Insuring a classic car isn't like insuring your daily driver. The requirements are totally different because the entire philosophy behind the coverage is different. Insurers focus on three core things: an agreed value, secure storage, and limited use. It’s a specialized approach because you're not just protecting a mode of transportation—you're preserving a valuable, often appreciating, asset.

Why Your Classic Car Needs Specialized Insurance

Trying to cover a classic car with a standard auto policy is a huge mistake. It's like putting a cheap, plastic frame on a priceless painting. Sure, it's technically "covered," but you're leaving your investment dangerously exposed.

A regular policy is built for cars that depreciate. The moment you drive a new car off the lot, it starts losing value. That's why these policies use "actual cash value," which means they'll pay you what your car was worth right before the accident, factoring in depreciation.

This is the exact opposite of what you need for a classic. Your car is an investment, a piece of automotive history that likely gains value over time. That's why genuine classic car insurance is built around an "agreed value." This is a number you and the insurance company settle on upfront. If your car is ever declared a total loss, you get that full, predetermined amount. No haggling, no arguments about depreciation. The value is locked in from day one.

To get a quick sense of the differences, here’s a simple breakdown.

Standard vs Classic Car Insurance At a Glance

| Feature | Standard Auto Insurance | Classic Car Insurance |

|---|---|---|

| Valuation Basis | Actual Cash Value (depreciates) | Agreed Value (appreciates/stable) |

| Primary Use | Daily driving, commuting | Pleasure use, shows, events |

| Mileage Limits | Typically unlimited | Restricted (e.g., 2,500-7,500 miles/year) |

| Storage | No specific requirements | Requires secure, enclosed storage |

| Cost | Generally higher | Often significantly lower |

As you can see, the policies are designed for completely different purposes and owner lifestyles.

Understanding the Core Protections

To offer this kind of specialized coverage, insurers have a few ground rules. Think of it as a partnership. You promise to be a responsible caretaker of the vehicle—keeping it safe and using it carefully—and in return, they provide coverage that truly reflects its worth.

This approach is more important than ever. The classic car market is booming, with the global classic car insurance sector valued at nearly USD 31 billion in 2022. It's projected to climb past USD 51 billion by 2029, a surge fueled by the rising value of these beautiful machines. You can dig into the numbers and see how market trends are shaping the industry by reading detailed industry reports. This growth just underscores why getting the right policy is critical.

