When your car is in an accident, the big question is always, "Can it be fixed?" But for an insurance company, the real question is, "Does it make sense to fix it?"

A car is usually declared a "total loss" when the cost to repair it surpasses its value right before the crash. It’s a purely financial calculation. Think of it this way: if fixing your cracked phone screen costs almost as much as a brand new phone, you’d just get the new phone, right? Insurance companies apply that same logic to your car.

Understanding When a Car Is Totaled

The word "totaled" often brings to mind a mangled heap of metal, but that's not always the case. A car can look surprisingly okay and still be a total loss. It's not about whether the car can be repaired; it's about whether the repairs are a sound financial decision.

This process ultimately protects both you and the insurer from pouring money into a vehicle that's simply not worth what it costs to fix. To figure this out, an adjuster has to dig into three key numbers that tell the whole story.

The Key Factors in a Total Loss Decision

At its core, the decision comes down to a simple formula: Is the cost to repair the car higher than its pre-accident value? To get to that answer, an adjuster carefully weighs these three factors:

- Repair Costs: This isn't just a ballpark guess. It's a detailed estimate covering every single part, from a new bumper to tiny electronic sensors, plus all the skilled labor hours needed to put your car back together safely.

- Actual Cash Value (ACV): This is the magic number representing what your car was worth just moments before the accident. The adjuster determines the ACV by looking at your car's age, mileage, overall condition, and what similar models have recently sold for in your local market.

- Salvage Value: Even a wrecked car has some value. This is the amount the insurance company can get back by selling the damaged vehicle to a salvage yard, which will then sell off usable parts and scrap the rest.

The economic fallout from car accidents is massive. Road traffic crashes cost most countries around 3% of their gross domestic product (GDP). Modern cars, packed with expensive tech and specialized materials, have only made this worse. A seemingly minor fender-bender can damage sensors and cameras that cost thousands to replace, quickly pushing the repair bill into total-loss territory. For more on the global costs of traffic incidents, the World Health Organization offers some eye-opening data.

