Even after the best body shop in town works its magic, a car that's been in an accident is worth less than it was before. This drop in value has a name: diminished value. It’s a real financial hit, often slicing an extra 10% to 25% off your car’s market value, on top of normal depreciation.

So, a car worth $20,000 before the crash might only fetch $15,000 to $18,000 afterward—even if it looks and drives like new. The accident history itself is what scares off future buyers.

The Real Cost of a Car Accident

When you tally up the costs of an accident, you’re probably thinking about the obvious things: repair bills, your insurance deductible, maybe even medical costs. But one of the biggest, and most frequently overlooked, financial losses is the permanent hit to your car’s resale value. This "invisible" damage is the true, lingering cost of a collision.

Think of your car like a valuable collectible. If a mint-condition comic book gets a tear and is professionally restored, it will never be worth as much as an untouched original. It may look perfect, but its history is now part of its story—and its price. The same logic applies to your car.

Understanding the Financial Impact

The moment that accident is documented, it leaves a permanent mark on vehicle history reports from services like CarFax and AutoCheck. Smart car buyers and dealers always pull these reports. An accident history is a huge red flag that immediately lowers the price they’re willing to pay, no matter how perfect the repairs are.

This isn't just a number on paper; it's a loss that hits your wallet in a few key ways:

- Lower Trade-In Value: Dealerships will offer you thousands less for your car compared to an identical, accident-free model.

- Reduced Private Sale Price: When selling it yourself, potential buyers will use the accident history to make lowball offers or simply walk away.

- Impact on Total Loss Settlements: Knowing the pre-accident value of your car is critical if it's ever declared a total loss. You can find out more by understanding what is actual cash value of my car.

How Severity Dictates Value Loss

Naturally, not all accidents are the same. The amount of value your car loses is tied directly to how bad the crash was. A minor parking lot scrape won't hurt its value nearly as much as a major collision that required structural or frame repairs.

Of course, beyond the financial side of things, it’s vital to know the immediate steps to take after a car accident to protect your safety and document everything correctly.

The core issue is buyer perception. An accident history introduces uncertainty about the vehicle's long-term reliability and structural integrity, and buyers are unwilling to pay a premium for that risk.

To give you a better idea, the table below provides a quick estimate of how much value you can expect to lose based on the severity of the accident.

Estimated Diminished Value by Accident Severity

| Accident Severity | Description of Damage | Estimated Diminished Value Range |

|---|---|---|

| Minor | Cosmetic damage like scratches, small dents, or a damaged bumper cover. No structural or mechanical repairs needed. | 5% – 10% of pre-accident value |

| Moderate | Significant body panel replacement (doors, fenders), mechanical repairs, but no frame or unibody damage. | 10% – 20% of pre-accident value |

| Severe | Major collision involving frame or unibody damage, airbag deployment, or significant mechanical system replacement. | 15% – 30%+ of pre-accident value |

Keep in mind, these are just estimates. The final figure can be influenced by your car's make, model, age, and pre-accident condition. A newer, high-end vehicle will typically see a much larger dollar-amount loss than an older, economy car.

Breaking Down the Three Types of Diminished Value

When your car gets into an accident, its value doesn't just drop—it fractures. To really get a handle on what your car is worth after the wreck, you need to understand that "diminished value" isn't a single number. It’s actually a catch-all term for three distinct ways your vehicle loses money.

Knowing the difference between these types is the key to building a solid claim and getting the compensation you deserve.

Think of your car like a collector's item, say, a pristine vintage watch. If it gets a deep scratch on the crystal, its value immediately falls, even if it still tells time perfectly. That's one kind of loss. But what if a watchmaker replaces the original Swiss movement with a cheap knock-off? That’s a whole different, and much more serious, blow to its value.

Your car’s post-accident value works the same way.

Inherent Diminished Value

This is the big one—the most common and unavoidable hit to your car's value. Inherent Diminished Value is the automatic loss in resale value that happens the second an accident is recorded on its history report. It’s that simple.

Even with flawless, top-tier repairs using genuine factory parts, your car is now officially "that car that was in an accident." When a potential buyer runs a CarFax or similar report, that accident history is a permanent red flag.

