When another driver hits your car, the damage goes deeper than just crumpled metal and scratched paint. Even after the best body shop in town makes it look brand new, your vehicle is now worth less money. Period. That drop in resale value has a name: diminished value.

The good news? Washington law is on your side. You have a right to be compensated for this loss. Filing a successful diminished value claim is all about proving that loss and making the at-fault driver's insurance company pay you what you're rightfully owed.

Your Right to Diminished Value in Washington

It’s a frustrating reality many Washington drivers don't even know about. They get their car fixed and think that's the end of it, not realizing they've lost thousands in equity. The concept is straightforward: a car with a documented accident history is simply less desirable to a future buyer. That stigma permanently lowers its market value, and a diminished value claim is your tool to recover that financial hit.

Knowing the legal ground you're standing on is crucial when you go up against an insurance adjuster. In Washington, the principle of being "made whole" means you're entitled to more than just the repair bill. It includes the cost to fix the car plus the remaining loss in its market value.

Understanding the Types of Diminished Value

You might hear a few terms tossed around, but the one that matters for most people is inherent diminished value. This is the automatic loss in value that sticks to your vehicle the second an accident is reported. The car now has a history, and that history follows it forever.

Let's be clear: this isn't about blaming the body shop for poor repairs. That's a different problem called repair-related diminished value. This is purely about market psychology. Any smart buyer, given the choice between two identical cars, will pick the one with a clean record every single time. To even get a look, you'll have to slash your asking price.

Thankfully, the legal footing for these claims has become solid. A key Court of Appeals ruling in 2023 gave diminished value claims in Washington State serious teeth. This decision confirmed that third-party claimants (the not-at-fault driver) can recover their car's diminished value even after it has been fully repaired. This precedent stops insurers from being able to flat-out deny your claim.

Key Factors Influencing Your Claim's Success

When you submit your claim, the insurance adjuster will immediately weigh a few key elements to decide what, if anything, they're going to offer. The stronger you are on these points, the better your outcome will be.

Here's a quick overview of what they're looking at.

Key Factors Influencing Your Claim's Success

| Factor | Why It Matters | Example |

|---|---|---|

| Vehicle Age & Value | Newer, high-value cars suffer the most significant drop. An insurer knows a hit on a new luxury SUV is a bigger deal than a fender bender on an old commuter car. | A 2-year-old electric SUV will have a far more substantial claim than a 10-year-old sedan. |

| Severity of Damage | The market cares a lot about what was damaged. Frame damage or deployed airbags are major red flags that signal a significant loss in value. | A $12,000 repair bill involving structural realignment is much more compelling than a $1,500 bumper replacement. |

| Pre-Accident Condition | A car with a clean title, pristine condition, and low mileage before the wreck has the strongest case. Its value was at its peak, so the drop is more pronounced. | A well-maintained vehicle with no prior accidents will have a stronger claim than one with a pre-existing salvage title. |

These are the core components that build the foundation of your claim. Getting them right from the start is half the battle.

If you're ready to dig deeper and see exactly how to assemble your proof, our full guide on navigating a diminished value claim in Washington State breaks down the entire process.

Does Your Car Qualify for a Diminished Value Claim?

Before you dive headfirst into a diminished value claim in Washington, you need to be honest with yourself about your chances. I've seen countless owners waste time and energy on claims that were doomed from the start.

Insurance adjusters have a mental checklist they run through to size up a claim, and knowing what they look for gives you a serious advantage. The first and most important question is always this: Who was at fault?

In Washington, diminished value is a third-party claim. This means you can only file against the at-fault driver's insurance policy. If the accident was your fault, your own collision coverage will handle the repairs, but it won't pay you for the hit to your car's resale value. The entire concept is based on recovering damages from the person responsible for the loss.

The Key Factors Adjusters Look For

Once you've cleared the fault hurdle, an adjuster will immediately scrutinize a few other core factors. Think of these as the building blocks of a credible claim. The more of these boxes you can check, the stronger your case will be.

