When it comes to your car's value in an insurance claim, the most important term you'll hear is Actual Cash Value (ACV). It's a common point of confusion, so let's clear it up: ACV is not what you originally paid for your car. Think of it as the real-world market price your vehicle was worth the moment before an accident, accounting for its age, mileage, and overall condition.

What Actual Cash Value Means for Your Car

Let's cut through the insurance jargon with a simple analogy. Imagine you're selling a three-year-old smartphone. You wouldn't expect to get the full price you paid when it was brand new, right? Its current value would depend on the model, its condition, and what similar used phones are selling for. That's exactly how Actual Cash Value works for your car.

Insurance companies use ACV as the standard yardstick to figure out the payout for a vehicle that’s been declared a total loss. This number is their calculation of what it would cost to buy a comparable used car today.

The Elephant in the Room: Depreciation

Depreciation is the natural, unavoidable drop in your car's value over time. Every mile you drive and every year that passes contributes to this decline through simple wear and tear. It’s the single biggest reason why your car's ACV is almost always lower than its original sticker price.

This concept is central to how insurance works.

The core idea behind an ACV payout is to restore you to the financial position you were in right before the accident—not to hand you the keys to a brand-new vehicle.

The speed of depreciation can be shocking. Industry data often shows a vehicle's value can plummet by 15-20% in the first year alone. Fast forward five years, and that same car might only be worth 40% of what you initially paid.

Getting a handle on this principle is the first step toward figuring out how much your totaled car is worth. Your insurer will dig into several key factors to calculate the final ACV, which becomes the starting point for your settlement offer.

ACV vs. Replacement Cost vs. Agreed Value

It's easy to get these terms mixed up, but they mean very different things for your wallet. Here’s a quick breakdown to see where ACV fits in.

| Valuation Method | What It Covers | Best For |

|---|---|---|

| Actual Cash Value (ACV) | The market value of your car right before the loss, minus depreciation. | Standard on most auto policies; the most common type of coverage. |

| Replacement Cost | The cost to buy a brand-new car of the same make and model, with no deduction for depreciation. | Owners of new cars who want to be fully covered for a new replacement. |

| Agreed Value | A specific value for the car that you and the insurer agree upon when you buy the policy. | Owners of classic, custom, or high-value vehicles where market value is hard to determine. |

While Replacement Cost and Agreed Value policies offer more complete protection, they also come with higher premiums. For most drivers, ACV is the standard, making it crucial to understand how that number is calculated.

How Insurance Companies Calculate ACV

When an insurance company tells you what your totaled car is worth, the number can feel like it was pulled out of thin air. In reality, figuring out a vehicle's actual cash value isn't magic—it's a specific, multi-step process. Think of it like a recipe, where each ingredient affects the final outcome.

The adjuster starts by establishing a baseline price. This initial number comes from the most basic facts about your car: its make, model, year, and mileage. This is just the starting point, the foundation upon which the final valuation is built.

Peeling Back the Layers of Valuation

With the baseline set, the real work begins. The adjuster starts to factor in the specifics that made your car your car. This is where the little things can make a big difference. For instance, a higher trim level (like a fully-loaded Ford F-150 Lariat versus a base XL model) or factory options like a sunroof and a premium stereo system will add value.

Next, they take a hard look at your vehicle's pre-accident condition. This is a critical step.

An insurance adjuster’s job is to determine what your exact vehicle was worth one second before the impact. This means they account for everything from pristine paint to existing scratches, dents, or worn tires.

Recent upgrades can also boost the value, but only if you have the paperwork to prove it. A brand-new set of tires or a recently replaced engine can certainly help your case, but you’ll need to show the receipts. From the insurer's perspective, if there's no documentation, the upgrade never happened.

The Tools and Data Behind the Offer

Insurers don't just pull these numbers from a hat. They rely on powerful, data-driven valuation services to generate their settlement offers. The two industry giants you'll almost always encounter are CCC ONE (CCC Intelligent Solutions) and Mitchell. These platforms analyze massive amounts of market data to create a detailed report.

Here’s a peek at what these valuation reports look at:

- Comparable Vehicles: The software scours your local area for recently sold cars of the same make, model, and year. These are called "comps."

- Condition Adjustments: It then adjusts the value of those comps up or down to match your vehicle’s specific condition, mileage, and features.

- Local Market Data: Geography plays a huge role. A 4×4 truck, for example, is naturally worth more in a snowy mountain town than in a sunny coastal city because local demand is higher.

Getting familiar with this process is the first step toward making sure you're treated fairly. If you and the insurance company are at a standstill over the valuation, it's worth reading your guide to the appraisal clause in auto insurance. This clause is your right to bring in a neutral expert to help settle the dispute.

