Understanding Your Legal Rights In Washington State

When another driver hits your car, their insurance company's main goal is to repair the visible damage. But what about the damage to your car's resale value? Many owners don't realize that Washington State law allows them to recover this financial loss, which can easily add up to thousands of dollars. This is about more than just fixing your car; it's about making your investment whole again. You shouldn't have to take a financial hit because of someone else's mistake.

The idea behind a diminished value claim in Washington State is simple. A vehicle with an accident on its record is worth less than an identical one without, even if the repairs are top-notch. A diminished value claim lets you recover the loss in your car's market value after an accident, even after it's been fully repaired. This payment covers the gap between your car's pre-accident value and its post-repair value, a drop that often gets logged in databases like CARFAX for future buyers to see. You can discover more insights about Washington state claim laws and your rights.

This isn't just a theoretical loss. Picture this: you own a nearly new SUV worth $45,000. Someone rear-ends you, causing $8,000 in damage that a great body shop repairs perfectly. Even though your SUV looks brand new again, its market value might have dropped to $40,000 simply because of its accident history. That $5,000 difference is your diminished value, and you have a legal right to claim it from the at-fault driver's insurance.

Navigating The Different Types Of Diminished Value

To file a successful claim, you need to understand the specific types of diminished value that Washington recognizes. Each one applies to a different situation, and knowing which one fits your case is the first step to building a solid argument. Most claims will fall into one of three buckets, but the most common by far is inherent diminished value.

It's helpful to see how insurance companies approach these claims, which we cover in our guide to navigating the insurance diminished value claim process. Getting these definitions right is crucial because it sets the stage for your entire negotiation with the insurance adjuster.

To help clarify, here’s a breakdown of the three types of diminished value claims you might encounter in Washington.

| Claim Type | Definition | When to Use | Typical Payout Range |

|---|---|---|---|

| Inherent Diminished Value | The automatic loss in value a vehicle suffers simply because it now has an accident history, regardless of repair quality. | This is the most common claim, used when repairs are done correctly but the vehicle's market value has still dropped. | 5% – 25% of pre-accident value |

| Repair-Related Diminished Value | The additional loss in value caused by poor-quality repairs, such as mismatched paint, non-OEM parts, or lingering mechanical issues. | Use this when you can prove the body shop's work was subpar, further reducing your car's value below its already diminished state. | Varies greatly based on repair cost and quality issues |

| Immediate Diminished Value | The difference in value between a vehicle's pre-accident condition and its immediate post-accident, pre-repair condition (i.e., its value as a damaged vehicle). | This is less common and typically used in specific legal contexts or as a negotiation point before repairs have been completed. | Not typically pursued; value is established after repairs |

With this legal foundation, you can approach the insurance company with confidence. You aren't asking for a handout; you're demanding fair compensation that you are legally owed under Washington State law.

Game-Changing Legal Developments That Strengthen Your Case

Filing a successful diminished value claim in Washington State has gotten a whole lot easier recently, and it’s a shift every car owner should know about. For a long time, insurance companies could often brush these claims aside, treating them like a legal gray area. That all changed with a major court decision that tipped the scales firmly in your favor. This isn't just a small rule change; it's a solid legal foundation that gives your claim some serious muscle.

This development gives you a huge advantage when you're dealing with the at-fault driver's insurance company. Before, adjusters might have argued that third-party claimants (that’s you, the not-at-fault driver) weren't clearly entitled to diminished value. Now, that argument just doesn't fly. This means claims that were once routinely dismissed now have clear legal support, forcing insurers to take you seriously from the get-go.

The Precedent-Setting Ruling You Need to Know

The heart of this change is a landmark 2023 decision from the Washington Court of Appeals. For the very first time, the court officially and explicitly recognized that third-party claimants can recover for the residual diminished value of their vehicle even after it has been fully repaired. This ruling set a powerful precedent, confirming that under state law, you are entitled to be paid for your car’s lost market value on top of the repair costs. You can learn more about this groundbreaking Washington court decision and what it really means for you.

