It’s a tough situation, and one that catches a lot of people by surprise. When your financed car is declared a total loss, there's one hard truth you need to know right away: you are still responsible for paying off the entire car loan, even though the vehicle is now a wreck.

Your insurance company’s job is to cut a check for what the car was worth right before the crash. But if that amount doesn't cover your full loan balance, you're on the hook for the rest.

Your Financial Responsibility After a Total Loss

Many drivers think that if their car is gone, the loan must be gone too. Unfortunately, that's a common and costly misunderstanding. Your loan agreement and your insurance policy are two completely separate contracts. The accident may have taken your car off the road for good, but your debt is still very much alive.

Suddenly, you're juggling a few different relationships. It helps to understand who's who and what they do in this process.

Understanding Who's Involved

When you total a financed car, you're dealing with a few key parties, and knowing their roles is crucial.

This table breaks down who is responsible for what.

Key Players and Their Roles After a Total Loss

| Player | Primary Role |

|---|---|

| You (The Borrower) | You’re responsible for keeping up with loan payments and acting as the go-between for the insurer and the lender to get the account settled. |

| Your Insurance Company | Their goal is to figure out the car's pre-accident value, called its Actual Cash Value (ACV), and pay out that amount. |

| Your Lender (The Lienholder) | Since they technically own the car until it's paid off, they get the insurance check first. They’ll apply it directly to what you owe. |

Once everyone's roles are clear, you can focus on getting the finances sorted out.

The Financial Reality of a Totaled Car

Let's be clear: the financial fallout from totaling a financed car can be a heavy hit. With the average new car loan in the U.S. sitting around $41,983 and used car loans at $26,795, that's a lot of debt to be left with. You’ve not only lost your transportation, but you could also be stuck with a big bill for a car you can't even drive anymore. Many owners find themselves under significant financial strain after an accident.

Key Takeaway: Think of your car loan like a mortgage. If a fire destroys a house, the homeowner still has to pay off the mortgage. It's the exact same principle with a car loan—the debt remains legally binding until it’s paid in full.

Grasping this one concept—that the loan outlives the car—is the most important first step. Once you understand your role and the lender's and insurer's, you'll be in a much better position to handle everything that comes next.