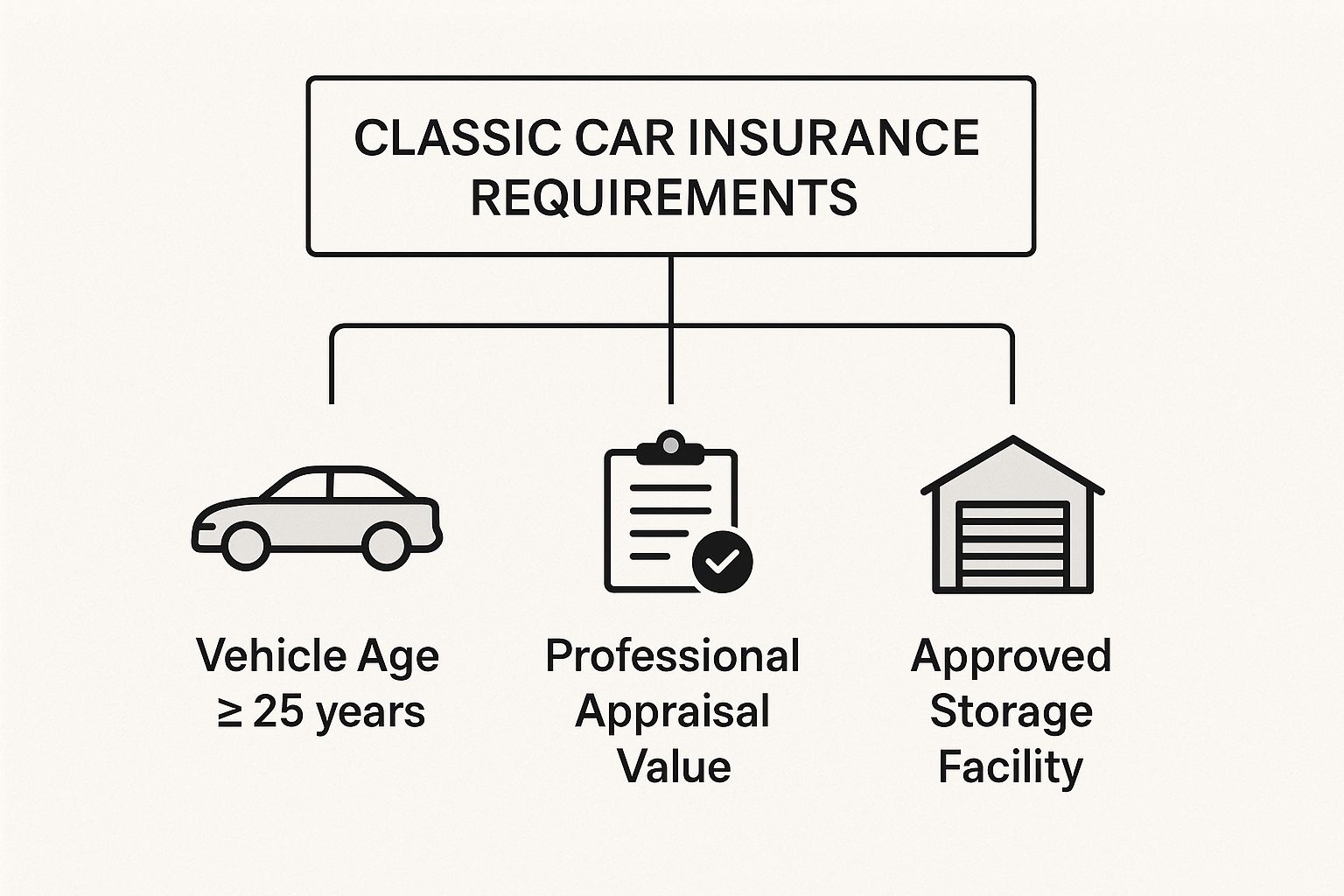

This image really breaks down the three pillars that all classic car policies are built on.

As you can see, it all comes down to the car's age and type, a professionally verified valuation, and proof of proper, secure storage. Get these three things in order, and you're well on your way to securing the right protection.

Meeting the Vehicle Eligibility Requirements

Before you can lock in that all-important agreed value policy, the insurance company needs to be convinced that your car is, in fact, a genuine "classic" by their standards. It's a common misconception that any old car will automatically get the nod for this kind of specialized coverage. In reality, insurers have a pretty specific checklist.

Think of it like getting your car into an exclusive car show. The organizers have rules to maintain the quality of the event, and classic car insurers have their own criteria to make sure they're covering a true collector's item, not just a beat-up daily driver. These rules exist because the entire policy is built around the idea that your car is a prized possession you treat with kid gloves.

The Age and Collectibility Standard

The first hurdle is usually the most straightforward: your vehicle's age. While there isn't one single rule that applies everywhere, most insurers have a clear age window. Generally, a car has to be at least 15 to 25 years old to even be in the running for classic or collector status.

This range can be a bit of a moving target. Some companies might consider a 10-year-old exotic model, while others are much stricter, insisting a car be 25 years old to earn the "antique" label.

But age is only half the story. The car also needs to be collectible. A run-of-the-mill 20-year-old sedan, for instance, probably won't make the cut, even if it's old enough. Insurers are looking for cars that hold their value—or better yet, appreciate—because they're rare, historically important, or just plain desirable to enthusiasts.

Key Takeaway: An eligible vehicle is more than just old; it has to be a recognized collectible. The insurer wants to protect a piece of automotive history, not just an aging form of transportation. This is the core distinction you need to understand.

Condition and Originality Matter

Beyond its age and pedigree, your car’s physical condition will be under the microscope. To qualify, a vehicle needs to be in good to excellent shape. This doesn't mean it has to be a flawless, concours-level showpiece, but it absolutely must be well-maintained, structurally sound, and free of significant rust.