So what does this mean in plain English? It means that when you file your claim, you're not just asking for something you hope to get. You are demanding compensation that Washington's own appellate courts have affirmed is legally yours.

How to Use This Legal Shift in Your Favor

Knowing about this legal update is one thing, but using it effectively is what gets you paid. When you start talking to the insurance adjuster, you can now do so from a position of established legal right, not just hopeful negotiation. Here's how to put this knowledge into action:

- Mention the Precedent: Casually but confidently bring up that Washington courts have affirmed the right to third-party diminished value. You don’t need to sound like a lawyer, but showing you've done your homework can shut down old, outdated denial tactics before they even start.

- Frame Your Claim as Standard Procedure: Don't present your claim like it's some kind of special request. Instead, treat it as a standard part of the property damage settlement, one that is now fully validated by recent court rulings.

- Counter Lowball Offers with Facts: If an adjuster gives you a tiny settlement offer or tries to blow off your claim entirely, you can professionally push back. Let them know that the validity of these claims is no longer a debatable point in Washington State.

This legal evolution is your strongest piece of ammunition. It changes your diminished value claim in Washington State from a simple request into a recognized right, making sure you're in a much better position to get the full compensation you're owed for your car's lost value.

Building Your Evidence Arsenal From Day One

This is where a successful diminished value claim in Washington State is often won or lost: the strength of your evidence. Insurance adjusters are professionals trained to evaluate claims based on solid documentation, not just your story. If you're missing even one key piece of paper, it can really hurt your case. The goal is to create an undeniable record from the moment the accident happens, building a paper trail that leaves no doubt about your loss.

Think of yourself as an investigator piecing together a case. The more detailed you are right from the start, the more power you'll have when it's time to negotiate. Don't just wait for the insurance company to ask for things; be proactive and gather everything you can. This approach shifts you from someone simply asking for money to someone demanding fair compensation with a mountain of proof to back it up.

Your Essential Documentation Checklist

Getting your documents in order is the first real step you can take. Every piece of paper tells a part of the story and helps prove your financial loss. A common mistake is thinking the insurance company has all the information they need. They don't. They have what the other driver gave them, which is usually the bare minimum. It's up to you to paint the full picture.

To make this manageable, I've put together a checklist of the crucial documents you'll need. Think of this as your roadmap to building an ironclad claim.

| Document Type | When to Collect | Importance Level | Tips for Collection |

|---|---|---|---|

| Police Report | Immediately after the accident | Critical | Washington law requires a report for damage over $1,000. Get the report number at the scene and request a copy from the police department ASAP. |

| Photos & Videos | At the scene & post-repair | Critical | Go overboard. Document damage to all cars, the surrounding scene, and road conditions. Critically, take detailed photos after repairs are done. |

| Initial Repair Estimate | Before repairs begin | High | This is your starting point. Keep this and any supplemental estimates that pop up as the body shop finds more hidden damage. |

| Final Itemized Repair Invoice | When you pick up your car | Critical | This is a core document. It must detail every part and labor hour. Check if it lists OEM or aftermarket parts—this is vital for your claim. |

| Pre-Accident Service Records | As soon as possible | High | Dig up receipts for new tires, recent oil changes, or any other maintenance. This proves you had a well-maintained vehicle. |

| Proof of Ownership | As soon as possible | Medium | Have a copy of your vehicle's title and registration handy to confirm you are the legal owner. |

Having these documents organized and ready to go shows the adjuster you are serious and well-prepared, which can make a big difference in how your claim is handled.

Pre-Accident Condition and Post-Repair Reality

To successfully argue that your car has lost value, you first need to establish what it was worth before the crash. This is a step many people overlook. You need to prove your car wasn't just any used car, but a well-cared-for asset. Pull out any service records, receipts for recent work like new brakes or tires, and any pre-accident photos you might have. All this documentation helps build the case for a higher pre-accident value.

