The Hidden Truth About Your Car's Post-Accident Value

Picture this: you’ve just picked up your car from the body shop. The new paint gleams, the panels align perfectly, and there’s no visible trace of the recent collision. To the eye, it’s fully restored. However, an invisible yet significant change has occurred. Your vehicle, despite its flawless repair, has silently lost a chunk of its market value. This phenomenon is known as diminished value, a permanent reduction in resale price that affects millions of vehicles simply because they now have an accident history.

This loss isn't just a theory; it's a concrete financial hit rooted in buyer psychology. Imagine two identical used cars for sale—same year, make, model, and mileage. One has a clean vehicle history report, while the other shows a record of a moderate collision, even one with expert repairs. Which one would you choose? Most buyers would select the accident-free car or demand a steep discount on the other, creating an immediate value gap.

The Real-World Financial Impact

This value discrepancy is not a minor detail. The moment an accident is recorded on a vehicle history report, it creates a permanent stigma. Prospective buyers will always wonder about the quality of the repairs and the potential for future issues, regardless of how pristine the car appears today. Insurance companies and automotive professionals understand this market reality well. Industry analysis reveals that diminished value losses following an accident average between 10% to 20% of the vehicle's pre-accident value. You can explore more on these insurance industry findings on the NAIC's public research site.

Understanding the Types of Diminished Value

To fully grasp the concept, it's helpful to see how this value loss is categorized. This screenshot from Wikipedia breaks down the three main types of diminished value.

The screenshot clearly distinguishes between Immediate, Inherent, and Repair-Related Diminished Value, each representing a different aspect of the financial loss. Your primary concern as a vehicle owner is inherent diminished value—the automatic loss in value that persists even after perfect repairs. This is the core of your claim and why understanding the diminished value appraisal cost is so important. It's an investment to prove and recover this hidden loss.

Understanding What You're Actually Paying For

When you hire a diminished value appraiser, you’re not just buying a document. You're investing in a detailed forensic analysis of your vehicle’s market value after an accident. The diminished value appraisal cost covers the expertise, specialized tools, and careful research needed to build a strong case that can hold up against an insurance company's questions. Think of it less like paying for a simple receipt and more like commissioning a financial investigation for your car.

This investigation starts with a detailed, hands-on vehicle inspection. Appraisers use equipment that goes far beyond a quick visual check. For instance, a digital paint thickness gauge can find areas where extra layers of paint and body filler were used, showing the true scope of repairs hidden under a shiny new finish. Likewise, diagnostic scanners can reveal stored trouble codes related to frame or sensor damage that are invisible to the naked eye. This level of detail is essential for proving the true impact of the collision.

Deconstructing the Appraisal Fee

A professional appraisal is a service with multiple components. The fee you pay covers several key activities that combine to create a solid and defensible valuation.

- Expert Analysis & Labor: This pays for the appraiser's time to conduct the physical inspection, perform market research, analyze data, and write the report. A skilled appraiser spends hours comparing your vehicle to similar ones on the market and documenting all the evidence.

- Specialized Tools & Software: The cost covers the use and upkeep of high-tech diagnostic tools, professional software for market analysis, and access to vehicle history databases.

- Documentation & Report Crafting: Creating a persuasive report is a skill. The appraiser must present their findings in a clear, logical way that an insurance adjuster can easily understand and act on. You can learn more about the key parts of a powerful diminished value report in our complete guide.

