Hearing that your car is a "total loss" can be a shock, but it’s important to know what that really means. It's not about how bad the damage looks; it's a purely financial calculation made by your insurance company.

Simply put, an insurer declares a vehicle a total loss when the cost to repair it safely is more than what the car was worth right before the accident. This decision is the starting point for everything that follows in your claim.

What It Means When Your Car Is Totaled

When an adjuster tells you your car is "totaled," they're looking past the twisted metal and broken glass. They're making a business decision based on a specific formula.

Think of it this way: if a contractor told you that fixing the storm damage to your roof would cost more than your entire house is worth, you wouldn't do it. You'd take the insurance payout and start fresh. It's the exact same logic with your car.

The core of the total loss calculation for a vehicle is a simple comparison. The insurer weighs the estimated cost of repairs against the car's market value just before the crash. If fixing it costs more than its value, they'll declare it a total loss because it's the more sensible financial path.

The Financial Crossroads

Grasping this concept is key because it completely changes the focus of your claim. As soon as your car is officially a total loss, the conversation stops being about body shops and repair timelines. Instead, it pivots to valuation reports, settlement amounts, and negotiation.

The insurance company's main job at this point is to figure out your car's Actual Cash Value (ACV)—what someone would have reasonably paid for it one minute before the accident happened. That ACV number is the baseline for the settlement they will eventually offer you.

Here’s what happens behind the scenes to get to that point:

- Damage Assessment: First, an appraiser goes over your car with a fine-tooth comb to write up a detailed estimate of what it would cost to fix everything properly.

- Value Determination: At the same time, the insurer researches the market to pinpoint your car's ACV, looking at its specific year, make, model, mileage, and overall condition.

- State Regulations: Every state has its own rules, called total loss thresholds, that set the exact damage-to-value percentage that legally requires a car to be totaled.

A "total loss" is just insurance-speak for the moment it no longer makes financial sense to repair a vehicle. It's the tipping point where the repair bill gets too close to—or exceeds—the car's actual worth.

This initial decision really sets the stage for the rest of the claims process. For a closer look at the nuts and bolts, you can learn more about what makes a car get totaled in our detailed guide. Understanding this first step is the best way to prepare yourself for the settlement discussions ahead.

How Insurers Calculate Your Vehicle's Value

So, how does an insurance company decide whether to fix your car or write it off? It all comes down to a straightforward financial formula. They compare two key figures: the total cost to repair the damage versus your car's Actual Cash Value (ACV) at the moment right before the crash.

Think of the ACV as your car's fair market value. It's what someone would have reasonably paid for your exact vehicle—same mileage, condition, and options—just before the accident happened. If the repair bill looks like it will exceed this value, the insurer will almost always declare it a total loss.

This is happening more often than ever. In 2023, a record-breaking 27% of vehicles in collision claims were totaled. As cars get packed with more complex technology, even a fender-bender can damage expensive sensors and systems, driving repair costs sky-high. You can read more about this rising trend at GMAthority.com.

Pinpointing Your Car's Actual Cash Value

The ACV is the most critical piece of the puzzle, and it’s where things can get a bit subjective. This isn't just about looking up a number in a book. Insurers use sophisticated software to pull data from multiple sources to land on a very specific value for your car.

They start with the basics—year, make, and model—but then they drill down into the details that make your car unique.

Figuring out this pre-accident value is a multi-step process. Here’s a closer look at what goes into the calculation.

| Factor | Description | Impact on Value |

|---|---|---|

| Year, Make & Model | The foundational identity of your vehicle. | A major driver of baseline value. |

| Mileage | The total distance the vehicle has been driven. | Lower mileage typically increases value; higher mileage decreases it. |

| Condition | Pre-accident state, including any prior damage, wear, or exceptional upkeep. | A well-maintained vehicle is worth more than one with dings and dents. |

| Options & Trim | Factory-installed features like a sunroof, navigation, or leather seats. | Higher trim levels and desirable options add significant value. |

| Local Market Data | Sales data for similar vehicles that have recently sold in your area. | Establishes the real-world, current market price for your specific car. |

Getting familiar with these factors is your best defense against a lowball offer. For a deeper dive, you can learn more about what Actual Cash Value means for your car in our dedicated article. This knowledge is key to making sure the insurer's number is fair.

