When an insurance company declares your car a total loss, they don't look at what you originally paid for it. They don't even consider how much you still owe on your loan. Instead, they calculate its Actual Cash Value (ACV)—the fair market value of your vehicle the moment before the accident happened.

Decoding Your Car's Actual Cash Value

Think of Actual Cash Value as the price a real person in your local area would have been willing to pay for your car in its pre-accident condition. This is the cornerstone of how insurers value a total loss. The goal isn't to get you a brand-new car; it's to put you back in the same financial spot you were in just before the crash.

This is often where the surprise comes in. Many people find the ACV offer is much lower than they anticipated, and the primary culprit is almost always depreciation. The second you drive a new car off the lot, it starts losing value. Every mile you drive, every year that passes, and every bit of normal wear and tear chips away at its worth.

The simplest way to think about ACV is this: it's what it would cost to replace your car today, minus all the depreciation it has accumulated over time. It's a snapshot of what your car was worth on the open market at a very specific point in time.

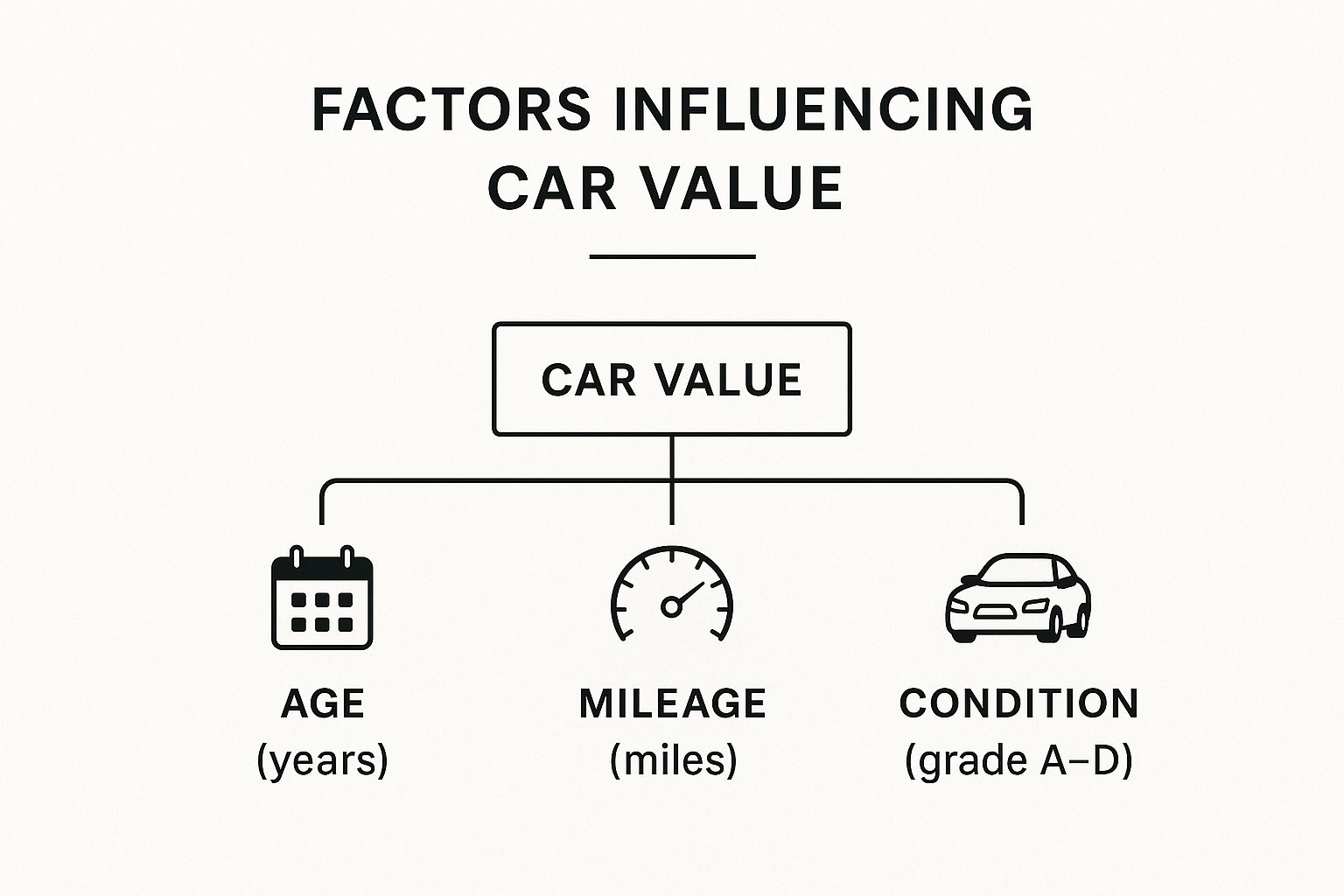

To nail down that number, adjusters look at a handful of key factors that paint a complete picture of your car's value and how desirable it would be to a potential buyer.

What Adjusters Look For

The final ACV calculation is a blend of several components, but they all boil down to one question: what was your specific car worth? Here's how they figure that out:

- Your Car's Condition: This is the big one. The physical state of your car—dents, dings, rust, interior stains, and tire tread—accounts for a massive 70-80% of its overall value. A pristine, garage-kept car is simply worth more than one that's seen better days.

- Local Market Trends: What are similar cars actually selling for in your city or region? Supply and demand, recent sale prices for the same make and model, and even the time of year can influence the remaining 20-30% of the value.

- Mileage and Age: These are the classic drivers of depreciation. Generally, the older the car and the more miles on the odometer, the lower its value.

- Maintenance Records: Can you prove the car was meticulously cared for? A complete service history shows an adjuster that your vehicle was in excellent mechanical shape, which can definitely help boost its ACV.

