Let's be honest: a car accident is a huge headache, but the pain doesn't stop once the repairs are done. The moment a collision shows up on your car's record, its value takes a permanent hit. This is called diminished value, and it can slash your car's resale price by anywhere from 10% to over 30%.

Even with perfect, high-quality repairs that make your car look brand new, it will never be worth the same as an identical car with a clean history. That's the harsh reality of the used car market.

What Diminished Value Means for You

Picture this: you're shopping for a used car and find two identical models. Same year, same mileage, same color, same features. One has a squeaky-clean vehicle history report. The other was in an accident last year but was professionally restored by a top-rated body shop.

Which one are you going to buy? Most people would instantly choose the one with no accident history. To even consider the repaired car, a savvy buyer would demand a steep discount. That discount is the diminished value in action. It’s the market's way of pricing in the risk and stigma that now comes with your car.

The loss isn't just about what was spent on repairs. It's about the nagging questions that pop into a future buyer's mind. Was the frame really straightened perfectly? Are there underlying issues waiting to surface down the road? This uncertainty is what really drags down the price tag.

What Determines How Much Value Your Car Loses?

So, how much value are we talking about? It's not a single number; it's a sliding scale based on a few key factors. Knowing what these are is the first step to understanding what your diminished value claim might be worth.

We've put together a table to break down the most important elements that contribute to your car's post-accident value loss.

Key Factors That Reduce Your Car's Value Post-Accident

| Factor | Impact on Value | Example |

|---|---|---|

| Severity of Damage | High | A minor fender-bender causes less value loss than a collision that required frame straightening or airbag deployment. Structural damage is a major red flag for buyers. |

| Quality of Repairs | High | Repairs done at a certified shop using original manufacturer (OEM) parts help minimize value loss. Shoddy work with aftermarket parts will make it much worse. |

| Vehicle Age & Value | Medium-High | Newer, more expensive, or luxury cars lose a much larger dollar amount. A 15% loss on a $50,000 SUV is a much bigger hit than 15% on a $10,000 sedan. |

| Vehicle History | Medium | A car with a pristine record before the accident will see a more significant drop in value compared to a car that already had a previous accident on its report. |

| Make and Model | Medium | High-end brands like Porsche or Mercedes-Benz often see a steeper percentage drop, as buyers in that market demand perfection and are wary of any accident history. |

Ultimately, the more significant the accident and the newer/more valuable the car, the greater the diminished value will be.

In short, diminished value is the invisible cost of a car accident. It's the difference between what your car was worth right before the crash and what it's worth now, simply because it has a documented collision in its past.

What Is Diminished Value, Really?

Let's start with a simple thought experiment. Picture yourself on a used car lot, looking at two identical vehicles. They're the same make, model, year, and have nearly the same mileage. One has a squeaky-clean vehicle history report. The other was in an accident a few months back, but the repairs are so good you can't even tell.

Which one do you buy?

If you're like pretty much every other savvy car buyer out there, you'd go for the one with the clean record. To even consider the other car, you'd expect a hefty discount. That price gap—that discount you'd demand—is the perfect illustration of diminished value.

It’s the permanent loss in a car's resale value that sticks to it simply because it now has an accident on its record. Even if the repairs are absolutely perfect, that collision history is a scar that makes the car less attractive to future buyers. This is the core concept you need to understand when figuring out how much an accident devalues your car.

The Three Flavors of Diminished Value

To really get a handle on this, it helps to know that diminished value isn't just one thing. It's actually broken down into three distinct types, and each one plays a part in what happens after a crash.

-

Immediate Diminished Value

This is the value drop that happens the second your car is hit, before a single tool has touched it. It's simply the difference between what your car was worth one minute before the accident and what it's worth sitting there, crumpled and damaged. For the most part, your insurance company covers this when they pay the body shop for repairs. -

Inherent Diminished Value

This is the big one. It's the most common and, frankly, the most important type for most claims. Inherent diminished value is the loss in value that remains after your car has been professionally repaired and looks brand new again. It’s a direct result of the stigma now attached to your car’s VIN. That accident is now part of its permanent record on services like CarFax or AutoCheck, and every potential buyer will see it. -

Repair-Related Diminished Value

This last type comes into play when the repair job itself is shoddy. If the shop used cheap aftermarket parts, couldn't match the paint color properly, or left other signs of a clumsy fix, the car's value takes an extra hit. This loss is caused by the quality of the repair, not just the fact that an accident happened.