Right away, questions pop into their head. Was the frame bent? Are there underlying problems waiting to surface? That doubt is powerful, and it means they will not pay the same price for your car as they would for an identical one with a squeaky-clean record.

A study from the University of Richmond confirmed what we see in the market every day: cars with damage history sell for significantly less. This stigma sticks around no matter how good the repairs look, and it's the very foundation of inherent diminished value.

This loss is "inherent" because it's now part of the car's story forever. It’s the permanent scratch on the watch—you can’t polish it away.

Repair-Related Diminished Value

While inherent diminished value assumes the repair work was perfect, Repair-Related Diminished Value kicks in when it's not. This is the extra loss in value caused by shoddy workmanship or the use of cheap, non-original parts.

This is where you can often see and feel the problems:

- Mismatched Paint: The new paint on the bumper is a slightly different shade of red that only shows up in direct sunlight.

- Uneven Panel Gaps: The new door doesn't sit quite right, creating a wider gap near the front fender than at the back.

- Aftermarket Parts: The insurance company approved a cheaper, aftermarket headlight that doesn't fit as snugly as the original.

- Lingering Issues: You notice a new rattle from the dashboard or the steering wheel is now off-center by a hair.

This is the knock-off movement in our watch analogy. The problem isn't just historical; it's a tangible, present-day flaw that makes the car objectively worse than it was. The good news? This type of diminished value is often easier to prove because you can literally point to the evidence.

Immediate Diminished Value

The third category is a bit different and doesn't come up in most standard claims. Immediate Diminished Value is the loss in value before any repairs are done. It’s the difference between your car’s pre-accident value and what it’s worth as a wrecked, damaged vehicle sitting on a tow lot.

This number really only comes into play in specific situations, like if you decided to sell the car as-is without fixing it, or if a legal dispute arises before the repair process even starts. For the vast majority of drivers, the focus will be squarely on the first two types of diminished value after the car is back on the road.

What Determines Your Car's Actual Value Loss

When people ask, "how much does an accident devalue a car?" there’s never one simple answer. You could have two identical cars get into very similar accidents, yet one might lose $2,000 in value while the other loses $6,000. That gap isn't random. It’s the result of several key factors that appraisers and, more importantly, potential buyers weigh heavily.

Getting a handle on these variables is the first step to understanding what your own car's situation looks like. The loss in value isn't just about the bent metal—it's about how that damage becomes a permanent part of the car's story, its appeal on the market, and the risk the next owner feels they're taking on.

Your Car’s Pre-Accident Profile

Before we even get to the collision itself, your car's basic stats set the stage for how much value is on the table to be lost. Think of it as its starting point on the value ladder; the higher it starts, the more rungs it can fall.

-

Age and Mileage: Newer, low-mileage vehicles always take the biggest hit. Buyers shopping for a nearly new car expect perfection, so an accident history is a massive red flag that sends the value tumbling. On the flip side, an older car with 150,000 miles has already lost most of its value to normal depreciation, so the added drop from an accident is far less dramatic.

-

Make, Model, and Trim: Luxury, exotic, and high-performance cars get hammered by this. Brands like Mercedes-Benz, BMW, or Porsche are built on a reputation for precision engineering. An accident, especially one that touched the frame or suspension, plants a seed of doubt: can that performance and safety really be restored to factory spec? A common family sedan just doesn't carry that same burden of perfection.

-

Pre-Accident Condition: Let's be honest—was your car immaculate before the crash, or did it already have its fair share of dings, scuffs, and interior wear? A car that was already in fair or poor shape will see a smaller diminished value claim simply because its starting value was already lower.

Typically, new cars lose around 16% of their value in the first year and another 12% in the second, leaving them with an average value retention of just 45% after five years. An accident makes this cliff even steeper. For instance, a $45,000 new car might be worth $20,250 after five years of normal use. An accident during that time can easily slice an extra 10-20% off that already depreciated value. You can find more great insights into how car depreciation is calculated at Experian.

The Nature of the Damage and Quality of Repairs

Once we know the car's starting point, the specifics of the wreck and the quality of the fix-up become the most critical factors. This is where the story of the accident gets written, and believe me, savvy buyers read every line.

A minor fender-bender that just needed a new bumper cover is one thing. But a high-speed collision that resulted in frame straightening and deployed airbags? That's a completely different story.

