So, what exactly is a car insurance appraisal? Think of it as a professional, deep-dive valuation to pinpoint your car's exact worth a moment before an accident occurred. This number is everything when it comes to figuring out what the insurance company owes you, especially if your car is a total loss or has lost value even after being fixed.

Why a Car Insurance Appraisal Matters to You

Navigating an insurance claim after a crash can be a real headache. You're juggling paperwork, making calls, and then you hear the word "appraisal." What does that actually mean for your bottom line? It's not just a quick price lookup; it's a detailed investigation into your car's true value, considering everything from its condition to its specific features.

This process becomes the bedrock of your settlement in a couple of key situations. Getting a handle on these is the first step to making sure you're paid what you're rightfully owed.

When Is a Car Insurance Appraisal Necessary?

A formal appraisal usually comes into play when you and the insurance company are miles apart on what your car is worth. Let's look at the two main scenarios where this happens.

Here’s a quick summary of the two main situations that require a formal car insurance appraisal, helping you identify if this guide applies to your situation.

| Appraisal Trigger | What It Means | Your Goal |

|---|---|---|

| Total Loss Claim | The insurer has declared your car "totaled," meaning it costs more to fix than it's worth. | To get a settlement check that accurately reflects the car's pre-accident market value. |

| Diminished Value Claim | Your car has been repaired, but its resale value has dropped just because it has an accident on its record. | To get compensated for the "diminished value"—the money you've lost in market value. |

These two scenarios are where a professional, independent valuation becomes your most powerful tool.

An appraisal isn’t just about the damage you can see. It's about establishing a fair, pre-accident baseline. This figure, known as the Actual Cash Value (ACV), is what the insurance company is contractually obligated to pay you, and getting it right is critical for your financial recovery.

This valuation process is more important than you might think, especially as the auto insurance world gets bigger. With the global automobile insurance market expected to hit USD 1,276.1 billion by 2035, insurance companies are always looking for ways to manage their payouts. You can read more about the automobile insurance market's growth to see how these trends are shaping the industry.

Ultimately, a car insurance appraisal is your best tool for ensuring a fair outcome. It gives you an objective, evidence-backed number that can challenge an insurer’s initial offer, which, let's be honest, is often on the low side.

How the Car Insurance Appraisal Process Actually Works

So, you've filed a claim, and now the insurance company is sending out an appraiser. What happens next? It might seem like a black box, but the process is actually pretty straightforward. It all boils down to a methodical journey to land on a final number for your vehicle's value.

It all starts with the vehicle inspection. An appraiser will come out to look at your car in person, meticulously documenting its condition before the accident. They'll note the mileage, check for any special features, and look for any custom modifications you've made. While some insurers now use virtual inspections with photos and videos, nothing beats a hands-on review for catching all the details that add value.

After getting a good look at your car, the appraiser puts on their detective hat for the data analysis phase. Their main job here is to dig into the local market to see what cars just like yours have sold for recently.

The Key Ingredients of Your Car's Value

To get to that final Actual Cash Value (ACV), the appraiser blends their notes from the physical inspection with hard market data. It’s not just a guess; several key factors carry the most weight.

- Pre-Accident Condition: The appraiser will assess the vehicle's overall shape before the crash, accounting for any old dings, scratches, or wear and tear that were already there.

- Mileage: This one's simple. Lower miles almost always mean a higher value. The appraiser will see how your car's odometer stacks up against the local average for its specific year and model.

- Options and Features: Did you have the premium sound system? A sunroof? Leather seats? All those factory-installed extras add up and contribute to the final valuation.

- Recent Local Sales: This is the big one. The appraiser hunts for "comps"—comparable vehicles of the same make, model, and year that recently sold in your area—to set a realistic market price.