After the repairs are finished, your work isn't done. Your vehicle now has something it didn't have before: an accident history. This is the very definition of inherent diminished value. The more severe that accident was, the greater the loss in value.

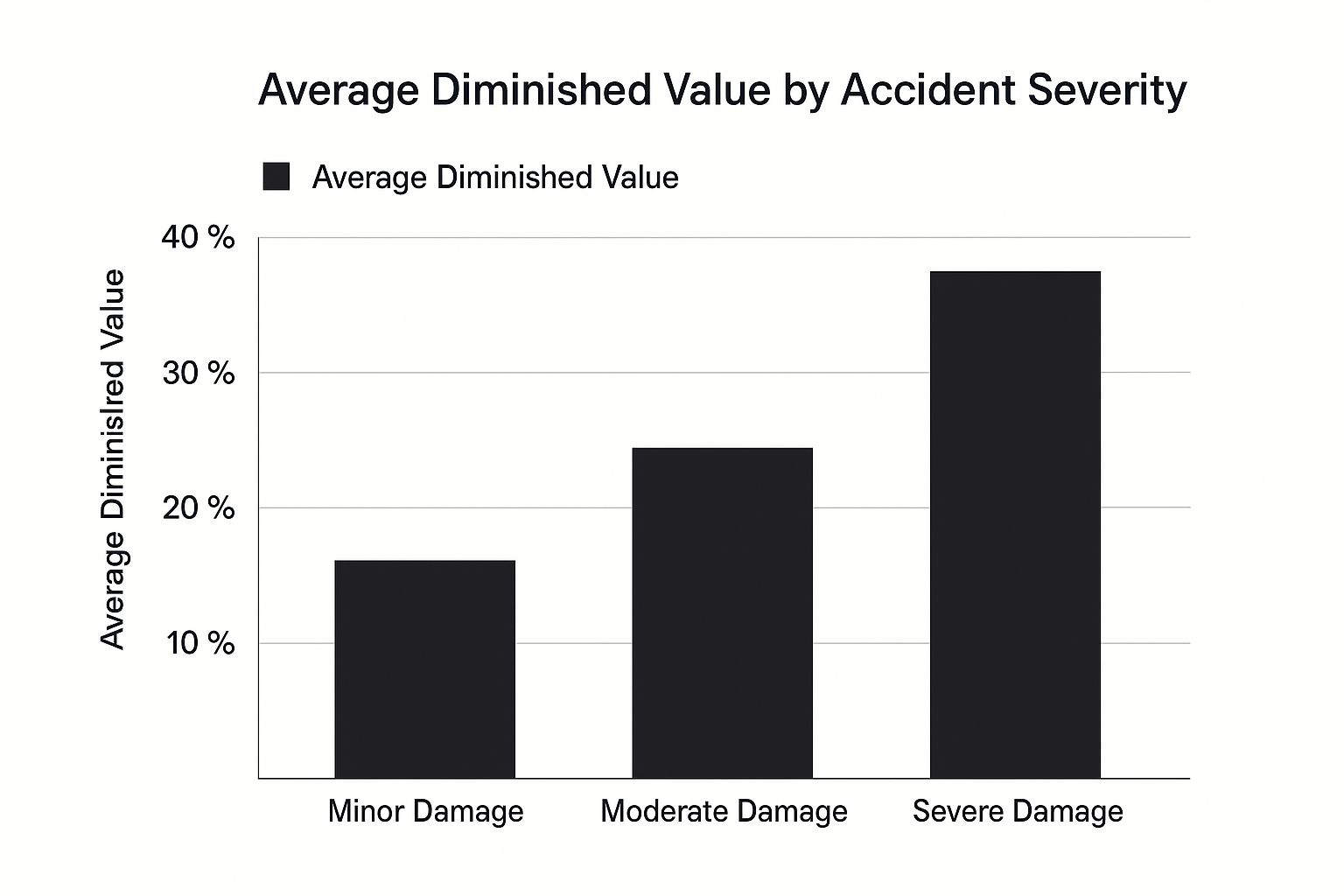

This infographic shows just how much the severity of an accident can affect your car's resale price.

