When your insurance adjuster tells you your car is a "total loss," your first thought might be about the wreck itself. But your next thought should be about the money. A total loss calculator is your first line of defense, helping you estimate your car's Actual Cash Value (ACV) before you even see the insurance company's offer.

This simple step is critical. It helps you figure out if the settlement they're proposing is fair or just a lowball number meant to pad their bottom line.

What a Total Loss Declaration Really Means

Hearing the phrase "total loss" sounds dramatic, but it isn't a judgment on your car's condition—it's just a math problem for the insurer. A car is declared a total loss when the cost of repairs plus what they can get for the wrecked car's parts (its salvage value) is more than what the car was worth right before the accident.

Let's break it down. Say your car had a market value of $15,000. The body shop says repairs will run $12,000. On the surface, it seems worth fixing. But the insurance company also knows they can sell the wrecked car for scrap and parts for around $4,000.

From their perspective, the total cost is $16,000 ($12,000 in repairs + $4,000 in lost salvage value). Since that's more than the car's $15,000 ACV, they'll total it out.

Why Cars Are Totaled More Often Now

If it feels like you're hearing about more cars being totaled, you're not wrong. This is happening more and more often, with a staggering 22.6% of all auto insurance claims now ending in a total loss declaration.

Why the increase? A few things are at play. Cars on the road are older than ever, and more importantly, the technology inside them has become incredibly complex and expensive to fix.

Even a minor fender-bender can damage the sensitive cameras, sensors, and computer modules that run everything from your cruise control to your airbags. Fixing these Advanced Driver Assistance Systems (ADAS) can quickly send repair bills skyrocketing, making it much easier to hit that total loss threshold. It’s worth learning more about the specific components that make a car a total loss to understand the adjuster’s perspective.

Key Takeaway: Your main job after your car is totaled is to double-check the insurance company's math on the ACV. Their first offer is just that—an offer. It’s the beginning of a negotiation, not the final number.

This is exactly why a total loss calculator is so essential. It gives you the evidence you need to push back against a weak offer and fight for the settlement you are actually owed. When you come to the table with your own valuation, you change the entire dynamic of the conversation.

Gathering Proof of Your Vehicle's Value

Any total loss calculator is just a starting point. Its accuracy depends entirely on the quality of the information you feed it. To get a realistic idea of what your car was worth right before the crash, you've got to dig deeper than just the make and model.

Think of it this way: you're building a case for your car's true value. Every little detail can make a difference.

Your car was more than just its year and mileage. Did you have the upgraded leather interior? The premium sound system or that beautiful panoramic sunroof? Those features add real money to its pre-accident value, but an insurance adjuster might conveniently gloss over them if you don't have the proof.

This is where you need to get organized and document everything that made your car stand out. Your goal is a complete file that proves its condition and worth before the accident happened.

Documenting Your Car's Specifics

First things first, let's nail down the core details. Your vehicle's trim level (like an LX versus a Touring model) is a massive factor. This alone can mean a difference of thousands of dollars in the final valuation. Don't let them value your top-tier model as a base version.

Next, you need to list out every single optional package and any aftermarket upgrades you made. These are the things that standard insurance company valuations almost always miss.

- Factory Upgrades: Jot down any special packages it came with—think technology, safety, or appearance packages. That "Tech Package" with navigation and driver-assist features adds real value.

- Recent Improvements: Have you bought new tires recently? A new battery? Replaced the brakes? Go find those receipts. That $1,200 set of new Michelin tires you just put on absolutely needs to be accounted for.

- Maintenance History: Pull together all your service records. A consistent history of oil changes and timely repairs shows the insurance company your car was well-maintained and in excellent mechanical shape.

Key Takeaway: The insurer's first offer is almost always based on a generic, base-model version of your car. It's your job to provide the specific details that push that value up to where it should be.

To help you get everything in order, I've put together a checklist of the documents and details you'll need to collect. This will be your arsenal when it's time to negotiate.

Your Vehicle Value Documentation Checklist

This table outlines the essential data points and documents you'll need to calculate a precise Actual Cash Value (ACV) for your vehicle.

| Data Category | Specific Details to Collect | Why It's Important |

|---|---|---|

| Basic Information | Year, Make, Model, Trim Level, VIN, Mileage | Establishes the baseline value for your specific vehicle configuration. |

| Optional Features | Factory-installed packages (e.g., tech, sport, luxury), sunroof, premium audio | These significantly increase the car's value over the standard model. |

| Recent Purchases | Receipts for new tires, battery, brakes, or other major parts | Proves recent investment in the vehicle's condition and longevity. |

| Maintenance Records | Oil change receipts, service invoices, repair orders | Demonstrates the vehicle was well-cared-for and in good mechanical condition. |

| Aftermarket Additions | Custom wheels, stereo system, remote starter, window tint | These upgrades add value that isn't captured in standard valuation tools. |

| Proof of Condition | Pre-accident photos (interior/exterior), detailing receipts | Visual evidence that counters any claim the vehicle was in poor shape. |

Having these documents ready will not only give you a more accurate number from the total loss calculator but also provide you with the ammunition you need to challenge a lowball offer from the insurance company.