Here's what truly matters to them:

-

Vehicle Age & Pre-Accident Value: Newer and higher-value cars suffer the most. A two-year-old Audi that gets into a wreck will lose far more value than a 12-year-old Honda Civic with 150,000 miles. As a general rule, cars under 10 years old with significant pre-accident value—like luxury models, sports cars, and newer EVs—are the strongest candidates.

-

Severity of the Damage: This is a big one. Was there frame or structural damage? Did the airbags deploy? These are massive red flags for any future buyer and signal a much more significant loss in value. A simple cosmetic fix, like a new bumper cover, just doesn't carry the same weight.

-

A Clean Pre-Accident History: Your vehicle needs a clean title and no prior accident history. This gives you a clear "before" picture of its value. If the car already had a branded title or a previous accident on its record, proving this new collision caused a specific loss becomes incredibly difficult, if not impossible.

The heart of your argument is that the other driver took your perfectly good car and permanently damaged its history and value. If the vehicle was already compromised, that argument loses its power almost instantly. Expect the adjuster to pull a vehicle history report right away.

Don't Let the Clock Run Out

Time is also a critical element you can't ignore. Washington's statute of limitations gives you three years from the date of the accident to file a claim for property damage.

While three years might sound like plenty of time, waiting is a huge mistake. The best practice is to start the diminished value process as soon as the repairs on your car are finished. This keeps the evidence fresh and clearly connects the loss in value directly to the accident in question.

Of course, if the damage was so severe that your vehicle was declared a total loss, the process is different. In that situation, you aren't filing for diminished value but for the entire pre-accident value of your car. You'll need to know how to determine what your totaled car is worth to make sure you receive a fair settlement.

How to Prove Your Vehicle's Loss in Value

Let's be blunt: an insurance adjuster's primary job is to protect their company's bottom line, not yours. They aren't going to simply accept your claim that your vehicle has lost value without a fight. If you want to succeed with a diminished value claim in Washington, you need to build an airtight case with undeniable, objective proof. This isn't about what you feel your car is worth; it's about presenting cold, hard facts the adjuster can't dispute.

Think of it like you're building a legal case. You're the prosecutor, and your job is to gather all the evidence that tells the story of your vehicle's value before the accident and the permanent damage done after the repairs. This evidence file will be the foundation of your demand letter and your strongest tool during negotiations.

Building Your Evidence File

The first thing to do is gather every single piece of paper related to the accident and the subsequent repairs. I mean everything. Don't dismiss a document because it seems minor—small details can become major leverage down the line.

Here’s a checklist of the absolute must-haves for your file:

- The Official Police Report: This is non-negotiable. It officially documents the facts of the accident and, most importantly, identifies the at-fault driver.

- Detailed Repair Invoices: You need the final, itemized bill from the body shop. This proves the extent of the damage by listing every part that was replaced and all the labor required to fix it.

- Pre-Accident Photos: If you happen to have photos of your car in pristine condition before the crash, they're pure gold. They create a powerful "before" snapshot that contrasts sharply with the post-accident reality.

- Vehicle History Report: Get a report from CarFax or AutoCheck. A clean report before the collision is a cornerstone of a strong claim, as it proves your car didn't have a history of pre-existing damage.

