An auto appraisal for diminished value is all about calculating the permanent hit your car’s market value takes after an accident—even if the repairs are flawless. This loss is real money, and you're legally owed it by the at-fault driver's insurance. A professional appraisal is the tool you need to get it back.

What Is Diminished Value and Why It Matters

Let's use a real estate analogy. Imagine two identical houses side-by-side. One is pristine. The other had a serious fire last year, but it was repaired perfectly by the best builders in town. Which one would you rather buy? Even with perfect repairs, a buyer will always pay less for the house with a history of damage.

That’s exactly what happens to your vehicle after a crash. This permanent loss in resale value, purely because of its accident history, is called diminished value. It's the invisible scar that remains long after the dents are gone and the new paint has cured. This "stigma" directly affects what a dealer will offer you on trade-in or what a private buyer is willing to pay. Getting a handle on this concept is the first step in the claims process, which can be part of the broader personal injury claims process if you were also hurt in the accident.

The Three Types of Diminished Value Explained

When we talk about diminished value, it's not a single, catch-all term. It actually breaks down into three distinct categories that represent the loss at different stages. Knowing the difference is crucial for building a solid claim with the insurance company.

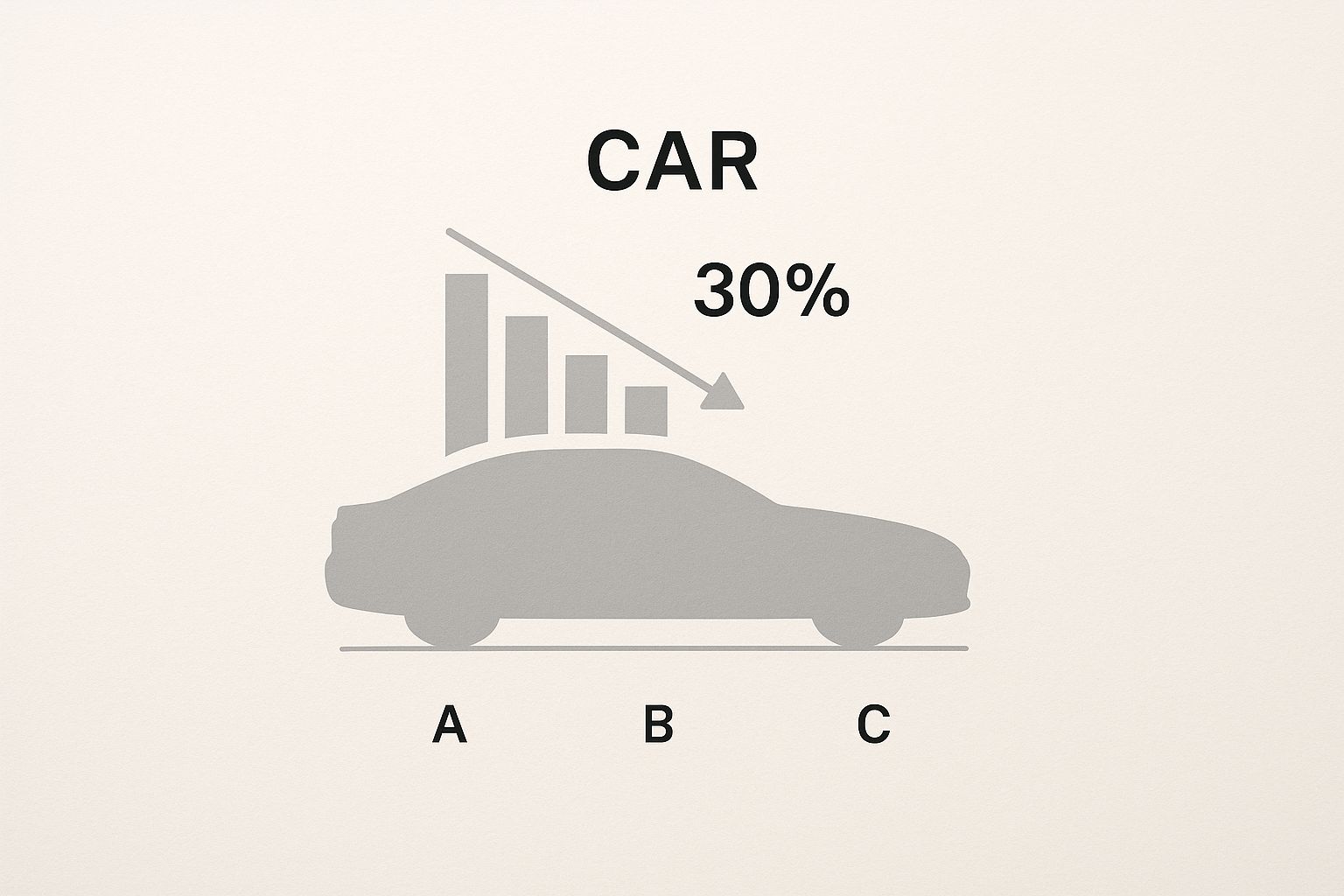

Below is a quick breakdown of how a car's value drops after an accident, even when it's put back together perfectly.

The image really drives home the point: a vehicle’s worth takes an immediate and permanent hit from which it never fully recovers, showing exactly why a diminished value claim is so important.

The most common and important type for most people is Inherent Diminished Value. This is the automatic loss in value that happens simply because the vehicle now has an accident on its record. In my experience, vehicles with a documented accident history can easily see their resale value drop by 20% to 30%.

To really understand your potential claim, it's helpful to see how these different types of diminished value fit together.

The Three Types of Diminished Value Explained

Understanding the nuances of diminished value is key. Here’s a simple table that lays out the three main categories you might encounter.

| Type of Diminished Value | What It Means | When It Occurs |

|---|---|---|

