Hearing your car is a "total loss" is a gut punch. It’s stressful, confusing, and immediately raises a ton of questions. The most important one? "What was my car actually worth?"

A car total loss value calculator is your first step toward an answer. It helps you get a handle on the Actual Cash Value (ACV) of your vehicle—the number that truly matters when the insurance company makes you an offer. Think of it as your own independent estimate, a powerful starting point for making sure you're treated fairly.

What a "Total Loss" Really Means

When your insurer says your car is a total loss, they're not just commenting on how bad the damage looks. They’ve run the numbers, and it's a purely financial decision.

Simply put, they've determined that the cost to fix your car is more than the car is worth to them. This decision pivots on something called the total loss threshold. It’s a specific percentage of your car's value, and once the repair bill crosses that line, the car is officially "totaled."

Understanding the Total Loss Threshold

Every state has slightly different rules, and insurance policies can vary, but there's a common industry standard. Most insurers will declare a car a total loss when the repair costs are somewhere between 70% to 80% of its pre-accident Actual Cash Value (ACV).

Let's say your car's ACV was calculated at $15,000. If the body shop comes back with a repair estimate of $10,500 (which is 70% of $15,000), the insurance company will almost certainly write it off. To learn more about how insurers determine these values, you can find great information on autoclaimconsultants.com.

It’s just a business calculation. Spending $12,000 to fix a car that was only worth $10,000 doesn't make financial sense for them.

Defining Actual Cash Value (ACV)

The entire settlement process comes down to one core concept: Actual Cash Value, or ACV. This isn't what you originally paid for the car, and it's definitely not what a brand-new one would cost today.

ACV is the fair market value of your vehicle the instant before the crash happened. It's a snapshot that takes everything into account—depreciation due to age, mileage, wear and tear, and its overall condition.

Imagine what a private buyer in your local area would have reasonably paid for your specific car in its pre-accident state. That's the ACV. Getting this number right is absolutely critical because it’s the foundation for the check you’ll receive. Every negotiation starts and ends with ACV, so you need to be confident it's accurate.

