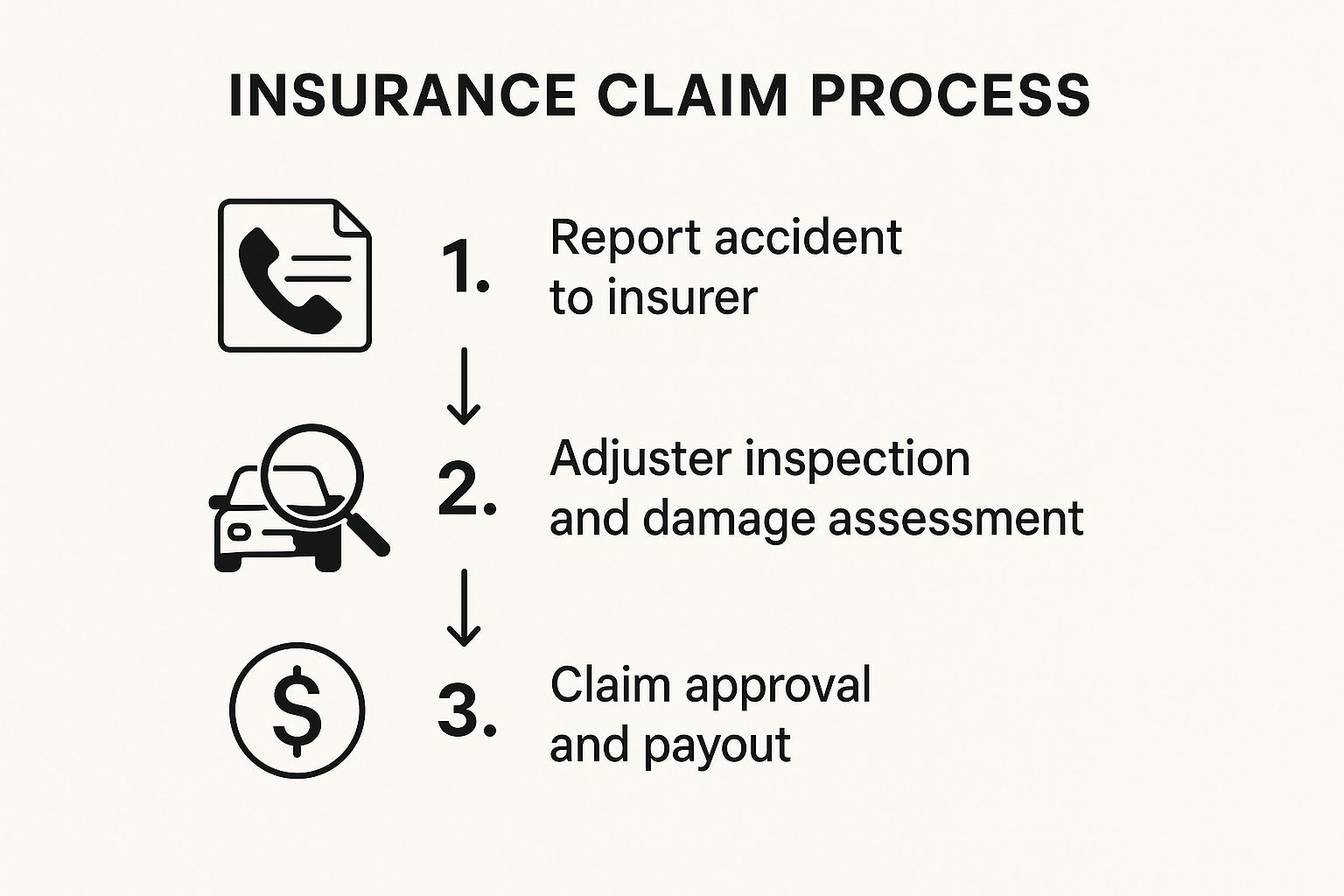

The claims process, from that first phone call to the final payout, has a few key steps. This chart lays out the typical journey.

As you can see, that adjuster's assessment is a pivotal moment that really dictates where your claim goes next.

Why Modern Cars Total Out More Easily

It might seem strange, but newer cars are often totaled from accidents that look surprisingly minor. A simple fender bender might not seem like a big deal, but the hidden costs can be astronomical. Why? It all comes down to the sophisticated technology packed into every inch of a modern vehicle.

