When your insurance company’s settlement offer feels insultingly low after an accident, it’s easy to feel powerless. But you have a powerful tool tucked away in your policy to fight back: the auto insurance appraisal.

Think of it as bringing in a neutral expert—a tie-breaker—to determine the real cost of your repairs or the true market value of your car when you and the insurer are at a stalemate. It’s often your best shot at getting the fair settlement you deserve.

Understanding The Auto Insurance Appraisal

Let's face it, after a wreck, the last thing you want is another fight. You pay your premiums on time, expecting your insurer to have your back. But what happens when their idea of "fair value" doesn't even come close to reality? This is exactly when an auto insurance appraisal becomes your most important next step.

This isn’t about filing a lawsuit or getting tangled in a messy legal battle. It's a right that’s usually built directly into your auto policy, often called the “Appraisal Clause.” This provision is a formal dispute resolution process. It allows both you and your insurer to hire your own independent, certified appraisers to value the loss, taking the insurance company's biased valuation software completely out of the picture.

When An Appraisal Becomes Necessary

So, when do you pull this lever? An appraisal is usually needed when you and the insurance adjuster have hit a wall and can't find any common ground. Recognizing these moments is key to protecting your financial interests.

Most often, you'll find yourself needing to invoke the appraisal clause in a few common situations.

Here’s a quick look at the most common scenarios where invoking the appraisal clause is your best move.

When You Might Need an Auto Insurance Appraisal

| Situation | Why an Appraisal is Needed |

|---|---|

| Lowball Total Loss Offer | The insurer's settlement is thousands less than what similar cars are actually selling for in your area. |

| Disputes on Repair Costs | Your trusted body shop says one thing, but the insurer’s estimate is far lower, often pushing for cheap, aftermarket parts. |

| Diminished Value Disagreement | Your car is repaired, but it's now worth less. The insurer denies your diminished value claim or offers a ridiculously low amount. |

Ultimately, initiating the appraisal process ensures you're not left at the mercy of an algorithm designed to save the insurance company money.

The whole point of an auto insurance appraisal is to get an objective, evidence-based valuation. It forces the settlement to be based on your vehicle's actual market value, not just the insurer's initial low offer.

This process is more critical now than ever. In early 2024, the U.S. auto insurance industry saw premium rates jump by 20.6% year-over-year—the biggest hike since the 1970s. This surge is fueled by skyrocketing repair costs, which makes insurers scrutinize every single claim payout more aggressively. You can dig deeper into the factors driving insurance rate hikes on GlobalData.com.

How the Appraisal Clause in Your Policy Works

Buried deep within the fine print of your auto insurance policy, there’s a powerful tool most people don't even know exists: the appraisal clause. It’s not just more legalese. It's your contractual right to fight back when an insurance company lowballs your settlement offer.

Think of it as a built-in dispute resolution system. When you and your insurer can't agree on what your car is worth, invoking this clause takes the argument out of the hands of adjusters and puts it into the hands of independent experts. It forces the insurance company to justify its numbers and levels the playing field.

