When you hear an insurance adjuster talk about “actual cash value,” they're really just talking about a simple formula they use to figure out what your property was worth the second before it was damaged.

The core idea is this: ACV = Replacement Cost – Depreciation.

Think of it as the real-world, fair market price for your used item—be it a car, a laptop, or even the roof on your house. It’s not about what it would cost to buy a brand-new one.

What the Actual Cash Value Formula Really Means

Let's cut through the jargon. When you file a claim, the insurance company's job is to "make you whole" again. This means they aim to pay you what your property was actually worth right before the incident, not what a shiny new replacement would cost (unless you have a specific policy for that).

It’s all about fairness. If your three-year-old car is totaled in an accident, you wouldn't get a check for a brand-new 2024 model. Instead, you'd get a payout that reflects its age, mileage, and condition. That’s actual cash value in a nutshell, and it all boils down to two key variables.

The Two Pillars of ACV

To really get a handle on your potential insurance payout, you need to understand the two main ingredients in the ACV recipe. They work together to produce that final number on your settlement check.

- Replacement Cost (RC): This is the starting point. It’s the full price to buy a new, comparable item on today's market. Critically, this isn't what you paid for your item years ago—it's what it would cost to replace it right now, often including taxes and fees.

- Depreciation: Here's the big one. This is the value your property lost over time. Every year, every mile, every scuff mark contributes to depreciation. It’s the natural result of age, wear and tear, and simply becoming outdated.

Key Takeaway: The actual cash value formula is designed to compensate you for the life left in your property, not to give you a free upgrade to something brand-new.

To make this crystal clear, let's break down these terms in a simple table.

ACV Formula Components at a Glance

This table shows how each part of the formula contributes to the final value.

| Term | What It Means | Example |

|---|---|---|

| Replacement Cost (RC) | The cost to buy a brand-new, similar item today. | A new laptop of the same model costs $1,200. |

| Depreciation | The value lost due to age, use, and wear. | Your 3-year-old laptop has lost $500 in value. |

| Actual Cash Value (ACV) | The item's market value right before the loss. | $1,200 (RC) – $500 (Depreciation) = $700 (ACV) |

Understanding this basic math is the first step to confidently navigating your insurance claim.

The distinction between ACV and replacement cost coverage is a fundamental concept in insurance. As Bankrate.com explains, a standard ACV policy pays out the depreciated value, while replacement cost coverage pays the full amount for a new item but almost always comes with higher premiums. Getting these terms straight puts you in a much better position during claim negotiations.

How Insurers Determine Replacement Cost

Before an insurance company can figure out your final payout using the actual cash value formula, they need a starting point. This figure is called the Replacement Cost (RC), and it's simply what it would cost to buy a brand-new, similar item on the open market today.

But it’s not just a quick search for a price tag. Think of it as the total, all-in cost to get you back to where you were before the loss. It’s a comprehensive number.

What Is Included in Replacement Cost

To nail down the RC, your insurer has to research what it would take to purchase an equivalent item right now. This isn't just about the item itself; the calculation usually bundles in a few other things:

- The base price of a "like kind and quality" item.

- Any sales tax that applies in your state or city.

- Typical fees for shipping and delivery.

- The cost for any necessary installation or setup.

Let’s say a premium, built-in dishwasher in your kitchen gets zapped during a power surge. The replacement cost isn't just the price of a new dishwasher on the showroom floor. It has to include the delivery charge and the fee for a professional to come out and properly install it. All those little costs are part of the true RC.

Crucial Point: Replacement cost is all about today's price, not what you paid for the item years ago. Thanks to inflation and market shifts, the RC could easily be much higher than your original purchase price.

How Adjusters Find the Right Number

Insurance adjusters don’t just pull this number out of thin air. They have a process for calculating a fair and accurate replacement cost before they even think about depreciation.

Often, they’ll get quotes straight from local stores or contractors. They also lean on specialized internal databases and industry pricing guides that track the current costs for everything from roofing shingles to laptops. This data-first approach ensures the starting point for your claim is grounded in reality, setting an accurate baseline for the rest of the actual cash value formula.

Decoding the Math Behind Depreciation

Let's be honest: depreciation is almost always the most debated part of the actual cash value formula. It’s the number that can make a settlement offer feel personal and subjective. But it isn't just a random percentage an adjuster pulls out of thin air. It’s a calculated loss in your property's value, and it's based on some very real factors.