For most people filing a claim, the fight is over Inherent Diminished Value. It's the financial damage you're left with even when your car looks and drives just like it did before, all because its history is no longer clean.

Why a Blemish on a Car's History Is a Big Deal

Every car depreciates. It's a fact of life. Your average family sedan can lose around 43% of its value in just three years from age and mileage alone. You can discover more insights about vehicle depreciation rates to see how this plays out across different models.

When an accident happens, diminished value piles another layer of depreciation right on top. This extra loss can be anywhere from 10% to 30% of the car's pre-accident value, depending on the car itself and how bad the damage was.

That permanent black mark on the vehicle’s history creates doubt. A future buyer will always be asking themselves, "Is there hidden damage? Will these repairs last?" Because of that risk, they will always offer less for a car with a reported accident than for an identical one without. A diminished value claim is your tool to recover that financial loss.

What Determines the Exact Drop in Your Car's Value?

Knowing your car has lost value is one thing, but figuring out exactly how much is a whole different ball game. It’s not just one number; it's a specific calculation that hinges on the unique details of the accident and your car.

Think of each factor like a dial. The severity of the crash, the quality of the repairs, your car's age—each one gets turned up or down, ultimately setting the final diminished value amount. A minor parking lot scrape on a ten-year-old sedan is a blip on the radar. A major collision in a brand-new luxury SUV? That's a serious financial hit.

The Severity and Nature of the Damage

First and foremost, the biggest driver of diminished value is how badly the car was crunched. A potential buyer's perception changes dramatically depending on whether it was a simple fender-bender or something that compromised the car’s very frame.

-

Cosmetic Damage: This is the low end of the scale. Think scrapes, small dings, or minor bumper scuffs. These repairs are usually simple and don't raise red flags about the car's safety, resulting in the smallest value drop.

-

Moderate Damage: Here, we're talking about replacing entire body panels like doors, fenders, or the hood. This signals a more significant impact, makes buyers nervous, and leads to a much bigger hit to the car's resale value.

-

Structural and Frame Damage: This is the kiss of death for a car's value. Any accident serious enough to bend the frame or result in a salvage title will cause a massive, permanent devaluation. For many buyers, a car with known frame damage is an absolute deal-breaker, no matter how well it was repaired.

Another huge red flag is airbag deployment. If an accident was forceful enough to set off the airbags, it gets recorded on the vehicle history report as a severe event, automatically leading to a much steeper loss in value.

Your Vehicle's Age and Pre-Accident Value

What was your car worth moments before the crash? This is the next critical piece of the puzzle. It’s a simple rule: newer, more valuable cars have much more to lose. They take a bigger hit both in raw dollars and as a percentage of their total worth.

For example, a 15% value loss on a $50,000 luxury car is a painful $7,500. That same 15% hit on a $12,000 daily driver is only $1,800.

Insurance appraisers and potential buyers understand this logic. The more a car is worth, the more an accident will take away. It's the same reason a low-mileage car is penalized more heavily—the expectation was that it was in near-perfect condition.

This entire calculation starts with your car's pre-accident market value. To get a better handle on this, our guide explains all the details of figuring out your car's actual cash value, which is the baseline for any diminished value claim.

The Quality of Repairs and Parts Used

How your car was put back together after the accident is hugely important. High-quality repair work can help minimize your losses, but a shoddy job can make a bad situation even worse.

A smart buyer will always ask for the repair receipts. They want to see proof that the shop used Original Equipment Manufacturer (OEM) parts, not cheap aftermarket knock-offs.

A professional repair from a certified shop is your best defense. Things like mismatched paint, panels that don't line up perfectly, or lingering dashboard warning lights are dead giveaways of a cut-rate job. If you can show proof of top-tier work, you can reassure a buyer and protect your car's value. Without it, they'll assume the worst and knock their offer down accordingly.

How to Calculate Your Car's Diminished Value

So, how do you actually figure out the dollar amount your car has lost? This is the most important part of building your claim, and you can't just pull a number out of thin air. You need a solid, evidence-based approach to arrive at a figure that's both fair and defensible.

