Even after the best body shop in town works its magic, your car has suffered a financial hit that no amount of paint or new parts can fix. This unavoidable drop in what someone will pay for your car later on is called diminished value. It's the simple, frustrating truth that a car with an accident on its record is worth less than one without.

Why Perfect Repairs Don't Restore Full Value

Put yourself in a car buyer's shoes for a moment. You’re at a dealership and find two identical cars—same make, model, year, and even the same color and mileage. They're priced the same, too. But then you pull the vehicle history reports. One is squeaky clean. The other was in a pretty serious wreck a few months back, even though it looks perfect now.

Which one are you buying?

Exactly. Almost everyone would choose the car with no accident history. To move the repaired car off the lot, the dealer has no choice but to slash the price. That price difference? That’s diminished value in a nutshell.

The Three Types of Diminished Value

You'll hear a few different terms thrown around when talking about diminished value. It's helpful to know what they mean, as they each describe the value loss at different stages of the process.

| Type of Diminished Value | What It Really Means |

|---|---|

| Immediate Diminished Value | This is the loss in value that happens the second the accident occurs, even before any repairs are made. It's the difference between the car's pre-accident value and its immediate post-accident, damaged value. |

| Inherent Diminished Value | This is the most common type and the one we focus on. It's the automatic loss in market value because the vehicle now has a permanent accident history, even after it has been fully and properly repaired. This stigma is what deters future buyers. |

| Repair-Related Diminished Value | This is extra value lost due to poor or incomplete repairs. Think mismatched paint, aftermarket parts instead of OEM, or lingering mechanical issues. This is a loss on top of the inherent diminished value. |

While all three exist, inherent diminished value is the core of most claims because it’s a loss you suffer even when the body shop does a flawless job.

The Stigma of an Accident History

The real problem is the permanent black mark on your car’s record. Thanks to services like CarFax or AutoCheck, that accident is now part of your car’s permanent digital history. For any savvy buyer, that history immediately raises red flags:

- Lingering Doubts: Was the frame bent? Are there hidden issues that will pop up later?

- Reliability Worries: Could the accident cause surprise electrical or mechanical problems years from now?

- Future Resale Problems: Buyers know they’ll face the exact same hurdles when they eventually try to sell the car.

At its core, diminished value is all about market perception. A car with an accident history is simply seen as less desirable—and therefore, less valuable—than an identical one without that history. This isn't just a feeling; it's a real, measurable financial loss.

