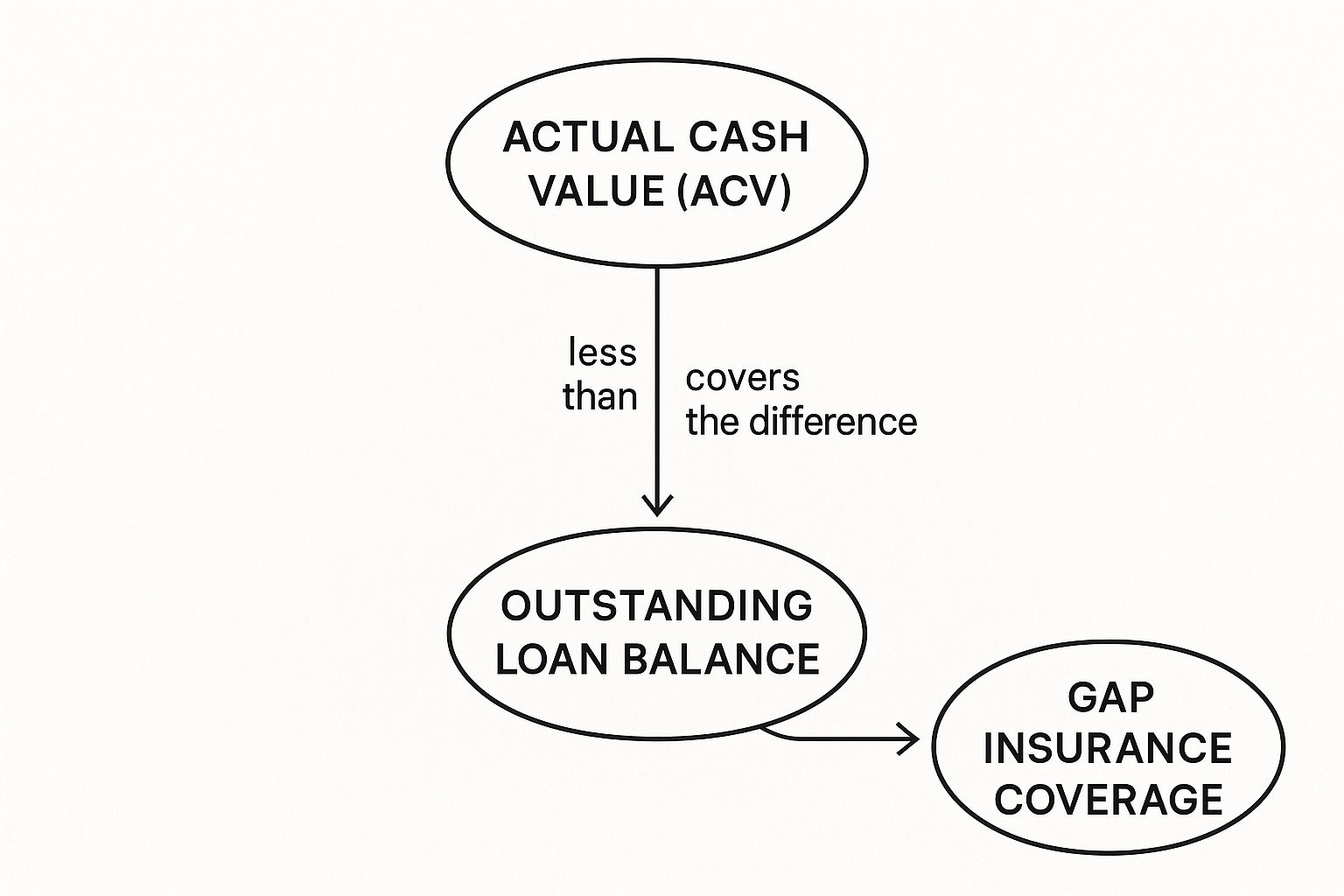

So, what exactly does gap insurance do? At its core, it covers the financial gap between what your car is actually worth (its actual cash value, or ACV) and the amount you still have left on your auto loan or lease.

If your car is totaled in an accident or stolen, this coverage pays off the remaining loan balance that your standard auto policy doesn't touch. It's designed to stop you from being stuck making payments on a car you can't even drive anymore.