Decoding the Total Loss Formula Insurers Use

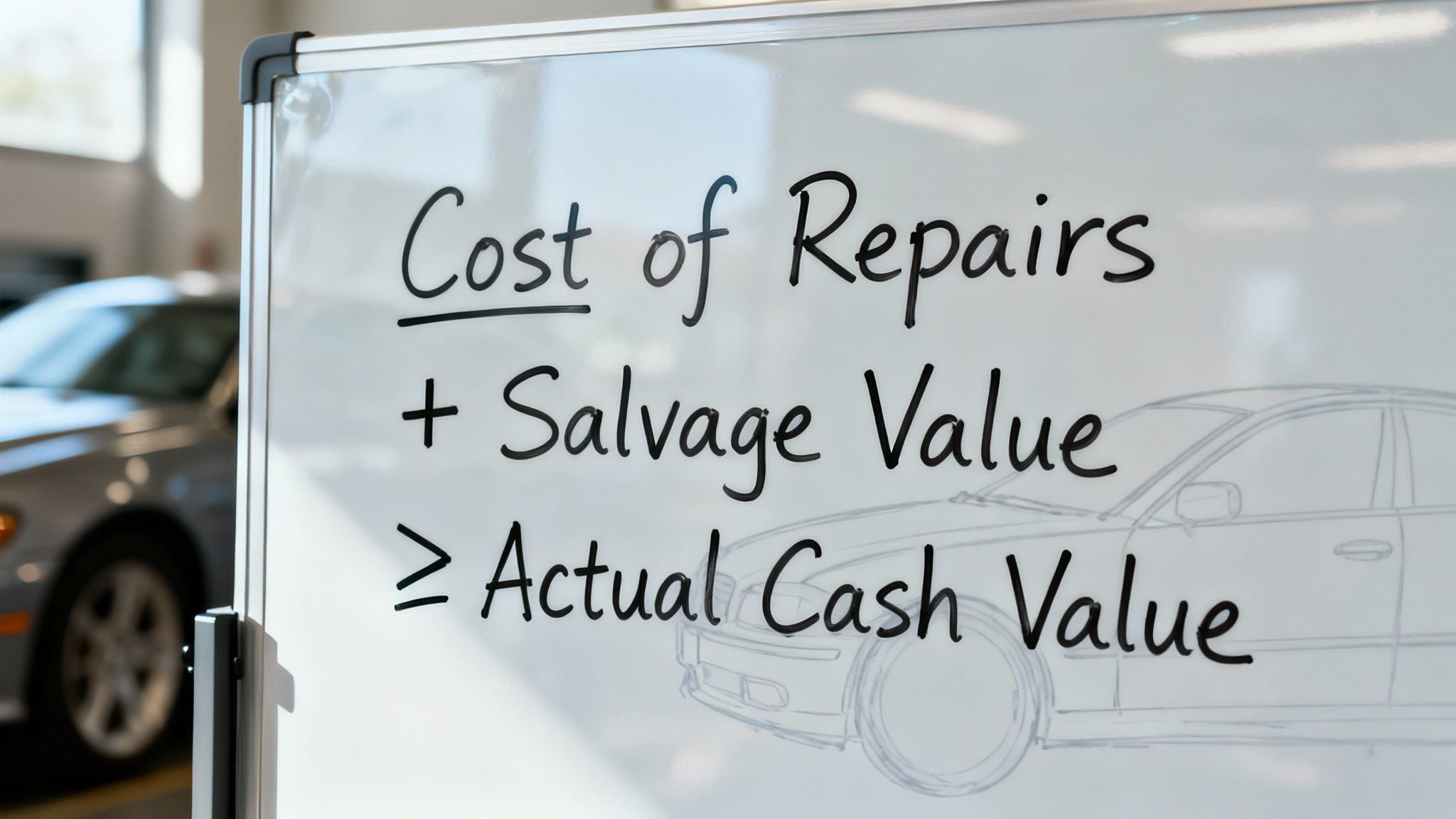

When an insurance company decides whether to repair your car or "total it out," they aren't just making a judgment call. The decision comes down to a specific calculation called the Total Loss Formula (TLF). This is the exact math they use to determine your car's fate.

At its heart, the formula is a simple cost-benefit analysis. A car is considered a total loss if the cost of repairs plus what they can get for the wrecked car (its salvage value) is more than what the car was worth right before the crash.

The Total Loss Formula

Cost of Repairs + Salvage Value ≥ Actual Cash Value (ACV)

If the two numbers on the left are bigger than the number on the right, it’s a financial no-brainer for the insurance company to declare it a total loss.

Breaking Down the Cost of Repairs

The first part of this equation, the Cost of Repairs, is much more than a ballpark estimate. It’s a highly detailed breakdown from a professional adjuster or a body shop.

This figure is meant to cover every single thing required to bring your car back to its safe, pre-accident condition. This includes:

- Parts: Every nut, bolt, sensor, and body panel needed for the job.

- Labor: The estimated hours a qualified technician will spend on the repairs, billed at the shop's specific hourly rate.

- Hidden Damage: Experienced adjusters will often build in a buffer for damage they can't see yet, like a bent frame support hidden behind a crumpled fender.

Getting this number right is the crucial first step in the whole process.

Understanding Salvage and Actual Cash Value

The other two variables in the formula are just as important. Salvage Value is simply the money the insurer can get back by selling your damaged car to a salvage yard for scrap or parts.

Finally, you have the Actual Cash Value (ACV). This is probably the most significant number of all. The ACV is the fair market value of your vehicle the instant before the accident happened. It’s what a reasonable person would have paid for your car, considering its make, model, year, mileage, and overall condition.

Let’s put it all together with a quick example. Say your car had an ACV of $10,000. The body shop quotes the repairs at $8,000, and the insurance company determines it can get $2,500 for the salvage.

Here’s the math: $8,000 (Repairs) + $2,500 (Salvage) = $10,500.

Since that $10,500 total is greater than the car's $10,000 ACV, it’s officially a total loss. The numbers can get a bit more involved in the real world, and you can get a more detailed look by exploring how to go about calculating a total loss vehicle. But at the end of the day, this is the fundamental formula that decides it all.