Today’s cars are loaded with advanced driver-assistance systems (ADAS). We're talking about:

- Sensors embedded in bumpers and side panels

- Cameras in grilles and mirrors

- Radar units for cruise control and collision avoidance

A bumper isn't just a piece of plastic anymore. Damage it, and you could be looking at replacing multiple expensive sensors that then need to be painstakingly recalibrated. That's how a repair that once cost a few hundred dollars can now easily run into the thousands, pushing the car right over the total loss threshold.

State Laws and Total Loss Thresholds

The final say doesn't always rest solely with the insurance company. Most states have specific laws that set the bar for when a car must be declared a total loss. These rules are known as Total Loss Thresholds (TLT).

A TLT is a set percentage. If the estimated cost of repairs goes over this percentage of the car's ACV, the insurer is legally required to total it out.

- For example, one state might have a TLT of 75%. If your car is worth $20,000 and the repairs are estimated at $16,000 (80% of the ACV), it's a mandatory total loss.

- Other states use a "Total Loss Formula" (TLF), where the cost of repairs plus the car's salvage value must exceed the ACV.

The decision to total your car is a mix of your insurer's financial formula and the specific laws in your state. It's an objective calculation, not a subjective opinion on how wrecked the car is.

Knowing these factors is key. You can find more details about what makes a car totaled and how these rules work in practice. The more you understand about why the insurer made their decision, the better prepared you'll be for what comes next.

Understanding Your Car's Actual Cash Value

When your car gets totaled, one phrase suddenly becomes the most important part of your vocabulary: Actual Cash Value (ACV). This single number is the bedrock of the insurance company’s settlement offer, so getting a grip on what it really means is your first step toward a fair payout.

Simply put, ACV is what your car was worth on the open market just moments before the crash. It isn't what you paid for it, what a brand-new replacement costs, or even what you still owe on your loan. It’s the vehicle’s fair market price tag right before the accident happened.

Insurance companies don’t just guess this number. They have a specific formula and use market data to calculate your car's ACV, and you have every right to see how they did their math.

How Insurers Calculate Your Car's Worth

Adjusters rely on detailed valuation reports, usually from third-party data companies that live and breathe market analysis. These reports crunch several key numbers to pinpoint the ACV for your exact vehicle.

Here’s what they’re looking at:

- Year, Make, and Model: This is the basic starting point for any car's value.

- Mileage: Fewer miles on the odometer usually means a higher value. More miles, a lower one. It's that simple.

- Overall Condition: This is a big one. They'll look at everything from the state of the paint and interior to any dings, scratches, or known mechanical quirks that existed before the accident.

- Recent Upgrades: Did you just put on a new set of tires? Maybe a new stereo or a recently replaced engine? If you have the receipts, these can add real value.

- Geographic Location: A 4×4 truck is going to be worth more in a snowy mountain town than in a sunny city. Local market demand plays a huge role.

The insurer’s mission is to figure out what a willing buyer in your area would have paid for your car. That's why their report will list "comparables"—examples of similar cars that recently sold near you.

Your Action Plan: Remember, the first ACV figure you see is just an opening offer. You don't have to accept it on the spot. Your job is to dig in, check their work, and come back with your own evidence to support a higher, more accurate value.

Building Your Case for a Fairer ACV

If the insurance company’s offer feels low, it’s time to roll up your sleeves and build your own argument. Don’t just complain that it's unfair; present them with clear, documented proof that shows your car was worth more. This is how you can directly influence your final settlement.

Start by gathering these key pieces of evidence:

- Maintenance Records: A full stack of receipts for regular oil changes and service proves your car was well-cared for, not neglected.

- Receipts for Upgrades: Those new tires you bought six weeks ago? That new battery you had installed? Dig up the receipts. These are tangible additions the adjuster might have overlooked.

- Find Your Own Comps: Get online and become a car shopper. Search auto marketplaces for vehicles just like yours—same year, make, model, trim, and similar mileage—for sale in your region. Screenshot those listings as proof of a higher market value.

When you arm yourself with this kind of information, you change the conversation. You’re no longer just a passive recipient of an offer; you’re an active negotiator armed with real-world data. A little bit of prep work here is the best tool you have for making sure you get what your car was truly worth.