The Financial Safety Net for Your Totaled Car

The second you drive a new car off the dealer's lot, its value starts to plummet. This instant drop is called depreciation, and it can quickly create a "gap" between your car's market value and what you owe the bank. A standard collision or comprehensive policy will only pay out the vehicle's ACV at the time of the incident. If that check is less than your loan balance, you're on the hook for the difference.

This is precisely what gap insurance covers: that specific shortfall. It isn't a bonus check for you; it's a direct payment to your lender to wipe the slate clean on your auto loan. Think of it as a crucial bridge over a serious financial hole.

This infographic does a great job of showing how your loan balance, the car's depreciated value, and gap insurance all interact.

As you can see, the gap coverage zeroes in on that negative equity. It makes sure you don't walk away from a total loss with a hefty car payment and no car.

Why Does This Gap Even Exist?

Depreciation is the main culprit here. It's not uncommon for a new vehicle to lose 20% to 30% of its value in the very first year. For most people, their loan payments just can't keep up with that steep of a decline.

This reality means a huge number of new car owners are "upside down" on their loans almost right away, which is what makes gap insurance such a smart move for so many. The first step is always understanding what your car is worth in the eyes of an insurer, as their ACV calculation is the foundation of any total loss claim. You can learn about the nuances of determining the value of your totalled car in our other guide.

Here's a quick breakdown to make it crystal clear.

Gap Insurance Coverage at a Glance

| Scenario | Standard Auto Insurance Payout | Gap Insurance Coverage |

|---|---|---|

| Your Loan Balance | N/A (Does not consider your loan) | The remaining balance after the standard payout |

| Car's Actual Cash Value (ACV) | Pays the ACV (minus your deductible) | N/A (Relies on the standard policy's ACV) |

| Your Deductible | You pay this amount out of pocket | Sometimes covers the deductible (policy dependent) |

| "The Gap" | Does not cover this amount | This is exactly what it pays for |

Ultimately, gap insurance works in tandem with your primary policy to ensure you're not left with a financial burden after a total loss.

How Gap Insurance Clears Your Car Loan After a Wreck

To really get your head around what gap insurance does, it helps to walk through a real-world scenario. Its whole purpose isn't to hand you a check, but to square things up with your lender if your car is totaled.

Let’s say you just bought a new car and financed $30,000. A year goes by, you get into a bad accident, and the car is a total loss. Because of depreciation (which hits new cars hard and fast), your insurance company looks at the car's current market value and determines its actual cash value (ACV) is now only $22,000.

That $22,000 is all your standard collision or comprehensive policy is going to pay out. The problem? You look at your loan statement and see you still owe $25,000.

Bridging the Financial "Gap"

Without gap insurance, you’re in a tough spot. You’d get the $22,000 from your insurer, but you'd have to pull the remaining $3,000 out of your own pocket to pay off the lender. So, you're left with a hefty bill for a car you can't even drive anymore.

This is exactly where gap insurance saves the day. It steps in to cover that $3,000 difference between what you owe and what your car was worth. The payment goes straight to your lender, paying off the loan and wiping the slate clean.

It’s always a good idea to understand the details of how insurance companies figure out your car's value. You can get a better handle on this by learning more about what the actual cash value of your car is and how that calculation works.

The need for this kind of protection has definitely grown. Back in the mid-2010s, it was already common for nearly 20% of new car buyers in the U.S. to add gap insurance, precisely to avoid this kind of financial nightmare.

The Bottom Line: Gap insurance doesn't pay you. It pays your lender to cover the negative equity on a totaled vehicle. It makes sure you're not starting the hunt for a new car while still paying off the old, wrecked one.

Ultimately, this coverage is designed to solve a very specific problem, letting you walk away from a total loss without being haunted by the debt from your last vehicle.

Understanding Common Gap Insurance Exclusions

Gap insurance is a fantastic safety net, but it's not a catch-all policy. Knowing what it doesn't cover is just as crucial as knowing what it does. Think of it as a specialist with a very specific, very important job: to pay off the negative equity on a totaled or stolen car. It doesn't step in to handle other costs related to the incident or your loan agreement.

Getting clear on these boundaries ahead of time prevents any nasty surprises down the road. You'll know exactly which expenses are yours to handle and which your standard auto insurance policy will take care of.