Calculating the Full Cost of Repairs

The other side of the equation is the repair estimate, and it's far more than just the cost of a new bumper. A proper estimate has to cover every single expense needed to bring the car back to its pre-accident condition, both structurally and electronically.

The repair estimate is a comprehensive list of all parts, labor, and specialized procedures needed for a complete and safe restoration. This includes everything from paint and materials to complex sensor recalibrations.

For instance, a simple-looking front-end impact isn't so simple anymore. The final estimate has to account for all of it:

- Labor Costs: The number of hours a qualified technician will need to do the job right.

- OEM vs. Aftermarket Parts: The cost and quality of the specific parts required for the repair.

- Sensor Recalibration: Modern cars rely on Advanced Driver-Assistance Systems (ADAS). After a collision, these cameras and sensors must be professionally recalibrated, which is a pricey, specialized task.

- Hidden Damage: Sometimes, the true extent of the damage isn't clear until the shop starts taking the car apart. The estimate has to be flexible enough to include these discoveries.

The claims adjuster adds up every last line item to arrive at the total repair cost. Once they have that number and the ACV, they can make the final call on your vehicle.

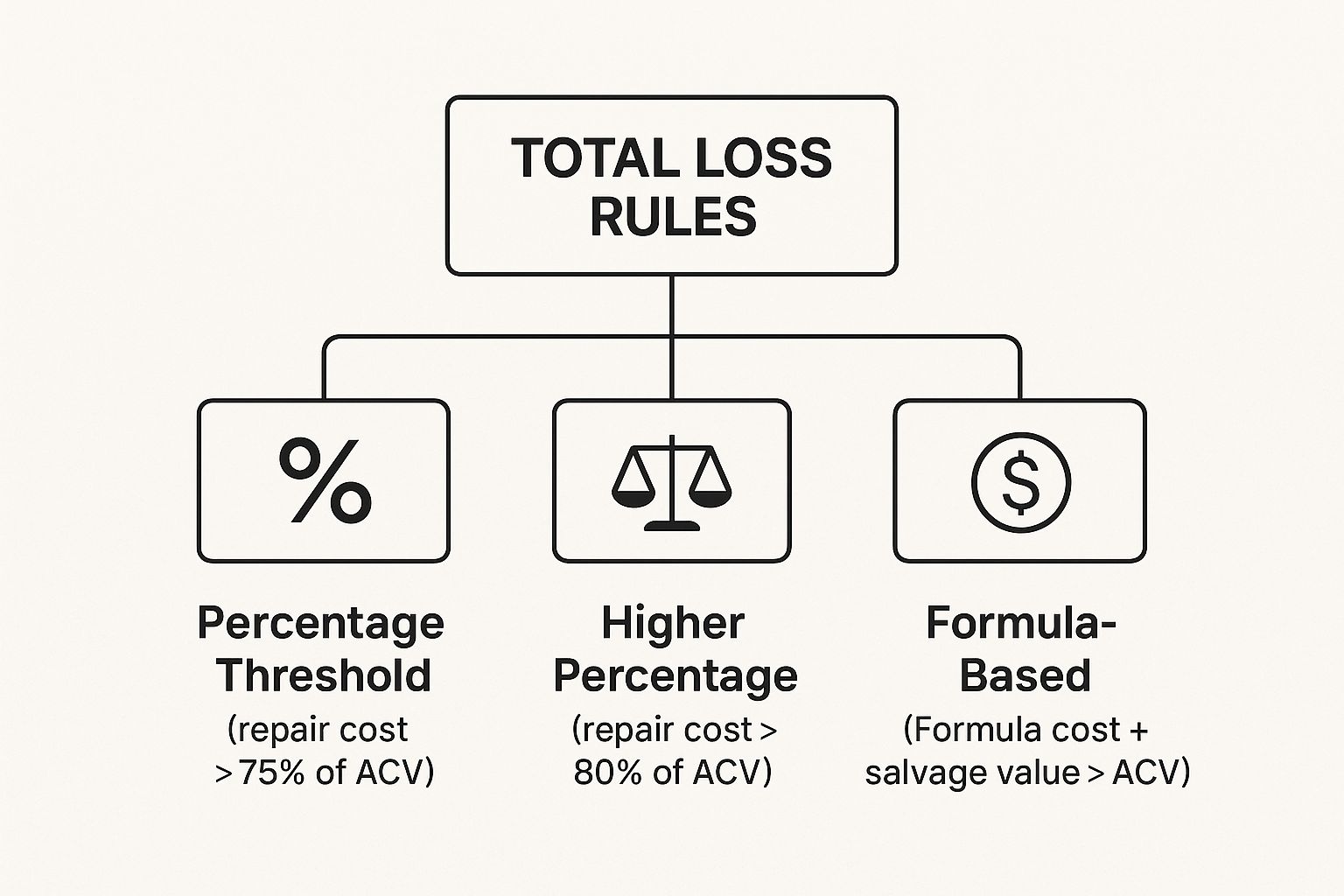

Understanding State-Specific Total Loss Rules

Deciding whether to total a car isn't a one-size-fits-all process. In fact, the rules can change dramatically just by crossing a state line. The entire total loss calculation for a vehicle hinges on local laws, which means a car that’s considered perfectly repairable in one state might be instantly declared a total loss just a few miles away.

These state-specific regulations are what we call Total Loss Thresholds (TLT). Think of them as a legal line in the sand. Once the cost to fix your car crosses that line, the insurance company is often legally required to declare it a total loss and issue a salvage title.

This threshold is the specific rule that dictates exactly how much damage a car can take before it's officially written off.

The Two Main Types of State Thresholds

States generally take one of two routes to figure out this cutoff point. While the end goal is the same—to get dangerously damaged vehicles off the road—the math they use to get there is quite different.

The most common method is the Percentage-Based Threshold. In these states, a vehicle is totaled if the repair estimate climbs past a certain percentage of its Actual Cash Value (ACV). That percentage can vary quite a bit from state to state, but a common figure is 75%.

For instance, if you're in a state with a 75% threshold and your car has an ACV of $20,000, it will be declared a total loss if the repair bill is more than $15,000 ($20,000 x 0.75).