How to Navigate the Settlement Negotiation

When that first settlement offer from your insurance company lands in your inbox, it's tempting to breathe a sigh of relief and just accept it. But hold on. It’s crucial to see that initial number for what it is: a starting point.

Think of it as the opening bid in a negotiation, not the final word. The insurance adjuster has a file, some data, and a valuation report. You have the real story of your car. Your job now is to bridge the gap between their numbers and your car’s actual worth.

Dissecting the Initial Offer

Before you do anything else, put on your detective hat and dig into their valuation report. This document is the foundation of their offer, so you need to understand every single detail. Did they get the trim level right? Did they account for the premium sound system or the new set of tires you just put on two months ago?

And don't forget about the little things that add up. A common oversight is sales tax and title fees. Your settlement is supposed to make you "whole," which means it should cover the cost of replacing your vehicle—and that includes the taxes and fees you'll have to pay on the next one. These details can easily add hundreds of dollars to your final check.

If the offer feels low, don't get mad. Get organized. This is where all the homework you did earlier pays off.

- Present Your Comps: Lay out the comparable vehicle listings you found that show higher asking prices in your local market.

- Show Your Receipts: Did you recently invest in a major repair or upgrade? Provide the invoices to prove the added value.

- Keep a Paper Trail: Document every conversation. Make a note of who you spoke to, the date, and what you discussed. A clear record is your best friend.

The key is to be polite but firm. You're not accusing the adjuster of lowballing you; you're simply presenting new information they may not have had. You're helping them see that their data was incomplete and that your car was worth more than their initial report suggested.

Understanding GAP Insurance and Loan Balances

One of the most stressful situations is when the settlement offer is less than what you still owe on the car loan. This is often called being "upside down," and it’s a tough spot to be in. For example, if the insurance company values your car at $15,000, but you still have an outstanding loan of $17,000, you’re on the hook for that $2,000 difference.

This is exactly what Guaranteed Asset Protection (GAP) insurance is for. If you have this optional coverage, it steps in to cover that gap between the car's value and your loan balance, saving you from a significant out-of-pocket expense.

Without GAP insurance, that debt doesn't just disappear—you're still legally required to pay it off. This is why learning how to negotiate a total loss settlement is so important. By building a strong case with solid evidence, you can increase the settlement amount and minimize, or even eliminate, the financial hit you have to take.

Deciding What to Do After the Settlement

Once you and the insurer shake hands on a settlement figure, a new decision is waiting for you. This is the moment you decide what actually happens to your totaled car. What you choose next really hinges on your finances, how much of a project you’re willing to tackle, and what your plans are for your next set of wheels.

For most folks, the path of least resistance is the best one. You take the full settlement check, sign the title over to the insurance company, and hand them the keys. It’s the cleanest break. This route lets you close the chapter on your old car and use that money to move forward, whether that’s clearing a loan or putting a down payment on a new vehicle.

Keeping Your Totaled Car

But there is another way. It’s called owner retention, and it’s exactly what it sounds like: you decide to keep the wrecked car. If you go down this road, the insurance company pays you the settlement amount, but they'll subtract the car's salvage value. Think of the salvage value as the price the insurer expected to get for your car by selling it for parts or scrap at an auction.

Let's put some numbers to it. Say your settlement was $15,000, and the insurer determines the car's salvage value is $2,500. If you keep the car, you’d get a check for $12,500. This can look pretty good on paper, especially if you know your way around a toolbox or the damage seems mostly cosmetic. Be warned, though—it comes with some serious strings attached.

The Reality of a Salvage Title

The second you choose to keep the car, its legal identity changes forever. Your state’s DMV will brand the title, issuing a salvage title. This is a permanent red flag on the vehicle's record, declaring to the world that it was once written off as a total loss. More importantly, it means the car is illegal to drive on public roads until it goes through a tough certification process.

Here’s a glimpse of the journey ahead if you choose owner retention:

- The Repairs: You're on the hook for every single repair. You have to pay for the parts and labor needed to get the car back into safe, working condition.

- The State Inspection: After the repairs are done, the car has to pass a special, high-stakes state inspection. This is way more intense than your typical annual check-up. Inspectors will be looking deep into the car’s frame, safety systems, and structural integrity to make sure it's truly roadworthy.

- The Rebuilt Title: If—and only if—it passes that inspection, the state will issue a rebuilt title. This new title finally lets you legally register, drive, and insure the car again.