| Inherent Diminished Value | The automatic loss in value from the vehicle having a documented accident history. | Occurs immediately after an accident, even with flawless, high-quality repairs. This is the most common type. |

| Repair-Related Diminished Value | Additional loss in value due to poor or incomplete repairs. | Happens when the body shop uses non-OEM parts, fails to match paint correctly, or leaves evidence of the repair. |

| Immediate Diminished Value | The difference in value immediately before the accident and immediately after, before repairs are made. | This is a temporary state, as the value is restored (partially) once repairs are complete. It’s less commonly used in claims. |

While all three are valid, your claim will almost always focus on Inherent Diminished Value—the loss that can't be fixed by a body shop.

At the end of the day, a diminished value claim is about making you whole again. The at-fault party didn't just dent your bumper; they damaged your vehicle's long-term worth. Knowing how to define and prove that loss is everything. For more on this, you can check out our guide on how to determine fair market value for your specific vehicle.

How Insurance Companies Undervalue Your Claim

After an accident, you’d think the at-fault driver's insurance company would step up and make you whole. But when it comes to a diminished value claim, their goal isn't to compensate you fairly for your car's lost resale value. Their objective is to minimize their payout, and they have a tried-and-true playbook for doing just that.

You’ll almost certainly get a lowball offer. It’s not personal; it’s just business.

To justify these low numbers, most insurance carriers pull out a flawed, one-size-fits-all calculation known as the "17c formula." This came out of a Georgia court case back in 2001 (Mabry v. State Farm), and it was never meant to be the universal standard for every car and every accident. It's a tool they use for their convenience and financial benefit, not for an honest market valuation.

Their Secret Weapon: The 17c Formula

So, what is this 17c formula? Think of it as the insurance industry's secret handshake for calculating diminished value. They love it because it’s a quick, assembly-line calculation that systematically lowballs your claim through a series of arbitrary caps and modifiers.

It completely ignores the unique details of your vehicle, the severity of the repairs, and what buyers in your local market are actually willing to pay for a car with an accident history. It’s designed from the ground up to produce a small number that saves them money.