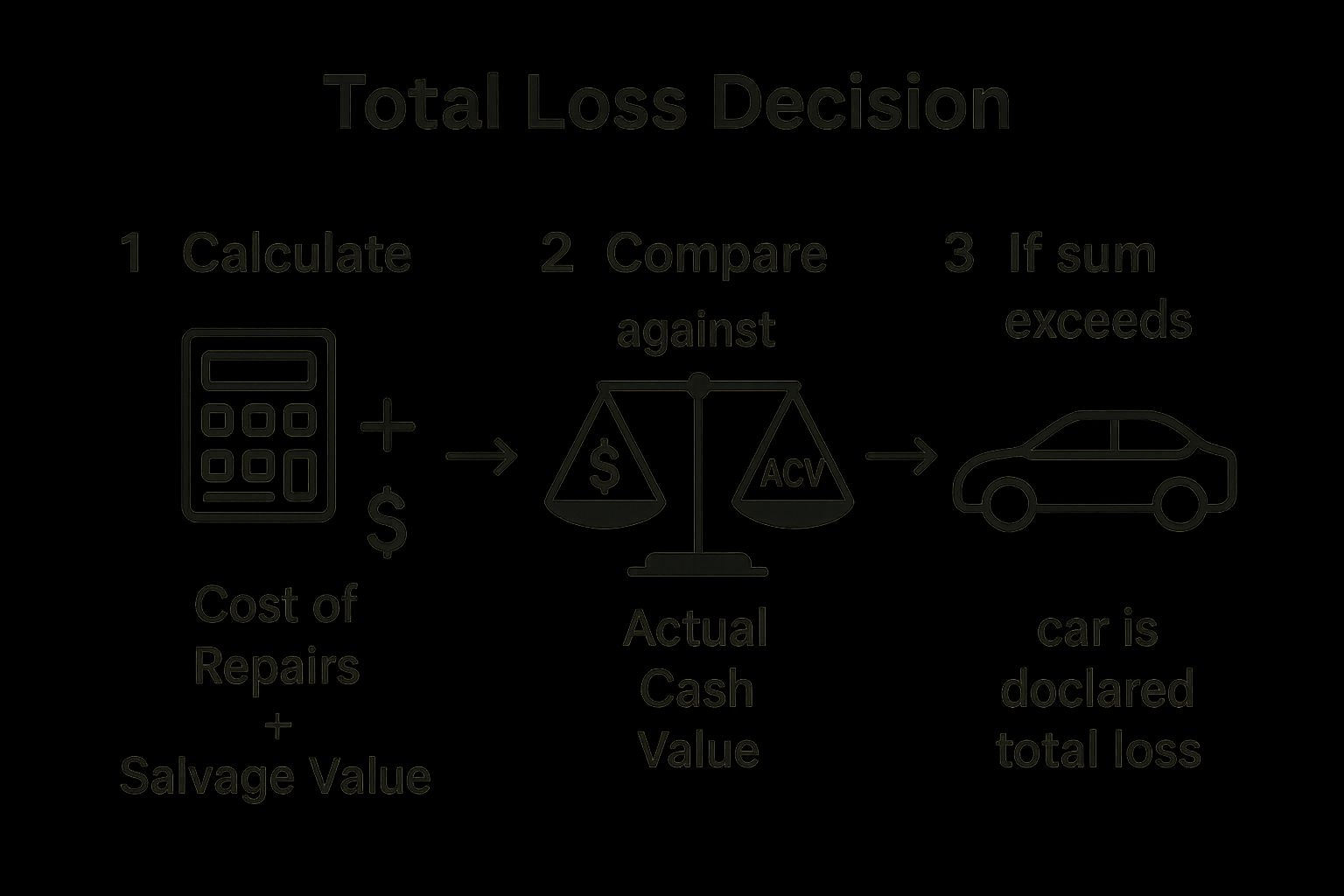

How Insurance Companies Decide a Car Is a Total Loss

When you hear the term "total loss," it's easy to picture a car mangled beyond recognition. But in the eyes of an insurance company, the decision has nothing to do with how the car looks—it's all about the numbers. The entire process boils down to a cold, hard business calculation.

An insurer will declare your car a total loss if the cost to repair it (plus what it's worth as scrap) adds up to more than the car's value right before the crash. This pre-accident value is a critical term you'll hear over and over: the Actual Cash Value (ACV).

The Actual Cash Value Explained

Forget what you paid for the car or what you still owe on the loan—the ACV is neither of those things. Instead, think of it as the fair market price for your vehicle just moments before the accident happened. It’s a snapshot of what someone would have reasonably paid for it in your local area.

To land on this number, insurance adjusters dig into several key details that shape a car's real-world worth.

- Age and Mileage: This one's straightforward. An older car with high mileage is naturally going to have a lower ACV.

- Condition: They'll account for any pre-existing dings, scratches, or serious wear and tear that your car already had.

- Recent Sales: Adjusters pull sales data for cars just like yours (same make, model, and year) in your local market to see what they've actually been selling for.

- Features and Trim: A fully-loaded model with a premium sound system and sunroof will have a higher ACV than the base model.

This infographic breaks down how insurers put these pieces together to make the final call.

As you can see, it's a purely mathematical comparison, not an emotional one. If the numbers show it's cheaper to pay you the ACV than to fix the vehicle, it's officially a total loss.

Understanding the Repair Estimate

The other side of this financial seesaw is the repair estimate. When a claims adjuster or body shop assesses the damage, the projected cost of repairs is a huge piece of the puzzle. This estimate, which can be influenced by the debate over OEM vs aftermarket parts, is what gets weighed against your car's ACV.

It's not just the insurer's internal policy, either. Many states have laws that dictate when a car must be totaled.

Key Insight: Most states have a specific Total Loss Threshold. For example, a state might mandate that an insurer must declare a vehicle a total loss if the repair costs exceed 75% of its ACV. This is designed to stop insurers from pouring money into a car that simply isn't worth saving from an economic standpoint.