The single biggest factor in determining how much value is lost is whether the vehicle sustained structural or frame damage. Any compromise to the car's core structure is a permanent red flag for safety and reliability.

The quality of the repair work is just as crucial. A top-notch job can help minimize the loss, while shoddy work will make it exponentially worse. Here's what really matters:

-

OEM vs. Aftermarket Parts: Repairs done with Original Equipment Manufacturer (OEM) parts are always the gold standard. These are the exact parts the automaker designed for the car. Using cheaper, aftermarket parts is a dead giveaway of a cost-cutting repair and immediately drags the value down further.

-

Visible Flaws: Any obvious sign of a subpar repair—think mismatched paint, panel gaps that aren't quite right, or overspray on the trim—will drastically increase the value loss. These are the tangible flaws that any educated buyer will spot from a mile away.

-

Title Branding: In the worst-case scenarios, a major accident can result in the car being issued a "salvage" or "rebuilt" title. This is the ultimate scarlet letter for a vehicle, slashing its market value by 50% or more and making it incredibly difficult to sell at any price.

How to Calculate Your Car's Diminished Value

So, how do you put an actual dollar amount on your car's lost value? This is where the rubber meets the road. While the number might seem pulled from thin air, there are established methods to figure it out. The most common starting point, especially for insurance companies, is a formula known as "Rule 17c."

Understanding this formula is key, as it gives you a peek into the insurance adjuster's playbook. But it's just as important to recognize its serious flaws and why their first offer is usually just the start of the conversation, not the final word.

The Rule 17c Formula Explained

The Rule 17c formula isn't a law; it's more of an industry shortcut that originated from a Georgia court case. Insurers love it because it’s a simple, standardized way to spit out a number. Let's walk through how they do it.

Everything starts with your car's market value before the accident, which you can estimate using guides like Kelley Blue Book or NADAguides.

-

Start with the Pre-Accident Value: Let's imagine your car was worth $30,000 before the crash.

-

Apply the 10% Cap: The formula immediately caps the maximum possible diminished value at 10%. So, $30,000 x 0.10 = $3,000. This $3,000 becomes the absolute highest value we can start with.

-

Apply a Damage Multiplier: Next, they apply a multiplier based on the severity of the damage. This part is pretty subjective, but it generally follows this kind of scale:

- 1.00: Severe structural damage

- 0.75: Major panel damage

- 0.50: Moderate panel damage

- 0.25: Minor panel damage

- 0.00: No structural damage or replaced panels

If your car had major panel damage, they’d multiply the starting figure by 0.75. That brings our number down to $3,000 x 0.75 = $2,250.

-

Apply a Mileage Multiplier: Finally, they reduce the number again based on mileage. The logic here is that a high-mileage car has already lost most of its value, so a wreck doesn't hurt it as much.

- 1.00: 0-19,999 miles

- 0.80: 20,000-39,999 miles

- 0.60: 40,000-59,999 miles

- 0.40: 60,000-79,999 miles

- 0.20: 80,000-99,999 miles

- 0.00: 100,000+ miles

If your car had 45,000 miles, we'd use the 0.60 multiplier. This gives us our final number: $2,250 x 0.60 = $1,350. According to Rule 17c, your diminished value is just $1,350.

The Problem with Formulaic Approaches

As you can see, that final number is a tiny fraction of our starting point. Critics argue—and I agree—that this formula is built from the ground up to produce lowball offers.

It completely ignores crucial real-world factors. Things like your vehicle's make and model (a wrecked Porsche loses more value than a wrecked Honda), its pre-accident condition, or what buyers in your specific local market are willing to pay. That arbitrary 10% cap is especially damaging to a fair valuation.

Insurance companies often rely on formulas like 17c because they are consistent and predictable. However, they fail to capture the real-world market dynamics that truly determine how much an accident devalues a car.

