A diminished value claim calculator is your best starting point for getting back the money your car lost after a wreck—even if the repairs are perfect. These tools give you a solid estimate of the gap between your car's value before the accident and its new, lower value now that it has a damage history.

This permanent loss is called inherent diminished value, and it's exactly what you're entitled to claim from the at-fault driver's insurance company.

Understanding What a Diminished Value Claim Is

The moment your car is in a collision, its history gets a permanent black mark. No matter how fantastic the body shop is, that accident report is now attached to your vehicle's VIN forever.

Think about it from a buyer's perspective. If they're looking at two identical cars, but one has a clean history and yours has been in a wreck, which one will they choose? They'll always go for the one without the crash history or demand a serious discount on yours. That drop in what someone is willing to pay is your car's diminished value.

Filing a claim for this loss is your right, but don't expect the insurance company to bring it up. Their goal is to pay for the physical repairs and close the claim. The invisible financial damage to your car's worth? That's on you to prove. This is why a diminished value claim calculator is so crucial; it gives you a data-backed figure to kick off the conversation.

The Three Types of Diminished Value

When you hear "diminished value," it can actually mean a few different things. Knowing the lingo helps you build a stronger case for what you're owed.

- Inherent Diminished Value: This is the big one and the most common type of claim. It's the automatic loss in value that happens just because the vehicle now has an accident on its record, assuming the repairs were done to a high standard.

- Repair-Related Diminished Value: This comes into play when the repairs themselves are sloppy. Maybe the paint color is slightly off, the shop used cheap aftermarket parts, or you're still dealing with lingering mechanical problems. This is an additional loss on top of the inherent value drop.

- Immediate Diminished Value: This refers to the loss of value immediately after the crash but before any repairs have been made. It's not typically used for insurance claims but is more of a technical term.

Your claim will almost always focus on inherent diminished value. You're making a simple argument: even though my car looks great again, it's worth less than it was a minute before the collision, and I need to be compensated for that financial hit.

Ultimately, the goal is to be made financially whole. The other driver's mistake didn't just bend metal; it damaged your asset's equity. Before you can argue for what you've lost, you need to establish a rock-solid starting point for your car's pre-accident worth. Our guide on how to determine a car’s fair market value is the perfect place to begin.

Key Factors That Influence Your Diminished Value

Several variables come together to determine how much value your vehicle has lost. Insurance adjusters will look at these same factors when evaluating your claim, so understanding them gives you a major advantage.

| Factor | Impact on Claim | Example |

|---|---|---|

| Vehicle's Age & Mileage | High Impact: Newer, low-mileage cars lose a larger percentage of their value. | A 1-year-old luxury sedan with 10,000 miles will have a much larger DV claim than a 7-year-old commuter car with 120,000 miles. |

| Severity of Damage | High Impact: Structural or frame damage results in the highest diminished value. | A bent frame or deployed airbags will always cause a more significant loss of value than a minor fender bender. |

| Vehicle's Pre-Accident Value | Moderate Impact: Higher-value vehicles (luxury, sports, exotic) have more value to lose. | A $75,000 Porsche will see a much larger dollar-figure drop than a $20,000 Honda, even with similar damage. |

| Accident History | Moderate Impact: A vehicle with a pre-existing accident history will have a smaller claim. | If the car had a prior accident, its pre-crash value was already lower, which lessens the impact of the new damage. |

Knowing where your vehicle stands on each of these points is the first step in calculating an accurate and defensible claim amount.

How to Document Your Vehicle's Pre-Accident Value

Before you can make a case for what you’ve lost, you first have to prove what you had. The entire foundation of a successful diminished value claim rests on a rock-solid, evidence-backed valuation of your vehicle before the accident. Trust me, the insurance adjuster's primary job is to minimize what they pay out, and they will absolutely tear apart any valuation that seems vague or pulled out of thin air.

Your first move is to nail down a credible market value. Start with the big names like Kelley Blue Book (KBB) or NADAguides. Don't just pick your make and model and call it a day. You need to get granular—the exact trim level, every optional feature, and the correct condition. These details can swing the value by thousands, so getting it right is non-negotiable.