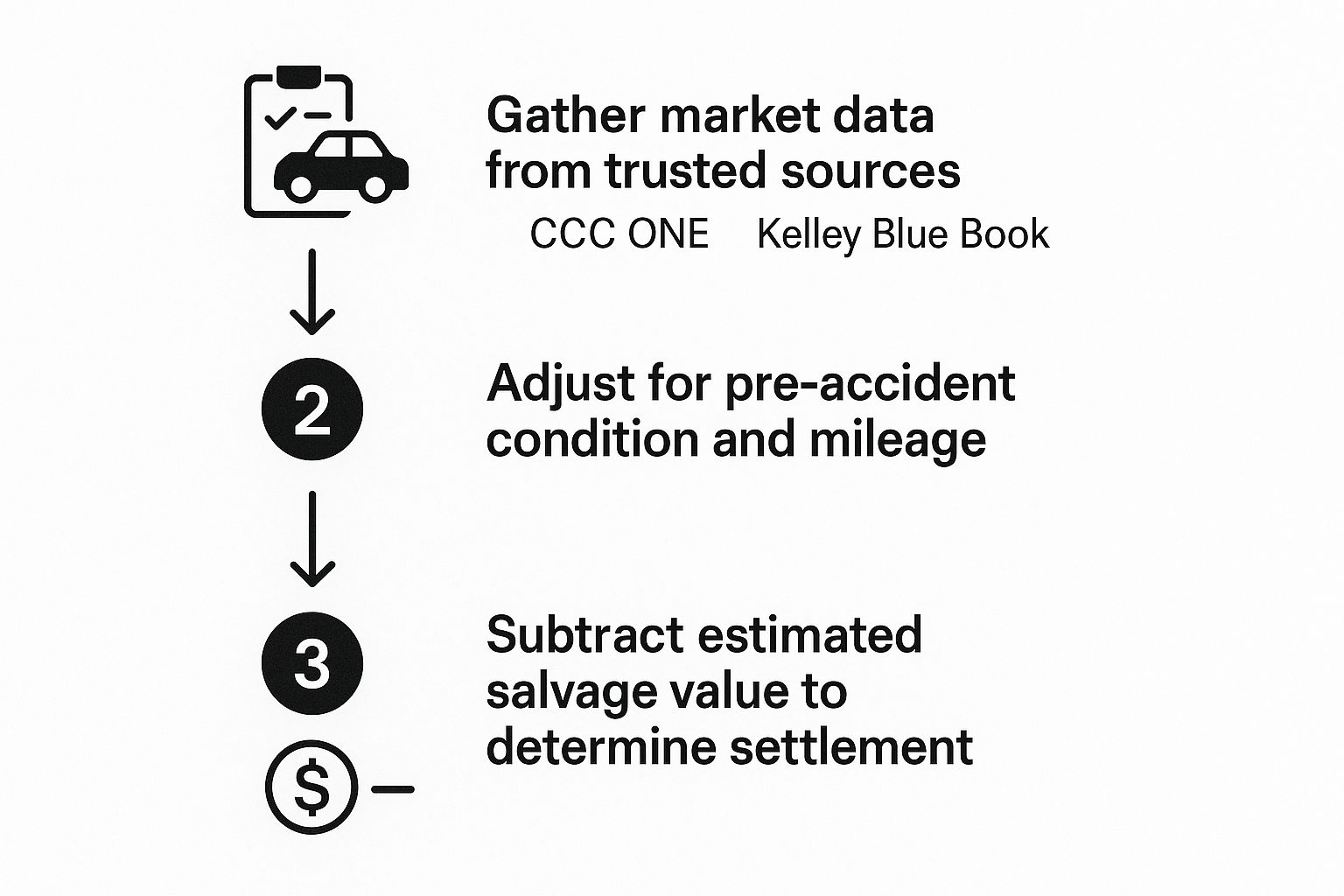

How Insurance Companies Calculate Your Car's Value

When an insurance adjuster hands you a settlement offer, that number can feel like it came out of nowhere. It’s not a guess, though. It’s the result of a very specific, data-driven process designed to pinpoint your car’s Actual Cash Value (ACV)—what it was worth the moment before the accident.

Insurers don’t pull these figures from a hat. They rely on massive databases and standardized formulas, subscribing to third-party valuation services like CCC ONE or Mitchell. These platforms crunch data from local dealerships, private party sales, and auction results to establish a baseline value for a vehicle of the same year, make, and model right in your area.

But that’s just the starting point. The real work begins when they start adjusting that baseline to match your specific car.

The Core Valuation Formula

At its heart, the process is about calculating the ACV and then subtracting the vehicle's potential salvage value. This is the math that determines if your car is officially a "total loss."

Insurance adjusters work from a simple but powerful formula: ACV minus Salvage Value. For example, if your car's ACV before the crash was $15,000 and its salvage value (what it's worth for parts) is $3,000, the insurance company sets the total loss threshold at $12,000. If the mechanic's repair estimate tops that $12,000 figure, the car is declared totaled.

It all comes down to what's more cost-effective for the insurer. This calculation tells them whether it's cheaper to pay for repairs or just cut you a check for the car's pre-accident value.

This graphic breaks down the key steps an insurer follows when plugging your vehicle's details into a car total loss value calculator.

As you can see, the process funnels down from broad market data to the specific, unique details of your car's history and condition.

Key Factors That Adjust Your ACV

Your car isn't just a line item in a database. Its unique characteristics will either raise or lower the final settlement offer you receive.

Let's break down the main components that insurance companies scrutinize when determining your vehicle's pre-accident value.

