So, you just got the call. Your car is a total loss. That initial settlement offer from the insurance company? It's almost never their final one. Think of it as an opening bid in a negotiation.

The whole reason these disputes happen is because the insurer's valuation—what they call the Actual Cash Value (ACV)—often doesn't match what your vehicle was actually worth right before the accident. Knowing how to push back is the key to getting the money you're owed.

Your Car Is Totaled. What Happens Next?

Hearing your car is "totaled" can be a shock. It simply means the insurance company has run the numbers and decided it's cheaper to pay you out than to fix the vehicle. This is usually triggered when repair costs exceed a certain percentage of the car's value, a threshold that varies by state.

If this feels like it's happening more often, you're not wrong. With cars getting more complex and repair costs skyrocketing, total loss declarations are on the rise. Some industry reports show that over 30% of auto claims now result in a total loss.

This trend makes it absolutely critical to know your rights. The insurance company’s first offer comes from a valuation report they generate. Your first job is to get your hands on that report and start digging.

Decoding the Insurer's Valuation Report

Don't just take the adjuster's word for it over the phone. Your first move should always be to ask for a complete, detailed copy of their valuation report. This document is the playbook for their low offer, and it's where you'll find the weak spots.

When you get the report, zoom in on these areas:

- The "Comps": Look closely at the comparable vehicles they used. Are they really comparable? Check the trim level, mileage, options, and model year. It's common for them to use base models to value your fully-loaded one.

- Condition Adjustments: Did they slap an "average" condition rating on your meticulously maintained car? This is a classic tactic to shave hundreds, if not thousands, off the value.

- Your Local Market: Where did they pull the comps from? A vehicle's value in a small town can be drastically different from its value 200 miles away in a major city. They need to be local.

The heart of most total loss disputes is a straightforward disagreement on value. The insurer uses data that serves their bottom line. Your job is to counter with evidence that reflects the real world.

If you find comps with way more miles, the wrong features, or from a completely different market, you've got your starting point for a challenge. For a deeper dive into this initial stage, check out our complete guide on what to do when your car is totaled.

Your Immediate Options After a Total Loss Offer

Once you've had a chance to go through their report, you're at a crossroads. It's tempting to take the quick money, but acting too fast can be a costly mistake.

Here’s a quick look at your choices when you receive that initial total loss settlement offer from your insurance company.

| Your Action | What It Involves | Potential Outcome |

|---|---|---|

| Accept the Offer | You agree to their number, sign the release forms, and hand over the title. | This is the fastest way to get paid, but you're likely leaving money on the table. |

| Negotiate Directly | You gather your own evidence (comparable listings, receipts) and present a counteroffer to the adjuster. | With strong evidence, you can often secure a better settlement without needing a formal appraisal. |

| Invoke the Appraisal Clause | You officially demand an independent appraisal as laid out in your policy—the next step for a serious dispute. | This triggers a more formal process with neutral, third-party experts determining the vehicle’s true ACV. |

Making an informed decision here is crucial. Let’s break down what each of these paths really looks like.

Think of the insurance company's first settlement offer as exactly what it is: an opening bid. It’s not the final word—it's the start of a negotiation. Your job is to pivot from reacting to their number to proactively building a powerful, evidence-based case for what your vehicle was actually worth.

The core of your argument will be built on finding solid, accurate comparable vehicles, often called "comps." The insurance adjuster's report is almost certainly filled with comps that work in their favor—think base models, cars with way more miles, or listings from cheaper markets hundreds of miles away. You need to find better ones.

Finding True Comparable Vehicles

Start your search on online auto listing sites, but keep it local. The key is to find what it would actually cost you to replace your exact car, right here, right now.

Focus on vehicles that are a mirror image of yours:

- Year, Make, and Model: This is the obvious starting point.

- Trim Level: This is a huge one. A fully-loaded Platinum trim is in a different league than a base model, so don't let them get away with comparing the two.

- Mileage: Look for comps with similar mileage. If your car had exceptionally low miles for its age, that’s a major value booster you need to prove.