Establishing the Vehicle's Condition

You need to be honest but firm about your vehicle’s condition before the crash. If your car was immaculate, "Excellent" is the right choice. If it had the usual minor dings and scuffs for its age, "Good" is probably more accurate. Left to their own devices, insurers will almost always default to a lower condition unless you have proof.

This is where your paperwork becomes your superpower. It's time to gather every shred of evidence that tells the story of a well-cared-for, valuable car.

- Detailed Maintenance Records: Every oil change, tire rotation, and service receipt shows you were a meticulous owner.

- Recent Repair Invoices: Just drop a grand on new brakes or a timing belt? That invoice proves the car was in prime mechanical shape.

- Pre-Accident Photographs: Time-stamped photos are gold. A picture of your clean, waxed car sitting in the driveway just a month before the wreck can be incredibly persuasive.

Understanding how to properly assess a vehicle's worth, including getting familiar with tips on how to buy a used 4×4, can give you some great perspective here. Learning to think like a critical buyer is exactly the mindset you need. You're not just throwing numbers at the adjuster; you're building an argument for why someone would have gladly paid top dollar for your specific vehicle.

Organizing Your Evidence for the Adjuster

Once you've hunted down all your documents, get them organized. Please don’t just email a chaotic mess of crumpled receipts. Scan everything into a single, clean PDF, arranged either by date or by category (maintenance, upgrades, photos).

Pro Tip: I always recommend creating a simple cover sheet that summarizes your evidence. State the book value you've determined, then use bullet points to list the documents you’ve attached to back it up. This makes the adjuster's life easier and immediately frames your claim as professional and serious.

Think of it this way: you're building an airtight case. The stronger and more organized your evidence, the less wiggle room the insurance company has to fight you on the pre-accident value. This level of preparation is often what separates a frustrating lowball offer from the fair compensation you actually deserve.

Decoding the Insurance Company's Formula

Insurance companies almost never eyeball a diminished value claim; they have a playbook. It’s a specific, and frankly, self-serving formula designed to pay out as little as possible. If you want to fight for what you're owed, you first need to understand their secret weapon: the infamous “17c formula.”

This calculation became the industry standard after a 2001 Georgia Supreme Court case, Mabry v. State Farm. The whole thing starts by setting a "Base Loss," which immediately caps the maximum possible diminished value at just 10% of your car's pre-accident value. They'll typically grab this value from a source like NADA or Kelley Blue Book.

So, if your car was worth $25,000 before the wreck, the absolute most they'll consider for your claim is $2,500. Right off the bat, your potential payout is drastically limited. You can read more about how this court case changed the game for insurers at KBB.com.

But it doesn't stop there. From that already-reduced number, they start applying deductions to shrink it even more.

The Damage and Mileage Penalties

First, the adjuster applies a damage multiplier. This is a subjective penalty based on their assessment of the damage severity. It’s a scale, ranging from 1.0 for severe structural damage down to 0.0 for a few scratches.

Let's stick with our $25,000 car. If they decide the damage was "moderate" and assign a 0.50 multiplier, your potential $2,500 claim is instantly chopped in half to $1,250.

Next up is the mileage modifier. This penalty further reduces your claim based on your car's odometer reading. The logic is that higher-mileage cars have less value to lose, and vehicles with over 100,000 miles often get reduced to nothing.

Here’s a common breakdown they use:

- 0-19,999 miles: 1.00 multiplier (no deduction)

- 40,000-59,999 miles: 0.60 multiplier (a 40% cut)

- 80,000-99,999 miles: 0.20 multiplier (an 80% cut)

- 100,000+ miles: 0.00 multiplier (your claim is wiped out)

In our example, if your car has 50,000 miles, they'd apply a 0.60 multiplier. That $1,250 figure now gets cut down again to a final offer of just $750. A real-world loss of several thousand dollars gets whittled down to pocket change through their formula.