While there isn't one single magic formula, there are a few established methods for getting to a realistic number. Let's start with the one the insurance company will likely use.

The Infamous Rule 17c

Often, the first calculation an insurance adjuster makes is based on a guideline known as "Rule 17c." This formula came out of a court case in Georgia and has become a go-to for insurers because, frankly, it tends to produce very low numbers.

Here’s the gist of it: Rule 17c starts by capping the maximum diminished value at 10% of your car's pre-accident value. Then, it applies two "multipliers"—one for the severity of the damage and another for the vehicle's mileage—to whittle that number down even further.

For instance, if your car was worth $30,000 before the crash, the formula immediately puts a $3,000 ceiling on your claim. From there, it chips away at that amount based on the damage and odometer reading. It’s a tidy formula for them, but it rarely reflects the true market loss for you.

Expert Tip: Think of the 17c formula as the insurance company's opening bid in a negotiation. It's their starting point, not the final word on what your claim is actually worth.

Better Ways to Prove Your Car's Lost Value

Since the 17c formula is designed to favor the insurer, you’ll need to do your own homework to justify a higher, more accurate amount. Simply accepting their number means you're almost certainly leaving money on the table.

Here are three far more effective ways to establish your car's true diminished value:

-

Get Real-World Trade-In Quotes: This is one of the most powerful pieces of evidence you can get. Head to a few reputable car dealerships and ask for a trade-in appraisal. Be completely transparent about the accident and show them the repair records. Ask them for two numbers: one for your car as-is, and one for an identical vehicle (same make, model, year, and mileage) with a clean history. The gap between those two figures is your diminished value in black and white.

-

Use Online Estimation Tools: While not a replacement for a formal appraisal, online calculators can give you a solid ballpark estimate to start with. Many sites offer tools specifically for this purpose. For a quick look, you can use a car value after accident calculator to get an instant estimate and see how various factors affect the result. This data helps you know what to expect.

-

Hire a Certified Appraiser: This is the gold standard for proving your case. A licensed, independent auto appraiser will perform a detailed inspection of your vehicle and its repair documentation. They’ll then analyze local market data to produce a comprehensive report that formally states the diminished value. This professional document carries serious weight in negotiations and is your single strongest piece of leverage.