We've put together a table to summarize these key valuation points.

Key Factors in Actual Cash Value (ACV) Calculation

This table breaks down the primary components insurance companies consider when determining your car's value.

| Valuation Factor | What It Means for Your Car's Value |

|---|---|

| Physical Condition | The single biggest influence. Adjusters assess everything from the paint and body to the interior and tires. Better condition equals higher value. |

| Market Data | Your car's value is tied to what similar vehicles are selling for in your specific area. This includes local supply and demand. |

| Mileage & Age | Core drivers of depreciation. Higher mileage and older model years almost always lead to a lower ACV. |

| Maintenance History | A well-documented service record can prove the vehicle was well-maintained, potentially increasing its value. |

Understanding these factors demystifies the process and gives you a much clearer picture of how the insurance company arrived at their settlement offer.

Getting a handle on ACV is the first step in navigating a total loss claim. To go even deeper, be sure to read our guide on what is actual cash value of my car.

The Three Pillars of Vehicle Valuation

Ever wonder how an insurance company actually lands on a specific number for your car's value? It’s not a random guess. Their process is surprisingly methodical, built on what I call the three pillars of valuation: establishing a baseline, accounting for depreciation, and adjusting for the local market.

It all begins by finding a baseline value. Insurance carriers don't just use consumer-facing sites like Kelley Blue Book. They subscribe to powerful, industry-specific databases like CCC ONE or Audatex. Think of these as massive data engines that crunch the numbers on millions of real-world vehicle sales, dealer asking prices, and auction results, all filtered down to your specific geographic area. This gives them a solid, data-backed starting point for a car just like yours.

Pillar 1: Accounting for Depreciation

With a baseline set, the next step is factoring in depreciation. A car’s value starts to drop the second it drives off the lot. Every mile you add and every year that goes by chips away at its original worth. This isn’t a penalty; it’s just the reality of wear and tear on any complex machine.

This image really breaks down the biggest factors that cause a car's value to decline over time.