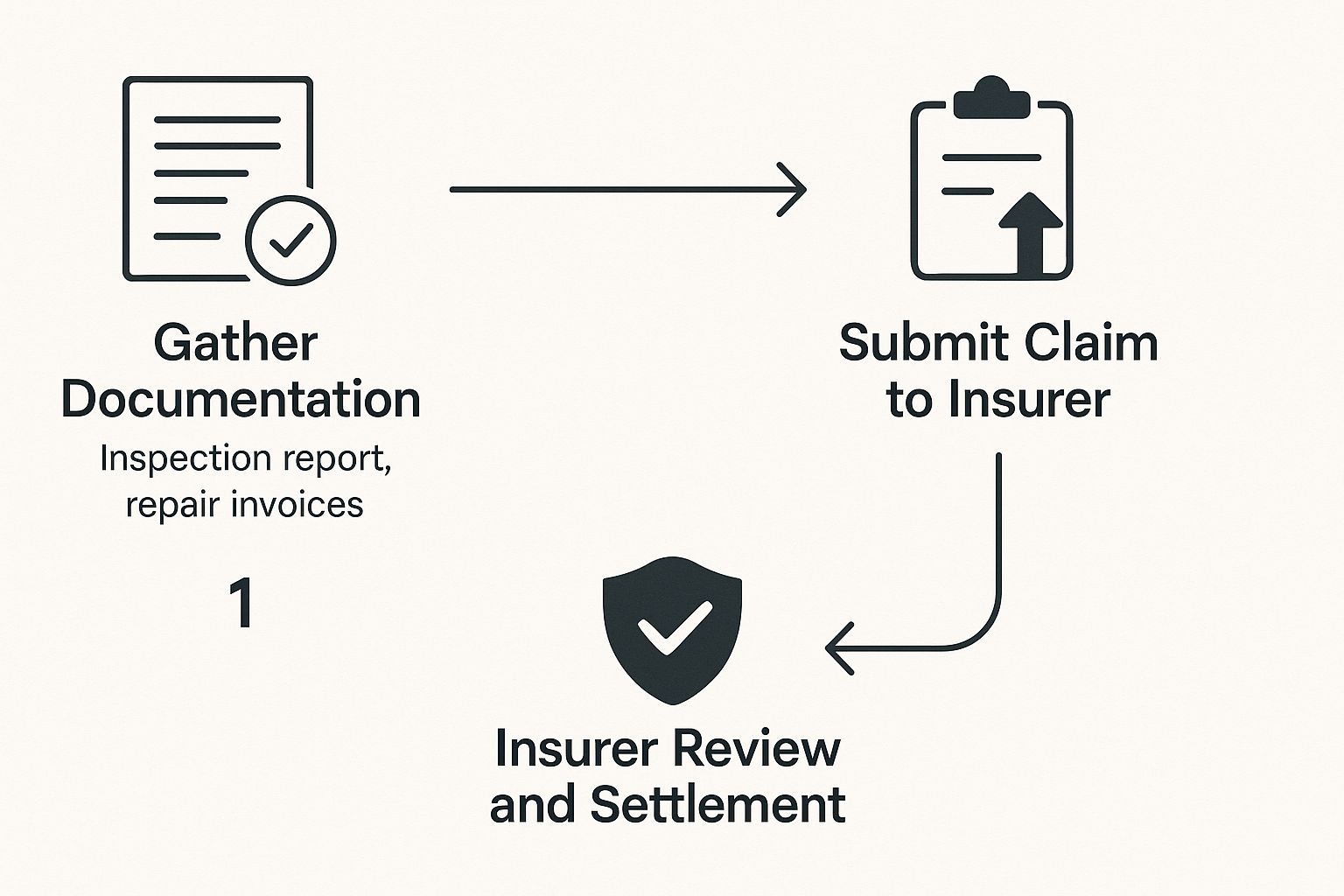

This image lays out the typical path of a successful claim, from the initial evidence gathering to the final settlement.

As you can see, solid documentation is the critical first step. Without it, your claim is built on sand and will likely crumble under the first bit of pressure from the insurance company.

The Single Most Important Piece of Evidence

While all the documents we've discussed are essential, one piece of evidence carries more weight than all the others combined: a professional diminished value appraisal.

Don't be tempted by free online calculators or the formulas the adjuster uses. They are intentionally designed to give you a lowball figure. An independent, third-party appraisal is your most powerful countermove.

Think of it this way: The insurance company has its expert—the adjuster. You need your own expert. A certified appraiser acts as your professional advocate, providing an unbiased, market-based report that details exactly how much value your vehicle has lost.