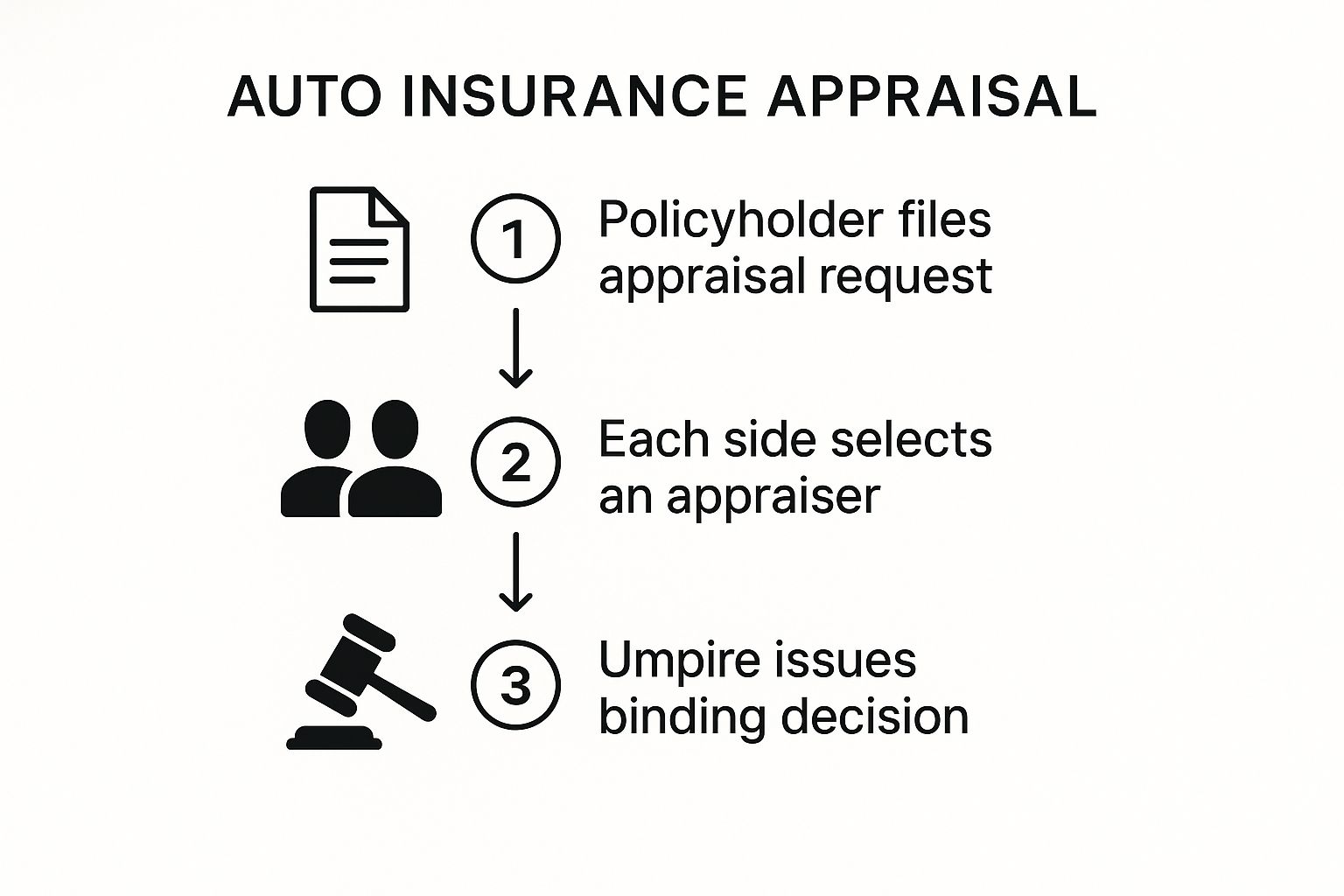

Kicking Off the Appraisal Process

Getting started requires a formal step. You have to tell your insurance company—in writing—that you are invoking the appraisal clause. A phone call won't cut it. Sending a certified letter is the best way to create an official record and get the ball rolling.

Once you send that letter, the process officially begins. You and the insurance company must each hire an independent and competent appraiser. This is the single most important decision you will make. The quality of your appraiser will make or break your case.

Key Takeaway: The appraisal clause is a binding process. Once it’s finished, the value determined by the appraisers is almost always final. Both you and the insurer have to accept it.

Appraisers and the Umpire: How It Works

Once both sides have chosen their experts, the real work begins. Your appraiser and the insurer's appraiser will independently research your vehicle's value, pulling market data and building a case for their valuation. This isn't a shouting match; it's a methodical, evidence-based negotiation.

Often, the two appraisers can come to an agreement on their own. They're professionals who speak the same language, and they can usually find a middle ground based on the facts. If they agree, the dispute is settled. But what if they’re at a deadlock?

That's when an "umpire" steps in.

If the two appraisers can't agree, they will together select a neutral third-party expert to act as a tie-breaker. The umpire reviews the reports from both sides and makes a final call. The decision is settled as soon as any two of the three parties agree on a number.

