When it comes to insuring your vehicle, the difference between an agreed value and an actual cash value (ACV) policy is everything. It’s not just insurance jargon; it’s the line between a predictable, fair payout and a potentially disappointing surprise after a total loss.

At its heart, the distinction is simple. An agreed value policy guarantees a specific, predetermined dollar amount if your car is totaled, completely sidestepping depreciation. An ACV policy, on the other hand, pays out what your vehicle was worth the second before the accident, which means depreciation takes a huge bite out of your check.

Understanding the Core Valuation Methods

The valuation method written into your policy is the single biggest factor that will shape your financial recovery after a major claim. It’s the rulebook for how your insurance company calculates your final settlement.

Most standard auto policies you get for your daily driver will default to actual cash value. It’s the industry norm. But if you own a classic, a heavily modified car, or a rare collectible, you’ll quickly find that an ACV policy just doesn't offer the right kind of protection.

The choice really comes down to this: do you want to lock in a guaranteed payout amount from the start, or are you okay with the insurance company deciding your vehicle’s depreciated value after it's already gone? Your answer has major financial implications.

The Role of Depreciation

Depreciation is the natural decline in a vehicle's value from use, age, mileage, and general wear and tear. It’s the reason a car is worth less today than when you bought it, and it's the central character in the ACV story.

An agreed value policy takes depreciation completely out of the picture. Your payout is based on the value you and the insurer settled on when you bought the policy—a figure that reflects the car's true worth as a special-interest vehicle.

Key Insight: The entire debate of agreed value vs. actual cash value hinges on one thing: depreciation. Agreed value ignores it. Actual cash value is built on it.

Think about it this way: for your daily commute car that loses value predictably, ACV makes sense. But for a painstakingly restored 1969 Chevrolet Camaro, an ACV payout would be a disaster. It would completely ignore the thousands of dollars and countless hours invested, treating it like any other old car on the market.