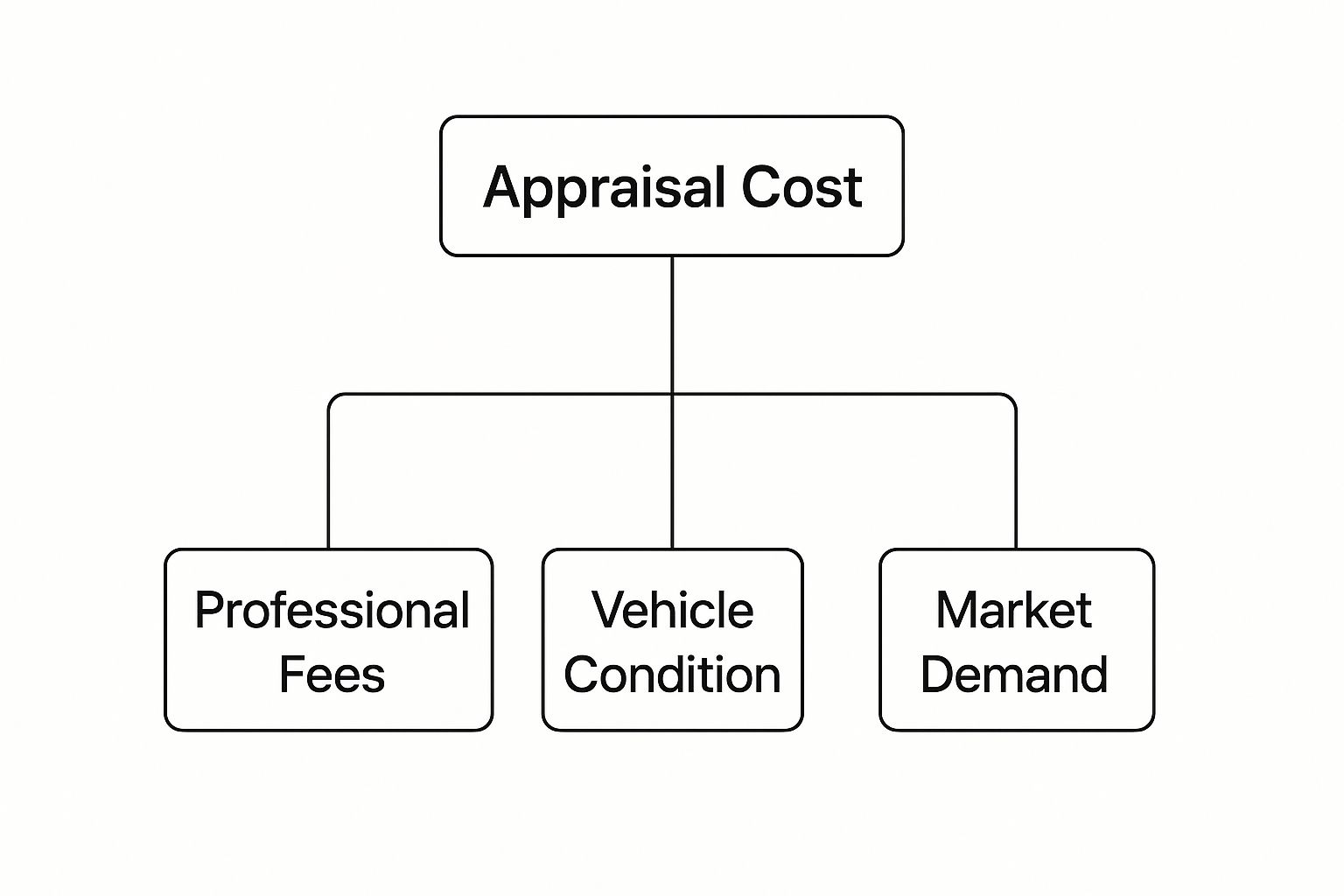

This infographic shows the main factors that determine the final appraisal fee.

As you can see, the total cost is a mix of professional services, the specific details of your vehicle, and current market conditions.

Justifying the Investment

Trying to save money with a cheap, template-based evaluation can be a big mistake. Insurance companies are experts at spotting and rejecting weak or poorly supported claims. A low-quality report often doesn't have the detailed evidence needed, making it easy for an adjuster to dismiss. A thorough appraisal, on the other hand, presents a fact-based argument they can't simply ignore.