What Gap Insurance Will Not Pay For

Gap policies are pretty consistent across the board when it comes to exclusions. You can bet that your policy will not cover any of the following:

- Your primary insurance deductible. This is the amount you agreed to pay out-of-pocket when you signed up for your main collision or comprehensive coverage. Some gap policies might offer a special add-on to cover this, but it's definitely not standard.

- Late fees or loan penalties. If you've missed payments or incurred other penalties that were added to your loan balance, gap insurance won't pay for those. It only deals with the original financed amount of the vehicle itself.

- Extended warranties and other add-ons. Did you roll the cost of an extended warranty, credit life insurance, or a vehicle service contract into your car loan? Gap insurance won't cover that portion of the balance.

- Vehicle repairs. This one is simple: gap insurance only comes into play when your car is declared a total loss. It never, ever covers repair costs for a vehicle that can be fixed.

- A down payment on your next car. Its mission is to wipe the slate clean on your old loan, not to give you a head start on a new one.

By understanding these common exclusions, you can see the precise role gap insurance plays. It’s not a comprehensive auto policy; it’s a targeted financial tool designed to clear your auto loan after a total loss. That sharp focus is exactly what makes it so effective.

When Gap Insurance Becomes a Financial Lifesaver

So, when does gap insurance really matter? The best way to understand its power is to see it in action. Let's walk through a few common scenarios where this coverage can be the one thing that saves you from a serious financial headache.

Scenario 1: The Small Down Payment

Imagine Sarah. She just drove off the lot in her brand-new car, absolutely thrilled. To make it happen, she put just 5% down and financed the rest. Six months later, disaster strikes—a distracted driver blows through a red light, and her car is totaled.

- Loan Balance: $28,500

- Car’s ACV: $22,000

- The Gap: $6,500

Without gap insurance, Sarah’s collision coverage would pay out $22,000. That sounds great, until she realizes she still owes her lender another $6,500 for a car that no longer exists. With gap coverage, that entire debt is paid off, and she can start fresh.

Scenario 2: The Long-Term Loan

Next, meet David. He financed his new SUV with a 72-month loan to keep his monthly payments low. The problem with long loans is that you build equity at a snail's pace while your car's value plummets.

Two years into his loan, his vehicle is stolen and never found.

- Loan Balance: $31,000

- Car’s ACV: $24,500

- The Gap: $6,500

David is in the same boat as Sarah. His insurance pays what the car was worth, but gap insurance is what truly saves the day. It prevents him from having to make payments on a stolen vehicle for years. It's no surprise that industry data reveals over 60% of gap insurance claims occur in the first 18 months of ownership, right when depreciation hits hardest.

Scenario 3: The Leased Vehicle

Finally, let’s look at Maria, who is leasing a luxury sedan. Most lease contracts actually mandate gap coverage, and for good reason—the leasing company is protecting its asset from rapid depreciation. A year into her lease, her car is declared a total loss in a highway pile-up.

Because a lease is essentially a long-term rental, the financial stakes are high. The leasing company expects its asset to be paid for, regardless of what happens to it.

Gap insurance steps in to cover the difference between the car's value and her remaining lease payments, allowing Maria to walk away clean. Dealing with a total loss can be overwhelming, so knowing the next steps is crucial. Our guide on what to do when your car is totaled can give you a clear plan.

In every one of these cases, gap coverage transformed a potential financial nightmare into a simple inconvenience.

When is Gap Insurance Most Needed?

Not everyone needs gap insurance, but for some, it's a non-negotiable part of their financial safety net. If any of the situations in the table below sound familiar, you're likely a prime candidate for this type of coverage.

| Financing Situation | High Risk of a 'Gap'? | Reason |

|---|---|---|

| Down payment under 20% | Yes | You have very little equity from the start. |

| Loan term of 60+ months | Yes | Your loan balance decreases slower than the car's value. |

| Leasing a vehicle | Almost always | Most lease agreements require it for this reason. |

| Rolling negative equity into a new loan | Absolutely | You're starting the new loan "upside down." |

| Buying a car that depreciates quickly | Yes | Luxury or high-performance models lose value fast. |

Ultimately, if your loan balance is likely to be higher than your car's actual cash value for any significant period, gap insurance is a smart move. It's a small price to pay for major peace of mind.

Is Gap Insurance a Smart Move for You?