Putting a Number on the Loss

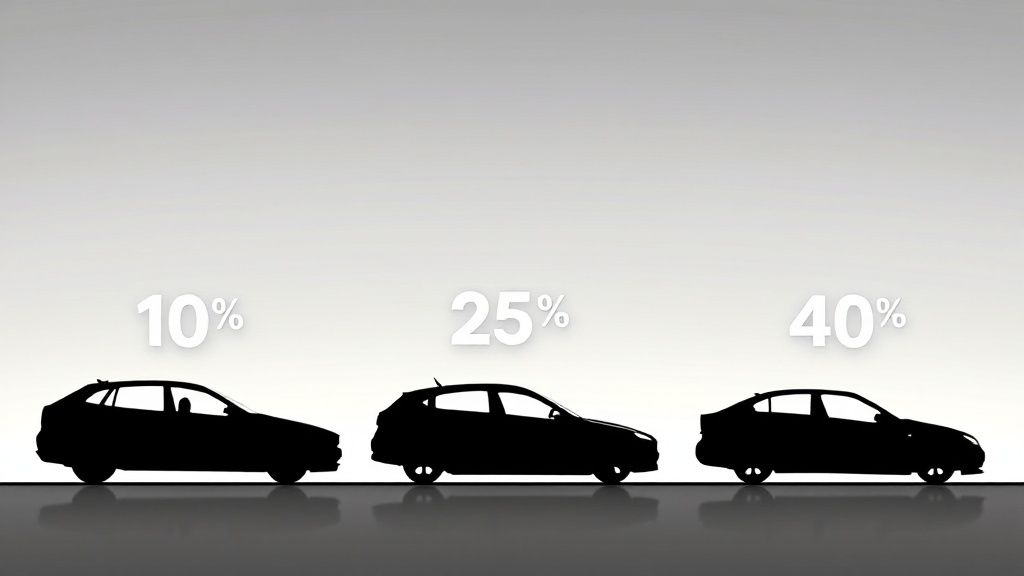

So, how much are we talking about? It really boils down to how bad the wreck was. Minor cosmetic damage might only cause a small dip, but a major collision requiring structural work is a different story.

Industry data consistently shows that even minor, properly repaired accidents can knock 5%–10% off your car's resale value. For accidents involving significant structural damage, that loss can easily jump to 15% or more. You can get more insights on how accident severity impacts trade-in value and learn to assess post-collision depreciation.

The bottom line is that repairs make your car look and drive right again, but they can't erase its past. This guide is here to show you how to measure, prove, and—most importantly—recover the money you're owed for that hidden financial damage.

Understanding the Three Types of Diminished Value

When your car gets into an accident, its value doesn't just drop once—it actually depreciates in a few different ways. It’s not a single, straightforward loss. To successfully file a claim and get back the money you're owed, you first need to understand these distinct stages of depreciation.

Think of it like a valuable antique vase that’s been broken and expertly glued back together. Even if the repair work is invisible to the naked eye, its history of damage means it will never be worth as much as an identical, undamaged piece. Your vehicle is no different, and its loss in value falls into three main categories.

Immediate Diminished Value

The moment of impact is also the moment your car’s value takes its first, and biggest, nosedive. This is called immediate diminished value. It’s the raw difference between what your car was worth seconds before the crash and what it’s worth sitting there, mangled and undrivable.

If your car had a market value of $25,000 pre-accident and would only sell for $10,000 with a crumpled front end, the immediate diminished value is a staggering $15,000. While this is a huge drop, it’s not usually the focus of a claim. Why? Because the at-fault party's insurance is meant to cover the cost of repairs to make the car whole again. The real battle is what happens after the repairs are done.

Inherent Diminished Value

This is the heart of every diminished value claim and the type you’ll hear about most often. Inherent diminished value is the automatic, permanent loss of value that’s forever attached to your car simply because it now has an accident on its record. This loss exists even if the repairs were absolutely perfect, done by certified technicians using the best parts available.

The reason is simple: vehicle history reports. Thanks to services like CarFax and AutoCheck, a car’s accident history is an open book. Once an accident is on that report, it’s there for good.

An accident history immediately creates doubt and suspicion in a potential buyer's mind. Given two identical cars, a buyer will always choose the one with a clean history—or demand a steep discount on the one that's been wrecked. That discount is your inherent diminished value.

This is the loss you suffer no matter how great the repair job was. It’s all about market perception—the simple fact that a previously damaged car is less trustworthy and therefore less valuable.