The second approach, used by a smaller group of states, is the Total Loss Formula (TLF). This calculation is a bit more involved because it doesn't just look at repair costs. It also factors in the car's salvage value—the cash the insurer can get back by selling the wrecked vehicle for parts or scrap.

Under the TLF, your vehicle is a total loss if: Cost of Repairs + Salvage Value > Actual Cash Value

This formula prevents a situation where repairing the car might seem cheaper on the surface, but would actually cost the insurance company more than just paying you the ACV and selling off the wreck.

This infographic breaks down how these different rules work.

As you can see, the specific rule your state follows—whether it's a simple percentage or the more complex formula—is what ultimately drives the final decision on your claim.

How State Rules Impact Your Settlement

Let's walk through a real-world scenario to see how this all shakes out. Imagine your car has an ACV of $10,000, a salvage value of $2,000, and the body shop estimates repairs at $7,800.

- In a state with an 80% TLT: The line in the sand is $8,000 ($10,000 x 0.80). Since the $7,800 repair cost is below this, the insurer would probably fix the car.

- In a state with a 75% TLT: The threshold drops to $7,500 ($10,000 x 0.75). Now, that $7,800 repair cost is above the limit, making the car a mandatory total loss.

- In a TLF state: The math is $7,800 (Repairs) + $2,000 (Salvage) = $9,800. Since $9,800 is still less than the $10,000 ACV, the insurer would likely opt to repair it.

To give you a better idea of the variation across the country, here are a few examples of state thresholds.

Example of State Total Loss Thresholds

| State | Threshold Type | Threshold Percentage |

|---|---|---|

| Texas | Percentage | 100% |

| Colorado | Percentage | 100% |

| Florida | Percentage | 80% |

| Iowa | Percentage | 70% |

| Massachusetts | Total Loss Formula (TLF) | N/A |

As you can see, a car with damage equal to 90% of its value would be repaired in Texas but totaled in Florida.

Knowing your state's specific threshold is a huge advantage. It helps you understand the adjuster's reasoning and gives you the power to double-check that they're applying the law correctly to your total loss calculation vehicle settlement.

It might seem like you're hearing about cars being "totaled" more than ever these days. You're not imagining things. The insurer's decision to write off a car isn't just about the damage from your accident—it’s also a reflection of huge economic shifts happening across the auto industry.

Several powerful trends are making it more common for insurance companies to declare a vehicle a total loss rather than pay for repairs. The biggest culprits are skyrocketing repair costs, fueled by increasingly complex cars and stubborn supply chain problems that make parts both expensive and hard to come by.