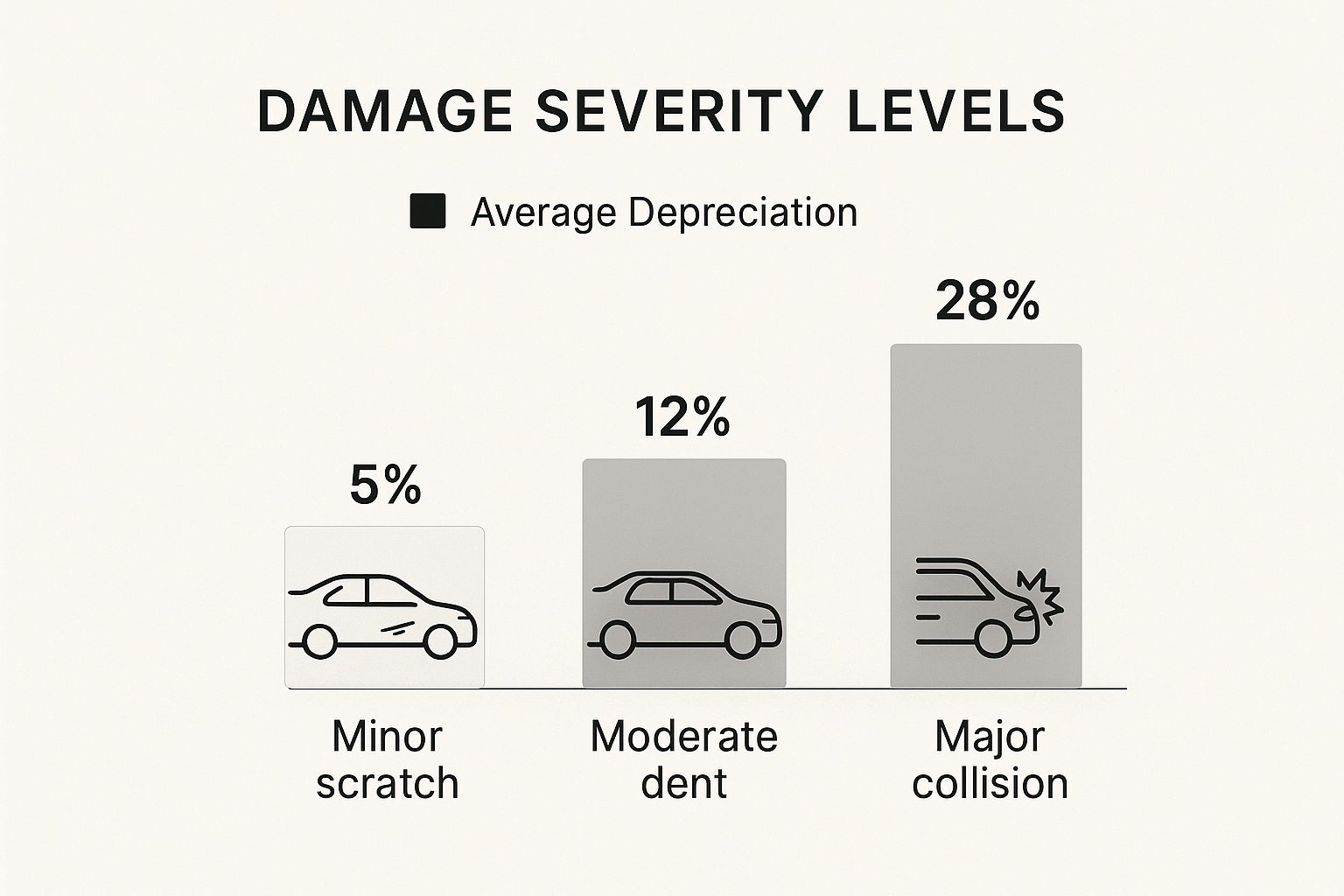

This infographic gives you a much more realistic picture of how damage severity actually impacts a car's resale value in the real world.

It’s pretty clear that major collisions can cause a value drop far greater than the 10% limit imposed by these simplistic formulas. You can get a better feel for this by running some numbers through a car value after accident calculator.

A formula like Rule 17c is a handy tool for an insurance company, but it's not the right tool for a vehicle owner seeking fair compensation. For that, you need a true expert.