Key Factors Influencing Your Car's Actual Cash Value (ACV)

| Valuation Factor | How It Impacts Your Settlement Value | Example |

|---|---|---|

| Mileage | One of the biggest drivers of depreciation. Significantly lower-than-average mileage for its year will increase the value, while high mileage will decrease it. | A 5-year-old car with 30,000 miles is worth more than the same model with 90,000 miles. |

| Pre-Accident Condition | Adjusters assign a condition rating (Excellent, Good, Fair, Poor). A well-maintained, clean car justifies a higher rating and a better offer. | Providing maintenance records or recent photos can prove your car was in "Excellent" condition, not just "Good." |

| Optional Features | Factory-installed upgrades add value. This includes everything from a sunroof and leather seats to premium sound systems and advanced safety packages. | A "Touring" or "Limited" trim package will have a higher ACV than the base model of the same car. |

| Regional Demand | The value of a vehicle can change based on your location. Local market demand plays a significant role in determining what a car is worth. | A 4×4 truck is typically worth more in a snowy, rural area than in a dense city with mild weather. |

These are the core elements, and it's crucial that the insurer's initial report accurately reflects them. Your job is to ensure their interpretation aligns with the true state of your vehicle right before the accident happened.

For a deeper dive into how these elements come together, check out our guide on what is the actual cash value of my car.

And when it comes to high-end vehicles, the details become even more granular. Understanding the factors influencing luxury car valuations can give you some useful context on how brand reputation and premium features can dramatically swing the final number. At the end of the day, every detail matters.

Getting Every Penny You Deserve: How to Prove Your Car's True Value

Here's something you need to understand right away: the first settlement offer you get from an insurance adjuster is just that—an offer. It’s the opening line in a negotiation, not the final word. Their number is based on broad data, but it almost never accounts for the specific details and care that made your car worth more.

This is your opportunity to step in and make a real difference in your payout. Your job is to build a case proving your car was in better-than-average shape just before the crash. Every receipt, every photo, and every record you can find helps paint a more accurate picture of your car’s actual value, giving you the leverage to counter the insurer's lowball starting point.

Build Your Evidence File: Documenting Condition & Upgrades

The adjuster never saw your car on a good day, so you have to show them what they missed. It's time to do some digging for anything that proves the value you know your car had. These details, which seem small on their own, can collectively add up to hundreds or even thousands of dollars on your final check.

Start pulling together a dedicated file with these crucial documents:

- Maintenance Records: Every oil change, tire rotation, and scheduled service appointment is proof of a well-maintained vehicle. This is your best weapon against the adjuster's default assumption that your car was just in "average" condition.

- Proof of Recent Purchases: Did you buy a brand-new set of tires a few months back? What about a new battery or brakes? Those receipts are hard evidence that you were investing money into the car, increasing its value right before the accident.

- Aftermarket Add-ons: Don't forget any upgrades you made. Receipts for a new sound system, custom wheels, a high-end roof rack, or even a remote starter all need to be included. These are almost always missed in an initial valuation.

And don't underestimate the power of photos. If you have any recent pictures of your car looking clean and cared for, they are invaluable. A clear shot of a spotless interior or a gleaming, wax-finished exterior can speak volumes.

My Advice: Don't just dump a pile of papers on the adjuster. Organize everything neatly in a folder or a single PDF. Label each receipt and photo, and maybe even create a one-page summary sheet. When you make their job easier, they're often much more willing to see things your way.

Find Your "Comps": The Power of Local Market Data

The single most effective tool you have for negotiation is real-world data. The insurance company is using "comparables" (or comps) to justify their offer, and you need to do the same. The goal is to find vehicles just like yours currently for sale in your local area.

Your comps should be a close match to your car’s:

- Year, make, and model

- Trim level (e.g., LX, EX, Touring)

- Mileage (try to stay within a 10-15% range)

- Overall condition

Go beyond a single source. Scour the websites of local dealerships, browse online marketplaces like Autotrader, and check private listings. Take screenshots of every good match, making sure the asking price is clearly visible.

If you can present the adjuster with 3 to 5 solid local comps priced higher than their offer, you've completely changed the conversation. You’re no longer arguing about their database; you're talking about the real-world, local market where you would have had to replace your vehicle.