A credible appraisal from a reputable firm is far more than just a number on a page. A quality report will typically include:

- A detailed inspection and critique of the repair quality.

- An analysis of comparable vehicles for sale right here in the Washington market.

- Direct quotes or commentary from local dealership managers about how an accident history craters a vehicle's resale value.

- A clear, defensible final valuation that is backed by specific market evidence.

An adjuster can easily argue with your personal opinion. It's much, much harder for them to argue with a detailed, 20-page report from a certified professional. This document transforms your request from a simple complaint into a formal, evidence-based demand. In my experience, this single document is often what separates a token "nuisance" offer of a few hundred dollars from a fair settlement that truly compensates you for your financial loss.

Negotiating With The Insurance Adjuster

This is where the rubber meets the road. You've gathered all your evidence and have a professional appraisal in hand, so it’s time to engage the at-fault driver’s insurance adjuster. All that prep work is about to pay off. Your goal here is simple: be firm, be professional, and be impossible to dismiss.

Kicking Things Off: The Demand Letter

The first move is yours. You’ll send a formal demand letter to the adjuster, which is essentially your opening statement in the negotiation. This isn't just a quick note; it's a comprehensive package that lays out your entire case for a diminished value claim in Washington.

In this package, you'll clearly explain why you're entitled to compensation and attach every single piece of evidence you've collected. The star of the show, of course, is your certified appraisal report. Submitting a complete, well-organized file right from the jump shows you mean business and cuts down on the needless back-and-forth that can drag these things out.

Brace Yourself for the Adjuster's Tactics

Once the adjuster has your demand package, get ready for a response. It’ll likely come as a phone call or email containing a counteroffer—one that is almost guaranteed to be insultingly low. Remember, insurance adjusters are professional negotiators, and their job is to minimize the company's payout.

A favorite trick you'll encounter is a reference to some internal calculation, most notoriously the "17c Formula." This is a generic, one-size-fits-all formula created by insurers for their own benefit. It has no legal authority in Washington and is designed to spit out artificially low numbers.

Don't fall for it. The second the adjuster brings up the 17c Formula or any other internal worksheet, shut it down. Your response should be direct: "My claim isn't based on a formula. It's based on specific market evidence detailed in my certified appraisal."

Your appraisal is your most powerful tool. Lean on it. This isn't just your opinion versus theirs; it's your expert's fact-based report against their unsupported, self-serving number.

A Real-World Example of Pushing Back

Standing your ground with solid evidence is incredibly effective. For instance, I recently saw a case where a vehicle had $15,000 in repair work. The insurance company's initial offer, based on their 17c formula, was a paltry $1,300.

The claimant didn't flinch. They refused the offer, hired an independent appraiser, and filed in small claims court. Before it even got to a hearing, the insurer settled for $3,800—nearly triple their first lowball attempt. This just goes to show how a credible appraisal and the willingness to take the next step can completely change the game.

When you're on the phone with the adjuster, stay calm and keep pointing back to the facts in your report. Be ready to reject any offer that isn’t justified by the market data your appraiser found. This part of the process is crucial, and for a deeper dive into tactics, you can learn more about how to negotiate a diminished value claim in our guide. Knowing how to stand firm can make all the difference in your final settlement.

When to Escalate a Stalled Claim

https://www.youtube.com/embed/ThXQ2hPwyvk

So, you’ve done everything right. You sent a solid demand letter, backed it up with a professional appraisal, and the insurance company either shot back a laughably low offer or, worse, went completely silent. It's a frustrating, all-too-common roadblock, but it’s definitely not the end of your claim.

This is a classic insurance tactic. The adjuster wants you to feel defeated and give up, accepting pennies on the dollar just to be done with it. Don’t let them win. When negotiations stall, you still have options to force their hand and move your claim to an arena where their usual delay tactics won't fly.

Taking Your Claim to Small Claims Court

For most Washington drivers, the best next step is small claims court. Think of it as the great equalizer. It’s a less formal legal setting designed specifically for people to resolve disputes without the cost and complexity of hiring an attorney.