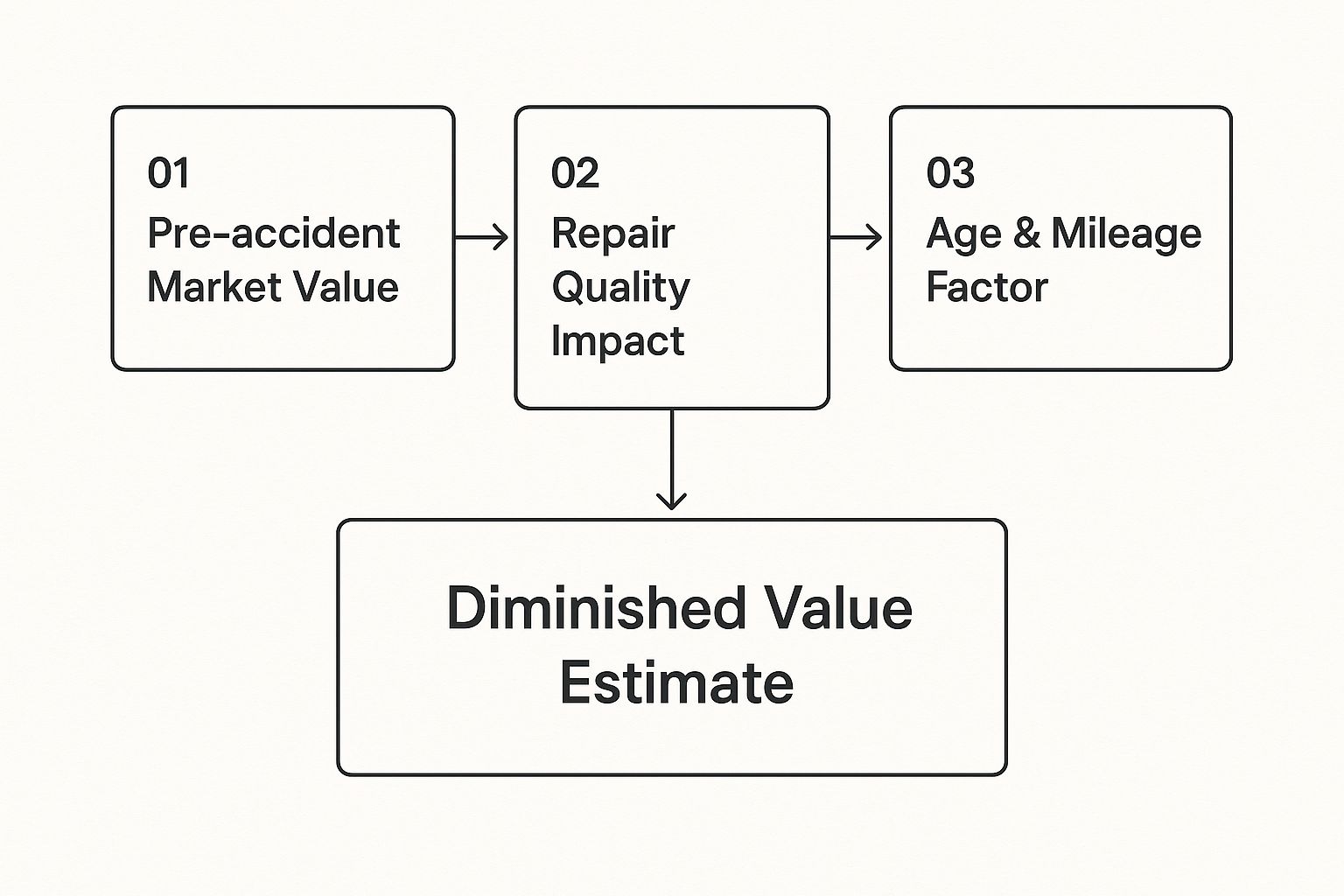

This visual helps break down the factors that really influence a diminished value calculation.

As you can see, the pre-accident value, quality of repairs, and vehicle age are the pillars of a legitimate estimate—things the 17c formula often skews.

Spotting the Flaws in Their Logic

The 17c formula is designed to protect the insurance company's bottom line, not to reflect what actually happens in the used car market. Its single biggest flaw is the arbitrary 10% cap, which has absolutely no basis in real-world resale data. A pristine luxury SUV or a sought-after sports car can easily lose far more than 10% of its value after a significant collision.

The core weakness of the insurer's formula is its one-size-fits-all approach. It fails to account for a vehicle's specific make, model, desirability, or local market conditions, treating a high-demand truck the same as a common sedan.