Here’s a look at how this flawed formula typically works to shrink your payout:

- An Arbitrary Starting Cap: The calculation kicks off by immediately capping your potential diminished value at 10% of the car's pre-accident value, based on a pricing guide like NADA or Kelley Blue Book. This 10% ceiling is completely arbitrary and has no basis in real-world market data. Right from the start, your potential claim is limited, no matter how bad the accident was.

- The Damage Modifier: Next, they apply a "damage modifier." This is a multiplier that reduces the already-capped value even further. Major structural damage might get a 1.0 multiplier (no reduction from the cap), but moderate damage could get a 0.50 multiplier, instantly cutting the figure in half.

- The Mileage Modifier: Finally, they hit your claim with a "mileage modifier" that punishes you for simply driving your car. A vehicle with over 100,000 miles could see its diminished value figure slashed by another 80% or more.

By the time they're done, the final offer is just a tiny fraction of what your car truly lost in value.

Relying on the insurance company's 17c calculation is like letting the person who crashed into your car decide how much they owe you. The conflict of interest is obvious, and the formula is rigged in their favor.

A Real-World Example of Undervaluation

Let's walk through how this plays out with a real-world example. Say your two-year-old SUV, worth $40,000 before the wreck and with 30,000 miles on the odometer, gets hit. The damage is significant, but the frame is intact.

Here’s how the insurer’s math would likely look:

- Step 1 – Base Loss Cap: 10% of $40,000 = $4,000

- Step 2 – Damage Modifier: The damage was serious but not structural, so they assign a 0.75 multiplier. ($4,000 x 0.75 = $3,000)

- Step 3 – Mileage Modifier: With 30,000 miles, they might apply a 0.60 multiplier. ($3,000 x 0.60 = $1,800)

The insurance company proudly offers you $1,800.

The problem? A true market analysis from an independent appraiser would likely show that buyers would pay $5,000 to $6,000 less for your SUV compared to an identical one with a clean CARFAX report. The 17c formula just cheated you out of thousands of dollars.

This is precisely why getting an independent auto appraisal for diminished value is so critical. A professional appraiser doesn’t use a self-serving formula. They perform a detailed, evidence-based analysis of your specific vehicle and local market to determine the real financial loss. That expert report is the ammunition you need to fight back and demand the full compensation you're legally owed.

The Power of an Independent Auto Appraisal

After seeing how insurance companies can lean on flawed formulas like "17c" to downplay your claim, it's pretty clear you can't just take their word for it. This is where you bring in your secret weapon: an independent auto appraisal for diminished value.

Think of it as hiring your own expert—someone who is on your side—to counter the insurer's biased math and fight for the money you're actually owed. An independent appraiser works for you, and only you. Their entire job is to figure out the real, fair market loss your car suffered because of the accident. They don't use arbitrary formulas; they rely on established, professional methods to build a credible, evidence-backed valuation. This report is the bedrock of your claim and your single best piece of leverage.

This professional assessment isn't just a number on a page. It's a comprehensive document that meticulously builds the case for your vehicle's lost value, making it incredibly difficult for an insurance adjuster to dismiss.

What Goes into a Professional Diminished Value Report

A high-quality diminished value report is a world away from a simple estimate. It's a detailed analysis that dissects every single factor contributing to your car's loss in value. It's this level of detail that separates a real appraisal from the insurer's often superficial calculation and gives you the proof you need.

A credible report will almost always include:

- Vehicle Information: A complete profile of your car—year, make, model, trim, options, mileage, and its specific pre-accident condition.

- Market Analysis: A deep dive into the local market, comparing your vehicle to similar ones that have a clean history and are currently for sale.

- Repair Quality Scrutiny: An expert assessment of the repair work itself. This includes looking at the extent of the damage and, importantly, whether the shop used OEM parts or cheaper aftermarket ones.

- Pre-Accident vs. Post-Repair Values: Clear, side-by-side documentation showing the car's fair market value right before the crash versus its value after the repairs were finished.