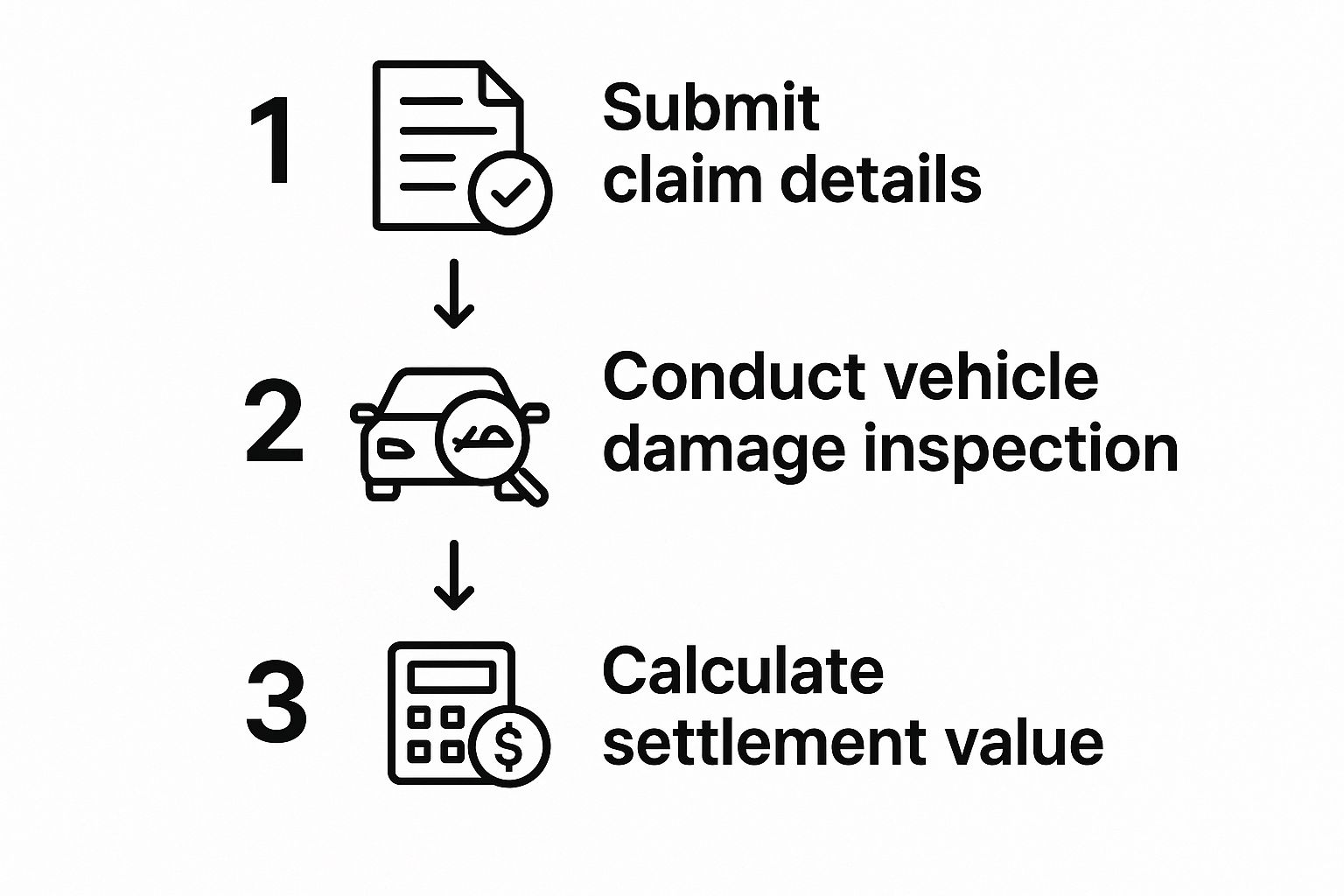

This handy infographic gives you a bird's-eye view of how the process flows, from filing the claim to getting the final number.

As you can see, it's a logical path from gathering the initial information to the final dollars-and-cents calculation.

Putting It All Together in the Final Report

Finally, the appraiser takes all this information—the inspection notes, the market research, the comps—and bundles it into a detailed valuation report. This document is your window into their logic. It should clearly break down how they landed on their number, listing the comparable vehicles they used and showing any adjustments made for your car's specific condition, mileage, or features.