A rebuilt title never goes away. It permanently marks the vehicle's history, and its resale value will plummet compared to an identical car with a clean title. You might also find that getting insurance for a rebuilt vehicle is more of a headache and costs more.

Deciding to keep the car is a major commitment. If you’d rather not deal with the hassle, exploring options for getting cash for damaged cars is a smart and practical alternative.

Surrendering vs Keeping Your Totaled Car

This table breaks down the core pros and cons to help you decide the best course of action after your total loss claim is settled.

| Action | Pros | Cons |

|---|---|---|

| Surrendering the Car | – Receive the full settlement value. – Simple, clean, and fast process. – No further responsibility for the car. |

– Lose the ability to salvage parts. – You have to find a new vehicle immediately. |

| Keeping the Car | – You can repair it and drive it again. – Potential to sell it for parts yourself. – Might be cheaper than buying a replacement. |

– Settlement is reduced by salvage value. – You must handle all repairs and inspections. – The car will have a permanent rebuilt title, lowering its value. |

Ultimately, you need to weigh the potential savings against the guaranteed costs, time, and future headaches before you make that final call.

Common Questions About Totaled Cars

When an insurance company tells you your car is a total loss, your mind probably starts racing with questions. It's a confusing and stressful situation, and getting straight answers is the first step to getting back on your feet.

Let's walk through some of the most common things people ask when they're figuring out what to do next.

Do I Still Make Car Payments If My Car Is Totaled?

Yes, absolutely. This is probably the most jarring part for many people, but your car loan doesn't just vanish because the car is gone. That loan is a separate contract you have with a lender, and you’re still on the hook for those payments until it’s paid off.

Think of it this way: the insurance settlement is meant to help you close out that loan. The insurance company will typically send the settlement check directly to your lender to pay off your remaining balance. If there’s a gap between what they pay and what you owe, you’ll have to cover that difference yourself—unless you have GAP insurance.

Can I Keep My Totaled Car and Repair It?

Most of the time, yes. You have the option to keep the vehicle in a process called “owner retention.” If you go this route, the insurance company will pay you the car’s Actual Cash Value (ACV), but they’ll subtract your deductible and the car's salvage value (what they could have sold it for at auction).

But here's the catch: the car will be issued a "salvage title," which means it's not legal to drive on public roads. You'll have to pay out of pocket for all the repairs needed to make it safe again. Once the work is done, it has to pass a tough state inspection before it can get a "rebuilt" title, which finally lets you register and insure it.

Important Takeaway: Even after it's fixed, a car with a "rebuilt" title will always be worth less than one with a clean history. You might also run into trouble finding an insurance company willing to provide full coverage, or you might have to pay higher premiums.

How Long Does a Total Loss Claim Usually Take?

There's no single answer, but you can generally expect the whole process to take several weeks. It's not a one-day affair; there are several steps that have to happen in order.

Here’s a rough timeline of what to expect:

- Initial Report and Inspection: Getting the claim filed and having an adjuster look at the car can take a few days to a week.

- Valuation and Offer: The adjuster then has to research your car's value and put together a settlement offer. This can easily take another week.

- Negotiation: If you don't agree with their offer—and you shouldn’t if it feels low—the back-and-forth can add days or even weeks to the timeline.

- Paperwork and Payment: Once you agree on a number, it takes about a week to process the title transfer and cut the check.

A lot of this depends on how efficient your insurer is and how quickly you can get them all the documents they ask for.

What if I Disagree with the Insurance Offer for My Car?

You never have to take the first offer they throw at you. If you feel the insurance company is lowballing you on your car's value, you have every right to push back and negotiate for a better settlement.

Your first move should be to dispute their offer in writing. To make your case, you need to bring your own proof. Gather maintenance records, receipts for recent repairs or new tires, and, most importantly, find listings for comparable cars for sale in your area. If you still can't get them to budge, your policy likely has an "appraisal clause" that lets you bring in independent, third-party appraisers to settle the dispute for good.

Dealing with a lowball settlement offer is beyond frustrating. At Total Loss Northwest, we step in to fight for the true value you're owed. If you’re not getting a fair deal, we can invoke the Appraisal Clause for you and make sure you get the settlement you deserve. Find out more about how our certified auto appraisals can help at https://totallossnw.com.