Industry data shows that a professional diminished value appraisal cost usually falls between $350 and $699 for a report designed to stand up to insurance company review. This investment makes sure the appraiser does a detailed inspection and uses the right tools to build a solid case for you. To find out more about what this fee covers, you can review industry pricing insights on TheAutoMediator.com. In the end, paying for a quality appraisal is about giving yourself the credible evidence required to get the full amount you are owed.

What Makes Some Appraisals Cost More Than Others

Not every diminished value appraisal cost is the same, and understanding the variables can help you make a smart investment. Think of it like hiring a contractor for a home renovation. A simple bathroom refresh won't cost the same as a complex kitchen overhaul with structural changes. Similarly, the price of an appraisal is directly tied to the complexity of the job.

Several key factors influence the final price you’ll pay for a professional assessment of your vehicle's lost value.

Key Factors Driving Appraisal Costs

The unique characteristics of your vehicle and the nature of the accident are the main drivers behind pricing differences. A straightforward claim for a common sedan with minor cosmetic damage requires less intensive research than one for a rare or high-value vehicle.

Here are the main elements that affect the price:

- Vehicle Type and Value: Appraising a $150,000 luxury SUV or a classic muscle car is far more involved than evaluating a $20,000 daily driver. High-value, exotic, or classic cars have unique markets that require specialized knowledge and more extensive research to accurately determine value loss.

- Severity and Complexity of Damage: Minor cosmetic damage, like a dented fender, is relatively simple to assess. However, an accident that causes structural or frame damage introduces significant complexity. An appraiser must meticulously document how these repairs affect the vehicle's integrity and long-term value, which demands more time and expertise.

- Appraiser Credentials and Experience: Just like in any profession, expertise comes at a premium. An appraiser with advanced certifications, extensive court experience, and a proven track record of successfully challenging insurance company offers will naturally charge a higher fee. Their reports carry more weight and are built to withstand intense scrutiny.

To better visualize how these elements sway the final price, let's look at a breakdown of their impact.

| Factor | Low Impact | High Impact | Cost Difference |

|---|---|---|---|

| Vehicle Type | Common sedan or truck (e.g., Honda Civic, Ford F-150) | Luxury, exotic, classic, or custom vehicle (e.g., Porsche 911, vintage Mustang) | $150 – $400+ |

| Damage Severity | Minor cosmetic damage (e.g., bumper scrapes, small dents) | Major structural or frame damage, airbag deployment | $100 – $300+ |

| Appraiser Expertise | Standard certification, limited court experience | Advanced certifications, extensive court testimony, specialty vehicle knowledge | $100 – $250+ |

Note: The cost differences in the table are estimates and can vary based on the specific appraiser and market conditions.

As the table shows, a case involving a high-value car with major damage will require a top-tier expert, placing the appraisal cost at the higher end of the spectrum. Conversely, a standard vehicle with minor damage will be less expensive to appraise.

Ultimately, a higher diminished value appraisal cost often reflects the depth of work needed to build a powerful, evidence-backed claim. For high-stakes situations involving significant damage or valuable vehicles, investing in top-tier expertise is not just a cost—it’s a strategic move to maximize your financial recovery.

Regional Pricing Realities Across Different Markets

Just as the price of a house changes dramatically from a big city to a small rural town, the diminished value appraisal cost also varies. Geography plays a surprisingly large part in this, with local market trends, state laws, and the availability of qualified experts all shaping the final price. Where you live isn't just a minor detail—it's a major factor in the appraisal equation.

This difference in cost is especially clear in a state as diverse as Washington. Here, a combination of local factors influences what you should expect to pay for a reliable appraisal report.

Pricing Factors Unique to Washington State

Washington’s distinct automotive market creates different pricing levels across the state. An appraisal in the busy Seattle-Tacoma metro area will likely have a different price tag than one in Spokane or in a more rural region like the Palouse. Here’s a breakdown of why:

- Appraiser Availability: Big urban hubs like Seattle and Bellevue have more certified appraisers. This increased competition can lead to more competitive pricing for their services. On the other hand, rural counties with fewer appraisers might see higher fees, partly due to travel time and less direct competition.