Why Your Insurer's Valuation Can Be Too Low

It’s a moment most drivers dread. You get the call or email about your totaled car, look at the settlement offer, and your heart sinks. That number is almost always lower—sometimes much lower—than you were expecting.

It’s a frustrating experience, but don’t panic. That first offer is just that: an offer. It’s a starting point for a conversation, and understanding why it’s so low is your first step toward getting the fair value you deserve.

The problem usually isn’t malice; it’s the data. Insurance companies lean heavily on automated valuation reports, and while these systems are fast, they’re far from flawless. They often miss the very details that make your car unique, which is where you have the power to step in and correct the record.

Spotting Common Errors in Valuation Reports

So where do these reports go wrong? An inaccurate valuation usually comes down to a few common culprits.

-

Bad "Comps": The most frequent mistake is using the wrong "comparable" vehicles. The system might pull data for a base model when you drove the fully-loaded, top-tier trim package. That’s a huge difference in value right there.

-

Missed Upgrades: Did you just put a new set of premium tires on the car last month? Or maybe you had significant engine work done? The software doesn't know about those investments unless you prove it. Without receipts and documentation, that value simply vanishes from the actual cash value for my car.

-

Unfair Condition Adjustments: Another area to watch is "condition adjustments." An adjuster might knock your car’s condition from "good" down to "fair" because of a few minor, pre-accident scratches, which can disproportionately tank the value.

These systems can also struggle to keep up with major market shifts. For example, the huge 29% year-over-year jump in EV sales in Q1 2025 is shaking up the entire used car market. You can read more about global automotive trends and see how these complex forces can create blind spots in a valuation report.

Key Takeaway: Think of the insurer's valuation as a rough draft, not the final story. It’s built on data that is often incomplete or just plain wrong, giving you the perfect opportunity to present your own evidence and argue for a better number.

By carefully combing through their report, you can spot these errors and build a powerful counter-argument. The key is to shift from being a passive victim of the process to an active advocate for your car's true worth.

How to Dispute a Low ACV Offer

Getting a low settlement offer from your insurance company can feel like a punch to the gut, but it's important to remember this is almost never the final word. That first number isn't a decision; it's an opening bid in a negotiation.

The key to turning the tables is solid, undeniable evidence. By systematically building a case for your vehicle's true worth, you can challenge their valuation with confidence and fight for the fair actual cash value you’re entitled to.

Your First Move: Demand Their Report

Before you do anything else, you need to understand exactly how the insurer landed on their number. You have every right to see their homework. Formally request a complete copy of their valuation report.

This document is your roadmap. It will show you which comparable vehicles (comps) they used and what adjustments they made for your car's mileage, features, and overall condition. Pour over it with a fine-tooth comb—this is where you’ll almost always find the mistakes and unfair assumptions that led to the lowball offer.