Originality is another huge factor. Insurers tend to favor vehicles that are kept in their original, factory-stock condition. A 1969 Camaro with its numbers-matching engine is a much simpler proposition to insure than one that's been heavily modified. Why? Because original vehicles have a more predictable market value and are seen as being preserved, not just used.

What About Modified Vehicles and Replicas?

So, what if your pride and joy isn't exactly how it left the factory? Plenty of us love modified cars, from hot rods and restomods to high-quality kit cars and replicas. The good news is, you can often get these insured, but you'll need to be prepared for some extra homework.

Insurers willing to cover these unique builds will ask for a mountain of documentation, including things like:

- Detailed Build Sheets: A complete rundown of every modification, the parts used, and any professional labor involved.

- Photo Documentation: Clear, high-quality photos of everything—the engine bay, interior, undercarriage, the works.

- Professional Appraisal: For a modified car, this is almost always non-negotiable. It’s the only way to establish a fair and defensible "agreed value" for a one-of-a-kind vehicle.

Getting a modified classic insured is really about proving the quality and value of the craftsmanship. Without that paper trail, it's nearly impossible for an underwriter to figure out what your car is truly worth, making it a critical step you can't afford to skip.

Understanding Agreed Value vs. Stated Value

Of all the things you’ll need to figure out when insuring your classic, how the insurance company values your car is hands-down the most important. This one detail dictates the exact dollar amount you’ll get back if your pride and joy is stolen or totaled. Getting it wrong can be an absolutely devastating financial mistake.

The two big terms you'll hear are "Agreed Value" and "Stated Value." They might sound like the same thing, but they work in completely different ways. Confusing the two can leave you thousands of dollars short when you need the money most.

The Power of Agreed Value

For any collector vehicle, Agreed Value is the gold standard. It's a simple, straightforward handshake between you and your insurer. You both agree on exactly what your car is worth the day the policy starts. If the worst happens, that agreed-upon number is precisely what you get paid—no ifs, ands, or buts, and no deductions for depreciation.

Think of it as a price tag you both lock in from day one. Let’s say you own a gorgeous 1965 Ford Mustang that you’ve insured for an agreed value of $40,000. If that car gets stolen two years down the road, you get a check for $40,000. That's it. It’s clean, simple, and gives you real peace of mind.

This is crucial because classic cars often go up in value, not down. The classic car market is a serious business. In the UK alone, it’s worth around £757.6 million, with the average insured classic valued at about £12,500. An Agreed Value policy protects that appreciating investment.

The Pitfall of Stated Value

Now, Stated Value is a whole different ballgame—and it's rarely in your favor. With this kind of policy, you "state" what you think your car is worth, but the insurance company only agrees to pay up to that amount.

Here’s the catch, and it’s a big one. They'll pay you the lesser of two numbers: the value you stated, or the car’s Actual Cash Value (ACV) at the moment of the loss. ACV is the same method used for a standard daily driver, and it always factors in depreciation.

Here's how that plays out: You insure that same Mustang for a Stated Value of $40,000. After an accident, the insurer’s adjuster decides its ACV is only $32,000 because of market changes or a few minor dings they found. You get a check for $32,000, not the $40,000 you thought you were covered for.

Securing Your Car’s True Worth

To lock in an accurate Agreed Value, you have to come to the table with proof. This is where a professional appraisal becomes your best friend.

Here’s what a good insurer will want to see:

- A Professional Appraisal: This is the foundation. You need a detailed report from a certified appraiser who truly knows classic cars.

- High-Quality Photos: Don’t skimp here. They’ll want recent, clear shots from every angle—outside, inside, the engine bay, and even the undercarriage.

- A Paper Trail: Have receipts for restoration work, major parts purchases, or any historical documents? That all helps build the case for your car’s value.

The appraisal is key to establishing your car's Fair Market Value, a concept that's central to any valuation discussion. You can get a deeper understanding by reading up on what is fair market value.