As you can see, age and mileage are the heavy hitters. The adjuster's job is to look at your car’s specific history—its age, the odometer reading, and its overall condition before the accident—and calculate just how much value it has lost since it was new.

Pillar 2: Adjusting for the Local Market

The final pillar, and one that many people overlook, is the local market adjustment. A car's worth isn't the same everywhere in the country. This is a core part of figuring out what is fair market value in your specific city or town.

A rugged 4×4 truck is going to be worth a lot more in the snowy mountains of Washington than it would be in sunny, flat Florida. On the flip side, a convertible will fetch a much higher price in Miami than it ever could in Seattle.

This is where the adjuster puts on their local economist hat. They fine-tune the value by analyzing supply and demand right where you live.

They’re looking at things like:

- Regional Popularity: Is your car a hot seller in your area?

- Recent Sales Data: What have similar cars actually sold for nearby in the past 90 days?

- Dealer Inventory: Are local dealerships overflowing with cars like yours, or is yours harder to come by?

This last step is crucial because it roots the valuation in reality—what a willing buyer in your community would have likely paid for your exact car, right before the loss. By combining a data-driven baseline, subtracting for use and age, and then refining it with local market intelligence, the insurer paints a complete picture of your car's value.

How Your Car's Condition Impacts the Final Offer

While market data gives the insurance company a starting point for your car's value, the actual physical condition of your vehicle is what really dials in the final number. This is where the process gets personal. The adjuster’s inspection—or the photos you send in—is what separates your car from every other one just like it.

Think of it this way: two identical houses built side-by-side can sell for wildly different prices. One might have a modern kitchen and a new roof, while its neighbor has peeling paint and a leaky faucet. It's the exact same logic for your car. Its real-world condition is what truly matters.

The Adjuster's Grading System

Insurance adjusters aren't just winging it. They follow a standardized grading system to score everything from your car's engine to its interior. This process is meant to be consistent, but it also means every little flaw gets put under a microscope and can lower the final valuation.

Here's what they're typically looking for:

- Exterior Damage: This covers the obvious stuff like dings, scratches, rust, and faded paint. Mismatched body panels from a previous repair also get noted.

- Interior Wear and Tear: Stained carpets, rips in the seats, cracks in the dashboard, or broken knobs all tell a story of a car that’s seen better days.

- Tire Tread Depth: Bald tires are an immediate red flag for an expense a new owner would have to cover. Adjusters will actually measure the tread and adjust the value down if they’re worn.

- Mechanical Soundness: They'll listen for any weird engine noises or look for visible leaks that existed before the accident that caused the claim.

A car in "excellent" condition might get a bump up in value, while one graded as "poor" could see a major reduction from that initial market baseline. This condition assessment is probably the most hands-on and impactful part of the entire valuation.

Proving Your Car's Worth

When it comes to getting a fair offer, your paperwork is your best friend. It’s not enough to just tell the adjuster your car was in great shape—you need to show them. Meticulous maintenance logs, receipts for a recent brake job, or an invoice for those new tires you just bought can directly counter any deductions the adjuster might try to make.

On the flip side, a rough history can be a huge liability. A salvage title, for example, can tank a car's value by 20% to 40% right off the bat, as it signals a history of major damage. If the insurer declares your car a total loss, figuring out how to sell a salvage car is the next step you'll face.

Ultimately, your car’s history and condition tell a story. Even a minor previous accident can affect its future resale price, which is why it's so important to understand the concept of https://totallossnw.com/diminished-value-after-car-accident/. The adjuster is reading every single chapter.

The Role of AI in Modern Vehicle Valuations

If you’re picturing an insurance adjuster thumbing through a dusty guidebook to find your car's value, you might want to update that image. The reality today is far more sophisticated. The process has moved from a somewhat subjective art to a data-driven science, all thanks to artificial intelligence (AI).