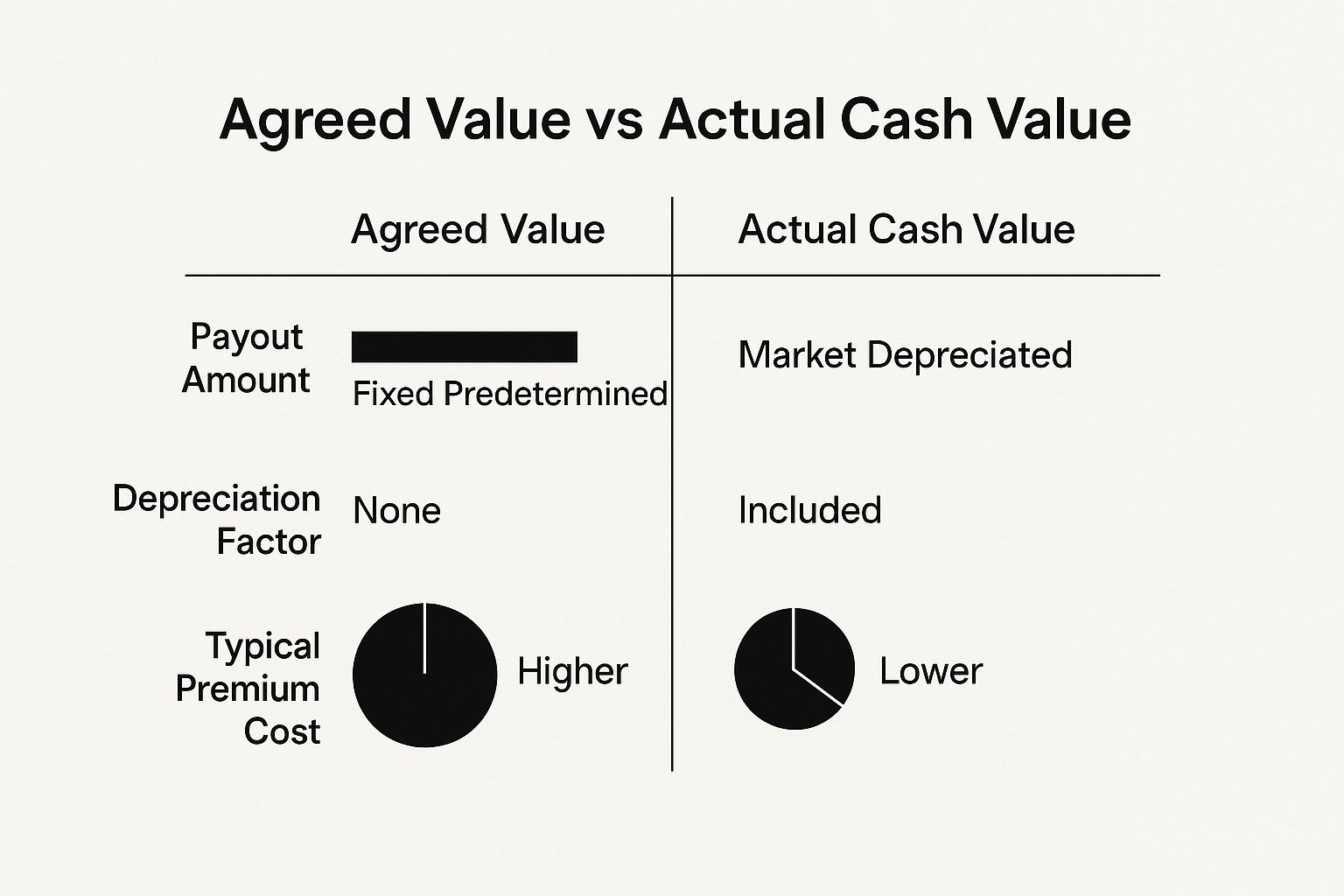

To make this crystal clear, let's break down the essential differences side-by-side.

Key Differences At a Glance

This table gives you a quick snapshot of how these two valuation models stack up against each other. It's a great reference for seeing the core distinctions in one place.

| Feature | Agreed Value | Actual Cash Value (ACV) |

|---|---|---|

| Payout Basis | A fixed amount you and the insurer agree upon when the policy begins. | The market value of the vehicle at the time of the loss, minus depreciation. |

| Depreciation | Not a factor in the final payout. The agreed-upon amount is guaranteed. | The primary factor used to calculate the final payout. |

| Financial Certainty | High. You know the exact payout amount from day one. | Low. The payout is unknown until after the loss occurs and is assessed. |

| Best Suited For | Classic cars, custom vehicles, collector items, and appreciating assets. | Standard, mass-produced vehicles used for daily transportation. |

| Premium Cost | Generally higher due to the guaranteed payout and increased risk for the insurer. | Typically lower, as the insurer's liability decreases over time with depreciation. |

As you can see, the right choice really depends on the type of vehicle you're insuring. One approach provides certainty and protects your investment, while the other offers a more basic, cost-effective coverage for standard cars.

How Agreed Value Insurance Protects Your Investment

With agreed value insurance, you’re creating a clear, upfront financial safety net for your most prized assets. This approach completely changes the dynamic of a total loss claim. Instead of haggling over value after a disaster, you settle on a number before the policy even starts. It’s a method designed to sidestep the uncertainty and frustration that can come with standard insurance payouts.

The process is straightforward. You and your insurer come to a mutual understanding of your car's specific worth. This isn’t a ballpark figure; it’s a formal agreement on the exact dollar amount you’ll receive if your vehicle is ever declared a total loss.

Establishing the Value

For vehicles with a unique or subjective worth—think restored classics or heavily customized builds—you'll need to back up the number with solid proof. Insurers will want to see why your car is worth what you say it is. You'll likely need to provide:

- A Professional Appraisal: A certified, independent appraiser can properly assess your car’s condition, rarity, and custom work to pin down its true market value.

- Detailed Photographs: Good pictures are non-negotiable. High-quality shots from every angle, including the interior, engine bay, and undercarriage, document the vehicle's real-world condition.

- Restoration Records: Keep every receipt. Invoices for parts, labor, and custom modifications provide tangible proof of the money you've poured into the vehicle.

Once this value is set and locked in, it becomes the guaranteed payout amount for your entire policy term. No last-minute surprises. No arguments about depreciation.