Why Are Repairs So Expensive Now?

Modern cars are essentially computers on wheels. A simple fender-bender isn't so simple anymore. What used to be a straightforward bumper replacement now often means recalibrating an entire suite of sensitive cameras and sensors that run critical safety systems like automatic braking or lane-keeping assist. This isn't a job for any mechanic; it requires specialized tools and expertise, sending labor costs through the roof.

An accident that might have been a few hundred bucks to fix ten years ago can now easily turn into a multi-thousand-dollar repair bill. When the cost to fix gets that high, it doesn't take much for it to creep dangerously close to the car's actual value, making a total loss almost inevitable.

On top of that, there’s a real shortage of skilled auto body technicians, which means shops have to pay more to retain good people. It's a perfect storm: advanced technology, pricey parts, and high labor rates mean even moderate damage can push the total loss calculation for a vehicle past the point of no return.

Shaky Car Values and Financial Headwinds

The other side of this coin is the rollercoaster of used car values. The last few years have been wild for the used car market, and this directly impacts your car's ACV calculation. When used car prices are sky-high, it can make more sense to repair a damaged vehicle. But when those values drop, it becomes much easier for a car to be declared a total loss.

This financial climate hits car owners hard, too. A Q1 2025 report shows that while average car values have bumped up a bit, many people are stretched thin. In fact, in late 2024, a staggering 25% of new vehicle loans were underwater—meaning the owner owed more than the car was worth—by an average of nearly $7,000. You can dig deeper into these trends in the CCC Intelligent Solutions Crash Course report.

When you boil it all down, three key market forces are driving up the number of total loss claims:

- Complex Car Tech: The astronomical cost of repairing and recalibrating sensors and advanced driver-assistance systems (ADAS).

- Pricey Parts and Labor: Ongoing supply chain headaches and a shortage of qualified techs make every repair more expensive.

- Economic Squeeze: Wild swings in used car values and financial pressure on car owners change the math for everyone involved.

What does this all mean for you? It means insurers are crunching the numbers more carefully than ever. The settlement offer you receive is a direct result of this new reality, where fixing cars is often just too expensive to make financial sense.

How to Negotiate Your Total Loss Settlement

When the insurance company sends over their settlement offer, it can feel like the end of a long road. But that first number you see? It’s just that—an offer. It’s a starting point for a conversation, not a final decision. If that offer feels low, you have every right to question it and negotiate for what your vehicle was actually worth.

Remember, the adjuster's job is to close the claim based on their valuation. That valuation might have missed a premium sound system, recent repairs, or the fact that you kept your car in pristine condition. Your job is to fill in those gaps with evidence. The goal isn't to be difficult; it’s to be prepared.

Step 1: Start With the Insurer's Report

Your first move is always to ask for a copy of the valuation report. This is the document the insurance company used to calculate their offer, and it’s the blueprint for their entire total loss calculation vehicle assessment.

Don't just give it a quick glance. You need to go through this report with a fine-toothed comb, looking for any mistakes. Pay close attention to:

- Vehicle Trim and Options: Did they list your car as the base model when you had the fully-loaded Limited trim? This happens all the time.

- Mileage: It seems basic, but is the mileage accurate? A typo here can make a difference.

- Overall Condition: Check how they rated your car's pre-accident condition. If they marked it as "fair" but you have service records to prove it was "excellent," you've found a major negotiating point.

The insurer's valuation report is your roadmap for the negotiation. Errors in this document are the fastest and easiest way to prove your vehicle was undervalued.

Even small errors can add up. A missed factory option or an incorrect trim level can easily swing the Actual Cash Value by hundreds, if not thousands, of dollars.

Step 2: Build Your Counter-Offer With Evidence

Now that you know where they're coming from, it's time to build your own case. Simply telling the adjuster their offer is too low won't get you very far. You need to show them why with hard evidence. This is where you become a detective.

Your mission is to find "comps"—comparable vehicles for sale in your local market—that support a higher value. You're looking for real-world proof of what it would cost to buy your exact car right before the accident happened.

To make a convincing argument, you should gather:

- Comparable Listings: Scour online marketplaces and local dealer sites for cars that are the same make, model, year, and trim as yours, with similar mileage. Save screenshots or printouts of at least three to five local listings priced higher than the insurer's valuation.