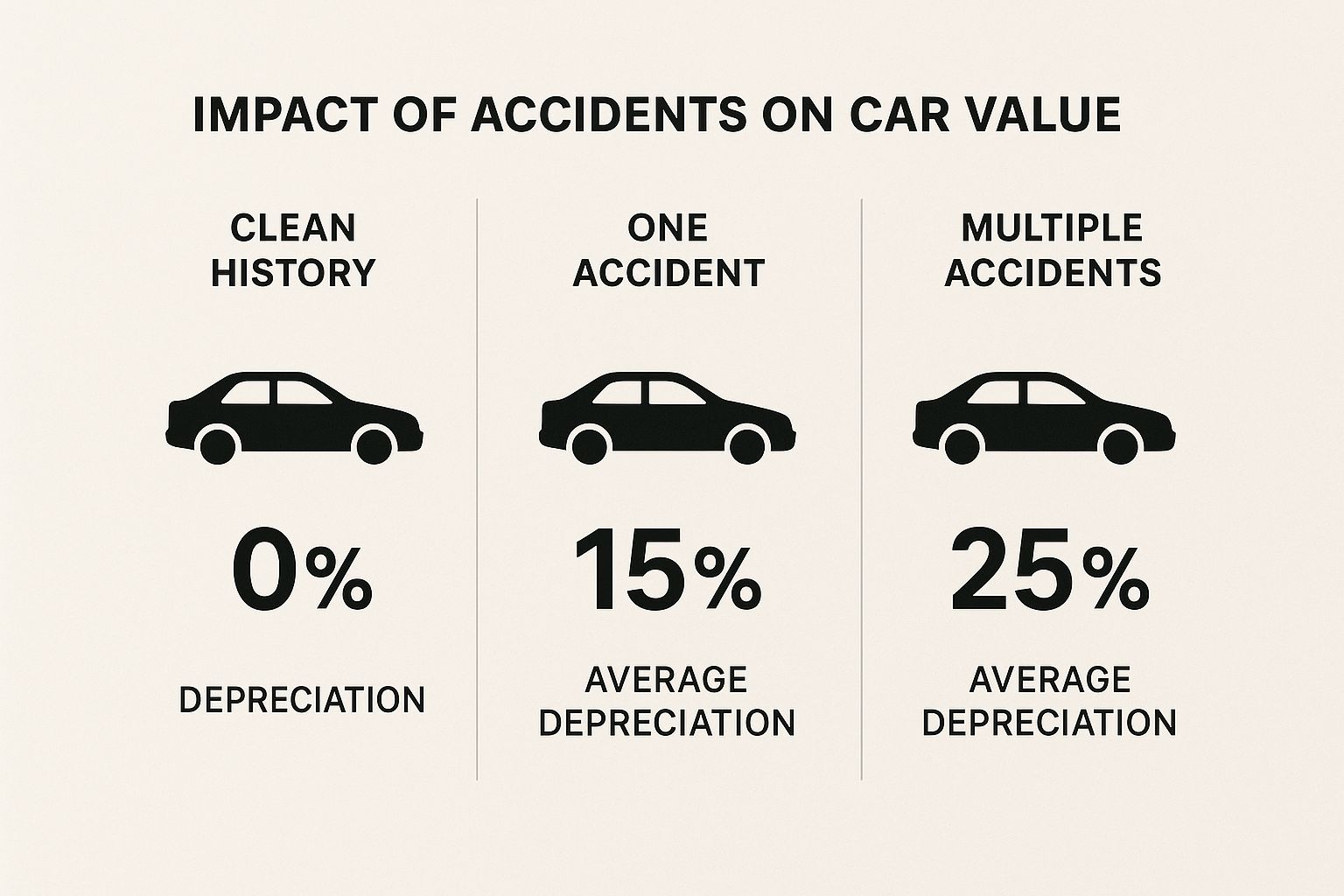

This image shows just how much of a financial hit a car's value takes after an accident is reported.

As you can see, a single accident causes a major drop, but multiple incidents make the financial loss even worse.

Comparing Methods to Calculate Diminished Value

Deciding how to prove your claim depends on your situation. Here’s a quick look at the different ways to estimate your car's loss in value, highlighting the pros and cons of each approach.

| Method | How It Works | Pros | Cons |

|---|---|---|---|

| Rule 17c Formula | An insurer-favored calculation that caps value loss at 10% of the car's pre-accident value, then reduces it with damage/mileage multipliers. | Simple and provides a quick number. | Almost always results in a very low valuation; heavily biased toward the insurance company. |

| Trade-In Quotes | Get written offers from dealerships for your repaired car vs. an identical one with no accident history. The difference is the DV. | Provides tangible, real-world evidence from market experts. Hard for insurers to dispute. | Can be time-consuming to visit multiple dealerships; offers can vary. |

| Online Calculators | Web-based tools that use algorithms and market data to provide an instant, automated estimate of your vehicle's diminished value. | Fast, free, and gives a great starting point for understanding your potential loss. | Not a formal appraisal; a general estimate that won't hold up as primary evidence on its own. |

| Certified DV Appraiser | A licensed professional conducts an in-depth inspection and market analysis to produce a formal, legally recognized report. | The most authoritative and credible evidence you can have. Carries significant weight in claims. | Costs money upfront (typically a few hundred dollars); may be overkill for very minor claims. |

Ultimately, the best strategy is often to combine these methods. Start with an online calculator for a baseline, get a couple of trade-in quotes for real-world proof, and if the stakes are high, bring in a certified appraiser to seal the deal. This layered approach gives you the documentation you need to counter a lowball offer and successfully argue for the full compensation you deserve.

Filing a Successful Diminished Value Claim

Knowing exactly how much value your car has lost is a huge first step, but it’s really only half the battle. Now comes the hard part: turning that number into a successful insurance claim. It can definitely feel like a daunting process, but if you go in prepared, you can confidently ask for the money you're rightfully owed.

The first thing to understand is that your ability to file a diminished value claim almost always hinges on who caused the accident. In most states, you can only file a claim against the at-fault driver's insurance policy. This is what's known as a third-party claim. Trying to file a "first-party" claim against your own insurance is rarely an option, with a few exceptions in certain states.