Building Your Counter-Argument

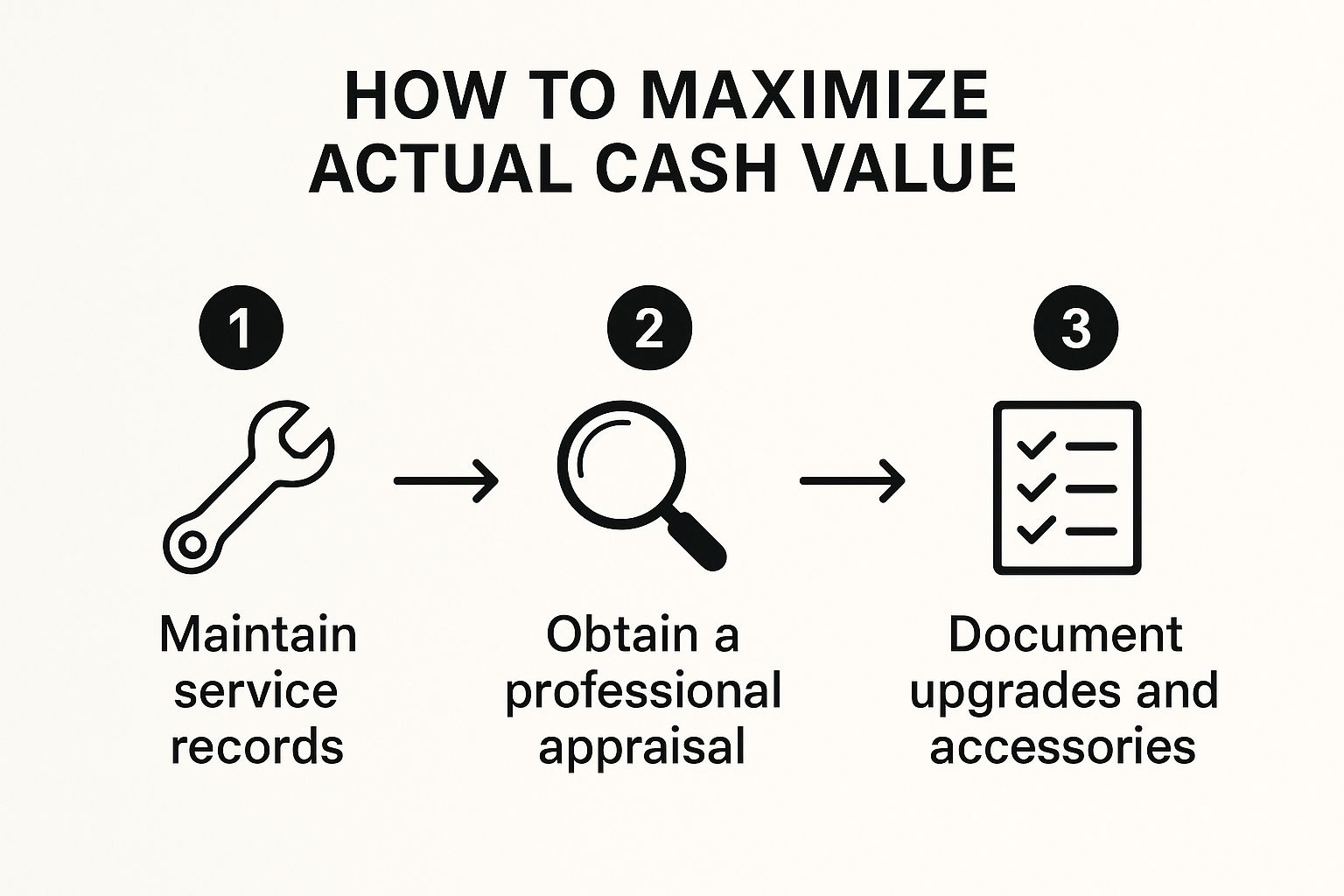

Once you have their report, it’s time to build your own. Your mission is to assemble a file of proof that paints an accurate picture of your car's real pre-accident value. Think of yourself as an appraiser proving your case.

This is all about documentation. A strong evidence file can make all the difference.

- Service and Maintenance Records: A complete service history is gold. It directly refutes any vague claims of "poor condition" and proves you took excellent care of your vehicle.

- Receipts for Recent Upgrades: Did you just put on a set of $1,200 tires? Replace the brakes? Install a better sound system? Every receipt adds documented value that their standard valuation software almost certainly overlooked.

- Pre-Accident Photos: A picture is worth a thousand words, especially when it shows your car looking sharp and clean. This is powerful visual proof to counter any subjective "condition adjustments" they might have tacked on.

Next, you need to find your own comps. Search for vehicles currently for sale at local dealerships—not private party listings on Craigslist. You're looking for the same make, model, year, and trim level. Print these dealer listings out. They are direct, real-world proof of what it would actually cost to replace your car in your local market today.

To stay organized, use a simple checklist to gather everything you need.

Your Evidence Checklist for an ACV Dispute

Here’s a practical list of the documents you should gather to build a strong, fact-based counter-offer. Having these items organized will make your communication with the adjuster much more effective.

| Document Type | Why It's Important | Where to Find It |

|---|---|---|

| Insurer's Valuation Report | Shows their methodology and is the basis for your dispute. | Request directly from the claims adjuster. |

| Full Maintenance History | Proves the vehicle was well-cared-for, countering condition penalties. | Your mechanic, dealership service department, or personal files. |

| Receipts for Upgrades/Repairs | Documents recent investments that add value (tires, brakes, stereo, etc.). | Personal records, credit card statements, or repair shop invoices. |

| Pre-Accident Photos | Provides visual evidence of the vehicle's excellent condition. | Your phone's camera roll, social media, or family photos. |

| Local Dealer "Comps" | Establishes the true local market replacement cost. | Dealership websites, AutoTrader, Cars.com (filter for local dealers). |

| Original Window Sticker | Lists all factory-installed options and packages that add value. | With your original purchase documents or sometimes available online by VIN. |

Once you have these documents in hand, you have a powerful case that is based on facts, not feelings.

Crafting and Submitting Your Counter-Offer

With your evidence organized, you're ready to make your move. Draft a professional but firm letter or email. Don’t just say, "I want more money." You need to show them why your vehicle is worth more, using the proof you've gathered.

This entire process highlights why good record-keeping is so valuable, even before an accident happens.