- Condition: Find listings for cars in the same pre-accident condition as yours. When you find a good match, save the listing and take screenshots. Good comps can disappear fast.

Your target is a portfolio of 3-5 rock-solid, local comps. This isn't just data; it's direct evidence that refutes the insurer’s valuation by showing them the real-world replacement cost in your market.

This hands-on research is your single most effective tool in a total loss dispute. It replaces their questionable data with undeniable proof.

Documenting Every Added Feature and Upgrade

Now, let's look beyond the basics. You need to account for every single detail that added value to your specific car. Did you recently sink money into upgrades or major maintenance? These things add real dollars to its worth, but the insurance company will completely ignore them unless you provide receipts.

Put together a detailed list with proof for any value-adding items:

- New Tires or Brakes: A new set of high-quality tires isn't a minor expense; it can easily add hundreds of dollars to the car's value.

- Aftermarket Additions: Did you install a remote starter, custom wheels, or an upgraded stereo? List them out.

- Recent Major Repairs: If you just had a new transmission put in, that’s a massive value-add that can't be overlooked.

- Meticulous Maintenance: Show them your service records. They prove your car was in excellent mechanical shape, which makes it worth more than an average, neglected vehicle.

Treat it like you're selling a house—every improvement you made contributes to the final price. The more documentation you have, the stronger your negotiating position becomes. Present this evidence clearly in a simple list or spreadsheet. This kind of organization signals to the adjuster that you’re serious and have done your homework.

As insurance premiums continue to climb, we're seeing the claims environment get a lot more competitive. More and more policyholders are fighting back against low appraisals to get what they're owed in a tough economy. This makes having your documentation in order more critical than ever. To get a better sense of the trends shaping these disputes, you can explore detailed industry analysis from Claims Journal.

Alright, you've done your homework and have a solid case. Now it's time to put that research into action and formally push back on the insurance company's lowball offer. This isn't about firing off an angry email; it’s about presenting a professional, evidence-backed argument that the adjuster simply can't ignore.

This is where you shift from defense to offense, and it all starts with well-documented, formal communication.

Putting It All in a Demand Letter

Your first move is to draft a formal demand letter. This document is the cornerstone of your dispute. It officially rejects their initial offer and lays out your counteroffer, supported by all the evidence you've meticulously gathered. Think of it as your opening argument.

A strong demand letter makes it clear you're serious and organized. It should be structured to make your case undeniable.

Here’s what to include:

- A firm rejection: Start by clearly stating that you do not accept their settlement offer and explain, in brief, why it's insufficient.

- Your counteroffer: Present your own figure for the vehicle's Actual Cash Value (ACV). Be specific.

- Your evidence: Attach copies of everything—your comparable vehicle ads, maintenance logs, photos, and any third-party appraisal reports you secured.

- A clear deadline: End the letter by requesting a response within a specific, reasonable timeframe, like 10-15 business days, to discuss a revised settlement.

Knowing how to write an effective appeal letter is a great starting point for getting the tone and structure right. For a more focused guide on this specific type of communication, we've put together a detailed breakdown on how to craft an https://totallossnw.com/insurance-demand-letter/ over on our blog.

Pro Tip: From this point forward, keep everything in writing. If you absolutely have to talk to the adjuster on the phone, send a follow-up email immediately afterward summarizing the key points of your conversation. This creates a paper trail that is invaluable if the dispute drags on.

Talking to the Adjuster: Stay Cool, Stick to the Facts

The way you communicate is just as critical as the information you present. You need to be firm and confident, but always professional. Remember, adjusters deal with heated conversations all day long; getting emotional or confrontational won't get you anywhere. It just gives them a reason to label you as "difficult."

Let your evidence do the talking.

Keep a running log of every single interaction you have. For every email, call, or letter, jot down the date, time, the name of the person you dealt with, and a quick summary of the conversation. This log becomes your bible, ensuring no detail gets forgotten or twisted later on.

This methodical approach shows the insurance company you're not just another frustrated customer—you're an organized and informed party who is fully prepared to see this through to a fair conclusion. That alone can significantly strengthen your negotiating position.