- Documentation of Recent Upgrades: Did you just put on a new set of tires, replace the battery, or upgrade the stereo? Pull together the receipts for any significant investments you made right before the crash.

- Maintenance History: Meticulous care adds value. If you have a thick folder of service records proving your car was exceptionally well-maintained, it justifies a higher condition rating than "average."

Step 3: Consider the Appraisal Clause

What happens if you've presented all your evidence and you're still at a stalemate with the adjuster? Your policy likely contains a powerful tool you can use: the Appraisal Clause.

Invoking this clause moves the negotiation to a more formal process. Here's how it works: You hire an independent, certified auto appraiser, and the insurance company hires their own. The two appraisers then work together to agree on the vehicle's value. If they can't reach an agreement, they bring in a neutral third appraiser (an umpire) to cast the deciding vote. The final number is binding for both sides.

This takes the decision out of the hands of the insurance adjuster and places it with unbiased market experts. It ensures the final total loss calculation for your vehicle is based on real-world data, not just the insurer's internal software.

If you want to dig deeper into the process, you can explore how to negotiate a total loss settlement effectively and arm yourself with the right information. A successful challenge always comes down to having the data to back up your claim.

Common Questions About Total Loss Claims

https://www.youtube.com/embed/7CylFept2Jw

Dealing with a total loss can be a confusing time, and it’s completely normal to have a lot of questions. Once the insurance company runs the total loss calculation for your vehicle, you’ll have some big decisions to make about the settlement, your car loan, and what comes next.

Let's walk through some of the most common questions people have when their car is declared a total loss.

Can I Keep My Car If It Is Declared a Total Loss?

Believe it or not, yes—in almost every case, you have the option to keep your car. This is often called "owner-retained salvage." If you go this route, the insurance company will cut you a check for the car’s Actual Cash Value (ACV) minus what they would have gotten for it at a salvage auction.

But here’s the big catch: the car will be issued a salvage title. That means it isn't street-legal anymore. To get it back on the road, you'll have to get it professionally repaired and then pass a pretty tough state safety inspection to get the title changed to "rebuilt."

Keep in mind that insuring a car with a rebuilt title can be a real headache. Many insurance companies won't offer full coverage (comprehensive and collision) on them, and the premiums can be higher. It's a huge factor to consider before you decide to keep it.

How Long Does a Total Loss Claim Usually Take?

There's no single answer, but you can generally expect the whole process to take a few weeks from the day of the accident to the day you get paid. It isn’t just one step; it’s a sequence of events that have to happen in order.

Here’s a rough breakdown of the timeline:

- Initial Inspection: First, an appraiser has to look at the car and write up a detailed estimate of the repair costs.

- Valuation Research: This is often the longest part. The insurer digs into local market data to find comparable vehicles and figure out your car's ACV.

- Review and Offer: An adjuster reviews everything, officially declares the car a total loss, and then calls you with a settlement offer.

- Final Processing: Once you agree to the offer, it's just a matter of signing the paperwork and waiting for the payment to be processed.

One tip: you can help speed things up by getting all the requested documents back to your adjuster as quickly as possible.

Does Gap Insurance Cover My Remaining Loan Balance?

Yes, that’s exactly what it's for! If your car is totaled and the insurance settlement is less than what you still owe, you're "underwater" on your loan. This gap can easily add up to thousands of dollars you'd be stuck paying out of pocket.

GAP insurance is your financial safety net. It pays the difference between your vehicle's ACV and the outstanding balance on your loan, preventing you from making payments on a car you can no longer drive.

For example, say your car’s ACV is $15,000, but you still owe $18,000 on your auto loan. GAP coverage would step in and pay that $3,000 difference for you.

Will My Insurance Rates Increase After a Total Loss?

This almost always comes down to who was at fault. If the other driver caused the accident and their insurance is paying the claim, your rates shouldn't go up.

However, if you were at fault for the accident, you should probably expect your premium to increase at your next policy renewal. It’s also worth noting that some insurers might raise rates simply based on claim frequency, regardless of who was at fault. The best move is to check your policy or have a quick chat with your agent to see how a claim might affect your future premiums.

Navigating a total loss settlement can be challenging, but you don't have to do it alone. If you feel the insurer's offer is unfair, Total Loss Northwest can help. Our certified appraisers will conduct a thorough, independent valuation of your vehicle to ensure you receive the full compensation you deserve. Visit us at https://totallossnw.com to get an expert on your side.