Think of it this way: depreciation is the adjuster's attempt to measure how much "life" your car, or any other property, has already used up. Their job is to put a number on that wear and tear based on real evidence, not just a gut feeling.

The Core Factors of Depreciation

When an insurance adjuster figures out depreciation, they’re looking beyond just the age of your car. It’s a bit more nuanced than that. Three key elements come together to paint the full picture of how much value has been lost.

- Age: This one's the most obvious. All things being equal, an older item has had more time to lose value.

- Condition: Here's where the details really make a difference. A five-year-old car that’s been garage-kept with perfect service records is in a completely different league than another five-year-old car that has rust, dings, and a questionable maintenance history. The first has far less depreciation.

- Obsolescence: This is about how outdated something has become. A top-of-the-line car stereo from 2005 might still sound great, but it has lost a ton of value simply because it doesn't have Bluetooth, Apple CarPlay, or other features we now consider standard.

Important Insight: Depreciation isn't a one-size-fits-all penalty. The specific, real-world condition of your car before the accident is what should drive this calculation, not just a chart on a clipboard.

Expected Useful Life

To bring some consistency to these calculations, insurers often lean on a concept called "expected useful life." It's a standard estimate of how long a certain item is supposed to last under normal conditions.

This makes the most sense with parts that wear out predictably, like tires. For example, a quality set of all-season tires might have an expected useful life of 50,000 miles. If your tires had 25,000 miles on them when the accident happened, the adjuster will reasonably argue they've used up 50% of their value—no matter if they were one year old or three.

Knowing that depreciation is tied to a measurable lifespan puts you in a much stronger position to negotiate. You can have a productive conversation with the adjuster about the actual condition and remaining life of your property. This helps ensure the final number in the actual cash value formula is a fair reflection of what your property was truly worth a moment before the loss.