Comparing Diminished Value Calculation Methods

Understanding the insurance company's formula is one thing, but getting a truly fair assessment requires a different approach. The table below compares the industry-favored formula with the method that actually works for vehicle owners: a professional appraisal.

| Method | Accuracy | Cost | Best For |

|---|---|---|---|

| Rule 17c Formula | Low. Relies on arbitrary caps and multipliers, ignoring market specifics. | Free (used by insurers). | Insurance companies looking for a quick, low, and standardized payout. |

| Professional Appraiser | High. Based on physical inspection, market research, and expert analysis. | Typically $300-$700. | Vehicle owners who need a credible, evidence-backed report to negotiate a fair settlement. |

While using a basic formula costs you nothing upfront, it can cost you thousands in the end. The most reliable path to determining your car's true loss in value is to bring in a professional.

The Professional Appraiser: The Gold Standard

While the 17c formula helps you anticipate the insurer’s opening move, the most accurate and authoritative way to determine your car’s diminished value is to hire a certified, independent auto appraiser.

An independent appraiser doesn't use a generic formula. They conduct a deep-dive analysis tailored specifically to your vehicle and its situation. Their process is thorough and evidence-based:

- A Physical Inspection: They get hands-on with the vehicle, meticulously checking the quality of the repairs. They’re looking for things you’d miss, like mismatched paint, poor panel gaps, or subtle signs of structural work.

- Market Research: They dig into the data, researching what identical, accident-free cars are actually selling for right now in your local area.

- Dealer Quotes: This is a crucial step. They will often call multiple dealership managers and ask them point-blank, "How much less would you offer for this car on trade-in, knowing it has this specific accident history?"

- A Detailed Report: You don't just get a number; you get a comprehensive, multi-page report. It lays out their entire methodology and provides the evidence to justify their final diminished value figure.

A professional report carries immense weight in a negotiation. It elevates your claim from "this is what I think I'm owed" to a documented, expert-backed assessment of your true financial loss. It's the single most powerful tool you can have in your corner when fighting for what you're rightfully owed.

A Step-By-Step Guide to Your Diminished Value Claim

Knowing your car has lost value is one thing, but actually getting that money from an insurance company is a whole different ballgame. It takes a methodical approach. Filing a diminished value claim isn't about simply asking for money—it's about building a rock-solid, evidence-based case that an insurance adjuster can't just brush aside.

Think of it like you're a detective building a case file. Every photo, every receipt, and every expert opinion adds another layer of undeniable proof. The goal is to present a clear, compelling argument that your vehicle is worth less because of someone else's mistake, and you've got the paperwork to prove exactly how much.

First, Confirm You're Eligible to File a Claim

Before you pour time and energy into this, you need to make sure you can even file a claim in the first place. Diminished value claims are almost always filed against the at-fault party's insurance, not your own. If you caused the accident, you generally can't claim this from your own insurer.

On top of that, state laws can be tricky. Most states give you the green light to go after a third-party diminished value claim, but a handful have specific restrictions. A quick check on your state’s rules is a critical first step. If the other driver was at fault and your state is on board, you're clear to move forward.

Next, Assemble Your Evidence and Documentation

This is where the real work begins, and it's the most important part of the entire process. An adjuster’s job is to minimize what their company pays out, and a claim with flimsy evidence is an easy one to deny. You need to gather a complete package of documents that backs up every part of your claim.

Your paperwork should paint a clear before-and-after picture of your car's value and condition.

- Police Accident Report: This is the official document that points the finger and establishes who was at fault.

- Photos and Videos: Snap pictures of the damage right after the crash and even during the repair process if you can.

- Repair Invoices: Make sure you get a final, itemized bill from the body shop. It should detail every single part that was replaced and all the labor performed.

- Proof of Pre-Accident Value: Use reliable sources like KBB or NADAguides to establish what your car was worth on the open market before the collision.

- A Professional Diminished Value Appraisal: This is your secret weapon. A report from a certified, independent appraiser gives you an expert, unbiased assessment of your financial loss.

A professional appraisal report takes your claim from a simple request and turns it into a formal, evidence-backed demand. It effectively shifts the burden of proof to the insurance company, forcing them to explain why their number is any more accurate than an independent expert’s.

This isn’t just a local issue, either. The hit a car’s value takes after an accident is a well-known phenomenon around the world. In major automotive markets like the USA, Germany, and Japan, even a minor fender-bender can slash a car’s resale value by 10-20%, on top of its normal annual depreciation. Looking at global auction data, cars with accident histories can sell for a staggering 30-50% less than identical, undamaged models. You can dig deeper into these global trends by exploring findings on international automobile depreciation.