It's worth noting that appraisal methods can differ, and some vehicles present unique challenges. For example, accurately valuing an electric vehicle takes a specialist who understands things like battery health and specific EV market trends. Getting familiar with this report is the critical first step in making sure you're getting a fair shake and knowing how to push back if the offer seems low.

The goal of a proper car insurance appraisal isn't just to find the cheapest comparable car on the market. It's to find the replacement cost—what it would genuinely cost you to buy a similar vehicle in similar condition right now.

Understanding Your Total Loss Appraisal Report

When you hear "total loss," the first image that comes to mind is probably a car twisted into a pretzel. But in the world of insurance, a total loss is an economic call, not a judgment on the car's physical state. It simply means your insurer has decided it costs more to fix your car than it was worth before the accident.

This is the exact moment a car insurance appraisal takes center stage in your claim. The insurance company runs the numbers to figure out your car's Actual Cash Value (ACV)—its fair market value a second before the crash. They then pit that number against the body shop's repair estimate. If the repair bill is higher, it’s totaled.

Decoding Your ACV Report

The valuation report the adjuster sends over can look intimidating at first, packed with jargon and numbers. But don't be discouraged. It all boils down to a few key pieces of information, and learning to read them is your first step toward getting a fair payout.

Think of this document as the insurance company's opening argument for what they believe your car was worth. You have every right to cross-examine it. To do that, you'll need to know what to look for.

Start by zeroing in on these three core components:

- Base Value: This is the starting price. It’s calculated by looking at "comps"—comparable vehicles that have recently sold in your area. The report should list these cars out, detailing their year, make, model, and mileage.

- Condition Adjustments: Next, the insurer will tweak that base value up or down based on your car's pre-accident condition. Unusually low mileage might add a few bucks, while existing dings, scratches, or heavy interior wear will knock the value down.

- Feature and Option Additions: Did your car have a sunroof, a premium sound system, or a specific trim package? Every single factory-installed option adds value and should be listed and accounted for in the final ACV.

It's a huge mistake to assume the insurance company's report is gospel. These valuations are often spit out by third-party software that can easily miss custom upgrades, misinterpret a car's condition from a few grainy photos, or pull comps that aren't a true match.

Spotting Inaccuracies and Protecting Your Investment

Your job here is to become a detective. Look closely at the "comparable" vehicles they used. Are they really the same trim level as yours? Did they have the same options? Did the appraiser account for the brand-new set of tires you just bought last month or the immaculate condition of your interior?

This is where your own records and research become your most powerful tools. Every receipt and photo helps build your case.

If the math feels off, you absolutely have the right to push back. By methodically going through every line of that ACV report, you can pinpoint the errors and build a solid argument for what your vehicle was actually worth. For a more detailed walkthrough, check out our guide to understanding your https://totallossnw.com/total-loss-estimate/.

How to Navigate a Diminished Value Claim

So, you’ve picked your car up from the body shop. The repairs are perfect, and it looks just as good as it did before the accident. But even with flawless work, your vehicle now carries an invisible financial scar: a permanent accident history.

This blemish on its record reduces its resale value, a loss known as diminished value. The hard truth is that most people don't even know they're entitled to compensation for this drop.

Think about it from a buyer's perspective. If you have two identical cars to choose from, but one has been in a wreck, which one are you picking? The one with the clean history, of course. That difference in what a buyer is willing to pay is the value your car has lost, and you have a right to claim it.

Filing a diminished value claim means you have to prove this loss to the at-fault party's insurance company. The ball is in your court, and it's up to you to build the case.

Building Your Case for Compensation

Successfully claiming diminished value isn’t just about asking for money; it’s about presenting a professional, evidence-based argument. You need to gather the right documents to show the insurance adjuster exactly how much value your vehicle has lost.

Your mission is to paint a clear "before and after" picture of your car's market value.