How Insurers Calculate Your Car's Actual Cash Value

When your car is in a serious accident, the single most important number in your insurance claim is the Actual Cash Value (ACV). Forget what you originally paid for it or what it’s worth to you sentimentally; the ACV is what the insurance company determines your car was worth in the open market the second before the crash happened.

Think of it this way: what could you have reasonably sold your car for in a private sale just before the accident? That number is the ACV, and it becomes the foundation for your entire settlement. Getting a handle on how this figure is calculated is crucial if you want to ensure you're getting a fair shake.

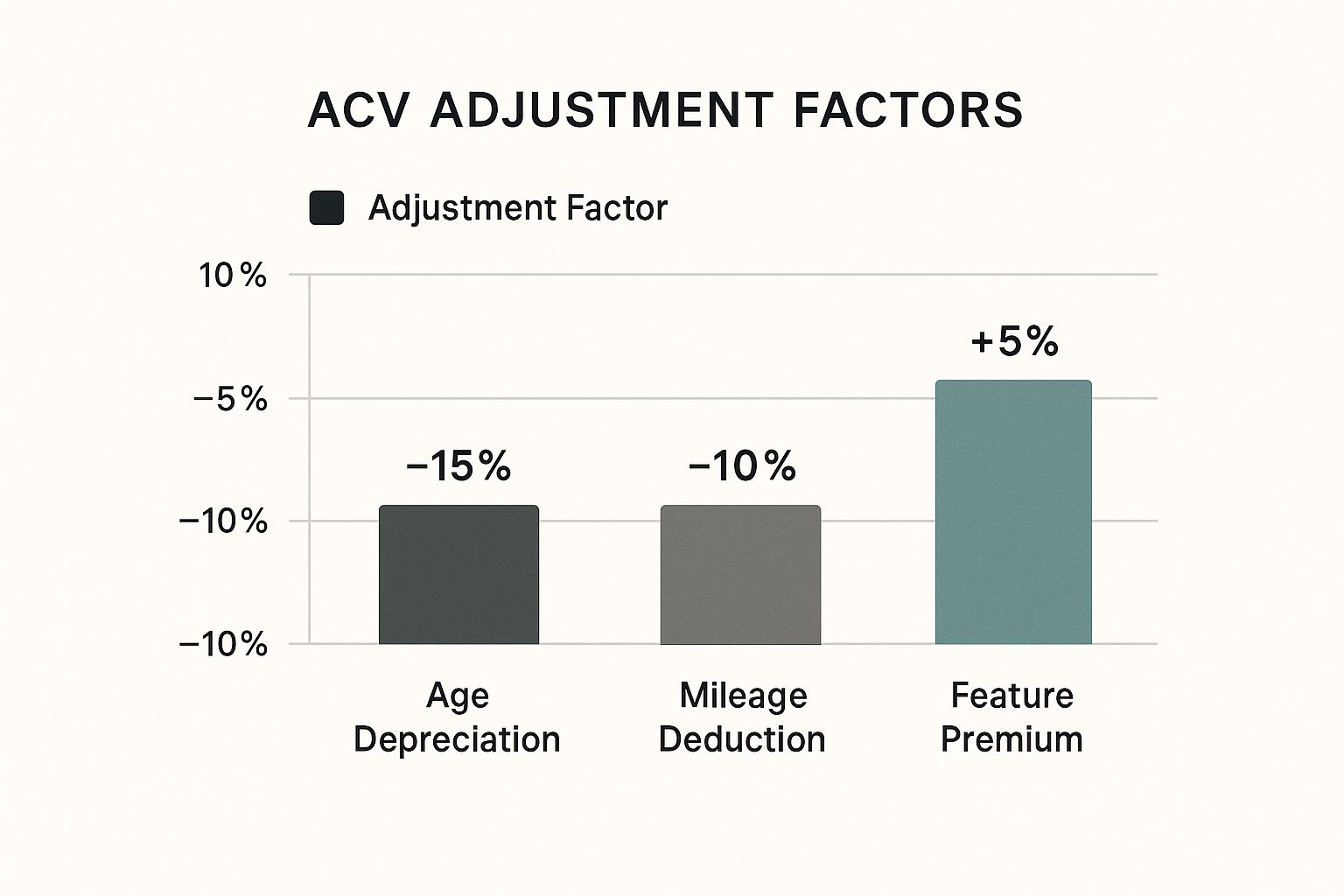

The Core Factors That Determine ACV

Insurance adjusters don’t just pull a number out of a hat. They rely on a pretty structured process, often using data from third-party valuation tools like CCC ONE or Mitchell to get a baseline. While the exact recipe can differ slightly between carriers, they all look at the same core ingredients.

These are the main things that move the needle on your car's ACV:

- Age and Mileage: No surprise here—this is the big one. As cars get older and rack up more miles, their value goes down. A five-year-old car with 50,000 miles is naturally going to be worth a lot more than the same model with 150,000 miles.

- Trim Level and Options: Was your car a base model or the fully loaded version? A sunroof, a premium sound system, or advanced safety features all add to its value and will push the ACV higher.

- Overall Condition: The adjuster will assess the car's pre-accident condition. This includes the state of the interior, the quality of the paint, and even the tread on the tires. A well-kept car with no prior dings or scratches will always be valued higher.

- Local Market Data: Where you live matters. Your car's value is benchmarked against recent sales of similar vehicles in your area. That popular pickup truck might hold its value incredibly well in a rural state but less so in a dense city.

This infographic breaks down how these different factors can adjust a vehicle's starting value.

As you can see, negative adjustments from things like high mileage or wear and tear often have a much bigger impact than the positive adjustments from fancy features.

How You Can Defend Your Car’s Value

The first ACV figure the insurance company gives you is just an initial offer, not the final word. You absolutely can, and often should, negotiate it—especially if you have proof to back up a higher value. Your job is to build a case that shows them what your car was really worth.