Finally, don't just set it and forget it. Your car's value can change. It’s a smart move to review your policy and get an updated appraisal every few years, especially if the market for your model is heating up or you've put more work into it.

Following the Rules for Usage and Storage

One of the biggest reasons classic car insurance is so affordable is that insurers are betting on one simple fact: you aren’t using your prized vehicle for the daily grind. These policies are built around the idea of limited use and secure storage, which dramatically lowers the risk of accidents, theft, and weather damage. Following these rules isn't just a friendly suggestion; it’s the bedrock of your insurance agreement.

Think of it like owning a piece of fine art. You wouldn't hang a priceless painting on your front porch, exposed to the elements. Insurers expect you to be a careful custodian of your classic car in the same way. That means keeping it safe from harm and using it for what it's meant for—pleasure, not picking up groceries or commuting to the office.

Staying Within Your Mileage Limits

The most common rule you'll run into is a hard cap on how many miles you can drive your classic each year. Go over that limit, and you could find yourself in hot water if you need to file a claim.

Most policies offer a few different tiers. You'll typically see annual mileage limits ranging from 5,000 to 10,000 miles, and you can often get a nice little discount for choosing a lower-mileage plan.

Be honest with yourself about how much you'll actually drive. Trying to save a few bucks by picking a limit you know you'll exceed is a risky gamble that could lead to a denied claim down the road.

Secure Storage Is Not Negotiable

Where you park your classic is just as important as how much you drive it. Insurers are almost always rigid on one requirement: the vehicle must be stored in a secure, fully enclosed, and locked location.

This usually means one of these options:

- A Private Garage: A locked garage at your home is the gold standard.

- A Rented Storage Unit: A dedicated, secure storage facility is typically a solid alternative.

- A Secure Carport: Some insurers might give a locked, four-sided carport the nod, but it’s far less common.

Leaving your car parked on the street or in an open driveway overnight is a definite no-go for almost every classic car policy. It's also worth understanding the security standards of different automotive workshop environments, especially if your car will be stored somewhere else during a long restoration project.

Crucial Reminder: If you don't keep your vehicle in the agreed-upon secure location and it gets stolen or damaged, your insurer has every right to deny the claim. This is one of the easiest rules to follow and one of the most expensive to break.

For cars undergoing a long-term restoration that won't see the road for a while, some companies offer "storage-only" or "laid-up" insurance. This is a great option that provides comprehensive coverage against fire, theft, and other damage while it's parked, usually at a much lower rate. If your project car is currently in a million pieces, this is the best way to protect your investment. Just remember, even for a storage claim, having a solid valuation is critical. You can learn more by checking out our guide on understanding total loss appraisals for fair settlements.

Meeting the Driver and Documentation Requirements

It’s not just about the car. When you apply for classic car insurance, the insurance company is just as interested in the person behind the wheel. They want to see that you’re a responsible custodian of a special vehicle, not just another driver.

Think of it like this: the car might get you an invitation to the party, but your own credentials are what actually get you through the door. This part of the process is all about showing the insurer that you’re a low-risk driver who treats your classic as a cherished hobby, not a daily commuter.

Qualifying as a Collector Driver

Insurers have a pretty clear picture of their ideal client, and while the details can differ between companies, most have a few key requirements you'll need to meet personally.

For starters, age and experience matter. Many providers will want you to be at least 25 years old with a solid number of years of driving under your belt. This isn't arbitrary; it's based on reams of data showing that more experienced drivers tend to be safer drivers.

On top of that, a clean driving record is almost always a deal-breaker. If your record is littered with accidents, speeding tickets, or a DUI, you’ll likely be seen as too high of a risk and could be denied coverage outright.

The Daily Driver Rule: This might be the single most important requirement of all. You absolutely must own and insure another vehicle for your everyday use. Be prepared to show proof of a standard auto policy for your daily driver, because this is the insurer's guarantee that your classic is truly just for pleasure.