Finally, Draft and Submit a Formal Demand Letter

Once you have all your evidence lined up, it's time to formally make your case. You'll do this with a demand letter—a professional document sent to the at-fault driver's insurance adjuster that lays out your entire claim. Keep it clear, concise, and firm.

Your letter needs to include your personal details, the claim number, and a brief summary of the accident. Most importantly, it must state the exact amount of diminished value you are demanding and point directly to your professional appraisal report as the basis for that number. You can see exactly how to put this critical document together by checking out our guide on writing an effective insurance demand letter.

After you send it, get ready to negotiate. The adjuster will almost certainly come back with a lowball counteroffer, probably citing some internal formula they use. This is where your preparation pays off. Stand your ground, keep referring back to your professional appraisal, and calmly defend your position. Your hard work in building this case is your biggest advantage in getting the fair compensation you deserve.

Your Top Questions About Diminished Value Claims, Answered

After a car wreck, you’re left with a lot to sort out. Once you’ve wrapped your head around the different kinds of diminished value and how it’s calculated, a few specific questions always seem to pop up. Let’s tackle the most common ones we hear from car owners every day.

Getting these answers straight is crucial. They can be the difference between getting paid what you’re owed and walking away empty-handed. Let’s clear up the confusion so you can move forward with confidence.

Can I File a Claim If the Accident Was My Fault?

This is easily the most frequent—and most important—question we get. The short answer is almost always no.

Think of a diminished value claim as a way to hold the at-fault driver responsible for the full scope of the damage they caused. Their insurance company's job is to make you "whole" again. That doesn't just mean fixing the dents; it means compensating you for the hit your car’s market value took because of the accident history.

- Third-Party Claim: This is when you file against the other driver's insurance. This is the only place a diminished value claim really exists.

- First-Party Claim: This is when you file with your own insurance, like for a collision claim. Insurance policies are specifically written to exclude paying for diminished value on these first-party claims.

So, if you caused the accident, you can't claim diminished value from your own insurer. The entire process hinges on someone else being responsible for the damage.

Is There a Time Limit for Filing a Claim?

Yes, absolutely. This is a hard deadline you cannot afford to miss. It’s called the statute of limitations, and it’s the legal window you have to file a lawsuit over property damage. Every state sets its own timeline.

Miss this deadline, and you forfeit your right to pursue the claim forever, no matter how strong your case is.

The statute of limitations for property damage usually falls somewhere between two to six years, depending on your state. It's critical to figure out your state's deadline right after the accident so you don't accidentally run out of time.

For example, if your state has a three-year window, waiting three years and one day means your claim is legally dead. That’s why we always tell people to start the diminished value process the moment their car repairs are finished. Don't put it off.

Will a Diminished Value Claim Raise My Insurance Rates?

This is a huge fear that stops people from getting the money they’re legally owed. But here’s the good news: if you are the victim in the accident and filing against the at-fault driver's insurance, it should not affect your insurance rates.

Your insurance premiums are based on the risk you pose as a driver. When someone else hits you, the accident doesn't reflect poorly on your driving record. You are simply asking the responsible party’s insurer to cover the full loss their client caused.

A couple of things to keep in mind:

- No-Fault States: The rules in "no-fault" states can get a bit tricky, but this system usually applies to bodily injury claims. Property damage, including your car’s diminished value, is still almost always handled based on who was at fault.

- "Claim Forgiveness" Programs: Many policies have a feature that prevents a rate hike after your first at-fault accident. That doesn’t apply here because a diminished value claim isn't an at-fault claim on your record.

Filing against another driver’s policy is not the same as filing against your own. You’re holding their insurance carrier accountable, which is a fundamental part of how the system is supposed to work. You should never be penalized for exercising your right to be fully compensated for the accident's impact on your car's value.

At Total Loss Northwest, we specialize in empowering vehicle owners with the certified appraisals needed to win these fights. If your car's value has dropped due to an accident that wasn't your fault, don't leave money on the table. We provide the expert documentation and support you need to secure a fair settlement. Learn more about how we can help at our official website.