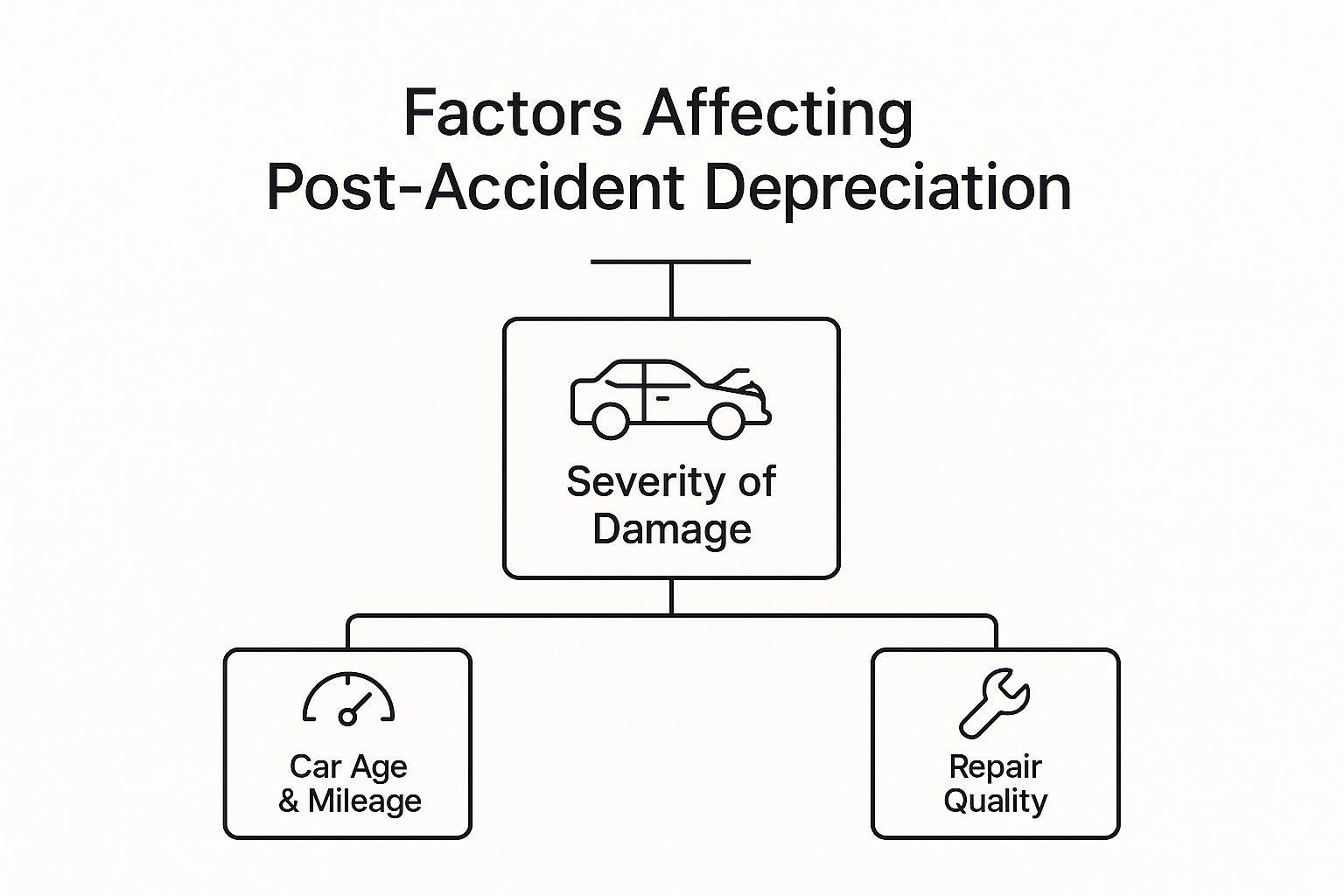

The infographic below breaks down the key factors that determine just how much value is lost after an accident.

As you can see, things like the severity of the damage, your car’s age and mileage, and the quality of the repair all play a role in the final number.

Repair-Related Diminished Value

Last but not least, we have repair-related diminished value. This is an extra layer of depreciation that gets piled on when the repair job itself is subpar. If the body shop you were sent to cut corners or did shoddy work, your car loses value from both the accident stigma and the bad repairs.

You can often spot this type of diminished value with a careful inspection. Look for tell-tale signs like:

- Mismatched Paint: The repaired panel is a slightly different shade or doesn't have the same finish as the original paint.

- Aftermarket Parts: Non-original (non-OEM) parts were used, which can compromise the fit, finish, and safety of your vehicle.

- Uneven Panel Gaps: The spaces around the doors, hood, or trunk are inconsistent or too wide.