This thorough, step-by-step approach ensures every aspect of your loss is properly documented and justified.

Finding and Vetting a Qualified Appraiser

Hiring the right appraiser is probably the single most important step you'll take. A credible, experienced professional adds significant weight to your claim. A weak or unqualified one can completely undermine it. You're looking for someone whose credentials and methods will stand up to scrutiny from the insurance company.

When you start your search, look for certifications from recognized industry bodies. A certified appraiser is held to professional standards, which instantly adds a layer of credibility to their report. A good place to begin is searching for local, independent appraisers who specifically specialize in diminished value.

Once you have a shortlist, it's time to do some digging and ask the right questions to make sure they're a good fit for your case.

A professional appraisal isn't just an opinion; it's evidence. It transforms your claim from a simple request into a well-supported demand for fair compensation, shifting the balance of power back in your favor.

To help you choose wisely, here are a few key questions you should ask any potential appraiser:

- "Are you a certified appraiser?" Ask to see their credentials and find out which organizations they belong to.

- "Do you specialize in diminished value?" A general auto appraiser might not have the specific expertise you need for this unique type of claim.

- "What methodology do you use?" They should be able to explain their process clearly, and it definitely shouldn't be the 17c formula.

- "Have your reports been used against my specific insurance company before?" Experience going up against particular carriers can be a huge advantage.

Armed with a solid appraisal report from a true expert, you'll be well-prepared for the negotiation phase. When you're ready to move forward, our guide on how to negotiate a diminished value claim offers practical, actionable strategies.

How State Laws Impact Your Diminished Value Claim

Trying to get a handle on diminished value is a bit like playing a game where the rules change every time you cross a state line. Your ability to get paid for your car's lost value doesn't just depend on the quality of your appraisal; it's deeply tied to the specific laws of the state where the accident happened. This legal patchwork can feel overwhelming, but understanding a few key concepts is the first step toward building a winning strategy.

The most critical legal distinction you'll encounter is who you're filing the claim against. This one factor splits every claim into two different buckets: first-party and third-party. Get this right, and you’ll know if you even have a path forward.

The Critical Difference: First-Party vs. Third-Party Claims

These terms might sound like dry legal jargon, but the idea is actually quite simple. It all boils down to whose insurance company you're asking to pay up—yours or the other driver's.

- First-Party Claim: This is when you file with your own insurance company. You'd typically do this if you were at fault or if you're using your own collision coverage to get your car repaired, regardless of who caused the accident.

- Third-Party Claim: This is when you file against the at-fault driver's insurance company. In this scenario, you are the "third party" to the insurance contract between the other driver and their insurer.

This distinction changes everything. Why? Because the insurance policy you have is a contract, and that contract almost always includes fine print that excludes diminished value. Your insurer agrees to pay to repair your vehicle to its pre-accident condition, but they make no promise to restore its pre-accident market value.

The takeaway is simple but powerful: In nearly every state, you can only recover diminished value from the at-fault party's insurance (a third-party claim).

For the most part, trying to file a first-party diminished value claim is a dead end. The at-fault driver's carelessness is what caused your financial loss, so it's their insurance company that's on the hook to make you whole again.

A Look at How States Handle Diminished Value

Even with the nearly universal first-party vs. third-party rule, states still have different legal precedents and approaches. This crazy quilt of regulations makes knowing your local rules absolutely essential.

Some states have strong, clear court rulings that explicitly back a vehicle owner’s right to third-party diminished value. Others have murkier case law, which can make the process more of an uphill battle—but not necessarily an impossible one. For example, successfully navigating a diminished value claim in Oregon means knowing the specific local precedents and the common tactics insurers use there.

To give you a better sense of how much this can vary, the table below provides a general overview of how different states often treat these claims. Keep in mind, this is just a high-level summary to illustrate the differences, not legal advice.