- Local Market Conditions: The car market in the Pacific Northwest has its own quirks. Factors like the damp climate, which can speed up rust, or the high demand for certain vehicles like AWDs and trucks, influence a car's base value. A local appraiser who understands these details brings valuable insight, which affects the diminished value appraisal cost.

- State Insurance Regulations: Washington has specific laws that dictate how insurance claims, including diminished value, are handled. An appraiser must be knowledgeable about these state-specific legal rules and requirements. This expertise adds complexity and value to their work, ensuring the report they create is designed to hold up under scrutiny within Washington's legal system.

Ultimately, your goal is to find an appraiser who offers a fair price and has a deep understanding of your local market. A cheap report from an out-of-state appraiser who doesn't know Washington's market can be easily challenged by an insurance adjuster, making any initial savings worthless. Investing in localized expertise is key to building a strong claim that accurately reflects your real financial loss.

The Science Behind Professional Diminished Value Assessment

Behind every trustworthy appraisal is a detailed analytical process that makes the professional fee a worthwhile investment. A proper assessment is much more than a quick glance at a car’s book value; it’s a deep dive into market data, repair quality, and buyer psychology. This blend of art and science is what makes a professional report worth the diminished value appraisal cost, especially when an insurance carrier pushes back.

Uncovering the True Market Value

One of the biggest hurdles for an appraiser is determining a vehicle's true market value after repairs. This requires more than a simple online search. A qualified expert must find truly comparable vehicle sales—cars of the same make, model, year, trim, and condition—to set a credible baseline. While this might be fairly simple for a common car like a Toyota Camry, the task becomes much more difficult for a limited-edition model, a classic car, or a vehicle with unusual damage, demanding extensive research.

The process typically involves:

- Statistical Analysis: Appraisers use specific, accepted methods to compare your vehicle against market data. This ensures their findings are objective and can be defended if challenged.

- Market Psychology: They must also consider the intangible element—how the stigma of an accident impacts a potential buyer's willingness to pay. This isn't just a guess; it's an evaluation based on real-world market behavior.

- Compliance with Standards: Reputable appraisers follow the Uniform Standards of Professional Appraisal Practice (USPAP). Think of these as the quality control rules for the appraisal profession, making sure the final report is ethical, unbiased, and well-supported. You can learn more about how we conduct a proper diminished value appraisal that meets these strict standards.

The Value of Expertise in Complex Cases

The complexity of this work is why expert opinions have a significant cost. Appraising diminished value for assets like vehicles often requires spending up to $2,500 for high-level expert opinions. Unlike normal depreciation from age and mileage, this specific loss is tied directly to the vehicle's accident history—a unique factor that requires specialized analysis to measure accurately. You can discover more about the complex nature of appraising diminished value on DailyJournal.com.

Ultimately, the diminished value appraisal cost is an investment in a carefully constructed, evidence-based argument. You are paying for the time, tools, and expertise needed to turn a complex market reality into a clear, justifiable number that an insurance company must take seriously. This professional rigor is what separates a speculative guess from a valuation that can secure your rightful compensation.

Making The Math Work: When Appraisals Pay For Themselves

The most important question for any car owner thinking about a diminished value claim is simple: Will investing in a professional report actually be worth it? Understanding this cost-benefit analysis is key before you move forward. The decision really comes down to a basic calculation—comparing the diminished value appraisal cost to what you could get back financially.

Think of it as a strategic investment. You are spending a few hundred dollars with the potential to recover several thousand.

Calculating Your Break-Even Point

A simple way to see if an appraisal is worthwhile is to find your break-even point. If a detailed, high-quality appraisal costs $450, it only makes sense to get one if your car's lost value is much higher than that.