Proving Your Vehicle's Condition

When it comes to proving condition, photos are your best friend. Scour your phone for pictures of your car from before the accident that show off its clean interior and scratch-free paint job. These visuals are powerful because they directly counter the adjuster's default assumption that your car was just "average."

If you don't have good photos, get creative. Do you have a receipt from a recent car wash or detailing service? Sometimes they note the car's condition on the invoice.

For those who need to build an airtight case, getting a professional https://totallossnw.com/vehicle-appraisal/ can be a game-changer. An appraiser uses all this detailed evidence to establish a certified, defensible value, which gives you incredible leverage during negotiations.

How to Calculate Your Car's Actual Cash Value

If you just sit back and let the insurance company tell you what your car was worth, you're almost guaranteed to get a lowball offer. It's that simple. To get a fair settlement, you need to do your own homework and build a data-backed case for your car’s true Actual Cash Value (ACV).

My approach has always been to use multiple sources to build a valuation that can stand up to scrutiny. We won't just plug numbers into one calculator; we'll gather data from several trusted places and then, most importantly, anchor that data in what's happening in the real world. This is how you gain the leverage to counter the insurer’s initial offer.

Start with Reputable Online Tools

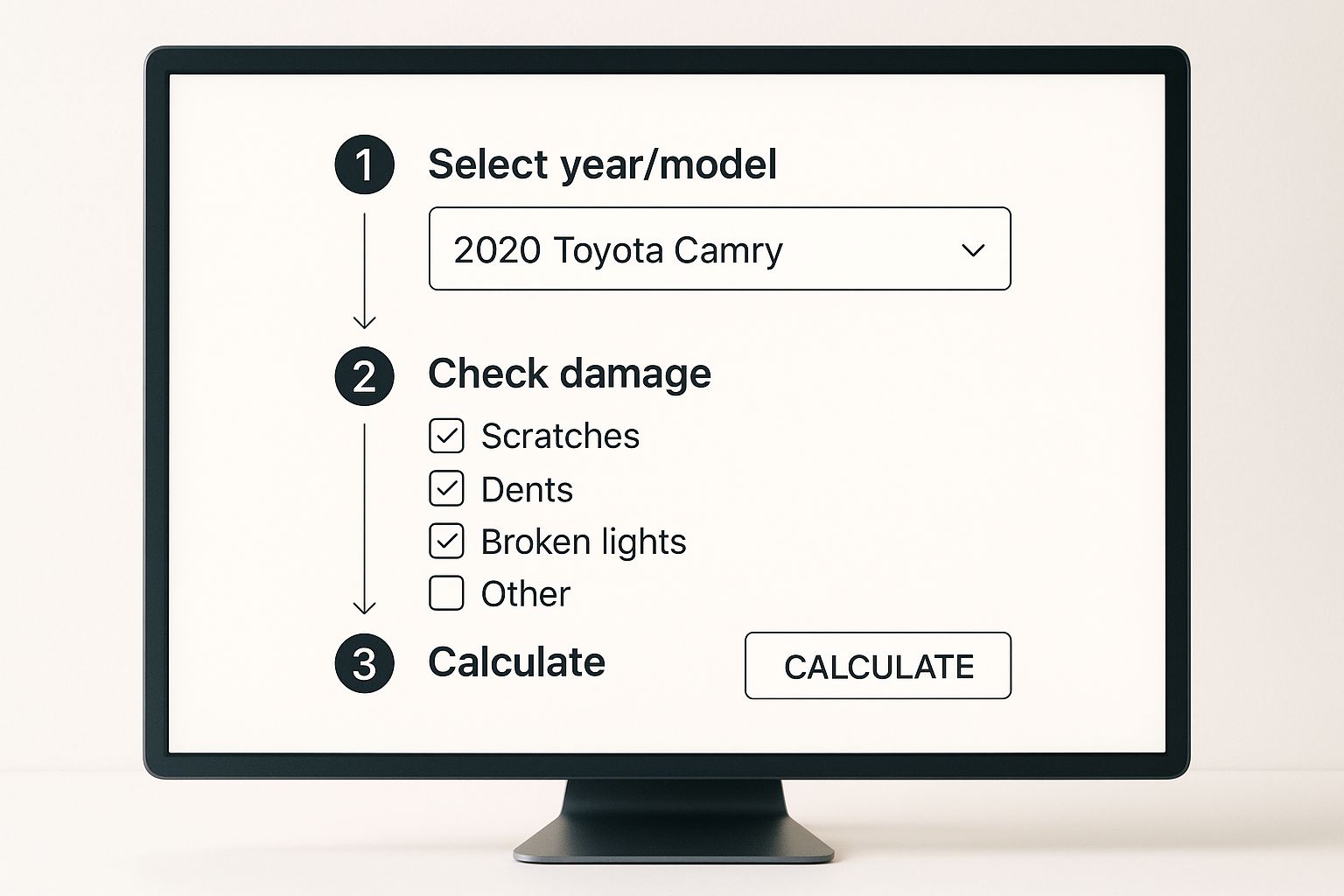

First things first, let's get a baseline value using the big names in vehicle valuation. Sites like Kelley Blue Book (KBB) and Edmunds are industry standards, and they're the perfect place to start.

When you're on these sites, details matter. Be meticulous. You need to input your car's exact trim level, every optional package it had, and the precise mileage. And be honest—but fair—about its condition before the accident. If your car was truly in "Excellent" shape, don't shortchange yourself by selecting "Good."

This image gives you a quick visual of the kind of information these online tools will ask for.

As you can see, every little detail—from the trim to the optional features—can move the needle on the final number. I always recommend getting values from at least two or three different sources. Once you have them, calculate an average to get a solid starting point for your negotiation.

Find Real-World Market Comps

Online calculators are a great start, but they aren’t the whole story. The most compelling evidence you can bring to the table is what similar cars are actually selling for right now, in your local area. In the industry, we call these "comparables" or "comps."

Head over to sites like Autotrader, Cars.com, or even Facebook Marketplace to find vehicles that are the same year, make, model, and trim as yours.

Here’s what to do:

- Set your search radius: Look for listings within a 50-100 mile radius of where you live.