As you can see, even what seems like minor cosmetic damage can lead to a significant loss. But when an accident involves structural or frame damage, it can wipe out a third or more of your vehicle's value. This is why that detailed repair invoice is so essential—it’s the proof of how extensive the damage was, which is what a professional appraiser will use to calculate your specific loss. A complete file—showing a pristine car before the crash and documenting major repairs after—creates the unshakable foundation you need for a successful claim.

Getting Professional Appraisals That Insurance Companies Respect

While your documents build the foundation of your case, a professional appraisal is the keystone holding it all together. Think of it this way: a well-researched, detailed report from a credible expert is your single most powerful tool for a diminished value claim in Washington State. Without it, you’re just sharing an opinion. With it, you're presenting a fact-based financial analysis that an insurance company is legally required to take seriously.

Insurance adjusters are trained to find holes in weak arguments. They will easily brush aside an estimate from an online calculator or a casual opinion from a local car dealer. To them, that isn't proof of your financial loss—it's just an invitation to give you a lowball offer. What they can't dismiss so easily is a formal report from a certified, independent appraiser who has carefully documented their findings with real-world market data. This is how you change your claim from a simple request into a well-supported demand.

Choosing an Appraiser with the Right Credentials

Not all appraisals carry the same weight, and the person who writes yours is incredibly important. Insurance companies are well aware of which credentials matter and which ones don't. You need an appraiser who is not only experienced but also certified by a recognized authority. Look for professionals with certifications from groups like the American Society of Appraisers (ASA) or other respected organizations that focus on vehicle valuation.

These certifications show that the appraiser follows strict ethical guidelines and proven methodologies. An uncertified appraiser might just give you a number, but a certified one provides a defensible position backed by industry-wide practices. For instance, a certified professional won't just invent a figure; they'll perform a thorough market analysis, comparing your repaired car to actual vehicles for sale in the Washington market. This approach gives a clear, data-driven look at your financial loss. The price of a quality appraisal is an investment that can pay for itself many times over, a subject we cover more in our guide to understanding diminished value appraisal costs.

Understanding Appraisal Methods: Beyond the Flawed "17c Formula"

Insurance companies often try to use their own calculation methods, with the most notorious being the "17c formula." This is a generic, insurer-friendly formula that nearly always calculates an artificially low value. It uses arbitrary limits and adjustments that have little to do with the actual car market in Washington State. A credible, independent appraiser will never rely on it.

Instead, they use established methods that hold up under review:

- Market Analysis: This is the best approach. The appraiser finds several real, comparable vehicles for sale (same make, model, year, and similar mileage) to set a baseline pre-accident value. They then research how a similar vehicle with an accident history is priced in today's market, using that data to pinpoint your specific loss.

- Dealer Consultations: A professional appraiser will often speak with sales managers at dealerships that specialize in your vehicle's brand. They’ll ask them directly, "How much would you discount this car, with this specific repair history, if you were taking it as a trade-in or selling it on your lot?" These expert opinions add powerful, supporting evidence to your claim.

The screenshot below shows how an appraisal formally documents a vehicle's value, which is vital for your claim.

This formal documentation is what separates a professional opinion from a simple guess. It gives your claim the credibility it needs to succeed. An adjuster can argue with what you think your car is worth, but it's much more difficult for them to argue with documented market data and expert analysis.