Since the ACV is the foundation of your settlement check, you need to feel confident it’s a fair number. If the initial offer seems low, you absolutely have the right to challenge it. Getting familiar with the valuation process is your best first step—you can get a much clearer picture by looking into how to get a fair total loss estimate.

Following the Money from Insurance Payout to Loan Balance

Once your car has been officially declared a total loss, the financial puzzle pieces start moving. This is the moment where the reality of the situation really hits home. A common mistake people make is thinking the insurance check comes directly to them, but when there's a loan involved, the process works a bit differently.

Because you financed the vehicle, your lender is the lienholder. In simple terms, this means they have a legal claim on the car until you’ve paid off every last penny of the loan.

This lienholder status is key. It means the insurance company will send the settlement check—the payment for your car's Actual Cash Value (ACV)—straight to your lender, not to your mailbox. Your lender takes that payment and applies it to your outstanding loan balance, and what happens next will dictate your financial path forward.

The Best-Case Scenario: Positive Equity

In a perfect world, the insurance payout is more than what you still owe on the loan. This happy situation is called having positive equity.

Here's how that plays out:

- Loan Balance: Let's say you owe $13,000 on your car.

- Insurance Payout (ACV): The insurer determines your car's fair market value was $15,000.

- The Result: The lender gets the $15,000 check, pays off your $13,000 loan, and then cuts you a check for the $2,000 difference.

That surplus cash is yours to keep, and it makes a great down payment for your next vehicle. While losing your car is never fun, this outcome at least puts you back on solid financial ground.

The More Common Scenario: Negative Equity

Unfortunately, it's far more common for drivers to be "upside down" on their loan, which is known as having negative equity. This is the financial trap where the insurance payout is less than what you owe. The leftover debt is called a deficiency balance.

Key Takeaway: The deficiency balance is the gap between what your insurer pays and what you still owe your lender. Even though the car is gone, you are still legally on the hook for this amount.

Let's run the numbers for this all-too-common scenario:

- Loan Balance: You owe $18,000 on the car.

- Insurance Payout (ACV): The insurance company values your car at $15,000.

- The Result: The lender applies the $15,000 to your loan, but you're still left with a $3,000 deficiency balance that you must pay out of pocket.

This is where things can get really tough. Your lender will come looking for that $3,000, either as a lump-sum payment or through a new payment arrangement. This is why having a solid grasp of how your car's ACV is calculated is so critical—it's your main defense in ensuring the initial payout is as fair as possible. To get a better handle on this, you can learn more about what the actual cash value of your car is in our detailed guide.

Payout Scenarios With and Without Positive Equity

To see these two outcomes side-by-side, let's break down how your equity position completely changes the financial result of a total loss claim.

| Metric | Positive Equity Scenario | Negative Equity Scenario |

|---|---|---|

| Loan Balance | $13,000 | $18,000 |

| Insurance Payout (ACV) | $15,000 | $15,000 |

| Loan Paid Off? | Yes | No, $3,000 remains |

| Money to You | $2,000 check | $0 |

| Money You Owe | $0 | $3,000 deficiency |

As the table shows, starting with positive equity means you walk away with cash in hand. But if you have negative equity, you're left with a bill for a car you can no longer drive. This single factor is the most important part of the financial equation.

How GAP Insurance Can Be Your Financial Lifesaver

https://www.youtube.com/embed/BzFLWfeHqL8

The absolute worst part of totaling a financed car is getting hit with a "deficiency balance." This is the financial black hole that opens up when your insurance payout is less than what you still owe the bank. Suddenly, you're on the hook for a car that doesn't even exist anymore.

Luckily, there’s a specific type of coverage built for this exact nightmare scenario: Guaranteed Asset Protection (GAP) insurance.

Think of GAP insurance as your financial safety net. It’s an optional policy that has one job and one job only: to cover the difference—the "gap"—between your car’s ACV and the outstanding balance on your loan. This is what can turn a potential financial disaster into a minor inconvenience.

How GAP Insurance Works in the Real World

Let's go back to that negative equity example. You're in a tough spot where the math is working against you.