- Match the specifics: Your goal is to find at least three to five listings that closely mirror your car’s mileage and pre-accident condition.

- Document everything: Take screenshots of these listings. Make sure you capture the asking price, mileage, and VIN. This is your proof.

Don't be shocked if the asking prices you find are higher than what the online calculators suggested. The used car market has been running hot, and values are often inflated compared to standard book values.

This isn't just a hunch. Current projections show that total loss market values in the U.S. are running about 8.5% above the historical average growth rate. If your insurer is using outdated data, you're the one who loses out.

By combining the data from valuation tools with hard evidence from local market comps, you're not just guessing—you're building an undeniable case for your car’s true ACV. For a deeper dive into all the factors that go into this number, take a look at our detailed guide on the Actual Cash Value formula.

Negotiating a Fair Settlement With Your Insurer

Alright, you’ve done your homework. With data from a total loss calculator and a list of real-world comps in hand, you’re ready to talk to the insurance adjuster.

The first thing to remember is that their initial offer is just that—an offer. It's almost never their best one. Think of it as the opening bid in a negotiation, and your preparation is what will give you the upper hand.

When that first number comes in, take a deep breath. Avoid reacting on the spot. Simply thank the adjuster, tell them you need to review the details against your own research, and schedule a time to talk again. This simple step sets a professional, serious tone and buys you valuable time.

Presenting Your Counter Offer

When you call the adjuster back, your goal is to walk them through your valuation, step by step. You’re not just throwing out a random number; you’re showing them the math and the evidence behind it.

Here’s how that conversation might go:

-

Lead with Your Comps: Start with the strongest evidence you have—comparable vehicles for sale right now, in your area. You could say, "I appreciate you sending that over. I did some local market research and found three similar 2021 Honda CR-V EX-L models within a 75-mile radius. Their asking prices are between $28,500 and $29,200."

-

Point Out What They Missed: The insurer's valuation report often defaults to a base model. Gently correct this. "I also noticed your report seems to be for the standard trim. My CR-V had the Technology Package and the panoramic sunroof, which were significant upgrades."

-

Document Recent Investments: Did you just put money into the car? Now's the time to bring it up. "We also just put on a brand-new set of tires and replaced the battery three months ago. I have the receipts here, and it came to over $1,400."

For a deeper dive into the tactics behind a successful negotiation, these powerful negotiation strategies offer some fantastic, real-world advice that applies perfectly here.