Calculating Your True Financial Loss Like A Pro

The numbers are what ultimately tell the story of your claim, but you have to know how to read them correctly. Insurance companies lean on their own formulas and internal data to figure out diminished value. Understanding their methods is the key to spotting and rejecting a lowball offer. Let's pull back the curtain on how these calculations really work and see how things like your car's mileage, the severity of the damage, and the quality of the repairs affect your final payout.

A successful diminished value claim in Washington State isn't about a vague feeling that your car is worth less. It’s about proving a specific, real-world financial loss with a logical, evidence-based approach that an insurance adjuster can't just brush aside.

Beyond the Insurer's Formula

One of the first things an insurer might throw at you is a formula like "Rule 17c." This is an internal, self-serving calculation that nearly always spits out a tiny number. It uses arbitrary caps and modifiers that have nothing to do with the actual car market here in Washington. For instance, the formula might automatically cap the highest possible loss at 10% of your car's pre-accident value, then shave off more for mileage and any prior damage. This often leaves you with an offer that's just a fraction of your real loss.

Your job is to push this formula aside and bring the conversation back to what actually matters: real market data. The true value of your loss is determined by what a buyer in your area would pay for a car with an accident on its record versus what they'd pay for the same car with a clean history.

Estimating Your Loss with Market Data

To calculate your loss like a professional, you need to think like an appraiser. This process builds a persuasive argument using a few key pieces of evidence:

- Establish Pre-Accident Value: Start by looking for several comparable vehicles for sale in your area. You want the same make, model, year, and similar options and mileage. The average listing price of these "clean history" cars is your vehicle's pre-accident value.

- Factor in Accident Severity: The extent of the damage is the biggest variable. A minor fender-bender with a $2,000 repair bill will cause far less diminished value than a major wreck with a $15,000 repair bill that involved structural work. Newer and luxury vehicles also tend to take a bigger percentage hit, as buyers in that market are especially wary of accident histories.

- Analyze Post-Repair Value: This is where it gets a bit tricky. You need to find examples of similar cars being sold with an accident history. An appraiser often gets this data by speaking directly with used car sales managers to get a realistic perspective on how much they'd have to discount a car like yours to sell it.

The difference between your car's pre-accident value and its post-repair market value is your diminished value. Putting all this information together in a clear, logical format is crucial. You can see how professionals structure this evidence by looking at what goes into a professional diminished value report. When you arm yourself with this kind of solid reasoning, you're in a much stronger position to counter an insurer’s low offer and get a fair settlement.

Mastering Insurance Company Negotiations

This is where all your careful preparation pays off. You've collected your evidence, you've got a professional appraisal in hand, and now it's time to turn that work into a check from the insurance company. Getting a fair diminished value claim in Washington State is a game of psychology, persistence, and solid presentation. You have to get inside an adjuster's mindset and frame your demand in a way that makes it easy for them to approve.

Think about it from their perspective: insurance adjusters are juggling dozens of claims at once. Their main goal is to close files quickly and stay within their approved payment limits. If you send them a messy, emotional, or poorly supported claim, it's easy for them to shoot back a low offer and move on. But when you present a professional package with clear documents, a credible appraisal, and a firm yet polite attitude, you make it simple for them to justify paying your number. Your goal is to make saying "yes" to your claim the path of least resistance.

Handling the Inevitable Lowball Offer

Let's get one thing straight: the first offer you get will almost certainly be low. Don't get angry or discouraged. This is just a standard opening move, a tactic to see if you'll get frustrated and accept a small amount just to be done with it. How you respond to this first offer sets the stage for the rest of the negotiation. Instead of getting mad, see it as the beginning of a business conversation.

Here's a common scenario: The adjuster calls and offers you $850, explaining it's based on their internal "worksheet," which is likely the infamous 17c formula. Instead of getting into a fight about their formula, try a calm and firm response:

- "Thank you for getting back to me with that initial figure. It seems a bit low compared to the specific market data for my vehicle here in Washington. My certified appraisal, which I already sent over, analyzed local dealership input and sales data, showing a documented loss of $4,200."