Eliminating Financial Ambiguity

The real power of this approach is certainty. You know exactly what you'll get paid in a worst-case scenario. This lets you make financial decisions without the stress of the unknown, which is crucial for anyone who owns an asset that doesn’t depreciate like a normal car.

The primary advantage of an agreed value policy is that it contractually removes depreciation from the claim equation. This ensures that the time, money, and passion invested in a special vehicle are fully recognized and protected.

This protection is a game-changer in the auto insurance world, especially for classic, collector, or highly modified vehicles. People invest in these cars expecting their value to hold steady or even grow. Standard actual cash value (ACV) policies chip away at payouts based on age and mileage, but agreed value guarantees a set amount. Of course, this guarantee often comes with a higher premium because the insurer is taking on more risk. You can learn more about how these policies work for unique vehicles at Bankrate.com.

Why the Higher Premium Is Worth It

Yes, agreed value policies usually cost more than their ACV counterparts. But that higher premium is a direct trade-off for complete peace of mind. You're paying for the guarantee that your investment is fully protected at a specific, predetermined figure.

Think about the alternative for a second. With an ACV policy, the insurance company decides your vehicle's value after it's been totaled. They'll use standard valuation tools that simply can't account for the unique qualities of a collector car, often resulting in a payout that falls painfully short of what you need to replace it.

Ultimately, an agreed value policy elevates your insurance from a simple necessity to a genuine asset protection tool. It ensures that a total loss is a manageable financial event, not a catastrophic one, by honoring the full, established worth of your unique vehicle. For anyone serious about safeguarding a significant automotive investment, this proactive approach to valuation is the gold standard.

Understanding Actual Cash Value and Depreciation

While an agreed value policy gives you a predetermined safety net, Actual Cash Value (ACV) works in a completely different way. It's the standard for the overwhelming majority of auto insurance policies out there, and it calculates your vehicle’s worth at the exact moment of the loss—not a day sooner.

The formula behind ACV is deceptively simple: Replacement Cost – Depreciation. What this really means is your payout isn't based on what you originally paid for the car. Instead, it’s based on what a similar used vehicle costs today, after subtracting value for every year, every mile, and every bit of wear and tear.

It's that one word—depreciation—that causes so much frustration. It's also the reason why an ACV settlement can feel like a lowball offer, as it systematically reduces the insurance company's payout over time. This is also why ACV policies usually come with lower premiums.

The Mechanics of Depreciation

Depreciation is simply the natural, unavoidable drop in an asset's value over time. When it comes to your car, insurers don't just pull a number out of thin air. They calculate it based on hard data that tells the story of your vehicle's life on the road.

Insurance companies rely on comprehensive valuation reports from third-party services that comb through market data to pinpoint a fair price. Several key factors get crunched in these reports:

- Age: The older a car gets, the more its value drops. It’s the biggest factor.

- Mileage: More miles mean more use, which directly lowers the car's worth.

- Condition: Every scratch, dent, interior stain, or minor mechanical issue gets factored in and reduces the vehicle's value.

- Market Demand: The popularity of your specific make and model also plays a role. A sought-after model might hold its value better than an unpopular one.

This process ensures the payout reflects what your car was realistically worth right before the accident. From a pure market standpoint, it’s fair. But for you, the owner, it can create a serious financial gap when it comes time to buy a replacement.

A Practical ACV Payout Example

Let's walk through how this plays out in the real world.

Imagine you bought a new sedan five years ago for $35,000. It's been your daily driver, and you've put 75,000 miles on it. After an accident, the insurance company declares it a total loss.

Here's a simplified look at how the insurer might calculate your payout:

- Find the Replacement Cost: The adjuster first looks at the current used car market and finds that a similar five-year-old sedan with around 75,000 miles is selling for $20,000.

- Calculate Depreciation: The valuation report takes into account its age, mileage, and some minor wear, calculating that the car has depreciated by $15,000 from its original sticker price.

- Finalize the Payout: Your final ACV settlement will be $20,000 (before you pay your deductible).

The Bottom Line: You get a check for $20,000, which is $15,000 less than you'd need to go out and buy a brand-new version of the same car. That shortfall is a direct result of depreciation, and it highlights the primary risk of an ACV policy.

This is exactly why getting a handle on ACV is so crucial. To go even deeper, you can learn more about what is actual cash value in our detailed guide. That difference between the insurance payout and the cost of a new car has to come straight out of your pocket.