So, you get what gap insurance does. Now for the million-dollar question: do you actually need it? The truth is, it's not for everyone. But for some drivers, it's the one thing that can save them from a massive financial headache.

It all boils down to one simple idea. Is there a good chance you’ll owe more on your car loan than the car is actually worth? If that happens, you're "upside down" or have "negative equity," and that's exactly where gap insurance steps in.

A Quick Reality Check

Figuring this out is easier than you think. Let's run through a quick checklist. Be honest with yourself—if you answer "yes" to even one of these, you should seriously consider getting a quote. The more you nod along, the greater your risk.

Here's what to look at:

- Was your down payment less than 20%? If you put down less than 20%, you started out with very little skin in the game. That makes it incredibly easy for normal depreciation to put you underwater on your loan almost immediately.

- Is your loan term 60 months or longer? Those long loan terms are great for keeping monthly payments low, but there's a catch. You're chipping away at the principal so slowly that your car's value is guaranteed to drop much faster than your loan balance.

- Are you leasing the car? Leases are a different beast. You're essentially just paying for the car's depreciation, not building any ownership equity. That's why nearly every lease agreement either includes a gap waiver or requires you to buy gap insurance outright. A "gap" is practically built-in.

- Did you roll over debt from your last car? If you traded in a car that you were already upside down on, you just dug the hole deeper. You started this new loan with a significant amount of negative equity right from day one.

- Does your car lose value fast? Let's face it, some cars just depreciate faster than others. Luxury brands, high-performance models, and even some popular sedans can see their value plummet. A quick online search will tell you what to expect for your specific make and model.

If these points sound a little too familiar, you're in the exact situation gap insurance was created for. It’s designed to be an affordable safety net, turning a potentially catastrophic financial blow into a predictable, manageable part of your budget. Think of it as a small price to pay to avoid a very big problem.

Your Gap Insurance Questions, Answered

Alright, even after you’ve got the basics down, some specific questions about gap insurance always pop up. Let's tackle the most common ones I hear so you can feel completely confident about your coverage. Think of this as clearing up the final few details.

Can I Get a Gap Insurance Refund if I Pay My Loan Off Early?

Absolutely, and it's something many people overlook. If you paid for your gap policy in one lump sum at the dealership, you're almost certainly due a prorated refund for the time you didn't use.

Here's the catch: it's not automatic. You have to be the one to reach out to the provider—be it the dealership or the insurance company—with proof that your loan is paid off. They'll do the math and cut you a check for the unused portion. Make sure you follow up on that; it's your money, after all.

I Have Full Coverage. Do I Still Need Gap Insurance?

This is probably the biggest point of confusion, and the answer is a definite "maybe." People hear "full coverage" and assume it covers everything, but that's not quite right. Full coverage simply means you have both collision and comprehensive policies.

When your car is totaled, these policies pay out its Actual Cash Value (ACV)—what it was worth the second before the crash.

Your standard insurance policy doesn't care about your loan balance. If you owe more than the car's ACV, that shortfall is your problem to solve. Gap insurance is the only thing designed to cover that specific financial hole.

How Long Should I Keep Gap Insurance?

You only need gap insurance as long as you’re "upside down" on your loan—that is, you owe more than the car is worth. Once you cross that threshold and have positive equity, the coverage is redundant.

A good rule of thumb is to check your loan balance against your car's estimated value (you can use sites like Kelley Blue Book for a quick check) once a year. The moment your car is worth more than you owe, you can confidently cancel the policy and save yourself some money.

Can I Buy Gap Insurance After I've Already Bought My Car?

Sometimes, but your window of opportunity is much smaller. The dealership will almost always require you to buy it on the day you sign the papers. However, some traditional auto insurance companies will let you add it to your policy later.

They usually have pretty strict rules, though, like the car has to be a recent model year with low mileage. If you're having second thoughts after driving off the lot, your best bet is to call your insurance agent right away to see what your options are.

Dealing with a total loss claim is stressful enough without the insurance company trying to shortchange you. And they often do, offering far less than your vehicle was actually worth.

If you're stuck with a lowball settlement offer, Total Loss Northwest is in your corner. We provide certified auto appraisals that give you the leverage to demand what you're rightfully owed. Don't let them undervalue your investment—visit us to get the fair settlement you're owed.