- Lingering Problems: You notice new rattles, wind noise, or a steering wheel that pulls to one side—issues that weren't there before the crash.

This is basically a penalty for a job done poorly, and it makes your vehicle even harder to sell. Proving this type of loss requires careful documentation of the repair flaws. Navigating this process can be complicated, which is why it's crucial to understand the specific diminished value laws in your state.

Key Factors That Drive Your Car's Depreciation

Not every accident leaves the same financial scar. The value your car loses after a collision isn’t a flat number; it’s a unique calculation based on a whole host of variables. Getting a handle on these factors is the first step toward understanding what your financial loss really looks like.

Think of it like this: a pebble tossed in a pond creates a small ripple, but a massive boulder makes a huge wave. The specific details of your car and the collision itself determine the size of that financial wave. Two different vehicles in the exact same type of accident can lose wildly different amounts of value.

Let's break down exactly what pushes that number up or down.

Your Vehicle's Pre-Accident Profile

The car you were driving right before the crash really sets the stage. A brand-new luxury sedan and a ten-year-old daily driver start from completely different places, so it only makes sense that their post-accident depreciation will be worlds apart.

Here are the key pre-accident details that can amplify diminished value:

- Age and Mileage: Newer cars with low mileage always get hit the hardest. Someone shopping for a nearly-new vehicle expects perfection, so an accident history is a massive red flag that sends the price plummeting. An older, high-mileage car has already lost most of its value, so the additional drop from an accident is less severe.

- Make and Model: Luxury and high-end brands suffer more. A buyer shelling out for a Mercedes-Benz or BMW isn't just buying a car; they're buying prestige and a reputation for perfection. A collision history tarnishes that image instantly.

- Previous Accident History: A car with a perfectly clean record takes a much bigger financial hit from its first accident. If a vehicle already has a collision on its report, the damage from a second one is less dramatic. That first blemish is always the most costly.

The Nature and Severity of the Damage

The single biggest factor, without a doubt, is the damage itself. A minor fender-bender might just be a footnote in a car’s history, but major structural damage is a screaming headline that scares off almost any buyer. This is where the story of the accident gets written directly onto the vehicle.

For appraisers and future buyers, the crucial distinction is between cosmetic damage and structural damage. A dented door can be replaced and forgotten. A bent frame, however, raises permanent questions about the car's safety, integrity, and long-term reliability.

Any damage involving the frame, unibody, or critical mechanical parts like the engine or transmission will trigger the highest level of diminished value. Even with flawless repairs, the simple fact that these core components were compromised creates a permanent stigma that no body shop receipt can erase.

The Quality of Repairs and Parts Used

Once the damage is done, the quality of the repair work becomes the next critical piece of the puzzle. A top-tier repair job can help soften the blow of diminished value, while a shoddy one will only make things worse.

The most important detail here is the type of parts used to fix your vehicle. You'll generally see two kinds:

- Original Equipment Manufacturer (OEM): These are the real deal—parts made by your car’s manufacturer that are identical to what was on your vehicle when it rolled off the assembly line. They guarantee a perfect fit, finish, and safety standard.

- Aftermarket Parts: These are generic parts made by third-party companies. While they're often cheaper, the quality can be a roll of the dice, potentially leading to fitment issues, a mismatched appearance, or premature wear.

You should always insist on—and get documentation for—the use of OEM parts. Having invoices that prove genuine parts were used is powerful evidence that the repair was done right, which can seriously strengthen your diminished value claim.

The table below summarizes how these different elements come together to influence your car's post-accident value.