Filing a lawsuit is often the wake-up call an insurance company needs. Your claim instantly transforms from a file they can ignore into a legal problem with a looming court date. The pressure of having to show up and explain their lowball offer to a judge is frequently enough to get them back to the table with a much more serious settlement figure.

In Washington, the small claims court limit is a generous $10,000. This covers the vast majority of diminished value claims, making it the most powerful and cost-effective tool you have for breaking a deadlock.

Knowing When to Call an Attorney

While small claims court is fantastic, some situations just call for professional legal muscle. If your claim is going nowhere, it’s wise to at least consider speaking with an attorney, especially when certain red flags pop up.

You should think about hiring a lawyer if:

- Your loss is over $10,000. High-end vehicles—luxury sedans, EVs, classic cars—can easily suffer diminished value well beyond the small claims limit. An attorney is needed to pursue these larger claims in a higher court.

- The accident involved injuries. If you're also dealing with a personal injury claim, a good lawyer will roll your diminished value into the overall case to negotiate a single, comprehensive settlement.

- The insurer is acting in "bad faith." This isn't just a low offer. It's things like refusing all communication, denying your claim without a legitimate reason, or straight-up lying about the law.

Bringing in an expert who lives and breathes diminished value cases can make all the difference. They know the ins and outs of Washington law and have gone head-to-head with insurance company lawyers countless times. Their experience can prevent you from leaving thousands of dollars on the table, particularly when the stakes are high.

Your Top Questions About Washington Diminished Value Answered

Even after you've mapped out the process, it's completely normal to have some questions pop up about filing a diminished value claim in Washington. You're navigating unfamiliar territory, and you want to make sure every step you take is the right one. Let's tackle some of the most common questions I hear from vehicle owners just like you.

What if the Accident Was My Fault? Can I Still File?

Unfortunately, no. A diminished value claim in Washington is what's known as a third-party claim. This means you can only recover these specific damages from the insurance policy of the driver who was at fault.

Your own collision coverage is there to get your car repaired, but it won't cover the hit to your car's market value. The entire legal foundation of a diminished value claim rests on recovering a financial loss caused by another person's negligence.

How Much Time Do I Have to File a Claim in Washington?

Legally, the statute of limitations for property damage claims in Washington State gives you three years from the date of the wreck. While that might sound like plenty of time, delaying your claim is a significant misstep.

The best practice is always to start your diminished value claim the moment your vehicle repairs are finished. This timing keeps all the evidence fresh, from the repair invoice to your car's condition, making it much simpler to prove its pre-accident state. A prompt filing strengthens your position immensely.

Don't give the insurance adjuster an opening to argue that something else caused your car's value to drop. Filing right away creates a direct, undeniable line between the accident and your financial loss.

Will Filing a Diminished Value Claim Make My Insurance Rates Go Up?

It shouldn't. Because you're filing against the at-fault driver's insurance, your own provider isn't the one paying out.

This is a third-party claim handled entirely by the other driver's carrier. As a result, it shouldn’t have any negative impact on your premiums or your standing with your own insurance company.

Is It Really Worth Paying for a Professional Appraisal?

Without a doubt. In my experience, this is the single most important investment you can make in your claim. Think about it from the insurance adjuster's perspective: their job is to protect their company's bottom line by minimizing payouts.

If you just ask for money without solid proof, they'll likely deny the claim or throw you a lowball offer that's a fraction of your actual loss. A credible, independent appraisal report changes the entire conversation. It's no longer just your opinion; it's an evidence-backed demand they can't easily ignore. This report is your key negotiating tool and often results in a settlement that's thousands of dollars higher than what you would have gotten otherwise.

Navigating the ins and outs of a claim can feel overwhelming, but you don't have to go it alone. Total Loss Northwest specializes in certified, independent appraisals that give you the leverage needed for a fair settlement. Get the expert support you need to secure what you're rightfully owed.