Navigating Payout Problems and Loan Balances

https://www.youtube.com/embed/j7pd-SuUI_Y

A total loss is stressful enough, but it gets a whole lot more complicated when you still owe money on the car. Here’s a hard truth many people learn too late: the insurance company’s payout is based on your vehicle's Actual Cash Value (ACV), not your loan balance. This disconnect can leave you in a serious financial bind if you're "upside down" on your loan.

Being upside down, or having negative equity, simply means you owe your lender more than what your car is currently worth. When the insurance check arrives, it might not be enough to clear the loan. You could be left with a hefty bill for a car that’s sitting in a salvage yard.

This gap is a frustratingly common problem. It’s critical to get your head around how this happens and what your options are before the settlement offer even hits your inbox.

The Math Behind Being Upside Down

Let's look at a real-world scenario to see exactly how this plays out. Say you bought your car a couple of years ago and you still owe $18,000 on your auto loan.

After the accident, the insurance adjuster runs their numbers and decides your car’s ACV is $15,000. On top of that, you have a $1,000 collision deductible.

Here’s the breakdown:

- Actual Cash Value (ACV): $15,000

- Your Deductible: -$1,000

- Final Insurance Payout: $14,000

The insurance company will likely send that $14,000 check straight to your lienholder. But the bank is still owed $18,000. That leaves a $4,000 difference that you are on the hook for, and you'll have to pay it out of your own pocket.

This shortfall is the core financial challenge many face. A key issue arises when the payout does not cover the outstanding loan balance, and without gap insurance, consumers remain liable for paying off a car loan even if the vehicle is totaled. You can discover more insights about this common insurance situation on insurify.com.

Bridging the Gap with GAP Insurance

This is precisely the situation where Guaranteed Asset Protection, better known as GAP insurance, proves its worth. If you have this optional coverage, it’s designed to step in and handle this exact problem.

GAP insurance covers the difference—the "gap"—between what the insurance company pays out and what you still owe the lender. In our example, it would cover that $4,000 shortfall, saving you from a significant financial hit.

This kind of protection is especially crucial for drivers who:

- Made a small down payment (less than 20%)

- Financed their car for a long term, like 60 months or more

- Rolled negative equity from a previous trade-in into their current auto loan

If you find yourself facing a total loss, the very first thing you should do is dig up your auto loan paperwork to see if you purchased GAP insurance. It’s often sold by the dealership when you buy the car, but it can also be added through your auto insurer. It can single-handedly turn a financial disaster into a manageable bump in the road. And if the settlement offer seems too low, it's always smart to learn how to negotiate a total loss settlement to close that gap as much as possible.

Using an Online Calculator to Get a Fair Estimate

You don't have to sit around waiting for the insurance adjuster's report to figure out what your car was worth. Honestly, one of the smartest things you can do right now is get your own independent estimate. Using a car total loss value calculator online gives you a solid benchmark to work from.

This isn't just about getting a number. This figure becomes your anchor point for the entire negotiation. When that official settlement offer finally comes in, you’ll have a reliable, data-backed value to compare it against. It’s the easiest way to spot a lowball offer from a mile away.

Choosing the Right Valuation Tools

Not all online car estimators are built the same. If you want a number that holds water, you need to stick with established, reputable sources that everyone in the auto industry recognizes.

Here are the big three I always recommend:

- Kelley Blue Book (KBB): Probably the most famous name in the game. KBB’s tool is great because it gets really specific, letting you plug in your exact trim level and all the optional features.

- Edmunds: Another industry heavyweight. Edmunds gives you a "True Market Value" (TMV), which is a fantastic metric because it reflects what people in your actual area are paying for cars just like yours.

- NADAguides: This is the one many banks, credit unions, and dealerships rely on. Getting a valuation from NADA adds another powerful layer of credibility to your research.

My advice? Run your car's details through at least two, if not all three, of these tools. This gives you a realistic range. For example, if all three sources put your car's value somewhere between $14,500 and $15,200, you can be pretty confident that an insurer's offer of $12,000 is way off the mark.