This simple diagram shows how the process flows.

This structure guarantees a resolution, so you're not stuck in a never-ending argument with the insurance company.

The Costs and the Final Decision

It's important to know what you're getting into, both financially and legally. Here’s a quick breakdown of the costs:

- Your Appraiser: You pay for the expert you hire.

- Insurer’s Appraiser: The insurance company pays for their own.

- The Umpire: If one is needed, you and the insurer split the cost 50/50.

Yes, there's an upfront cost to you, but a good appraisal can add thousands of dollars to your final settlement, making it a worthwhile investment. For a deeper dive, you can learn more about what is the appraisal clause and see how it plays out in real scenarios.

Remember, the outcome of the appraisal is legally binding. You can't just try again if you don't like the number. This is why it is absolutely critical to hire a skilled, experienced appraiser right from the start. You really only get one shot to get this right.

Total Loss vs Diminished Value Appraisals

After a car accident, you'll hear insurance adjusters throw around terms like "total loss" and "diminished value." While they both involve your car's worth, they represent two completely different financial battles. Getting them straight is critical, because confusing them can cost you thousands.

An auto insurance appraisal is your key weapon in both fights, but how you use it depends entirely on the type of loss you're trying to prove.

A total loss is pretty straightforward: your car is so badly damaged that the cost to fix it is more than it's worth. The insurance company decides to "total it out" and, in theory, pays you its Actual Cash Value (ACV) right before the crash. This is where the first fight usually begins.

A diminished value claim, on the other hand, comes into play after your car is repaired. Even with the best bodywork, your car now has an accident on its record. That history permanently torpedoes its resale value, and an appraisal is used to calculate exactly how much money was lost.

The Total Loss Appraisal Fight for Fair ACV

When your insurer declares your car a total loss, their first offer is just that—an offer. It's almost always a lowball number spit out by valuation software designed to save them money, not make you whole.

This initial offer rarely accounts for the real world. It might ignore recent upgrades you made, the excellent condition you maintained, or the high demand for your specific model in your local area. An independent auto insurance appraisal is how you fight back against their low figure.

A good appraiser doesn't just pull numbers from a database. They build a solid case for your vehicle's true pre-accident worth by:

- Pinpointing what identical vehicles have actually sold for in your immediate market.

- Documenting your car's specific condition, mileage, and any special features.

- Accounting for recent major maintenance or valuable upgrades you've invested in.

This process forces the conversation away from the insurer's low estimate and toward the reality of what it would cost you to replace your car today. If you're struggling with the adjuster's numbers, our guide on how to read a total loss estimate can help you make sense of their report.

An insurer's ACV offer is an opening bid, not a final number. An independent appraisal provides the hard evidence you need to negotiate a fair, market-based settlement.

It's no surprise that disputes over vehicle value leave a bad taste in people's mouths. In fact, 57% of auto insurance customers went shopping for a new provider last year—the highest rate ever recorded in a 19-year study. A huge driver for this was frustration over claims and appraisals. You can explore more about these customer satisfaction trends on J.D. Power's website.

Understanding Diminished Value: The Hidden Loss

Diminished value is the financial loss that insurers often hope you never learn about.

Let me put it this way: imagine two identical used cars on a lot. Same make, model, year, and mileage. One has a squeaky-clean vehicle history report. The other was in a major collision but has been perfectly repaired. Which one are you buying? And more importantly, which one would you pay more for?

That price gap is diminished value. Even with flawless repairs, the stigma of an accident permanently drags down what a smart buyer is willing to pay. An appraisal for diminished value calculates this specific loss, which you are legally entitled to recover from the at-fault driver's insurance company.

To help you get a clearer picture of these two claim types, here’s a quick breakdown.