How Different Factors Impact Post-Accident Depreciation

| Factor | Impact on Depreciation |

|---|---|

| Newer Vehicle (Low Mileage) | Increases the value loss significantly. |

| Luxury/High-End Brand | Increases depreciation due to buyer expectations. |

| First-Time Accident | Increases the hit compared to a car with prior damage. |

| Structural/Frame Damage | Dramatically Increases the value loss. |

| Airbag Deployment | Increases loss, as it signals a severe impact. |

| Use of Aftermarket Parts | Increases depreciation by lowering repair quality. |

| Older Vehicle (High Mileage) | Decreases the overall diminished value amount. |

| Minor Cosmetic Damage | Decreases the loss compared to structural issues. |

| Documented OEM Repairs | Decreases loss by proving high-quality restoration. |

Ultimately, a combination of these factors paints the full picture of your car's lost value.

The Role of Vehicle History Reports

Finally, the thing that makes this all permanent is the vehicle history report. Companies like CarFax and AutoCheck are the official record-keepers of a car’s life. Once an accident is reported, it becomes a permanent part of that vehicle's story.

This report is what officially transforms a "repaired vehicle" into a "vehicle with an accident history." It’s the mechanism that broadcasts the damage to every single potential buyer down the line.

Beyond the hit to your car's value, an accident can also impact your insurance premiums. It's helpful to know about the factors behind rising auto insurance rates and why they can go up even as your car gets older.

Navigating the Insurance Claim Process

So, you understand your car has lost value. That's the easy part. The real battle is getting an insurance company to actually pay for that loss. Moving from knowing you're owed money to getting a check in hand takes strategy, and it starts with understanding the rules of the game. You should probably expect some pushback.

The first and most important thing to get straight is who you can even file a claim against. Almost without exception, a diminished value claim is a third-party claim. In plain English, that means you file against the at-fault driver's insurance company, not your own. Your own collision policy is there to fix your car, not to pay you for the market value it lost after being fixed.

Knowing Who to File Against

Getting this right from the beginning is critical because it dictates your entire approach. If the other driver caused the wreck, their liability insurance is on the hook to make you whole again. That includes covering the hit your car’s resale value took because of the accident.

- The At-Fault Driver: You file the claim directly with their insurance carrier. It’s your right. Their client’s mistake caused your financial loss.

- Your Own Insurance: Don't even bother. Trying to file a first-party diminished value claim is almost always a dead end. Most insurance policies have language specifically excluding it.

Knowing this saves you from wasting weeks fighting a losing battle with your own insurer. Your energy needs to be focused on building a rock-solid case to present to the other guy's insurance company. For a more detailed breakdown, our guide on how to file a diminished value claim walks you through every step.

Anticipating the Adjuster’s Arguments

Let's be clear: insurance adjusters are trained professionals whose job is to minimize how much money their company pays out. It's not personal, it's business. When you submit your diminished value claim, you can bet you’ll hear a few well-rehearsed arguments meant to shut you down. Being ready for them is half the battle.

The classic line you’ll almost certainly hear is that the top-notch repairs they paid for have restored your vehicle to its pre-accident condition, and therefore, its pre-accident value. The adjuster will hold up the repair bill like it’s the final word on the subject.

They will argue that since the car is fixed, their job is done. This argument conveniently sidesteps the whole concept of inherent diminished value—the permanent stigma an accident history leaves on your vehicle, no matter how perfect the repairs are. As you get into these conversations, knowing how to effectively deal with insurance adjusters is a skill that will directly impact your wallet.

Preparing Your Counterpoints

Your goal is to meet their arguments with facts and logic, not emotion. Frustration won't get you paid, but a well-organized case file will.

Here’s how you can prepare to counter their most common excuses with evidence-based responses:

-

When the Adjuster Says: "The repairs made your car whole again."

- You Respond: "The repairs restored the car's function, but they couldn't restore its market value. No reasonable buyer will pay the same for a wrecked-and-repaired car as they would for an identical one with a clean history. That difference is my loss, and your client is responsible for it."

-

When the Adjuster Says: "We don't pay for diminished value in this state."