Key Insight: Frame this as a collaborative effort. You're not accusing them of lowballing you (even if they are). Instead, you are presenting new evidence to help them arrive at a more accurate number.

What if the adjuster won't budge? Don't lose your cool. Politely ask them to email you the specific comparable vehicles they used to justify their offer. Often, you'll find they are from distant locations or are not truly comparable models.

If you’re still at a standstill, remember the appraisal clause in your policy. It's your contractual right to invoke this clause as a last resort to get an independent, third-party valuation.

Costly Missteps That Can Sink Your Total Loss Claim

When your car is declared a total loss, it’s easy to feel rushed and overwhelmed. But a few common mistakes can leave you with a settlement that's thousands less than what you deserve.

The biggest blunder? Accepting the insurance company's first offer without a second thought. You need to see that initial figure for what it truly is: their opening bid in a negotiation, not the final word.

Another easy way to lose money is by forgetting about recent upgrades. Did you spend $1,200 on a great set of tires a few months back? What about that $800 you dropped on a new audio system? If you don't have receipts and don't bring them up, the adjuster's valuation won't include them, and that money is gone.

Don't Overlook the "Hidden" Fees

It’s natural to focus on your car's market value, but the settlement isn't just about the vehicle itself. Most states require the insurance payout to cover the "extras" you'll face when buying a replacement.

Make sure your settlement includes funds for:

- Sales tax on the new car

- Title transfer fees

- Vehicle registration costs

Failing to check that these are included is like willingly walking away from money you're owed.

A Pro Tip From Experience: The insurance game is all about data. The absolute best way to counter a lowball offer is to walk into the conversation with your own detailed valuation already in hand. Don't wait for their number; build your case first.

It's a tough world out there for insurers, too. Rising vehicle complexity and soaring repair costs—up an average of 40% since 2021—are pushing more cars into the "totaled" category. They’re using sophisticated software to manage these claims, which is why your own data-backed evidence is so crucial. You can learn more about these global auto insurance market trends and see what you're up against.

Lastly, don’t be too quick to back down. If you've used a total loss calculator and found comparable vehicles selling for more, you have a solid foundation. Present your findings calmly and professionally. The key to getting the full and fair amount you're entitled to is knowing your car's true worth and being prepared to advocate for it.

Your Top Total Loss Questions, Answered

Going through a total loss claim can feel like you're navigating a foreign country without a map. Once the initial shock of the accident subsides, the practical questions start piling up, and getting straight answers is the only way to get your bearings.

Let's cut through the jargon and tackle some of the most common concerns we hear from people in your exact situation. Understanding these key points is your first step toward getting through this and back on the road.

Can I Keep My Car if It’s a Total Loss?

Believe it or not, yes—in most states, you can choose to keep your vehicle. This is what the industry calls “owner retention.”

If you go this route, the insurance company will calculate the car's Actual Cash Value (ACV), then subtract what they would have received by selling the wreck at a salvage auction. You get a check for the difference.

But here’s the reality check: your car will be branded with a salvage title. This is a permanent red flag that makes the car incredibly difficult to insure or sell later on. To make it road-legal again, you'll need to complete significant repairs and pass a rigorous state safety inspection.

What if I Owe More Than My Car is Worth?

This is a tough spot to be in, and it's more common than you'd think. It's called being "upside-down" or "underwater" on your loan. The insurance company's job is to pay you for the car's current market value (the ACV), not what you happen to owe on your loan. You are still on the hook for the remaining balance.

This is the exact scenario Guaranteed Asset Protection (Gap) insurance was created for. If you bought Gap coverage when you first financed the car, it's designed to cover that "gap" between the ACV payout and your loan balance. Without it, that difference comes straight out of your wallet.

Expert Tip: Dig out your original loan paperwork right away. Finding out you have Gap insurance can be a massive financial relief.

How Long Does a Total Loss Settlement Usually Take?

There's no single answer here, but you can generally expect the process to take several weeks. A few things can really influence the timeline.

- Your Insurer's Workload: Some adjusters and departments are simply faster than others.

- The Complexity of Your Claim: A clear-cut case moves much quicker than one where you're disputing the value.

- How Fast You Respond: Getting documents back to your adjuster promptly can shave days, or even weeks, off the process.

If you decide to push back on their initial offer using reports from a total loss calculator and your own market research, be prepared for the timeline to stretch. Staying organized and persistent is the best way to keep things moving.

When you're fighting a lowball offer, you need a heavyweight in your corner. Total Loss Northwest provides certified auto appraisals that give you the evidence needed to make insurance companies pay the fair, accurate value of your vehicle. Don't let them undervalue your claim. Find out how we can help at https://totallossnw.com.