Here's the essential evidence you'll need to collect:

- Proof of Pre-Accident Condition: Dig up your service records, oil change receipts, and any photos you have. These documents prove your car was a well-maintained, high-value asset before the collision.

- Detailed Repair Records: Get a copy of the final, itemized repair bill from the body shop. This invoice is critical because it details the severity of the damage and the scope of the repairs, which directly impacts the loss in value.

- An Expert Diminished Value Appraisal: This is your secret weapon. A certified, independent appraiser will perform a detailed analysis and generate a formal report that calculates the precise dollar amount of your car's diminished value.

A professional car insurance appraisal for diminished value is your most powerful tool. It transforms your claim from a simple request into an evidence-based demand, making it much harder for an insurance adjuster to dismiss or lowball.

Overcoming Insurer Pushback

You can bet the insurance company will resist your claim. It's a common tactic. They might tell you that high-quality repairs made the car "whole" again, conveniently ignoring the market reality that a wrecked-and-repaired vehicle is always worth less.

They may even offer a quick, low-ball settlement, hoping you'll take it and disappear. Don't fall for it.

This is exactly why your own independent appraisal is non-negotiable. It provides an objective, third-party valuation that cuts through the insurer's arguments. With a professional report in hand, you’re not just asking—you’re proving. It gives you the leverage you need to negotiate effectively and recover the money you're rightfully owed.

For a more detailed walkthrough, you can learn more about how to file a diminished value claim and get fully prepared for the process.

What To Do When the Insurance Appraisal Is Too Low

It’s a sinking feeling. After everything you’ve been through with the accident, the insurance company’s settlement offer lands with a thud, and it’s nowhere near what you know your car was worth. It can feel defeating, but I’m here to tell you that their first number is just that—a first offer. It’s a starting point for a negotiation, not the final word. You absolutely have the right to push back and fight for what’s fair.

Your first move is simple: ask the insurance adjuster for a complete copy of their valuation report. This is the playbook that shows you exactly how they came up with their number. It will list the "comparable" vehicles they used as a baseline and any adjustments they made. Don’t just skim it; dig in and look for mistakes. You’d be surprised how often they get things wrong.

Building Your Case With Cold, Hard Facts

Once you see their logic (or lack thereof), it's your turn to build a counterargument. This isn't about what you feel the car was worth; it's about proving its market value with solid evidence. Your job is to paint a clear, undeniable picture of your vehicle's true pre-accident condition and value.

To do this effectively, you need to gather ammunition in three key areas:

- Find Better "Comps": The cars they compare yours to are critical. Hop online and find vehicles for sale that are a genuine match for your car’s year, make, model, trim, and options. Focus on listings from local dealerships, as their prices often hold more weight than private party sales. Screenshot everything.

- Show Your Work: Did you just put on new tires? A new battery? Have the receipts ready. Compile all your service records to demonstrate a history of meticulous care. A well-maintained vehicle is a more valuable vehicle, and you need to prove it.

- Point Out What They Missed: Did their report conveniently forget your premium sound system, sunroof, or that rare sports package? List every single feature their valuation overlooked. If you have the original window sticker, that's pure gold.

This kind of detailed pushback is more effective than ever. Insurers are in a tough spot—they know that a bad claims experience sends customers running to competitors. In fact, a 2025 study showed that only 51% of high-value customers are committed to staying with their current insurer, which has companies scrambling to improve satisfaction. As JD Power highlights, this puts a major focus on the customer experience, giving you more leverage than you might think.

How To Escalate Your Dispute the Right Way

So, you’ve sent your evidence, and the adjuster still won't budge. What now? It’s time to play your trump card: the appraisal clause. Buried in your policy documents, this clause is your most powerful tool for breaking a stalemate.

Invoking the appraisal clause takes the decision out of the insurance company’s hands. It forces them to negotiate based on the findings of neutral, third-party experts rather than their own internal software.

This clause allows both you and the insurer to hire independent appraisers. These experts then work to agree on a fair value for your vehicle. Hiring your own certified appraiser gives you an official, detailed report that an insurance company can’t easily dismiss.