The key to a successful negotiation is documentation. Without proof, it's just your opinion against the insurer's data. Collect service records, receipts for new tires or upgrades, and clear photos showing the car’s excellent condition before the crash.

You need to demonstrate that your vehicle was in better-than-average shape for its age. To get more specific on this, you can learn more about what the actual cash value of your car really means in the eyes of an insurer. Doing your homework here is critical, because a higher ACV could be the difference between getting your car repaired and having it declared a total loss.

Understanding State Laws and Total Loss Thresholds

So, you might think your insurance company has the final word on totaling your car. While they run the numbers, they don't get to make the call in a vacuum. The decision is actually anchored in state law.

Every state has its own set of rules to create a clear, consistent standard for when a vehicle is just too damaged to safely hit the road again.

What Is a Total Loss Threshold?

This is where the Total Loss Threshold (TLT) comes in. Think of the TLT as a legal line in the sand drawn by your state's DMV. It's a specific percentage, and if the estimated cost of repairs blows past that percentage of your car's Actual Cash Value (ACV), the insurer is legally obligated to declare it a total loss.

Let's break it down. Say your state has a TLT of 75%. If your car is worth $20,000, that line in the sand is drawn at $15,000. If the body shop comes back with a repair estimate of $15,001, the law steps in and says that car is officially totaled.

This isn't just about saving money on a complex repair job; it's a critical public safety measure. The whole point is to stop dangerously compromised vehicles from being patched up and put back on the street just because it was cheaper for the insurance company. By setting a firm threshold, states make sure severely wrecked cars are taken out of circulation for good.

How Thresholds Vary By State

Here's the tricky part: the TLT is not a one-size-fits-all number. It can vary wildly from one state to another, which means the same amount of damage might get your car totaled in one state but repaired in another.

Some states stick to a strict percentage. Others use the "Total Loss Formula" (TLF), where the math is a bit different: Cost of Repairs + Salvage Value ≥ ACV.

Let’s look at a few examples:

- Strict Percentage States: Places like Colorado (100%), Florida (80%), and New York (75%) use a hard-and-fast percentage. Cross that number, and it’s a done deal.