- You Respond: "You're right that first-party claims are often excluded, but this is a third-party liability claim. The law in my state recognizes that the at-fault party is responsible for all damages from their negligence, and that includes my property's loss of market value."

-

When the Adjuster Says: "Your car is older, so there isn't much value to lose."

- You Respond: "While the dollar amount might be less than on a brand-new car, any vehicle with a clear market value takes a financial hit after a collision. My claim is based on the real-world depreciation for this specific vehicle, not a hypothetical one."

Winning this comes down to your ability to stay calm and present a logical, well-documented argument. You need to show them not just that your car lost value, but exactly how much it lost, backed up by a professional appraisal.

How to Prove and Document Your Claim

Successfully getting paid for your car's lost value after a wreck comes down to one simple thing: proof.

An insurance adjuster isn’t just going to take your word for it. You have to build a rock-solid case, much like an attorney would, by presenting clear, undeniable evidence that your vehicle suffered a real, measurable financial hit.

The responsibility for proving this loss falls squarely on your shoulders. This means you need to gather and organize a file that tells the complete story—from your car's pristine pre-accident condition to its lower post-repair market value. A well-documented claim is the single most powerful tool you have.

Start with a Professional Diminished Value Appraisal

The absolute cornerstone of any successful claim is a professional diminished value appraisal from a certified, independent expert. This isn’t a quick guess from a dealership or a number you get from an online calculator. It’s a detailed, evidence-based report from someone who lives and breathes vehicle valuation.

Remember, an insurance company’s internal valuation is designed to protect their bottom line, not yours. An independent appraiser, on the other hand, works for you. They dig into the specifics—your car’s make, model, age, pre-accident condition, and the severity of the damage—to pinpoint the exact impact on its resale value.

A credible appraisal from a certified expert is the single most important document you will have. It elevates your claim from a subjective opinion ("I feel like my car is worth less now") to an objective, expert-backed financial assessment that an insurance adjuster simply can't ignore.

This report becomes your primary weapon. It provides a specific dollar amount for your loss, backed by real market data and professional analysis. To get a better idea of what makes a report persuasive, you can learn more about the components of a professional diminished value report and why they are so critical.

Assembling Your Complete Documentation Toolkit

Beyond the appraisal, you need to collect other key documents that back up your claim. Think of each document as another brick in the wall, strengthening your position and making it much harder for the insurance company to deny or lowball your settlement. Your goal is to leave no room for doubt.

This collection of paperwork paints a complete picture of the accident and its financial fallout. Each piece reinforces the others, creating a web of proof that is organized and easy for an adjuster to follow.

Here’s the essential documentation you’ll need to pull together:

-

The Police Report: This official document establishes the facts of the accident, most importantly, who was at fault. Since you can only file a third-party diminished value claim against the at-fault driver's insurance, this is non-negotiable.

-

Pre-Accident Photos: If you happen to have photos of your car before the crash, they're pure gold. These images establish a baseline, proving the vehicle’s great condition and showing that the damage was a direct result of this one accident.

-

Photos of the Damage: Detailed pictures taken at the scene and before any repairs begin are crucial. They visually document the severity of the impact, which has a direct relationship with the amount of diminished value.

Documenting the Repair Process

The final pieces of your toolkit are all about the repair work itself. These records aren't just proof that the car was fixed; they are a detailed account of what was damaged and how it was restored. This information is vital for your appraiser and for pushing back against any arguments from the adjuster.

Your repair documentation should include:

-

Itemized Repair Invoices: Always demand a final bill that lists every single part replaced and every hour of labor. This detailed breakdown shows the true extent of the damage.

-

Proof of OEM Parts: If Original Equipment Manufacturer (OEM) parts were used, make sure the invoices say so. If the shop used cheaper aftermarket parts against your wishes, this documentation can support a claim for repair-related diminished value.