These powerful systems are now the engine behind most modern valuations. Instead of just pulling a few local comps, AI platforms digest enormous amounts of data in the blink of an eye. We're talking millions of historical sales records, recent auction results, what dealers are asking for similar cars, and even repair cost data from all over the country.

This allows insurers to set a precise baseline value for a vehicle like yours with a level of consistency that a human simply couldn't replicate. The result is a valuation process that’s faster, more standardized, and less vulnerable to one person's opinion or bias. It’s a huge step forward in making sure your settlement starts from a place of solid market evidence.

From Data Points to Dollar Amounts

But AI doesn't just look at the final sale price. It goes much deeper, piecing together all the little things that nudge a car's value up or down.

These smart systems are trained to weigh key variables that a manual process might overlook:

- Geographic Demand: An AI can instantly see that a specific 4×4 truck sells for a premium in Colorado but is less sought-after in Florida, and it will adjust the value based on your location.

- Feature Packages: The system knows exactly how much value a premium sound system or a panoramic sunroof adds to your specific model—details that are easy to miss.

- Depreciation Curves: Instead of using a generic formula, it analyzes the unique depreciation curve for your car’s make and model, leading to a much more accurate estimate.

This technology has truly changed the game. By analyzing massive datasets, AI helps insurers estimate a car’s current worth with incredible precision. This efficiency is a big reason why the vehicle insurance market, which was valued around USD 217.5 billion in 2024, is expected to nearly double by 2034. If you're interested in the numbers behind this growth, you can dive into these vehicle insurance market trends and projections.

AI as a Tool for Fairness and Fraud Detection

Beyond just crunching numbers for valuations, AI also acts as a silent guardian of the entire claims process. These systems are incredibly good at spotting red flags and inconsistencies that might point to fraudulent activity.

For example, if a damage report doesn't quite match the physics of the described accident, the AI can flag it for review. This helps insurers stop fraudulent payouts, which in turn protects all of us from the higher premiums that fraud inevitably causes.

Ultimately, this shift toward data and AI creates a more transparent and fair system for everyone. By taking out the guesswork and grounding the valuation in hard data, AI helps ensure the settlement offer you receive is a true, objective reflection of what your vehicle was worth right before it was damaged.

What to Do When You Disagree with the Offer

Getting a settlement offer that feels like a lowball is frustrating, but don't panic. That first number from the insurance company isn't the final word—it's just their opening bid. You have the right to question it, push back, and negotiate for what your car was actually worth moments before the accident.

Your first step? Politely but firmly ask the adjuster for a complete copy of their valuation report. This document is your roadmap to their logic. It breaks down exactly how the insurance company valued your car, listing the comparable vehicles (or "comps") they used, the features they included, and every deduction they made. Go through it with a fine-tooth comb. Did they forget about your premium sound system or list it as a base model? Mistakes happen, and finding them is your first point of leverage.

Building Your Counter-Offer

Once you have their report, it’s time to assemble your own evidence. This isn't about what you feel your car was worth; it's about what you can prove. Your job is to present a strong, fact-based case that corrects their assessment.

Here's how to gather the proof you need:

- Find Your Own Comps: Hit the local online car listings. Look for the same make, model, year, and trim level as your car. You want apples-to-apples comparisons, so pay close attention to mileage and overall condition. Screenshot every listing that supports a higher value.

- Document Recent Upgrades: Did you just drop $800 on a new set of tires? Replace the brakes? Get a new battery? Dig up those receipts. These aren't just maintenance items; they directly contribute to the car's cash value and should be part of the calculation.

- Showcase Excellent Condition: If you have any recent photos of your car from before the crash, send them over. Pictures of a spotless interior or a gleaming, wax-finished exterior can prove your car was in better-than-average shape, justifying a higher value.

Invoking the Appraisal Clause

What if you've presented your evidence and the adjuster still won't budge? If you're truly at a stalemate, check your policy for a powerful but often-overlooked provision: the Appraisal Clause. This is your nuclear option for settling a valuation dispute.