- Total Loss Formula (TLF) States: States like Arizona, Washington, and Maine go with the TLF. They add up the repairs and what the car's junked parts are worth to see if it makes more sense to just pay you out.

Here is a table that gives you a better sense of how different states handle this.

Sample State Total Loss Thresholds (TLT)

This table shows how the percentage of damage required to total a car varies by state. Note: Always check your state's current regulations.

| State | Total Loss Threshold (%) | Regulation Type |

|---|---|---|

| Colorado | 100% | Fixed Percentage |

| Florida | 80% | Fixed Percentage |

| Georgia | 75% | Fixed Percentage |

| Illinois | 70% | Total Loss Formula (TLF) |

| Iowa | 70% | Fixed Percentage |

| New York | 75% | Fixed Percentage |

| Ohio | 60% | Fixed Percentage |

| Texas | 100% | Fixed Percentage |

| Washington | N/A | Total Loss Formula (TLF) |

As you can see, the differences are significant.

A car with 70% damage-to-value might be sent to the body shop in Texas (a 100% threshold state), but it would be an automatic total loss in Ohio, where the threshold is just 60%.

Knowing your local TLT is a huge advantage. It gives you a clear, legal benchmark for your claim, helping you understand your rights and know what to expect from the insurance adjuster. It’s the key to making sure you get a fair and lawful outcome.

What to Expect After Your Car Is Totaled

https://www.youtube.com/embed/-jRYaaxLJnU

Getting the news that your car is a total loss can feel like a punch to the gut. It's stressful, but knowing what comes next can make the whole process a lot more manageable. Once the insurance company officially declares your car totaled, they'll kick things off by sending you a settlement offer based on your car's Actual Cash Value (ACV).

Think of the ACV as what your car was worth just moments before the crash. This number is the foundation for everything, so your first move is to scrutinize their valuation report. Don't just take their first offer at face value. Look closely at the "comps" (comparable vehicles) they used to land on that number and make sure they're a fair match. If the offer feels low, you absolutely have the right to push back.

Navigating the Settlement Process

To successfully negotiate, you need to come prepared. Your job is to build a case showing your car was worth more than the insurer is offering. This isn't about emotion; it's about evidence.

Here's the kind of proof that can make a real difference:

- Maintenance Records: A full service history shows your car was in top shape.

- Receipts for Upgrades: Recently bought a set of $1,200 tires or installed a new stereo? Show them the receipts.

- Pre-Accident Photos: A picture is worth a thousand words, especially if it shows a clean, well-maintained vehicle.

By presenting solid documentation, you're not just asking for more money—you're proving why you deserve it.

Your settlement check is meant to cover the value of the car you lost. But remember, the final amount that hits your bank account can be affected by things like an outstanding car loan.

Speaking of loans, this is where another layer comes into play. If you're still paying off your car, the insurance company will pay your lender first. For instance, if your car's ACV is $15,000 and you owe $12,000 on your loan, the lender gets their $12,000, and the remaining $3,000 goes to you.

Handling Car Loans and Gap Insurance

But what happens if you owe more than the car is worth? This is a common situation called being "upside-down" or having negative equity, and it's where Gap Insurance can be a lifesaver.

Let's say your settlement is $15,000, but you still owe $18,000 on the loan. Without gap coverage, you'd be on the hook for that $3,000 difference—all for a car you can't even drive anymore. Gap insurance is designed specifically to cover that "gap."

Finally, you might have the option to keep your wrecked car, a process called "owner retention." If you go this route, the insurance company pays you the ACV minus the car's salvage value (what they could get for it at auction). Just know that the car will get a "salvage" title, which makes it much harder to insure and sell down the road.

To dig deeper into these choices, our guide on what to do when your car is totaled can walk you through every step to help you decide what's best for you.

Real World Examples of a Total Loss

The formulas and thresholds are great on paper, but how does this all work in the real world? Let’s walk through a few common situations to see exactly how an insurance adjuster makes the call.