For example, if your vehicle's value has only dropped by $500, your net gain after the appraisal fee would be just $50. That might not be worth the time and effort. But, if your estimated loss is $3,000, that $450 investment could lead to a net return of $2,550—a definite financial win. The real goal isn't just to break even, but to see a significant positive return.

When Is an Appraisal a Smart Financial Move?

Some situations almost always guarantee a good return on investment for a professional appraisal. The math works out in your favor when certain conditions are met, making a strong case for filing a claim.

These high-potential scenarios include:

- Newer Vehicles (Under 5 Years Old): Cars with fewer miles and recent model years have a higher value before an accident, which means they have more value to lose. An accident on the vehicle's history report causes a much steeper drop in price for these cars.

- Luxury, Exotic, or Classic Cars: The market for these types of vehicles is extremely sensitive to accident history. Even minor damage can result in a five-figure loss in value, making a top-tier appraisal report an essential tool for recovering that loss.

- Accidents with Structural Damage: If your car needed repairs to its frame or other structural parts, the diminished value will be substantial. The stigma of structural damage is a huge red flag for future buyers, easily justifying the cost of an appraisal.

- Clean Pre-Accident History: A car with a perfect record that suddenly has a collision reported will see a much bigger drop in value than a car that already had a less-than-perfect history.

Ultimately, deciding whether to pay the diminished value appraisal cost is a business decision. By looking at your vehicle’s profile and comparing it to these high-return scenarios, you can make a smart choice. For many owners, particularly those with newer or high-value cars, the appraisal is not just an expense but the critical first step toward getting back thousands in lost equity.

Your Strategic Roadmap For Smart Appraisal Decisions

Turning what you've learned into decisive action is the key to a successful diminished value claim. Now that you understand the diminished value appraisal cost and what influences it, you can make confident, strategic choices. This isn't about hiring the first appraiser you find; it's about making a smart investment to get back the money you're owed.

Think of it like preparing for a big negotiation—your success hinges on doing your homework and knowing who to bring to the table. Your path to a fair settlement begins with finding the right professional for the job.

Checklist For Finding A Qualified Appraiser

Choosing the right expert is the most important move you'll make. A credible appraiser provides the solid proof your claim needs to be taken seriously. Use this checklist to screen potential candidates:

- Verify Credentials: Look for appraisers with recognized certifications, like those from the Bureau of Certified Auto Appraisers (BOCAA) or who follow the Uniform Standards of Professional Appraisal Practice (USPAP).

- Request Sample Reports: A trustworthy appraiser will have no problem sharing a redacted sample report. This gives you a direct look at their professionalism and the thoroughness of their work.

- Confirm Local Market Knowledge: Ask about their experience with vehicles in your specific area, such as Washington State. An accurate valuation depends heavily on local market expertise.

Warning Signs Of A Poor-Quality Service

Knowing what to look for is only half the battle; you also need to know what to avoid. Certain red flags can signal an unprofessional or even fraudulent service that will waste your time and money, leaving you with a useless report. After a collision, the last thing you need is more stress, which is why understanding what to do after a car accident includes steering clear of bad actors.

Be cautious of any service that:

- Guarantees a Specific Outcome: No ethical appraiser can promise a certain dollar amount. Their job is to provide an accurate, unbiased assessment, not a predetermined number.

- Offers Instant Online Reports: A proper appraisal requires a detailed inspection—often in person—and careful market research. "Instant" reports typically rely on generic formulas that insurance companies can easily discredit.

- Lacks Transparency: If an appraiser is vague about their methods, fees, or qualifications, it’s a major warning sign. A true professional will be open and clear about their entire process.

By using this strategic roadmap, you can approach the appraisal process with confidence. This forward-thinking approach ensures your investment in the diminished value appraisal cost pays off, putting you in the best position to recover the money you rightfully deserve.

If your vehicle has lost value after an accident, don't leave money on the table. At Loss Values Auto Appraisals, we provide certified, evidence-backed reports that get results. Contact us today to ensure you receive a fair and accurate settlement.