When you're ready to formally dispute the offer, a well-structured plan is essential. Follow these steps to ensure you're organized and prepared.

Your Action Plan for Disputing a Low Appraisal

| Step | Action Required | Key Tip |

|---|---|---|

| 1. Formal Request | Immediately ask the insurer for their complete valuation report in writing. | This document is the foundation of their argument. Look for inaccurate "comps" or missed features. |

| 2. Gather Evidence | Compile receipts, service records, and find 3-5 truly comparable vehicle listings. | Focus on local dealership listings, as they are often seen as more credible than private sales. |

| 3. Present Your Case | Send a professional email or letter to the adjuster with all your counter-evidence attached. | Clearly and calmly state why you believe their offer is too low, using your evidence to back up your claim. |

| 4. Invoke the Clause | If they refuse to negotiate, formally invoke the appraisal clause in your policy. | This is a formal step. State your intention clearly in writing to the claims department. |

| 5. Send a Demand Letter | Combine your evidence with your independent appraisal into a final demand letter. | A strong, evidence-backed letter is often the final push needed. For guidance, learn how to craft a powerful insurance demand letter to finalize your claim. |

This process takes the emotion out of the argument and forces the insurance company to deal with facts. It's often the last step needed to get them to the table and secure the settlement you truly deserve.

Common Questions About Car Insurance Appraisals

Even when you understand the big picture, the appraisal process can still leave you with a lot of questions. Let's dig into some of the most common ones that pop up, so you can handle your claim with confidence.

Think of this as your go-to FAQ for those tricky "what if" moments.

How Long Does a Car Insurance Appraisal Take?

The timeline can definitely vary, but you can generally expect the whole thing to take about a week or two. That gives the appraiser enough time to inspect the car (either in person or virtually), dive into the local market data for comparable sales, and put together their final report.

Of course, some things can slow it down. If your car is rare, the damage is particularly severe, or you and the insurer are already at odds, expect delays. The good news? If you hire your own independent appraiser, they're often much faster since they're working only for you.

The key is to stay on top of it. If you haven't heard anything within a reasonable timeframe, don't be afraid to check in with the adjuster for a status update.

What If I Owe More Than the Appraised Value?

This is a tough spot to be in. It's often called being "upside down" or "underwater" on your loan, and unfortunately, it's pretty common. The insurance payout is based on your car's Actual Cash Value (ACV), not what you owe the bank. So, if the appraisal says your car was worth $15,000 but you still have an $18,000 loan, you're on the hook for that $3,000 gap.

This is exactly why Guaranteed Asset Protection (GAP) insurance exists. If you bought GAP coverage when you got the car, it's designed to step in and pay off that exact difference between the ACV and what you owe. It can be a real financial lifesaver.

Do I Have to Accept the First Offer?

Absolutely not. Think of the insurance company's initial offer as their opening move in a negotiation—it's not the final word. You should never feel pressured to accept a lowball number right out of the gate.

You have every right to ask for their valuation report, pick it apart, and come back with your own evidence. This is your chance to make your case, and solid research is your best weapon for getting a fair settlement.

Should I Get My Own Independent Appraisal?

Hiring your own appraiser is one of the smartest things you can do, especially in a couple of key scenarios:

- When the stakes are high: If you have a classic car, a high-value luxury vehicle, or something with a ton of custom work, the insurer's standard software just won't see its true value.

- When you reach a stalemate: If you've presented your evidence and the insurance company simply won't budge from their low offer, a professional report from a third-party expert is tough for them to argue with.

An independent car insurance appraisal gives you the unbiased, professional leverage you need to level the playing field and prove what your vehicle was really worth.

Navigating a total loss or diminished value claim requires expertise and a commitment to fighting for a fair number. At Total Loss Northwest, we provide certified, independent appraisals that force insurers to deal with real-world data, not their own biased software. If you're facing a lowball offer, let us help you get the settlement you rightfully deserve. Learn more and start your claim at https://totallossnw.com.