State-by-State Diminished Value Claim Approaches

| State Approach Category | Third-Party Claim (At-Fault Driver's Insurance) | First-Party Claim (Your Own Insurance) |

|---|---|---|

| Most States (e.g., California, Texas, Oregon) | Allowed. The at-fault party is legally responsible for all damages caused, including the loss of market value to your vehicle. | Generally Not Allowed. Most insurance policies explicitly exclude diminished value coverage. |

| "No-Fault" States (e.g., Florida, Michigan) | Can be complex. Rules vary. You often must meet a certain threshold of injury or damage before you can step outside the no-fault system to sue the at-fault driver for property damage. | Not Allowed. The no-fault system is designed to have each driver's own insurance cover their losses, and policies typically exclude DV. |

| Georgia | Strongly Supported. Georgia has some of the most established case law (like the Mabry case) that firmly recognizes and allows for third-party diminished value claims. | Allowed (Rare Exception). Georgia is one of the very few states where case law has allowed for first-party inherent diminished value claims under specific circumstances. |

At the end of the day, your geographic location sets the stage for your entire claim. It determines who you can file against and even influences how hard an insurance company might fight you. This is precisely why a professional, independent auto appraisal for diminished value is so crucial—it gives you the solid, market-based proof you need to build an undeniable case within your state’s unique legal framework.

Economic Trends That Affect Your Vehicle's Value

Your car doesn't exist in a bubble. Its value is constantly being pushed and pulled by the powerful currents of the automotive market. To get a fair diminished value claim, you first have to understand the bigger economic picture, because that's what sets the baseline value for your car before the accident.

Think of it like the housing market. A home's price is heavily influenced by things like neighborhood appeal, current interest rates, and how many other houses are for sale. It's the same with your vehicle. A professional appraiser has to dig into these major economic forces to get your auto appraisal for diminished value right.

If you ignore this financial backdrop, you're simply not seeing the full scope of your loss.

Supply Chains and Used Car Prices

We've all seen in recent years how fragile supply chains can be. When new car production grinds to a halt because of a computer chip shortage or shipping delays, what happens? The demand for quality used cars goes through the roof, creating a "hot" market where prices climb higher than usual.

When this happens, your vehicle's pre-accident value is artificially inflated. That means the dollar amount you lose from a wreck—your diminished value—is also much higher. An insurance company's generic formula will completely miss this real-time market pressure, but a dedicated appraisal is built to capture it.

On the flip side, when new car lots are full and interest rates climb, the used car market can cool off fast, which might lower your car’s pre-accident value. An appraiser's job is to pinpoint the precise market conditions at the moment of your accident to establish a fair and accurate starting point for the entire claim.

The Role of Market-Wide Depreciation

Depreciation—the inevitable drop in value over time—is the single biggest thief of your car's worth. But it's not a slow, steady decline. The connection between market depreciation and diminished value is critical. For instance, in 2024, while the average vehicle depreciated by about 12.5%, some segments got hit much harder. Full-size vans plummeted by nearly 19.8% and luxury cars by 18.0%. In stark contrast, compact cars only saw a 5.8% dip. You can see a more detailed breakdown of these depreciation figures and how they impact what a car is worth.

A professional appraiser doesn’t guess. They use current, localized market data to understand how your specific make and model is performing right now, ensuring your claim is based on today's values, not last year's.

The Growing Influence of Electric Vehicles

The automotive industry is in the middle of a massive pivot to electric vehicles (EVs), and this shift is sending new ripples across the entire market. It affects the value of both traditional gas-powered cars and even older EVs.

Here's how it breaks down:

- For gasoline cars: As more attractive and affordable EVs come out, the demand for certain gas models can start to soften, which speeds up their depreciation.

- For electric vehicles: Battery technology and driving range are improving at a dizzying pace. This can make EVs from just a few years ago seem outdated, causing them to lose value even faster than a comparable gas car.

A credible auto appraisal for diminished value absolutely has to account for these long-term trends. A good appraiser will analyze whether your vehicle belongs to a segment that is gaining or losing favor due to the EV transition. This provides a more complete, forward-looking assessment of its true place in the market—a level of detail an insurer’s quick calculation will never provide.