- "Would you be able to share the specific market data you used to get to your number? As you can see on page five of my report, my appraiser found that similar models with an accident on their record sell for a considerable discount in our area."

This approach skillfully sidesteps a pointless argument over their formula and pivots the conversation back to your strongest asset: your professional, evidence-based appraisal.

The Art of Professional Persistence

After you counter their low offer, the adjuster will likely come back with a slightly better number, but it will probably still be far from your documented loss. This is where you need to be persistent. Remember, you're not being a pest; you're advocating for fair compensation that you are legally owed. Keep your tone professional and calm in every email and phone call. It's a great idea to keep a log of every conversation: note the date, who you spoke with, and a summary of what you discussed.

If you find the adjuster is ignoring you or just won't budge from an unreasonable offer, it's time to escalate. Politely ask to speak with their supervisor or a claims manager. Managers typically have more authority to approve larger settlements and are often motivated to resolve stalled claims. Present your case to them just as you did before, highlighting the professional evidence you've provided. This methodical, firm-but-fair approach is what turns a potentially frustrating process into a successful diminished value claim in Washington State.

When To Escalate And Protect Your Financial Interests

Even with flawless preparation, some negotiations just hit a dead end. The insurance adjuster might suddenly go silent, stop returning your calls, or just keep repeating the same lowball offer. Knowing when to push back on your diminished value claim in Washington State is a vital skill that can stop you from leaving thousands of dollars behind. This isn’t about being combative; it's about knowing when the standard process isn't working and you need more leverage to protect your investment.

When an adjuster says their offer is "final" or that their manager has "already signed off," don't just accept it. These are common negotiation tactics meant to make you feel powerless and give up. The real red flag is when they stop negotiating and refuse to even discuss your evidence, especially your professional appraisal. If the adjuster won't give you a logical reason for ignoring your appraisal beyond saying it "doesn't follow our internal guidelines," it's time to take your claim to the next level.

Involving the Washington State Insurance Commissioner

One of the most effective tools you have is filing a formal complaint with the Washington State Office of the Insurance Commissioner (OIC). This is more than just firing off an angry email; it’s an official process that legally obligates the insurance company to respond to a state regulator. You can file a complaint right on the OIC's website, where you'll detail your claim, the insurer's low offer, and the proof you've submitted.

Once the OIC is involved, the entire situation changes. Your claim is no longer a minor file on an adjuster's desk—it's now a formal issue being watched by the same government agency that licenses the insurance company. This pressure often forces a senior claims manager to take a serious look at your file and make a fair offer just to resolve the complaint. Insurers hate having unresolved complaints on their record, and this pressure can be exactly what you need to get paid properly.

When Legal Help Makes Financial Sense

Another path for escalation is to speak with an attorney who specializes in diminished value claims. Many people are wary of this step, thinking about the cost of legal fees, but you need to weigh that against the potential gain. A good attorney in this field often works on a contingency basis, which means they only get paid if they win a larger settlement for you.

Imagine this real-world scenario: the insurance company's "final" offer is $1,500, but your documented, appraised loss is $6,000. That's a $4,500 gap. An attorney might charge a one-third fee on the final settlement amount. If they successfully negotiate the claim up to the full $6,000, their fee would be $2,000. You would walk away with $4,000—significantly more than double what the insurer was offering, even after paying for legal help. For claims involving high-value vehicles or substantial damage, hiring an attorney is almost always a smart financial move.

Navigating these escalations requires a calm approach and a rock-solid case. If you're up against a stubborn insurer or your loss is significant, getting professional help is key. At Loss Values Auto Appraisals, we create certified, evidence-based reports that act as the bedrock for these higher-level negotiations. Our appraisals are designed to hold up under the scrutiny of insurance managers, state regulators, and attorneys, giving you the powerful proof you need. Don't let an insurance company tell you what your car is worth—get a certified appraisal from us and fight for the full value you are owed.