So, you've hit a brick wall with the insurance adjuster. The negotiations have stalled, and it feels like you're stuck with their lowball offer. Don't throw in the towel just yet. Your policy likely has a powerful, but often hidden, tool designed for this exact situation: the appraisal clause.

Think of it as a built-in tie-breaker. Invoking this clause officially takes the valuation dispute out of the adjuster's hands and puts it into a more neutral, fact-based process. It's a structured way to settle the disagreement when you and the insurer are just too far apart on the numbers.

Finding and Triggering the Appraisal Clause

First thing's first: you need to find the clause in your policy. Grab your documents and look for a section titled something like "Damage to Your Auto" or "What to Do After a Loss." The language will be very specific, laying out the exact steps to get the ball rolling.

Once you’ve located it, you have to formally trigger the clause, and a phone call won't cut it. You need to send a certified letter to your insurance company. In it, clearly state your intent to invoke the appraisal clause to resolve the dispute over your vehicle's value. This isn't just a formality; it creates a legal paper trail and forces the insurer to follow the procedure outlined in the policy.

If you want to dive deeper into the nitty-gritty of this policy provision, you can find a comprehensive breakdown of the insurance appraisal clause and how it really works.

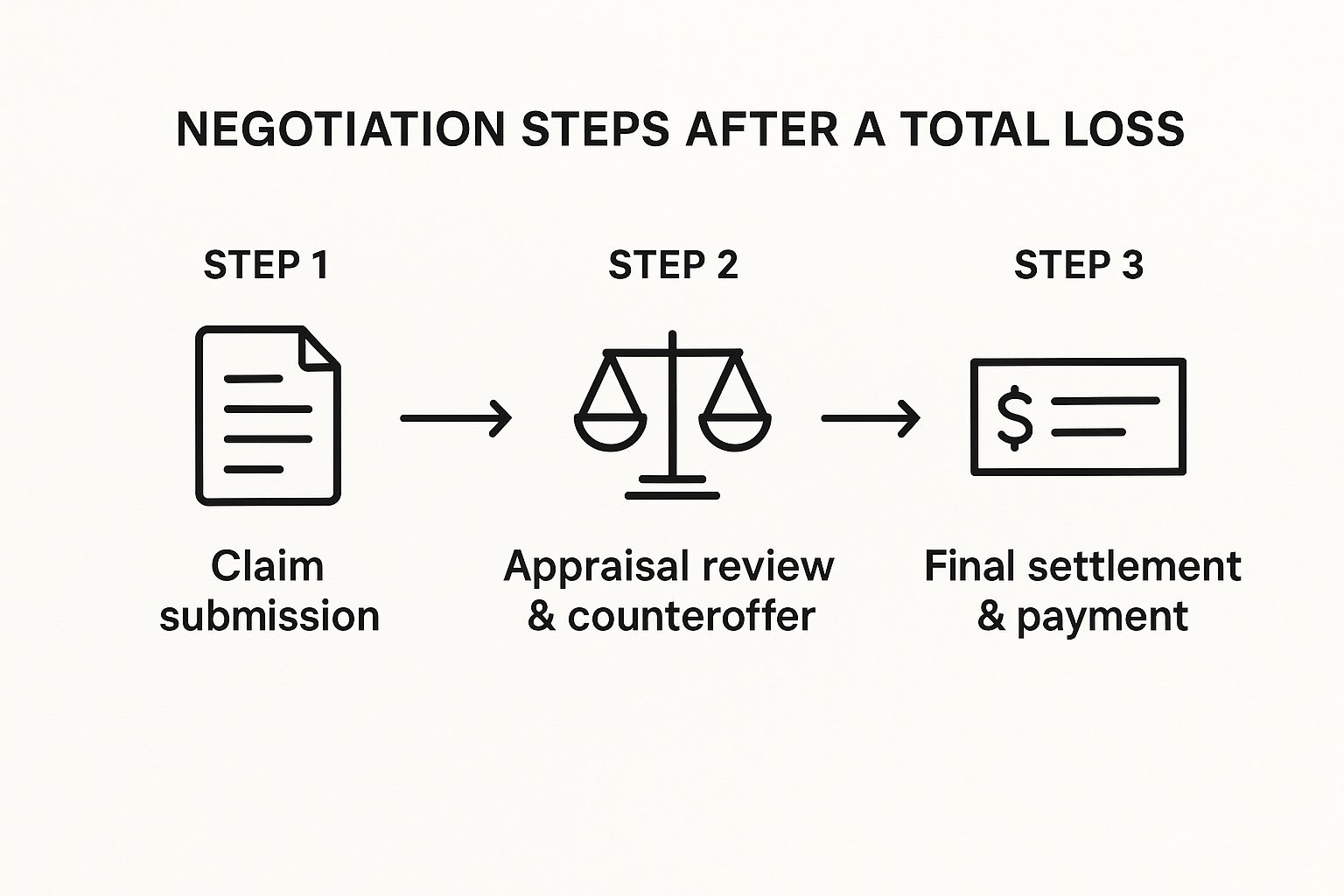

This infographic lays out the typical path from the initial offer to a final settlement.

As you can see, making a counteroffer is a critical part of the process. It's always worth trying to negotiate directly before escalating to the appraisal clause.

How Appraisers and an Umpire Settle the Score

After you've sent your letter, the process officially begins. You’ll hire your own independent appraiser, and the insurance company will hire theirs. The key here is choosing a true expert who is completely unbiased. Your appraiser's sole job is to build an ironclad, evidence-based report detailing your vehicle's actual cash value before the accident. The insurance company's appraiser will do the same for their side.

The whole point of the appraisal clause is to get an objective valuation from outside experts. This sidesteps the biased internal software and adjuster opinions that are often the root cause of total loss appraisals insurance claim disputes.

So, what happens if the two appraisers can’t agree on a number?