Tips for an Accurate Online Estimate

The old saying "garbage in, garbage out" is especially true here. The accuracy of any online calculator depends entirely on how accurate you are with the details.

First off, you have to be brutally honest about your car’s pre-accident condition. I know it’s tempting to click "Excellent," but that category is truly reserved for flawless, showroom-quality vehicles. Most cars that are driven daily fall into the "Good" or "Very Good" categories. Picking the right one keeps you from getting an inflated estimate that the adjuster will immediately dismiss.

Be ready to back up your condition rating. If you claim your car was in "Very Good" condition, have maintenance records and recent photos on hand. That documentation turns your opinion into a provable fact.

Next, get granular with the optional features. If you still have the original window sticker, dig it out. Did you have a sunroof? Leather seats? The upgraded sound system or that fancy tech package? Every single one of those adds value, and they're exactly the kinds of details adjusters might "forget" to include. For a closer look at how these elements are valued, check out this detailed guide on using a car value after accident calculator.

And one last crucial tip: always select the option for "private party value." This number represents what an individual buyer would have paid for your car. It’s almost always higher than the "trade-in value" and is the figure that most closely aligns with the actual cash value (ACV) your insurer is supposed to pay.

Common Questions About Total Loss Claims

When your car is declared a total loss, your mind starts racing with questions. The whole process can feel overwhelming and confusing, but getting straight answers is the first step toward getting through it. Let's break down some of the most common things people worry about when they're in this situation.

Can I Negotiate the Insurance Payout Offer?

Yes. Not only can you, but you absolutely should. Think of the insurance company's first offer as a starting point for a conversation, not the final word. Their number is based on their internal data, which often misses the unique details that made your car valuable.

If that initial offer feels too low, don't just accept it. The first thing you need to do is ask for a detailed copy of their valuation report and go over it with a fine-tooth comb. Are the mileage, features, and condition listed correctly? Even small errors can make a big difference.

Then, it's time to build your own case. This is where your homework pays off.

- Find comparable vehicles (same make, model, year, and similar condition) for sale in your local area. This shows the real-world market value right where you live.

- Dig up receipts for any recent work or upgrades. Did you just put on new tires? A new battery? Those add value.

- Get independent valuations from trusted sources like Kelley Blue Book or Edmunds.

Once you have your evidence, present it to the adjuster calmly and professionally. A counteroffer backed by solid proof is always more effective than an emotional reaction.

What Happens If I Want to Keep My Totaled Car?

In many cases, you can choose to keep your vehicle. This is called owner retention. If you go this route, the insurance company calculates your payout differently. They'll give you the car's actual cash value (ACV), but then they subtract your deductible and the car's salvage value.

So, what’s the salvage value? It’s the amount the insurer expected to get by selling your wrecked car to a salvage yard. By keeping the car, you're essentially buying it back from them for that amount.

Heads Up: If you retain your car, the state will issue it a "salvage title." This title brand makes the car much harder to insure and sell down the road. You’ll also be on the hook for all repairs needed to make it safe to drive again, which typically requires a thorough state inspection before it can be legally back on the road.

How Long Does a Total Loss Settlement Take?

While every claim is a bit different, most total loss settlements wrap up in about 30 days. This timeframe covers everything from start to finish.

The process really kicks off after the vehicle has been inspected and officially declared a total loss. From there, the insurer does its valuation research, puts together the settlement offer, and then you have the negotiation phase.

One of the best things you can do to keep things moving is to stay organized. Have your paperwork ready and respond quickly to any requests from the adjuster. The more you can do to streamline your side of the process, the faster you’ll get to a final agreement.

If you're dealing with a total loss and the insurance company’s offer just doesn't add up, you don't have to take it. At Total Loss Northwest, we provide independent, certified auto appraisals to establish your vehicle's true market value. We invoke the Appraisal Clause in your policy to make sure you get the fair settlement you're entitled to. Learn more about how we can help you fight for a fair payout.