Total Loss vs Diminished Value at a Glance

| Feature | Total Loss Appraisal | Diminished Value Appraisal |

|---|---|---|

| When It Applies | Your car is deemed "totaled" and will not be repaired. | Your car has been repaired after an accident. |

| Goal of Appraisal | To determine the car's true market value before the crash. | To calculate the loss in resale value after repairs. |

| What You Recover | The Actual Cash Value (ACV) to replace your vehicle. | Compensation for the permanent drop in your car's market worth. |

| Common Disagreement | The insurer offers a low ACV based on their software. | The insurer denies the claim or offers a minimal amount. |

| Who Pays the Claim | Typically your own insurance (if you have collision coverage). | The at-fault party's insurance. |

This table simplifies the core differences, but there are a few nuances to diminished value itself.

There are three key types you should know:

- Immediate Diminished Value: The instant drop in value the moment the accident happens, before any repairs are even considered.

- Inherent Diminished Value: This is the most common type of claim. It's the loss in value that still exists even after your vehicle has been repaired to the highest standard.

- Repair-Related Diminished Value: This is an extra loss in value caused by shoddy repair work, like mismatched paint, cheap aftermarket parts, or lingering mechanical issues.

An expert appraiser can document this loss with real-world market data, giving you the ammunition you need to prove your claim and get the compensation you deserve.

Finding and Hiring an Independent Appraiser

When you decide to invoke the appraisal clause, your single most important move is choosing the right independent appraiser. This person is your champion in the ring—the expert who will build the undeniable case for your vehicle's true value. Getting this choice right isn't just a box to check; it’s the cornerstone of your entire claim.

Think of it like this: if you were facing a complex legal battle, you wouldn’t hire just any lawyer. You’d find a specialist with a proven track record in your specific type of case. An experienced auto insurance appraisal expert is no different and can mean the difference between accepting a lowball offer and getting what you're rightfully owed.

Where to Look for a Qualified Appraiser

Finding a truly independent and skilled appraiser means looking beyond a quick Google search. You need someone with real credentials and a reputation for fighting on behalf of policyholders—not someone who plays nice with the insurance companies.

Your best bet is to start with trusted industry organizations. These groups maintain directories of certified professionals who are held to strict ethical codes and high standards of practice.

- The Bureau of Certified Auto Appraisers (BOCAA): A top-tier organization that certifies appraisers specifically for vehicle valuation.

- The American Society of Appraisers (ASA): This group offers demanding accreditation programs across many fields, including the machinery and technical specialties relevant to auto appraisals.

- The International Automotive Appraisers Association (IAAA): Another highly respected body providing training and certification for automotive appraisal professionals.

These associations are great starting points because their members have already been vetted. Resources that show you how to find an independent auto appraiser near me can also offer some excellent localized advice.

Vetting Your Potential Appraiser

Once you have a shortlist, it’s time to dig in and vet them properly. Not all appraisers bring the same level of skill to the table. You’re looking for a combination of deep technical knowledge, years of hands-on experience, and a history of successful negotiations.

Look for key certifications that prove they understand the nuts and bolts of vehicle construction and repair. I-CAR (Inter-Industry Conference on Auto Collision Repair) and ASE (Automotive Service Excellence) certifications are gold standards, showing an appraiser truly gets the complexities of modern vehicles and collision damage.

A truly independent appraiser’s loyalty is to the evidence and the facts of your vehicle’s value, not to any insurance company. Their entire business model should be based on providing unbiased, accurate valuations for consumers.

Before you hire anyone, get them on the phone and treat it like a job interview. This is your chance to really feel out their expertise and make sure they're the right person to have in your corner.

Key Questions to Ask a Potential Appraiser

Don’t go into that call unprepared. Have a list of specific questions ready to help you understand their background and how they work. A confident, competent appraiser will welcome your questions and give you straight answers.

- How many auto insurance appraisal cases have you handled? You want someone who lives and breathes this stuff, not someone who just dabbles in it.

- Have you worked on cases involving my specific insurance company before? Knowing the other side’s playbook is a huge advantage.

- What is your fee structure? Reputable appraisers almost always charge a flat fee, not a percentage. Be wary of anyone whose pay depends on the outcome—that’s a serious conflict of interest.