When you're weighing agreed value vs actual cash value, this scenario perfectly illustrates the trade-off. With ACV, you get more affordable premiums, but you accept the risk of depreciation. It's a solid choice for most daily drivers, but it's a model that can leave you financially exposed if your car is totaled.

Comparing Payouts in Real-World Scenarios

It’s one thing to understand the definitions of agreed value and actual cash value, but it’s another thing entirely to see how they play out when disaster strikes. The valuation method you choose is what ultimately determines your financial recovery after a total loss. Let's move past the jargon and dig into two real-world scenarios to see the massive impact this choice can have.

Scenario One: The Meticulously Restored Classic Car

Meet Alex. He's a classic car buff who poured five years and a small fortune into restoring a 1967 Ford Mustang. He did everything by the book, getting a professional appraisal that valued his masterpiece at $75,000, factoring in its show-car condition, rare parts, and countless hours of labor. Then the worst happens—the car is stolen and never seen again. It’s a total loss.

How does his insurance respond?

-

With an Agreed Value Policy: The process is straightforward and, thankfully, free of stress. Alex and his insurer had already settled on the car's $75,000 worth when the policy was written. He files his claim, and they send a check for the full $75,000, minus his deductible. There's no argument, no haggling over depreciation—just the simple fulfillment of their agreement. Alex has the money he needs to buy a comparable Mustang or begin his next project.

-

With an Actual Cash Value (ACV) Policy: This outcome is a financial nightmare. The insurance adjuster plugs the car's details into a standard valuation tool, which just sees a 50-plus-year-old vehicle. The system has no way to properly account for the concours-level restoration or its collector status. It spits out a "market value" of $30,000 for a typical '67 Mustang in "good" condition.

The Financial Gap: Alex is left with a crushing $45,000 shortfall. The ACV payout completely ignores his investment of time and money, leaving him without the funds to replace the car he poured his heart into.

This image breaks down the core differences in how these policies calculate payouts, handle depreciation, and what they cost.

As you can see, an agreed value policy provides a predictable, fixed payout because it removes depreciation from the equation. That’s why it justifies a higher premium, especially for owners of special assets.

Scenario Two: Major Damage to an Aging Commercial Property

Now, let's look at Sarah, who owns the 20-year-old building that houses her manufacturing company. A devastating fire causes catastrophic damage. The estimated cost to rebuild everything to today’s code is a staggering $1.2 million.

Her ability to recover hinges entirely on her insurance policy.

-

With an Agreed Value Policy: Before her policy term even started, Sarah and her insurer agreed the building's value was $1.2 million. By locking in this value, the policy’s coinsurance clause was waived. After the fire, she receives a check for the full $1.2 million (less her deductible). She has the capital to rebuild and get her business back on its feet without facing financial ruin.

-

With an Actual Cash Value (ACV) Policy: The adjuster's math is brutal. They start with the $1.2 million replacement cost but then subtract 20 years of depreciation on the roof, structure, and internal systems. That depreciation totals $400,000. Suddenly, the actual cash value of her building is determined to be only $800,000.

To make matters worse, if her policy included a coinsurance clause and she was underinsured, her payout could be slashed even further. She's now facing a massive financial hole just to get her business operational again. When you're facing a complex claim, learning how to navigate a total loss estimate is essential for getting a fair settlement.

Scenario Payout Comparison

The table below provides a clear financial breakdown of how these two scenarios would resolve under each policy type, highlighting the potential financial disparity.

| Scenario | Agreed Value Payout | Actual Cash Value Payout | Financial Difference |

|---|---|---|---|

| Classic Car Theft | $75,000 | $30,000 | -$45,000 |

| Commercial Property Fire | $1,200,000 | $800,000 | -$400,000 |

The numbers don't lie. For unique, high-value, or appreciating assets, an agreed value policy is a powerful guarantee of financial certainty. It ensures you can recover your full investment. An ACV policy, while cheaper upfront, leaves you exposed to the harsh and unpredictable reality of depreciation, a risk that can be financially devastating when you need your coverage the most.