On top of that, the damage multipliers are completely subjective. This gives the insurance adjuster a ton of power to downplay how serious the repairs were. Your job is to call them out on these weaknesses.

Knowing their playbook is the first step in building your counteroffer. For a deeper look at turning this knowledge into action, check out our guide on how to negotiate a diminished value claim. When you can dismantle their logic, you’re in a much stronger position to present a credible, evidence-based argument for the compensation you truly deserve.

Using Online Calculators to Build Your Case

Now that you know how insurance companies try to lowball claims with their internal formulas, it's time to build your own evidence-based argument. You don't need to hire a professional appraiser right out of the gate. Your first and most effective move is to use a free online diminished value calculator.

These tools, especially those based on trusted sources like Kelley Blue Book (KBB), have been the go-to for car owners for years. They give you a concrete number to work with by comparing your car's market value before and after the accident. You simply plug in your car's details—year, make, model, trim, mileage, and ZIP code—and run two different reports.

First, you'll value the car in its pre-accident "excellent" condition. Then, you'll run it again in its post-accident "fair" or "good" condition. The gap between those two numbers is your diminished value. For example, a KBB-based calculation might show a car dropping from $21,500 to $17,300, revealing a $4,200 loss in value. You can get a deeper dive into using KBB for your estimate.

Generating Your Own Estimate

Getting your initial number is pretty simple, but it pays to be meticulous. Here's what the process looks like on most valuation websites:

- Get Your Pre-Accident Value: Start by entering all your car's info. When you get to the condition, select "Excellent" or "Very Good," assuming your car was in great shape before the wreck. Make sure to print this valuation or save it as a PDF.

- Run the Post-Accident Value: Without changing any of the other details, run a second valuation. This time, choose "Fair" for the condition to account for the new accident history. Save this report, too.

- Do the Math: Just subtract the "Fair" value from the "Excellent" value. The result is your starting point for the diminished value claim.

You'll start the process on the Kelley Blue Book site by entering your vehicle's specific details, just like in the screenshot below.

This first step is all about locking in a credible baseline value for your car before the accident history ever came into play.

Knowing the Limitations of Calculators

Online calculators are a fantastic tool, but they aren't the final word. Think of the number they produce as your opening bid in a negotiation, not a certified appraisal. They have a few key weaknesses.

For one, they can't see the real damage. A calculator has no way of knowing if your car had serious structural damage, which can absolutely tank its resale value. They also might miss the nuances of your local market and can't fully capture the stigma that comes with a documented accident on your vehicle's record. "Good" and "Fair" are just generic labels, after all.

Think of the calculator's output as your opening offer in a negotiation. It’s a credible, data-supported figure that forces the adjuster to move beyond their lowball 17c formula and engage with your evidence.

When you present your claim, bring both valuation reports, your maintenance records, and any pre-accident photos you have. This immediately shows the adjuster you're serious and have done your homework. You're coming to the table with real-world market data, not just accepting their arbitrary formula. Right away, this shifts the dynamic of the conversation in your favor.

How Market Conditions Affect Your Claim

A diminished value calculation doesn't happen in a vacuum. The number you get from a calculator is just a starting point; it's heavily swayed by the real-world used car market, which is always in flux. Supply, demand, and even the time of year can make your claim stronger or weaker.

It’s a lot like selling a house. The exact same property will fetch a much higher price in a hot seller's market than it would when buyers have all the power. Cars are no different. When used car lots are bare and demand is high, buyers can't afford to be as picky. An accident on the vehicle history report might not be a deal-breaker, which can slightly lower your diminished value.

But flip that scenario. When dealership lots are overflowing and buyers have endless options, a car with an accident record is suddenly a tough sell. That's when the value gap between your repaired car and one with a clean history gets much wider, justifying a larger diminished value claim.

Supply and Demand Dynamics

The classic laws of supply and demand are a major force here. Think back to the recent new car shortages—the whole used car market went wild. When demand is sky-high and supply is tight, even cars with accident histories are fought over. This can actually reduce the diminished value because buyers are just desperate to get a vehicle. You can get more expert insights on how market factors impact your claim at DiminishedValueofGeorgia.com.