- Can you provide a sample of a past appraisal report? A solid report is much more than a printout from a valuation tool. It should be detailed, well-researched, and packed with hard market data.

Keep an eye out for red flags. If someone guarantees a certain outcome, pressures you to sign immediately, or gets defensive about your questions, walk away.

Arming Your Appraiser with Evidence

After you’ve hired your expert, your next job is to give them all the ammunition they need to build an ironclad case. The more proof you can provide about your vehicle's pre-accident condition, the stronger their report will be.

It’s time to become a detective. Dig up every document and piece of information you can find. This paperwork helps paint a complete picture of your vehicle's unique story and value, allowing your appraiser to justify a higher number.

Essential Documents to Provide:

- Maintenance Records: Every oil change, tire rotation, and service record shows you took meticulous care of your vehicle.

- Receipts for Upgrades: Did you add a premium sound system, performance tires, or a custom roof rack? Those receipts are proof of added value.

- Pre-Accident Photos: Recent pictures of your car looking its best are powerful visual evidence that's hard to argue with.

- Original Bill of Sale and Window Sticker: These documents are the blueprint of your car, detailing every factory option and package it came with.

By providing this file of evidence, you empower your appraiser to craft a report so detailed and persuasive that the insurance company simply can't ignore it. This preparation is your final, critical step in the journey to getting the fair settlement you deserve.

Common Mistakes to Avoid During the Appraisal

Knowing the steps to take in an appraisal is only half the battle. The other half is knowing which pitfalls to sidestep. It’s easy to feel overwhelmed and rush through the process, but a few common mistakes can end up costing you hundreds, if not thousands, of dollars.

Think of it as navigating a minefield. By knowing where the dangers lie ahead of time, you can plot a much safer course to the settlement you deserve. Let's walk through the most common traps and how to avoid them.

Instantly Accepting the First Offer

Here’s a hard truth: the insurance company’s first offer is almost never its best. It’s a starting point, a number their software generated to protect their bottom line, not yours. If you accept it just to get things over with, you're likely leaving a significant amount of money on the table.

Treat that initial figure as what it is—an opening bid. This is your cue to bring in the heavy hitter: your auto insurance appraisal. It gives you the concrete, market-based evidence you need to push back against a lowball offer and show them what your vehicle is really worth.

A verbal promise from an adjuster has no legal standing. If an agreement isn't documented in writing, it effectively doesn't exist. Always follow up phone calls with an email summarizing what was discussed to create a paper trail.

Failing to Get Everything in Writing

You'll probably talk to several different people at the insurance company, and while they might sound friendly and reassuring on the phone, a verbal agreement isn't worth the paper it isn't printed on. If a dispute pops up later, any promise made over the phone might as well have never happened.

Make it a habit to document everything. After a phone call, send a quick email summarizing the conversation and any agreements made. This simple step creates a paper trail that holds everyone accountable and protects you from "he said, she said" arguments down the road.

Hiring an Unqualified or Biased Appraiser

Choosing the right appraiser is just as crucial as deciding to get one in the first place. Not all appraisers are created equal, and hiring the wrong one can completely undermine your claim. Some have cozy relationships with insurance companies, while others simply lack the right credentials to produce a solid, defensible report.

An appraiser without proper certifications (like I-CAR or ASE) might create a valuation that falls apart under the slightest pressure. Before you hire anyone, do your homework:

- Check their credentials and experience.

- Ask to see sample reports.

- Confirm they work for a flat fee, not a percentage of the settlement.

A biased or unqualified appraiser is a waste of money and time. You need a true, independent expert on your side.

Overlooking the Impact of New Technology

The insurance world is changing fast, and technology is at the heart of it. Insurers are using more data and analytics than ever to assess claims, from telematics data in usage-based insurance (UBI) to automated appraisal systems. Ignoring these trends means you might not understand how your insurer is arriving at their figures.

Staying informed about how the industry operates helps you anticipate their moves. For a deeper dive into what's on the horizon, check out these 2025 insurance developments and trends on IRMI.com.