The Appraisal Clause is basically a dispute resolution system. You hire your own independent appraiser, the insurance company uses theirs, and if they can't agree, the two appraisers select a neutral "umpire." A final, binding value is set when any two of the three agree.

This move takes the insurance company's internal software out of the picture. It forces them to the table with an independent expert. Yes, you have to pay for your own appraiser, but when you're thousands of dollars apart, it’s often the best—and sometimes only—way to get a fair shake.

A Few Common (and Frustrating) Questions

Even with a good grasp of the process, a total loss claim can still leave you with some tough financial pills to swallow. Let’s walk through some of the most common hangups drivers run into, so you know exactly what to expect.

Why Is My Payout Less Than My Loan?

This is a gut punch, and unfortunately, a common one. The settlement check arrives, but it's not enough to cover what you still owe the bank. This happens when you’re “upside down” on your loan, meaning your car’s market value is less than your loan balance.

So, why the disconnect? Your insurance company’s job is to pay you the car’s Actual Cash Value (ACV)—what it was worth the moment before the crash. They aren’t responsible for the loan you took out to buy it. New cars, in particular, lose value much faster than you can pay down a loan. A car can drop 10% in value in the first month alone, while your first few payments have barely touched the principal.

This is precisely why Guaranteed Asset Protection (GAP) insurance exists. It’s an optional add-on that covers the "gap" between your ACV payout and your loan balance. Without it, you could be left making payments on a car that's already in a salvage yard.

What's the Difference Between ACV and Replacement Cost?

These two terms sound similar, but they represent a huge difference in your payout. The vast majority of standard auto policies are based on Actual Cash Value (ACV). As we've covered, this is today’s market value for your car, factoring in all the depreciation it has accumulated over time.

Replacement Cost Value (RCV), on the other hand, is a premium and much rarer type of coverage. It pays you enough to buy a brand-new version of the same car, with no deduction for depreciation. As you can imagine, this makes for a much higher payout, which is why RCV policies are more expensive and usually only offered for the first year or two of a brand-new car's life.

Do My Aftermarket Upgrades Increase My Car's Value?

This is a tricky one. The short answer is: maybe a little, but almost never for what you paid for them.

While a nice stereo system or a quality set of all-weather tires might add some value, some modifications can actually hurt it. Heavily personalized or performance-based upgrades can narrow the car's appeal to an average buyer, which can lower its market value.

The real key here is having the right coverage. If you don't have a specific add-on for Custom Parts and Equipment (CPE), most insurers will only pay for the factory-original parts your upgrades replaced. That means your $3,000 custom wheel and tire package might only get valued at the $800 it would cost to replace the stock set. If you've put money into mods, you have to declare them and get CPE coverage.

How Can I Get the Highest Valuation Possible?

To get the best possible settlement, you need to be proactive and organized. Documentation is your best friend. You have to build a strong case that proves your car was in excellent, well-maintained condition right before the accident.

Here's how to make your case:

- Gather Your Maintenance Records: Every single receipt helps. Oil changes, new brakes, tire rotations—a thick stack of paperwork is undeniable proof of a well-cared-for vehicle.

- Showcase Recent Investments: Did you just buy a new set of tires or replace the battery a month ago? Hand over those receipts. Those are direct, recent contributions to your car's cash value.

- Find Solid Local Comps: Do your own homework. Find listings for cars identical to yours—same year, make, model, and trim—that are for sale at dealerships in your immediate area. This gives you a real-world benchmark to push back against a lowball offer.

If you’ve done all this and still feel the insurance company's offer is just too low, you don’t have to take it. At Total Loss Northwest, our certified appraisers specialize in fighting for the true value of your vehicle. We invoke the Appraisal Clause in your policy to force a fair, data-driven settlement based on real market conditions—not the insurer's self-serving software. Visit us online to see how we can help you get the money you're rightfully owed.