Gathering Your Essential Documentation

Before you even pick up the phone to call the insurance company, you need to build a solid case. Think of it like a detective gathering evidence for a trial—the more proof you have, the stronger your argument will be. An insurance adjuster can easily brush aside a disorganized claim.

Your main goal here is to hand them an undeniable file that clearly spells out the value your car has lost.

Here’s a checklist of the core documents you'll need to pull together:

- Proof of Value: You have to establish what your car was worth right before the crash. Use trusted sources like Kelley Blue Book or NADAguides to set this baseline.

- Repair Records: Get a copy of every single invoice and receipt from the body shop. These documents need to detail all the work that was done and, importantly, whether they used original (OEM) or aftermarket parts.

- Accident Report: The official police report is crucial. It lays out the facts of the accident and, most of the time, clearly identifies who was at fault.

- Professional Appraisal Report: This is your secret weapon. A detailed report from a certified diminished value appraiser provides an expert, unbiased assessment of your loss, and it's something insurers find very difficult to ignore.

Industry data consistently shows that even after perfect repairs, a vehicle with an accident on its record can permanently lose an additional 10% to 20% of its market value. Why? Because savvy buyers are wary of a car's history, and that stigma is a real factor that goes beyond normal depreciation.

Crafting and Submitting Your Demand Letter

Once you have all your evidence in order, it's time to formally state your case. You'll do this by sending a demand letter to the at-fault driver's insurance adjuster. Keep the letter professional, concise, and straight to the point.

Your demand letter must clearly state the total amount of diminished value you're claiming and mention the evidence you've gathered to back it up. Now, be ready for some pushback. The adjuster's job is to minimize how much the insurance company pays out, so their first offer will almost certainly be low—they often lean on a flawed, insurer-friendly calculation called the 17c formula.

Don't let a lowball offer discourage you. Respond politely but firmly with your counteroffer, pointing directly to the data from your professional appraisal or trade-in quotes. If you hit a wall and feel the insurer isn't negotiating in good faith, it might be time to bring in an attorney who specializes in these types of cases.

For a more detailed walkthrough, check out our complete guide on how to file a diminished value claim.

Common Questions About Accidents and Car Value

Even after getting the basics down, you’re probably still left with a few nagging questions about how this all works in the real world. Let's dig into some of the most common ones people ask.

Does Even a Minor Reported Accident Hurt My Car's Value?

Yes, it absolutely does. As soon as a small fender-bender gets logged on a vehicle history report from a service like CarFax, it’s there for good.

While a minor scrape won't cause the same nosedive in value as a major collision, that accident history creates a stigma. Future buyers will see it and, almost without fail, use it as a powerful bargaining chip to talk you down on price. The simple truth is that any reported accident will have a negative impact on what your car is worth.

Can I File a Diminished Value Claim Against My Own Insurance?

This is where things get tricky, but the short answer is almost always no. Your own auto insurance policy is designed to pay for the cost of repairs, not for the drop in market value that happens after those repairs are done. This is what's known as a "first-party" claim, and it's typically excluded.

With very few exceptions (Georgia is a notable one), you can only file a diminished value claim against the at-fault driver's insurance company. This is called a "third-party" claim because you're seeking damages from the person who caused the loss.

What Is the Value Difference Between a Minor Accident and a Salvage Title?

The difference is staggering—we’re talking about two completely different leagues of value loss. A minor accident might knock 10% to 15% off your car's value. A car branded with a "salvage" or "rebuilt" title has fallen off a cliff.

A salvage title is issued when an insurance company decides a car is a total loss, usually because the repair costs were more than the car was worth. Even if it’s fixed up and passes a state inspection to get a "rebuilt" title, it has a permanent black mark. These vehicles often lose 50% or more of their original market value, and many dealerships and private buyers won't touch them at all.

Going head-to-head with an insurance company on a diminished value or total loss claim can be exhausting. But you don't have to just take their first lowball offer.

At Total Loss Northwest, our certified appraisers build ironclad, data-driven reports to fight for the true value of your vehicle. We know how to counter the tactics insurers use and get you the fair settlement you’re owed. Find out how we can help at https://totallossnw.com.