- Your Outstanding Loan Balance: $18,000

- Your Car’s ACV Payout: $15,000

- The Deficiency Balance: $3,000

Without GAP coverage, you’d be getting a bill from your lender for that leftover $3,000. Not fun.

But if you have a GAP policy, the story changes completely. After your main auto insurer sends the $15,000 to your lender, you simply file another claim with your GAP provider. They step in and pay the remaining $3,000 directly to the lender, and just like that, your debt is gone.

Key Insight: GAP insurance isn't a replacement for collision or comprehensive coverage. It’s a supplemental policy that rides shotgun with your primary insurance to protect you specifically from the risk of being upside down on your loan after a total loss.

This simple function can save you from a massive out-of-pocket expense and a whole lot of stress.

When Is GAP Insurance a Must-Have?

While the law doesn't require it, GAP insurance is something you should seriously consider if you find yourself in a few common situations. If any of these sound familiar, this coverage is practically essential.

- You made a small down payment: Putting less than 20% down on a new car is a classic recipe for immediate negative equity.

- You have a long loan term: Loans that stretch out past 60 months (five years) build equity incredibly slowly because your first few years of payments are mostly just interest.

- You rolled over debt: Did you trade in a car you were already upside down on? If you rolled that old debt into your new loan, you started out deep in the red.

- You drive a ton: High mileage tanks a car's value much faster than average, creating a huge gap between what it’s worth and what you owe.

Where to Get GAP Insurance

A common misconception is that you can only buy GAP insurance from the car dealership. While they'll certainly offer it, their policies are often rolled right into your auto loan, which means you end up paying interest on the premium itself.

You have better, and often cheaper, options:

- Your Auto Insurer: Most major insurance companies will let you add GAP coverage to your existing policy for just a few extra dollars a month.

- Banks and Credit Unions: The institution that financed your car probably offers its own GAP policies, too.

It pays to shop around. If you ever do need to use it, the process is simple: finalize the total loss settlement with your primary insurer first. Then, get in touch with your GAP provider, give them the settlement details, and they’ll take it from there.

Your Action Plan After Totaling a Financed Car

It’s easy to feel overwhelmed in the minutes and hours after a serious car accident. But when your car is financed, the situation gets even more complicated. Having a clear action plan can make a world of difference, giving you a sense of control when you need it most.

Think of the next few steps as a checklist to get you from the side of the road to a fair settlement. The key is to be methodical.

Your Immediate Next Steps

Right after the accident, a few key actions will set the stage for a smoother claims process.

- Secure the scene and file a police report. Your first priority is safety. Once everyone is out of harm's way, call 911. A police report creates an official record of the accident, which is absolutely essential for your insurance claim.

- Notify your insurance company. Call your insurer as soon as you can to get the claim started. They’ll need the basics: what happened, where it happened, and the police report number if you have it.

- Inform your lender. This is a step many people forget. Your lender is a legal stakeholder in your vehicle, so they need to know what’s happened. Give them a call to let them know the car is likely a total loss.

Getting these three things done quickly lays the groundwork for everything else.

Gathering Information and Working with Adjusters

Once the initial calls are made, your focus will shift to working with the insurance adjuster. This is the part where you'll need to be organized and ready to advocate for yourself.

An important piece of the puzzle is understanding the paperwork involved, especially the process of transferring your vehicle title to the insurance company. The insurer can't issue a final payout until they legally own the vehicle's remains.

Start by gathering all your documents—your loan agreement, the vehicle title, and any service records you have. Good maintenance records can sometimes help prove your car was in better-than-average condition, potentially bumping up its value.

When the adjuster gives you a settlement offer, don't just accept it immediately. Review it closely. If the number seems low, you have the right to negotiate. With repair costs soaring and Americans owing over $1.6 trillion in auto loans, getting a fair payout is more important than ever.

Finally, after you’ve settled with your primary insurer, it’s time to file your GAP insurance claim, if you have it. This is the policy that will cover any remaining loan balance. For a deeper dive into the entire process, our guide on https://totallossnw.com/what-to-do-when-car-is-totaled/ walks you through every detail.