As this shows, consistent maintenance and clear documentation are the bedrock of proving your car's true value. Lay out your comps, receipts, and service records clearly. Point to the specific errors in their report and provide the evidence that corrects them.

For a deeper dive into negotiation tactics and sample letters, check out our complete guide on how to challenge a low total loss offer. When you negotiate from a position of strength, armed with facts, your chances of reaching a fair settlement increase dramatically.

Sometimes, no matter how much solid proof you have, the insurance company just won't play fair. You've sent the comps, you've made the calls, but they're still not budging. This is when bringing in a professional can completely turn the tables.

Knowing when to escalate the fight is crucial. While both public adjusters and attorneys can help you get a fair actual cash value for your car, they each have their own strengths. Let's break down when it makes sense to tag in an expert.

When Professional Help Is a Smart Investment

Look, you don't need to hire someone for every little disagreement. But when the stakes are high or the claim gets complicated, it’s time to consider calling for backup. Think of it as leveling the playing field against a massive insurance carrier with a whole team of experts on their side.

So, when is it time to make that call?

- High-Value or Unique Vehicles: Is your totaled car a classic, a heavily modified ride, or a rare exotic? The standard valuation tools the insurer uses are practically useless for these. An expert brings in specialized knowledge to prove its true worth.

- The Insurer Is Unresponsive: If the adjuster is ghosting you, brushing off your evidence, or dragging their feet, that's a huge red flag. This isn't just poor service; it's a tactic.

- The Offer Is Egregiously Low: You've done your homework and know your car is worth thousands more than their offer, but they refuse to move. An expert can break through that stalemate.

As a rule of thumb, if the insurer’s first offer is less than 70-80% of what your research shows the car is worth, they’re probably not negotiating in good faith. It’s a sign they’re just testing to see if you’ll roll over.

Bringing in a pro means they take over the entire negotiation. They know the insurance company's playbook and can counter their tactics effectively, which takes a massive amount of stress off your shoulders.

Don't worry about the cost, either. Most public adjusters and auto claim attorneys work on a contingency fee basis. In plain English, that means they don’t get paid unless they win you more money. Their fee is just a percentage of the extra cash they recover, so you have nothing to lose and a fair settlement to gain.

Answering Your Top ACV Questions

Even after you get the hang of how ACV works, the real-world situations can get a little messy. It's totally normal to have questions when you're suddenly facing a total loss. Let's walk through some of the most common scenarios you're likely to encounter.

What Happens If I Still Owe Money on My Car?

This is probably the most stressful question for anyone with an auto loan. When the insurance company cuts the settlement check, it doesn't come to you. It goes straight to your lender to pay off what you owe.

The real trouble starts when the actual cash value of your car is less than your remaining loan balance. Imagine the insurance company values your car at $15,000, but you still owe $17,000. That $2,000 gap doesn't just disappear—you're on the hook for it. This is precisely the situation where gap insurance can be a financial lifesaver, as its entire purpose is to cover that shortfall.

Can I Keep My Car If It Is a Total Loss?

Surprisingly, yes. In many states, you can choose to keep your vehicle even after it's been declared a total loss. This is often called "retaining salvage," but it comes with a few major catches.

If you decide to keep your totaled car, the insurer will first figure out its salvage value—what the wreck is worth for its parts or as scrap metal. They then deduct that amount from your final ACV settlement check.

On top of getting less cash, your car will be issued a salvage title. This permanently brands the vehicle, slashing its future resale value and making it incredibly difficult to insure or sell down the road.

Is ACV Different for Classic or Modified Cars?

Absolutely, and this is where many enthusiasts get burned. A standard auto policy is designed for everyday commuter cars. It's just not equipped to recognize the true value of unique vehicles.

A typical ACV calculation will completely overlook the thousands of dollars you poured into custom modifications or the premium value of a meticulously maintained classic car. It sees a 20-year-old car, not a collector's item.

For these special cases, you need a different kind of policy:

- Agreed Value: This is the gold standard. You and the insurance company agree on the car's exact worth before the policy even starts. If it's totaled, that's the amount you get, period.

- Stated Value: This option is trickier. You "state" what you believe the car is worth, but the insurer reserves the right to pay the lower of either your stated value or their calculated ACV.

If you own a classic or heavily modified ride, an agreed value policy is the only real way to protect your passion and your investment.

Trying to navigate a total loss claim can feel like an uphill battle, especially when the insurance company’s offer seems completely out of touch with reality. At Total Loss Northwest, we live and breathe this stuff. We're certified appraisers who specialize in invoking the Appraisal Clause to force a fair valuation based on real-world data, not the insurer's biased software. If you've been handed a lowball offer, don't just accept it. Learn how we fight for the settlement you actually deserve.