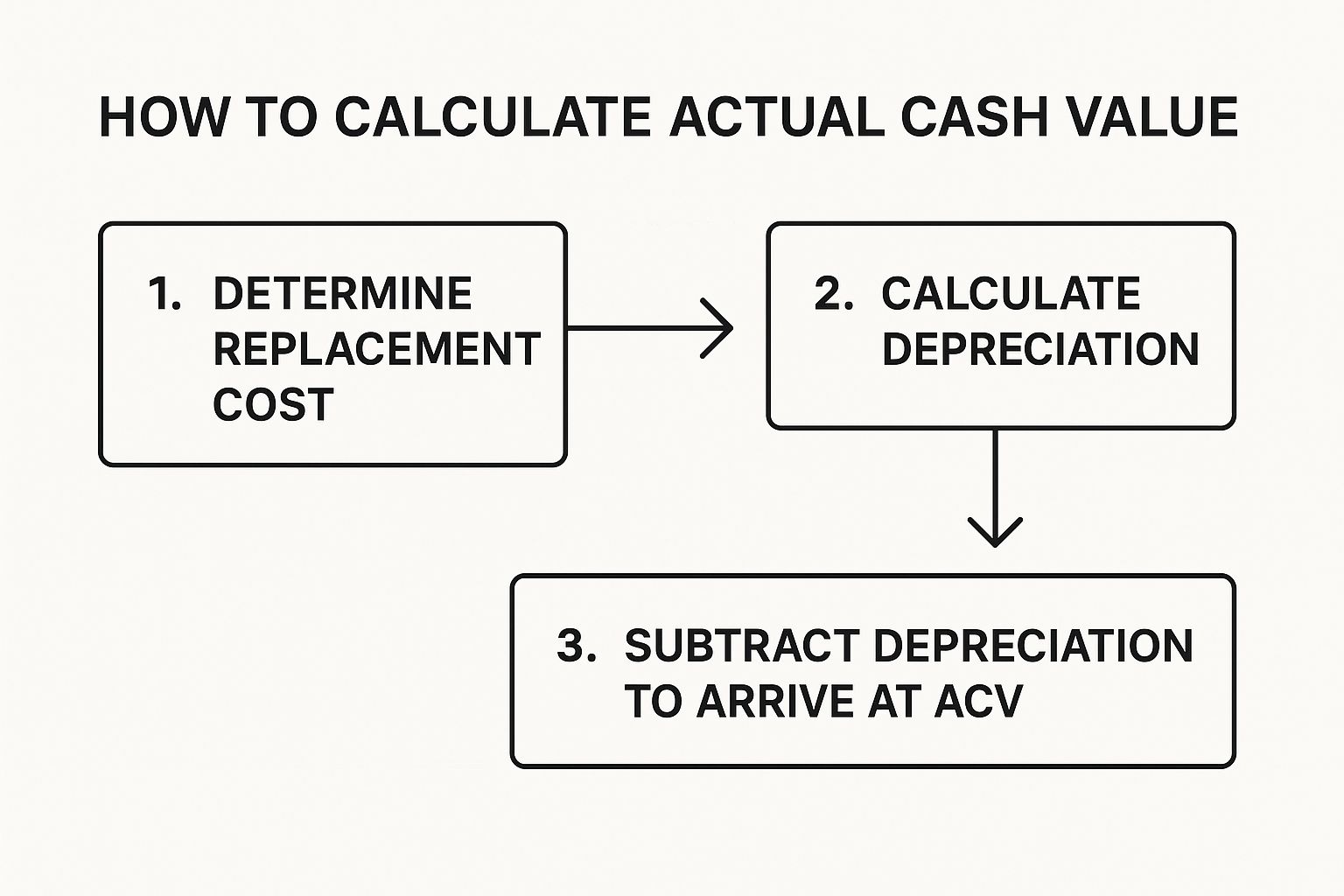

See the ACV Formula Work in a Car Insurance Claim

Theory is one thing, but seeing the actual cash value formula applied in the real world makes it all click. Let's walk through the most common situation where you’ll encounter ACV: a total loss car insurance claim. This is the practical, step-by-step roadmap an insurance adjuster uses to figure out what your vehicle was worth right before the accident.

The whole process starts with a solid baseline: the Replacement Cost. This isn't just a number pulled from thin air. Adjusters dig into data on recent sales of comparable vehicles—same make, model, year, and trim—right in your local area to find a realistic starting point.

This graphic breaks down the simple, three-step flow of the ACV calculation.

As you can see, it's a logical flow. You start with the value of a similar car, subtract for the wear and tear on your specific vehicle, and arrive at the final settlement number.

Calculating the Final Number

Once the Replacement Cost is set, it’s time to subtract for depreciation. This is where your car's personal history really matters. An adjuster will carefully deduct value for things like:

- Mileage: Higher numbers on the odometer mean more depreciation.

- Pre-accident condition: Dings, scratches, rust, and interior stains from before the crash will lower the value.

- Previous unrepaired damage: Any old damage that wasn't fixed will be factored in.

On the flip side, some things can actually add value back in. If you have documentation for recent major work, like a brand-new transmission or a fresh set of premium tires, that can help offset some of the depreciation.

Let's look at a clear, step-by-step example.

Sample Auto ACV Calculation

This table shows how an insurance company might work through the numbers for a totaled vehicle.

| Calculation Step | Description | Example Value |

|---|---|---|

| 1. Find Replacement Cost | Find recent sales of similar vehicles (same make, model, year, trim) in the local market. | $20,000 |

| 2. Calculate Depreciation | Deduct value for mileage (– $2,000), pre-accident wear like scratches and dents (– $500), and a cracked windshield (– $300). | – $2,800 |

| 3. Add for Recent Upgrades | Add back value for documented recent improvements, such as a new set of high-end tires. | + $600 |

| 4. Determine Final ACV | $20,000 (Replacement Cost) – $2,800 (Depreciation) + $600 (Upgrades) | $17,800 |

This process shows that the final ACV is a very specific number based on your car's unique condition and history, not just a generic book value.

Real-World Example: Imagine two identical 2018 sedans. Car A has 45,000 miles and a spotless maintenance record. Car B has 95,000 miles, a few door dings, and some interior stains. Even though they started as the same car, Car B will have far more depreciation subtracted, resulting in a much lower ACV settlement.

This valuation is a critical piece of the claims puzzle. To see where it fits into the bigger picture, you might be interested in our guide on how long it takes to settle a car accident claim. Understanding how the ACV is calculated gives you a much clearer idea of what to expect from your final offer.

When the ACV Definition Gets Complicated

https://www.youtube.com/embed/D1kuWKIa3sI

Just when you think you’ve got the actual cash value formula figured out, the legal system throws a curveball. That simple calculation of Replacement Cost minus Depreciation isn't the only game in town. In the real world, how ACV is interpreted can shift dramatically based on your specific insurance policy and state laws.