Seeing these concepts in action makes the whole process much easier to understand.

Scenario 1: The Older, Reliable Sedan

Let's start with a car many of us drive: a 10-year-old sedan that’s been a trusty daily driver. Its Actual Cash Value (ACV) is sitting at around $7,000.

After a moderate front-end collision, the bumper, hood, and radiator are smashed. The repair shop quotes $5,500 to fix it all. At first glance, $5,500 is less than the car's $7,000 value, so it seems repairable, right?

Not so fast. If this accident happened in a state with a 75% Total Loss Threshold, the math changes. The threshold for totaling this car would be $5,250 ($7,000 x 0.75). Since the $5,500 repair bill is higher than that threshold, the insurance company has to declare it a total loss, even though the repair cost is technically less than the car's full value.

Scenario 2: The Newer SUV With Hidden Damage

Now, picture a three-year-old SUV with an ACV of $30,000. It gets T-boned, deploying the side curtain airbags and damaging the door. The visible damage doesn’t look catastrophic, but an experienced adjuster knows the real costs are often hidden from view.

Here’s where modern vehicle complexity comes into play. The adjuster’s estimate starts adding up quickly:

- Airbag Replacement: $4,000

- Body and Paint Work: $6,500

- Frame Straightening: $5,000

- Sensor Recalibration: $1,500

Today's cars are packed with sophisticated safety systems, and a collision can easily require expensive ADAS calibration services to get everything working safely again. The total repair estimate balloons to $17,000. Even in a state that uses a flexible Total Loss Formula instead of a strict percentage, this high cost makes the repair a poor financial decision for the insurer.

Scenario 3: The Flood-Damaged Vehicle

Finally, consider a car that was caught in a flash flood. After the water recedes and the car is cleaned up, it might look almost perfect on the outside. But water is the silent killer of modern vehicles.

Water damage often results in an automatic total loss. The risk of future corrosion, mold, and complete electronic failure is so high that insurers rarely consider repairs a viable or safe option.

The engine might even start, but water gets into everything—wiring harnesses, computer modules, sensors, and the engine itself. The potential for long-term, catastrophic failures is almost guaranteed. The cost to gut and replace all the compromised electronics and mechanical parts will almost certainly soar past the car's ACV, making it a clear-cut total loss every time. It’s a stark reminder that the most destructive damage isn't always the most visible.

Common Questions After a Total Loss

When your car is declared a total loss, your mind probably starts racing with questions. It's a confusing, stressful situation, and it’s easy to feel overwhelmed. Let's walk through some of the most common concerns people have so you can feel more in control.

First off, what about all your stuff that was in the car? Don't worry, you absolutely get to retrieve your personal belongings. Just get in touch with the body shop or salvage yard holding your vehicle to set up a time to collect everything.

What to Expect From the Settlement Process

One of the biggest questions is always about the money. You do not have to accept the insurance company’s first settlement offer. Think of it as their opening bid. If you have solid evidence showing your car was worth more—like recent upgrades or comparable sales listings—you can absolutely negotiate for a higher amount.

People also want to know how long this whole ordeal will take. For a straightforward claim, you might have everything wrapped up in a couple of weeks. But if you end up in a back-and-forth negotiation over the car's value or if there are hitches with your auto loan, the process can easily stretch to a month or more.

Keep in mind, the settlement check is for the vehicle's Actual Cash Value (ACV), minus your deductible. This is what your specific car was worth right before the crash, not what it will cost to buy a brand-new replacement.

And what about the license plates? This varies by state, but generally, you'll need to remove the plates from the car. You'll then turn them in to the DMV before you officially cancel the insurance policy on that vehicle, which gets it out of your name for good. Handling these details helps the entire process go much more smoothly.

If you're in Oregon or Washington and feel the insurance company is lowballing you, don't just accept it. Total Loss Northwest provides certified independent appraisals to make sure you get paid what your car was actually worth. We invoke the Appraisal Clause in your policy to secure a fair settlement based on real market data. Visit us at https://totallossnw.com to learn how to fight for your vehicle's true value.