Common Questions About Diminished Value Claims

Once you get a handle on what diminished value is and why you need an independent appraisal, a few practical questions almost always come up. That’s perfectly normal. Getting the concepts down is one thing, but actually starting the claims process can feel like a big step.

This section is here to give you clear, straightforward answers to the questions we hear most often. Think of it as a final gut-check to clear up any lingering doubts, so you can move forward with confidence and get the money you’re owed.

How Long Do I Have to File a Diminished Value Claim?

This is one of the most important questions, and the answer is all about where you live. Every state has a legal deadline for filing property damage claims, known as the statute of limitations. This window usually falls somewhere between two and six years from the date of the accident.

But just because you might have a few years, you shouldn't wait. The best time to start your claim is right after the repairs on your car are finished.

Why the rush?

- Evidence is Strongest: The connection between the accident and your car’s drop in value is undeniable right after it happens. If you wait, the insurance company has an easier time arguing that other things—like wear and tear or mileage—caused the value loss.

- Market Data is Current: An appraisal relies on real-time market conditions. Filing promptly means your car’s value is assessed based on the market at the time of the loss, not years down the road when things might look completely different.

- You Get Paid Sooner: Let's be honest, this is about getting your money back. Acting quickly gets the ball rolling and puts the settlement in your pocket much faster.

Can I Claim Diminished Value if the Accident Was My Fault?

This is a frequent point of confusion, but the answer is almost always a firm no. You generally can’t file a diminished value claim if you were the one at fault for the accident.

It all comes down to the type of claim. When you file against the other driver’s insurance, that’s a third-party claim. When you file with your own insurance, it's a first-party claim. Your own policy is a contract that agrees to pay for repairs, but it specifically excludes covering your car’s drop in resale value. Because of this, you can only go after the person (and their insurer) who was negligent and caused the damage in the first place.

When you pursue a diminished value claim, you are holding the at-fault driver financially responsible for making you whole again. That includes restoring not just the physical damage, but also the market value their actions took away.

Will Filing a Diminished Value Claim Make My Insurance Rates Go Up?

It’s a fair question, but you can put this worry to rest. Filing a third-party claim against the at-fault driver’s insurance should have no impact on your insurance rates.

Your insurance company isn’t paying a dime for this claim, so they have no financial reason to raise your premiums. You are simply using your legal right to be compensated for damages caused by someone else’s mistake. The claim is against their policy, not yours, so it won’t show up on your record as a claim you filed.

Is It Worth Pursuing a Claim for an Older or High-Mileage Car?

It really depends, but don't write it off without a second thought. While it's true that newer, high-end cars see the biggest diminished value payouts, an older vehicle can still lose a significant and very real amount of money. The deciding factor is usually the ratio of the potential recovery to the cost of the appraisal.

For instance, picture a well-cared-for, 10-year-old truck worth $15,000 before someone hits it. If it needs $7,000 in repairs, its value on the market could easily be $2,000 lower than before, even after being fixed. In that scenario, pursuing the claim is absolutely worth it. An auto appraisal for diminished value is crucial even when a vehicle isn't totaled. When a car is totaled, insurers use market value to calculate a settlement, but diminished value represents the loss that exists beyond just the repair costs. This makes accurate appraisals vital for negotiating fair settlements in today's unpredictable market. You can discover more insights about car value trends on Diminished Value of Georgia.

A good appraiser can often give you an initial consultation to help you weigh the numbers. They’ll give you a realistic idea of what you might recover versus the appraisal fee, so you can make a smart financial choice before you dive in.

If you're dealing with a diminished value or total loss situation, don't let the insurance company dictate what your vehicle is worth. At Total Loss Northwest, our certified appraisers specialize in creating ironclad reports that force insurers to pay what you're truly owed. We serve vehicle owners across Oregon, Washington, and all 50 states, ensuring you get a fair and accurate settlement.

Take control of your claim and fight for your vehicle's true value at totallossnw.com