Assembling Your Application Paperwork

Once you're confident you meet the driver criteria, it's time to get your paperwork in order. Having everything organized and ready to go will make the whole process a lot smoother and faster. Frankly, a well-prepared application file also sends a strong signal to the insurer that you're a serious, organized owner.

Here’s a quick checklist of the documents you'll almost certainly need:

- Proof of Ownership: Have a copy of the car's title and the bill of sale handy.

- Detailed Photographs: They'll want to see the car from every angle. Take clear, recent, high-quality photos of the exterior, interior, engine bay, and even the undercarriage.

- Professional Appraisal Report: If you're getting an agreed value policy (which you should be), a formal appraisal is usually required to lock in the car's value.

- Proof of Primary Insurance: You'll need to provide a copy of the insurance card or declaration page for your daily driver.

- Restoration Receipts: If you've invested in significant restoration work or expensive parts, gather those receipts. They are crucial for justifying the vehicle’s valuation.

Getting these documents together not only proves the value of your car but also reinforces your standing as a responsible owner, checking all the boxes for the insurer.

Your Classic Car Insurance Questions Answered

Diving into classic car insurance can feel a bit overwhelming. Once you get past the basics, a whole new set of questions almost always surfaces. Let’s clear the air and tackle some of the most common things owners ask when trying to lock down the right policy.

Think of this as your go-to FAQ. We'll get into the nitty-gritty of insuring modified hot rods, what really happens if you drive a few too many miles, and more, so you can feel confident you're protecting your pride and joy the right way.

Can I Insure a Modified Classic Car or a Hot Rod?

You bet. Plenty of specialty insurers love working with owners of modified classics, restomods, and hot rods. The key difference is that the paperwork is a lot more involved than for a bone-stock vehicle.

You’ll need to be meticulous about documenting every single modification. This means keeping receipts for parts, invoices for professional labor, and photos of the work. For these one-of-a-kind builds, a professional appraisal is pretty much a requirement. It’s the only reliable way to establish an Agreed Value that truly reflects the time, money, and passion you’ve poured into your custom car.

What Happens If I Exceed My Annual Mileage Limit?

This is one area where you don't want to bend the rules. Exceeding your mileage limit can lead to some serious problems. If you're lucky, your insurer might just bump you into a higher-mileage plan and adjust your premium at renewal time.

But the worst-case scenario is a real nightmare. If you have an accident after you’ve already blown past your annual limit, the insurance company could have grounds to deny your claim entirely. Their argument would be that you breached the policy terms, potentially leaving you on the hook for every penny of the repair—or replacement—cost.

Do I Need a Professional Appraisal?

For a lower-value classic, you might be able to get by without one. But for anything high-value, rare, heavily modified, or particularly unique, a professional appraisal isn't just a good idea—it's essential. An appraisal from a certified expert gives you an objective, rock-solid valuation that becomes the foundation of your Agreed Value coverage.

This little document is your best defense against being underinsured. It also gives the insurance company the confidence it needs to write the policy for the car's true worth. If the unthinkable happens and your car is a total loss, that appraisal becomes your single most important piece of evidence. When facing a total loss claim, it's critical to know how to negotiate your total loss settlement to make sure you get what your car was actually worth.

An appraisal isn't just a suggestion; it's your most powerful tool for proving your car's value. It removes guesswork and ensures your "Agreed Value" policy is built on a solid, factual foundation that protects your financial stake in the vehicle.

Are My Spare Parts and Tools Covered?

In many cases, yes! Most classic car policies offer something called "Spare Parts and Automobilia Coverage." This is specifically designed to cover valuable original parts, specialized tools, and even car-related collectibles that aren't physically on the vehicle.

A standard policy might include a small amount of coverage automatically, maybe $500 to $2,000. If your collection of parts is more extensive or includes rare, date-coded components, you can almost always purchase higher limits. Just be sure to inventory and document what you have.

If you find yourself in a dispute over your vehicle's value after an accident, Total Loss Northwest can help. Our certified appraisers specialize in fighting for the fair settlement you deserve, ensuring your classic, custom, or daily driver is valued accurately. Visit us at https://totallossnw.com to get an expert on your side.