-

Post-Repair Vehicle History Report: Run a new CarFax or AutoCheck report after the repairs are done. This is often the final nail in the coffin. It provides black-and-white proof that the accident is now a permanent, official part of your car’s history, forever hurting its appeal to any future buyer.

With this complete toolkit in hand—led by a professional appraisal and supported by meticulous records—you completely change the dynamic. You're no longer just asking for money; you are presenting a formal, evidence-backed demand for compensation that the insurance company is legally obligated to take seriously.

Frequently Asked Questions About Diminished Value Claims

https://www.youtube.com/embed/_OiuLxg-rj0

Once you wrap your head around the concept of diminished value, the practical side of things can still feel a bit fuzzy. That's perfectly normal. It’s one thing to understand that your car is worth less after an accident, but it's another to know exactly how to get that money back.

Let's walk through some of the most common questions people have when they're standing in your shoes. Getting these details right can make all the difference in a successful claim.

Can I Claim Diminished Value If I Caused the Accident?

This is easily the most common question we get, and the answer is almost always no. Think of a diminished value claim as a type of property damage you're filing against the at-fault driver's insurance. It's their liability policy that covers the financial harm they caused you, which includes this loss of market value.

Your own collision coverage is there to pay for repairs—to physically put your car back together. It isn’t designed to compensate you for the hit your car’s resale value takes afterward. In nearly every state, you simply can't make a "first-party" diminished value claim against your own policy. The only exception would be if you have an extremely rare and specific policy that explicitly says it covers this loss, which is highly unlikely.

How Is the Amount of Diminished Value Calculated?

This is where things get tricky, because there's no single, universally agreed-upon formula. It's also why insurance companies and car owners are often so far apart in their numbers. The insurer wants to use a method that spits out the lowest possible figure, while you need a number that reflects your actual, real-world loss.

You might hear an adjuster mention the "Rule 17c" formula. This came out of an old court case and usually starts with 10% of the car's pre-accident value, then chips away at that number with deductions for mileage and damage severity. Most independent experts view this formula as a tool for generating lowball offers that have little to do with what a car is actually worth on the open market.

The most credible and accurate way to determine diminished value is through a detailed market analysis, which is what professional appraisers do. An appraiser will dig into the sales data for cars just like yours in your local area. They compare prices for vehicles with a clean history against those with an accident record to pinpoint the real-world difference in what buyers are willing to pay. This market-based evidence is the gold standard for proving your true financial loss.

Is It Worth Hiring an Attorney for My Claim?

Sometimes, but not always. Bringing in an attorney can be a powerful move, but whether it makes sense really boils down to the value of your claim and how the insurance company is behaving.

Here's a good way to think about it:

-

For High-Value Claims: If you drive a newer luxury car, a collector vehicle, or any car where the diminished value is likely to be $5,000 or more, an attorney is often a smart investment. Their fee is usually a percentage of what they recover for you, and it can be easily covered by the much larger settlement they're able to secure.

-

When the Insurer Is Stonewalling: If the at-fault driver's insurance company just says "no" or refuses to negotiate fairly, a lawyer can apply legal pressure that you can't on your own. They can manage the arguments and, if it comes to it, file a lawsuit to force the issue.

-

For Smaller Claims: On the other hand, if you have an older car and the diminished value is probably under $1,500, an attorney's fees might eat up too much of your settlement. In these cases, you're often better off handling the claim yourself, armed with a strong professional appraisal report.

A great strategy is to start by getting an independent appraisal. If the appraiser finds a substantial loss and the insurer's offer isn't even in the same ballpark, your next call should be to an attorney who specializes in this area.

If you're facing a diminished value claim or a total loss settlement dispute, don't let the insurance company dictate what your vehicle is worth. At Total Loss Northwest, our certified independent appraisers fight to get you a fair and accurate settlement based on real market data, not biased formulas. We provide expert reports that hold up in negotiations and ensure you recover the money you are truly owed. Visit us online to learn how we can help at https://totallossnw.com.