So, the experts have weighed in, the evidence has been scrutinized, and a final value for your car is on the books. The toughest part of your auto insurance appraisal is behind you. But what's next? Knowing the final few steps will help you smoothly wrap up the claim and get your settlement.

Once the appraisers—and the umpire, if one was needed—sign the official award document, that number becomes legally binding. This isn’t a suggestion; it’s the final word. Both you and the insurance company are contractually required to honor it.

Getting Your Settlement

With the binding award in hand, the insurance company gets to work processing the final claim paperwork based on the new value. The dispute is over, and now it's all about getting you paid.

Here’s how the last few pieces fall into place:

- The Check is Cut: The insurer must issue payment for the award amount, less your policy's deductible. You can typically expect this check within a few days to a week after they receive the official award.

- Paying Your Expert: Your independent appraiser works for you, so their fee is your responsibility. Most people simply use a small portion of their increased settlement to cover this cost, making it a worthwhile investment.

- Closing the Claim: Once you've received the settlement and paid your appraiser, the claim is officially closed. Done.

This is the moment your hard work pays off. The appraiser's valuation turns into actual money you can use to get back on the road.

Remember, the appraisal award is the final word on your vehicle's value. It brings the back-and-forth to a definitive close and sets the settlement amount in stone.

Moving On: What to Do with Your Car and Your Check

The very last step depends on why you filed the claim in the first place—was it a total loss, or was it for repairs and diminished value?

If your vehicle was totaled, you'll need to sign the title over to the insurance company. They'll then arrange to pick up the vehicle, and your settlement check is their payment for it.

If your vehicle was repaired, the settlement check is yours. It's meant to cover any outstanding repair costs and, importantly, compensate you for the loss in value your car suffered. You can finally close the book on this whole ordeal, knowing you didn't settle for a lowball offer. You stood your ground and got a fair outcome backed by solid evidence.

Still Have Questions? Let's Clear Things Up

Even after walking through the process, it's natural to have a few more questions pop up. Here are some of the most common ones we hear from car owners, along with straightforward answers to help you navigate your claim.

How Much Does an Independent Auto Appraisal Cost?

You can expect to pay anywhere from $300 to $800 for a high-quality, independent appraisal. The exact cost really depends on the specifics of your situation—things like whether it's a total loss or a diminished value claim, the complexity of the damage, and the appraiser's experience.

It’s easy to get sticker shock, but try to see it as an investment rather than a cost. Spending a few hundred dollars to potentially increase your settlement by thousands is a smart financial move. Just make sure you get a firm quote in writing before you agree to anything.

Can I Use the Appraisal Clause If the Other Driver Was At Fault?

Yes, you can, but how you approach it changes. The appraisal clause is part of the contract between you and your insurance company, so you can't force the at-fault driver's insurer into it directly.

That said, you have a couple of solid options:

- Negotiate with their insurer: You can still hire your own appraiser. You'll use their detailed report as undeniable proof to challenge the other company's lowball offer.

- File with your own insurer: This is often the smoothest path. File the claim under your own collision coverage, then invoke the appraisal clause with your company. Once they pay you a fair amount, they will go after the at-fault driver's insurance to get their money back through a process called subrogation.

Your insurance company has a contractual duty to honor the appraisal clause in your policy. If they refuse, they could be acting in bad faith, which gives you a powerful advantage.

What if My Insurer Refuses to Participate in the Appraisal?

If the appraisal clause is in your policy (and it's required in many states), your insurer is legally obligated to play ball. A flat-out refusal is a major red flag and likely a breach of contract.

If you find yourself in this situation, your first step is to send a formal demand letter by certified mail. In it, you'll want to point directly to the appraisal section of your policy. If they still won't budge, it's time to escalate. File a complaint with your state's Department of Insurance and seriously consider talking to an attorney who specializes in insurance bad faith claims to protect your rights.

When you're dealing with a total loss or diminished value claim, you need an expert on your side. Total Loss Northwest delivers certified, independent appraisals that give you the leverage to demand what you're rightfully owed. Don't let the insurance company dictate your settlement—get the proof you need. Learn more at https://totallossnw.com.