Navigating Commercial Property Insurance Risks

When we talk about insuring commercial property, the agreed value vs. actual cash value debate isn't just an academic exercise—the stakes are incredibly high. A commercial building isn't like a family car; it’s a massive, often illiquid, investment that serves as the backbone of an entire business. Picking the wrong insurance valuation here isn’t a small mistake. It can be a catastrophic, business-ending event.

For a business owner, an Actual Cash Value (ACV) policy introduces a tremendous amount of risk that's tough to get your arms around. A commercial property’s value is anything but static. It gets pushed and pulled by volatile market forces, especially fluctuating construction and material costs that can spike without warning. An ACV policy that looked perfectly adequate last year could leave you dangerously underinsured today, and you might not know it until it's far too late.

This volatility basically turns an ACV policy into a big gamble. If you suffer a major loss, like a fire or a structural collapse, your payout is based on the depreciated value of a building that might cost 30% more to rebuild than it did a few years ago. That creates a huge financial gap that can stop your recovery dead in its tracks.

The Hidden Danger of Coinsurance Penalties

One of the sneakiest and most damaging parts of an ACV policy for commercial properties is the coinsurance clause. This clause is a requirement from the insurer that you insure your property for a specific percentage of its total replacement value, usually 80% or 90%. If your coverage dips below that threshold when a loss occurs, the insurer hits you with a steep penalty, which slashes your claim payout.

Because ACV is tied to a constantly changing replacement cost, it's dangerously easy to slip into being underinsured without even realizing it. All it takes is a surge in construction costs, and if you haven't adjusted your coverage up, you could easily fall below that coinsurance requirement.

Crucial Takeaway: A coinsurance penalty is essentially a financial punishment for being underinsured. With an ACV policy, market volatility can push you into the penalty zone without any warning, turning a major loss into an absolute financial disaster.

A Mathematical Breakdown of Coinsurance Risk

Let's look at just how devastating a coinsurance penalty can be. This math really shows why agreed value coverage is so much safer.

Imagine you have a commercial building insured for $500,000 with an 80% coinsurance clause. However, the true replacement cost today is $800,000. If a fire causes $200,000 in damage, the insurer will penalize you for not meeting the 80% threshold.

The payout is calculated as (Coverage Purchased / (Replacement Cost × Coinsurance %)) × Loss – Deductible. In this scenario, you'd only get about $155,250 after a $1,000 deductible. That leaves you with a staggering, unexpected shortfall of nearly $45,000. If you want to dive deeper into the mechanics, you can find great resources on understanding the agreed value option.

This isn't a rare "what if" scenario; it happens all the time. Countless business owners get a nasty shock when their payout is cut, leaving them to scramble to cover a massive repair bill out of pocket.

Agreed Value as a Commercial Safety Net

This is precisely where an agreed value policy becomes an indispensable tool for commercial property owners. When you choose agreed value, you and your insurer work together to determine and lock in the property's full value right at the start of the policy.

This one simple step has a few powerful consequences:

- It waives the coinsurance clause entirely. As long as you insure the property for 100% of that agreed-upon amount, you will never, ever face a coinsurance penalty.

- It takes market volatility out of the equation. Your payout is guaranteed, no matter what happens to construction costs during your policy term.

- It gives you absolute financial certainty. You know the exact dollar amount you will receive to rebuild, which allows you to plan your recovery with confidence and act immediately.

For any serious commercial investor, this level of predictability isn't a luxury—it's a foundational risk management strategy. By knocking out the dual threats of depreciation and coinsurance penalties, an agreed value policy acts as a reliable financial backstop, ensuring that a property loss doesn't spiral into a complete business failure.

How to Choose the Right Insurance Valuation

When you're staring at the choice between agreed value vs. actual cash value, it really just boils down to a few straightforward questions about your vehicle and your financial comfort zone. There’s no single "best" answer here; the right policy for you is completely tied to your unique situation.

Thinking through these points honestly will help you sidestep a costly mismatch and make sure your coverage actually does its job when you need it most.

Assess Your Asset’s Value Trajectory

First thing's first: Is your vehicle gaining value, holding steady, or losing it? For the car you drive to work every day, the answer is a no-brainer—it’s depreciating. An Actual Cash Value (ACV) policy is built for exactly this reality, which is why the premiums are generally lower. The insurer's potential payout shrinks as the car gets older.