Got Questions? Let's Untangle the Total-Loss Process

Even when you know the steps, having your financed car totaled can leave your head spinning with questions. The "what ifs" can be completely overwhelming, but getting straight answers is the best way to get back in the driver's seat, financially speaking.

Let's tackle some of the most common worries people have in this situation.

What if I Owe More Than the Car Is Worth and I Don't Have GAP Insurance?

This is, without a doubt, the most nerve-wracking part of the whole ordeal for many drivers. If the insurance company's payout for your car's Actual Cash Value (ACV) doesn't cover your entire loan balance, you're on the hook for the difference. This leftover amount is called the deficiency balance.

Your lender will need to be paid, one way or another. You generally have a couple of paths forward:

- Pay it off in one go. If you have the savings, writing a check for the remaining balance is the cleanest and fastest way to close the loan for good.

- Work out a payment plan. Most lenders don't want to send you to collections; it's a hassle for them, too. They're often willing to set up a new payment schedule to let you pay off that deficiency balance over a few months or more.

Simply ignoring the debt isn't an option. It will tank your credit score and eventually end up in collections. The most important thing you can do is call your lender right away, explain the situation, and figure out a solution together.

Can I Actually Negotiate the Insurance Payout?

Yes, you absolutely can and probably should. The first number the insurance company gives you is just that—an opening offer. It’s not set in stone, and you have every right to push back if you feel their valuation of your car is too low.

But you can't just say you want more money. You need to build a case.

- Find "Comps": The best evidence is real-world evidence. Look for listings and recent sales of the exact same make, model, and year of your car in your immediate area.

- Show Your Work: Did you just put $1,200 worth of new tires on it? Or replace the transmission last year? Dig up those receipts. Major repairs and upgrades add real value.

- Bring in a Pro: If the insurance company's offer feels way off, hiring an independent appraiser can be a game-changer. A detailed report from a certified professional is hard for an adjuster to ignore.

Remember, the insurance adjuster's job is to close the claim for the company. Your job is to be your own best advocate and make sure their payout reflects what it would have actually cost to buy your car moments before the accident.

How Is My Credit Score Affected by a Totaled Car?

The accident itself doesn't directly hurt your credit. It's all about how the loan is handled after the car is gone.

The biggest risk to your credit is fumbling the loan payoff. If you end up with a deficiency balance and don't make arrangements to pay it, the lender will report those missed payments to the credit bureaus. That's when your score can take a serious hit.

On the flip side, if the insurance money, plus any GAP coverage or your own payment, settles the loan completely, the account is closed and reported as "paid as agreed." This is a neutral or even a slightly positive event for your credit, showing you successfully paid off a debt.

Can I Just Keep the Car and Fix It?

In most states, yes, you have the option to keep your wrecked car. It's often called "owner retention." If you go this route, the insurance company calculates your payout a little differently: they'll give you the car's ACV minus its salvage value.

Think of it this way: the salvage value is the cash the insurer would have gotten for selling your wrecked car for parts at an auction. By keeping the car, you're essentially buying the wreck from them for that price.

But before you do this, you need to know what you're getting into:

- It gets a "Salvage Title." Your state's DMV will permanently brand the car's title as a salvage vehicle, which is a huge red flag for any future buyers.

- Insurance will be a nightmare. Getting full coverage on a car with a salvage title is incredibly difficult and often much more expensive, if you can find it at all.

- Resale value plummets. Even if you restore it to pristine condition, a car with a salvage history is worth a fraction of one with a clean title.

Honestly, this path really only makes sense if the damage is mostly cosmetic, you have the skills and resources to do the repairs cheaply yourself, and you intend to drive that car until the wheels fall off.

Feeling like you're getting a lowball offer on your totaled vehicle? You don't have to take it. At Total Loss Northwest, we provide certified, independent auto appraisals that give you the leverage to get what you're truly owed. We invoke the Appraisal Clause in your policy to make sure you walk away with a fair market value settlement. Don't let them leave money on the table—get the expert appraisal you deserve at Total Loss Northwest.