That’s when an umpire comes in. The two appraisers will mutually select this neutral third party. The umpire reviews both reports, considers all the evidence, and makes a final decision. A binding settlement is reached when any two of the three parties—your appraiser, the insurer's appraiser, or the umpire—agree on a value. That final number is what the insurance company is legally obligated to pay, bringing the dispute to a definitive close.

Finalizing the Settlement and Getting Paid

After what feels like an eternity of research, phone calls, and tough negotiations, you've finally landed on a settlement figure you can live with. That's a huge win, so take a moment to breathe. But don't pop the champagne just yet—the last few steps are crucial for making sure the money actually hits your bank account without any eleventh-hour headaches.

Before you celebrate, the insurance company will send over a final settlement agreement or a release form. Whatever you do, don't sign it right away. This is the document that legally closes the book on your claim, so you need to read every single word with a fine-tooth comb.

Review the Settlement Agreement Meticulously

Think of this document as the final word. Once you sign it, there’s no going back. Make sure the settlement amount listed is the exact figure you negotiated. Just as important, scan for any sneaky clauses that might release the insurer from other obligations or, worse, try to pin some fault on you.

If a single sentence seems off or confusing, don't just let it slide. Get on the phone or email the adjuster and ask for clarification—and get their explanation in writing. It's infinitely easier to correct a typo or a misunderstanding now than to try and fight it after your signature is on the dotted line.

Your signature on that settlement release is the point of no return. It legally slams the door on your claim, preventing you from ever seeking more money for this incident. Get it right before you sign.

Once you’re completely satisfied that the agreement is correct, you can sign it. Now it’s time to get the paperwork ready to transfer ownership of your totaled car to the insurance company.

Handling the Title Transfer and Paperwork

To get your check, you have to formally sign over the vehicle’s title. In essence, the insurance company is buying the salvaged car from you as part of the deal. They’ll give you specific instructions on how to do this, but it usually comes down to a few key things.

- Signing the Title: You’ll sign your name in the "seller" section. Be incredibly careful here. Any mistakes, cross-outs, or corrections can create major delays and might even require you to apply for a duplicate title.