But what if you own a classic car, a custom hot rod, or a rare import? These vehicles often go up in value, or at least hold steady. An ACV policy just doesn't make sense here; it would actually penalize you for owning an asset that defies the usual depreciation curve.

The rule of thumb is pretty simple: A depreciating asset gets a depreciating valuation (ACV). An appreciating or stable asset needs a stable valuation (agreed value).

For anyone with a special vehicle, agreed value is almost always the right call. It locks in the car's true worth. If this is you, it’s also crucial to understand the specific classic car insurance requirements to make sure you’re properly covered from the get-go.

Evaluate Value Subjectivity and Your Risk Tolerance

Next, think about how easy it is to put a price tag on your asset. A 2021 Honda Civic has a clear market value you can look up in minutes. ACV works perfectly in this scenario because there's little room for debate on what it’s worth.

On the other hand, a custom-restored 1969 Camaro with a modern engine has a value that standard pricing guides simply can't capture. This is where an agreed value policy is a lifesaver. You and the insurer settle on the value upfront, eliminating any guesswork or arguments later.

Finally, you have to be honest about your own tolerance for financial risk. Would you be okay with a payout that might not be enough to buy the exact same car again, if it meant you paid less each month? If you can stomach that risk, ACV is a reasonable choice.

But if you need absolute certainty that you can replace your asset without touching your savings, then the higher premium for an agreed value policy is a worthwhile investment. It’s a bit like buying peace of mind.

This logic is especially critical in the world of commercial property. For a business owner, an agreed value endorsement means the insurer agrees on the property's value ahead of time. This removes nasty surprises like coinsurance penalties and ensures a predictable payout, providing much-needed stability in a fluctuating market. You can find more details on how agreed value works in commercial property insurance at TheCoyleGroup.com.

Frequently Asked Questions

When you're trying to figure out agreed value vs. actual cash value, a few common questions always seem to pop up. Let's clear the air and give you some straight answers to help you decide on the right coverage for your car.

What Is the Main Difference Between Agreed Value and ACV?

The big difference really boils down to one word: depreciation.

With an agreed value policy, you and the insurance company lock in a specific payout amount right at the start. If your car is totaled, that's the exact amount you get, no questions asked about depreciation. An actual cash value (ACV) policy, on the other hand, pays you what your car was worth the moment before the accident. That means its value has been chipped away by age, mileage, and general wear and tear.

Is Agreed Value Insurance More Expensive?

Yes, you can expect to pay a higher premium for an agreed value policy. Think of it this way: you're paying for the peace of mind that comes with a guaranteed payout. You're essentially transferring the risk of depreciation from your shoulders to the insurance company's.

For anyone who owns a classic, a custom build, or a rare vehicle, that extra cost is often well worth it.

Key Takeaway: The higher premium for an agreed value policy is the price you pay to eliminate financial uncertainty. You're protecting the full, established worth of a unique or even appreciating vehicle.

Can I Get Agreed Value for My Daily Driver?

In most cases, no. Agreed value coverage is really meant for special vehicles where the usual valuation methods just don't work. We're talking about:

- Classic and Collector Cars: Vehicles that often hold or even increase in value over time.

- Heavily Modified Vehicles: Cars with thousands of dollars in custom work and aftermarket parts.

- Exotic or Rare Models: High-end, limited-production cars.

Your everyday commuter car follows a pretty predictable depreciation path, which makes standard ACV coverage the right (and more affordable) fit.

How Is the Agreed Value Determined?

Setting the agreed value is a team effort between you and your insurer before the policy even starts. You can't just pick a number out of thin air. You'll need to back it up with solid proof, which usually means providing a professional third-party appraisal, detailed photos, and any receipts from restoration or custom work.

This back-and-forth ensures the final, locked-in value is a true reflection of what your car is actually worth.

If your car is totaled and you're staring at a lowball ACV offer from your insurance company, remember you don't have to take it. Total Loss Northwest specializes in independent auto appraisals to fight unfair valuations. We can invoke the Appraisal Clause in your policy to get you the fair, accurate settlement you deserve.

Visit us at https://totallossnw.com to see how we can help.