This isn't just a technicality—it can make a massive difference in your final settlement amount. Many insurance contracts don’t spell out a precise definition for ACV, leaving it open to interpretation. Because of this ambiguity, U.S. courts have landed on three primary ways to pin down a property's value. You can dive deeper into these legal perspectives by reading up on indemnity and insurance policy language on jsheld.com.

The Three Common ACV Interpretations

When a claim gets complicated or ends up in a dispute, the value can be determined using one of these three methods:

- Replacement Cost Less Depreciation: This is the standard formula we've been talking about. It's the go-to for most straightforward claims.

- Fair Market Value: This approach asks, "What would a willing buyer have paid a willing seller for this property right before it was damaged?" It’s a common way to value things where market demand is a huge part of the equation.

- The Broad Evidence Rule: This is the most flexible and holistic of the three, and it’s a concept you absolutely need to know.

Understanding the Broad Evidence Rule

Think of the Broad Evidence Rule as a way to look at the big picture. It empowers appraisers and courts to consider all relevant evidence to figure out an item's true value, rather than being locked into a single, rigid formula.

Key Insight: Under the Broad Evidence Rule, an adjuster can look beyond just the age and condition of your car. They might consider its location, local market demand, its original cost, and any other piece of evidence that helps paint a complete picture of its worth.

This rule is often your strongest tool for pushing back against a lowball insurance offer, especially in a complex claim. It’s a formal acknowledgment that an item's real-world value is sometimes much more nuanced than a simple depreciation calculation can capture.

This is a major reason why it’s worth investigating how much your totaled car is really worth instead of just accepting the first number the insurance company gives you.

Answering Your Top Questions About ACV

Even after you get the hang of the actual cash value formula, you're probably still wondering how it all works during a real insurance claim. Let's walk through some of the most common questions people have. My goal here is to give you the clarity you need to handle your settlement confidently.

Can I Negotiate the ACV Offer from My Insurer?

Yes, you absolutely can. Think of the insurance company's first number as a starting point, not the final word. If you look at their offer and your gut tells you it's too low, you have every right to push back.

Of course, a successful negotiation isn't just about feeling the offer is unfair—you have to prove it. Here’s how you can build a strong case for a higher value:

- Find Your Own Comps: Do your own homework. Look up what vehicles of the same make, model, year, and condition have recently sold for right in your local area. Car sale websites and dealer listings are gold mines for this kind of data.

- Document Everything: Pull together every service record you have. Got receipts for those new tires you put on last year or that new battery? Grab them. Pre-accident photos showing your car was immaculate are also powerful proof of its condition.

- Get an Independent Appraisal: This is your strongest weapon. An appraisal from a certified, independent expert provides an unbiased, detailed report on your car's true value. It’s hard for an insurer to argue with that.

If you hit a wall and can't reach an agreement, don't forget about your policy's "appraisal clause." You can learn more about how to invoke the appraisal clause in your auto insurance policy to force a fair and binding outcome.

What Is the Difference Between ACV and RCV?

This is a really important one, as it directly affects both what you pay for your policy and what you get paid after an accident. An Actual Cash Value (ACV) policy pays out based on your car's value today, with depreciation factored in. In contrast, a Replacement Cost Value (RCV) policy pays the full amount needed to buy a similar new vehicle, ignoring depreciation.

The Bottom Line: RCV coverage gives you a much bigger check, enough to go out and buy a brand-new replacement. Because of that superior payout, RCV policies always have higher monthly premiums than standard ACV policies.

Are Diminished Value and ACV the Same?

Nope. They're two distinct concepts that come into play in completely different scenarios.

- Actual Cash Value (ACV) comes up when your car is a total loss. It's the calculation of your vehicle's full market value right before the crash happened.

- Diminished Value (DV) applies after your car has been in an accident and repaired. It's the drop in resale value your car now has simply because it has an accident on its record. Even a perfectly fixed car is worth less to the next buyer.

So, you'd file an ACV claim when your car is totaled, but you'd file a DV claim to get compensated for the lost value on a car that was repaired.

At Total Loss Northwest, we specialize in making sure you get what you're truly owed. If you're staring at a lowball total loss offer or need to prove your vehicle's diminished value, our certified appraisals provide the leverage you need. Visit us at https://totallossnw.com to get started.