- Providing a Lien Release: If you had a loan on the car, you absolutely must provide a lien release letter from your bank. This is the official proof that the loan is paid off and the title is free and clear.

The insurance company won't cut your final check until they have a clean, properly signed title in their hands. Any issues with the title will bring the entire process to a screeching halt.

Understanding the Payment Process

Finally, the part you've been waiting for: getting paid. How this happens all depends on whether you owned the car outright or still had a loan.

If you have a loan, the insurance company will pay your lender (the lienholder) first. It's a non-negotiable step. For example, if your settlement is $20,000 and you still owe $15,000 on your loan, the check goes directly to the bank. Once they process it and close your account, they'll forward the remaining $5,000 to you.

If you own your car free and clear, it's much simpler. The full settlement check will come directly to you.

Common Questions About Total Loss Disputes

Going head-to-head with an insurance company over a total loss can feel like a daunting, uphill battle. It's completely normal to have questions and feel a bit lost. In my experience, most people facing this situation share the same core concerns.

Getting straight answers is the first step toward building the confidence you need to challenge a lowball offer and fight for what your car was actually worth. Let's walk through some of the most common questions that pop up.

How Long Does a Total Loss Appraisal Dispute Usually Take?

This is the million-dollar question, and the honest answer is: it depends.

If you’ve done your homework, presented solid evidence, and are dealing with a reasonable adjuster, you might wrap things up in just a few weeks. That’s the best-case scenario.

However, the moment you formally invoke the appraisal clause, the timeline naturally extends. You're now in a more structured, formal process. Realistically, you should expect this path to take anywhere from one to three months. This timeframe gives everyone enough time to select their appraisers, have the vehicle properly evaluated, and, if needed, for an umpire to be brought in to make the final call. The key here is patience and persistent, professional follow-up.

Can I Keep My Totaled Car and Still Get Paid?

You absolutely can. In the industry, this is called "owner retention," and it's a right you have in most states.

Here's how it works: if you decide to keep the car, the insurance company will determine its salvage value—what it's worth in its current, wrecked condition. They'll then deduct that amount from your settlement.

For instance, if you and the insurer agree your car was worth $18,000 before the accident and its salvage value is $2,000, they will send you a check for $16,000, and the car is yours to keep.

A Word of Caution: Choosing this path means your vehicle will be issued a salvage title. This is a permanent brand on the car's history, which makes it incredibly difficult to get full coverage insurance again and drastically hurts its future resale value.

Do I Need a Lawyer for My Total Loss Dispute?

For most standard total loss appraisals insurance claim disputes, bringing in an attorney is usually overkill. The system, including the appraisal clause, is designed so that you, the policyholder, can navigate it effectively. A good independent appraiser is often the only professional muscle you'll need in your corner.

That said, there are a few specific situations where getting legal advice is a very smart move:

- Serious Personal Injuries: If you were injured in the accident, the claim is much bigger than just the car's value.

- Bad Faith Suspicions: If the insurance company is giving you the runaround with unreasonable delays, refusing to communicate, or using deceptive tactics.

- Complex Legal Issues: If the dispute gets tangled in confusing policy language or other legal complexities.

In these scenarios, an attorney specializing in insurance law can be an invaluable advocate.

What if an Uninsured Driver Totaled My Car?

This is a deeply frustrating situation, but don't worry—you have options. When an at-fault driver has no insurance (or not enough), you'll need to turn to your own policy to make you whole.

The claim will be filed under either your collision coverage or your uninsured motorist property damage (UMPD) coverage. The specifics will depend on your policy and state laws.

From that point on, the dispute process is identical. You'll negotiate the vehicle's value with your own insurance company, just as you would have with the other driver's. Your insurer will handle paying you, and then it's their job to try and recover the money from the at-fault driver. That process, called subrogation, happens behind the scenes and won't involve you.

At Total Loss Northwest, we specialize in fighting for the true value of your vehicle. If you're facing a lowball settlement offer in Washington or Oregon, our certified independent appraisers can invoke the Appraisal Clause on your behalf, ensuring you get a fair and accurate payout. Don't leave money on the table—learn how we can help you today.