This creates a strange situation where damaged goods hold more value than they normally would. But as soon as those supply chains catch up and inventory levels rise, the tables turn completely.

Seasonal and Regional Influences

It's not just about the overall market—where and when you file your claim can make a real difference. The value of certain types of vehicles changes with the seasons and what's popular in your specific area.

Here are a few examples I've seen play out:

- Convertibles: Their value always climbs in the spring and summer and takes a nosedive in the winter. A wreck in April will result in a higher diminished value claim than the same accident in November.

- 4×4 Trucks and SUVs: These are worth their weight in gold in states with rough winters, like Washington or Oregon. A collision in Seattle is going to have a different valuation than the same incident in sunny Phoenix.

- Fuel-Efficient Cars: The second gas prices spike, everyone wants a hybrid or a small sedan. This temporary surge in demand inflates their market value and, by extension, their potential diminished value.

A smart strategy is to factor these external pressures into your claim. Pointing out that your specific model is in high demand in your local market adds a layer of credibility to your argument that an insurance adjuster can't just brush aside.

By thinking through these real-world market conditions, you're doing more than just plugging numbers into a calculator. You're building a more sophisticated, compelling case that reflects the true financial loss you've suffered. This makes it much, much harder for the insurance company to stick to its initial lowball offer.

Common Questions About Diminished Value Claims

Diving into a diminished value claim can feel like trying to navigate a maze. You get the big picture, but the details can be confusing. This is especially true when a diminished value claim calculator gives you one number, and the insurance adjuster's offer seems like it’s from another planet.

Let's walk through some of the questions I hear all the time from car owners just like you.

Can I File a Claim if I Was at Fault?

This is probably the most common question, and the answer is almost always no. Think of diminished value as a third-party claim. It’s something you file against the at-fault driver’s insurance, not your own.

Your own collision policy is there to fix the physical damage—the dents, the broken parts, the paint. It’s designed to restore your car's function, not its market value. Insurers draw a hard line here, arguing their job is to make your car drivable again, not to protect its resale price.

Now, there are a few rare exceptions. In some states, like Georgia, you might be able to file against your own uninsured/underinsured motorist (UIM) coverage if the person who hit you doesn't have enough insurance. But honestly, these scenarios are few and far between and depend heavily on state-specific laws. For those in the Pacific Northwest, our guide on handling a diminished value claim in Oregon has some great local insights.

When Should I Hire a Professional Appraiser?

Using an online calculator is a great starting point. It gives you a ballpark figure and lets you know you're on the right track. But what happens when the insurance company stonewalls you? Or what if your car is a high-end luxury model, a classic, or an exotic?

This is exactly when you bring in a professional. An independent appraiser doesn't just give you an estimate; they produce a detailed, authoritative report that carries serious weight with insurance companies.

A certified appraisal isn't just an opinion; it's expert evidence. The cost is usually just a few hundred dollars, but it can easily boost your settlement by thousands. It’s an investment that almost always pays for itself.

A good appraiser digs deep. They scrutinize the quality of the repairs, analyze your local market conditions, and pull sales data for comparable vehicles. They build a rock-solid case that an adjuster simply can't ignore. It turns your request into a professional demand backed by facts.

How Much Does Vehicle Mileage Affect the Claim?

Mileage is the insurance company's favorite tool for slashing your payout. Their go-to formulas, like the infamous Rule 17c, are designed to heavily penalize cars with more miles on the clock.

Their logic goes like this: a car with 80,000 miles has less value to lose than one with only 20,000 miles, so the diminished value must be lower. These mileage "modifiers" can be brutal, sometimes cutting a claim down to nothing on vehicles with over 100,000 miles, no matter how bad the wreck was.

Don't let them get away with this flawed reasoning. Your job is to push back. A well-cared-for car with high mileage still takes a huge financial hit after an accident. A potential buyer will always pay significantly less for a car with a wreck on its record, and that simple truth is the foundation of your entire claim.

If you're dealing with a difficult adjuster or just feel like you're being lowballed, don't give up and leave money on the table. The experts at Total Loss Northwest specialize in certified, independent auto appraisals that give you the leverage to get what you're truly owed. Get the professional backing you need at https://totallossnw.com.