Let's be honest: even after the best body shop in town works its magic, a car that's been in an accident is worth less than one with a spotless record. It's an unfortunate truth of the auto market.

This hit to your car's resale value is called diminished value. Think of it as the hidden financial damage from a crash—and if someone else was at fault, their insurance company should be the one to cover it. Getting a handle on how diminished value laws work is your first move toward getting the compensation you're owed.

What Is Diminished Value and Why Does It Matter?

Put yourself in the shoes of a used car buyer for a second. You've narrowed your search down to two identical SUVs. They have the same mileage, the same features, and the same asking price. There's just one difference: the first one has a clean CarFax report, while the second one was in a pretty serious wreck last year. The dealer assures you it was "professionally repaired."

Which one are you buying?

Nine times out of ten, you're picking the one with no accident history. Or, at the very least, you’d demand a significant discount on the previously damaged one. That gap in price—the one created solely by the stigma of an accident—is the core of what diminished value is all about. It’s the concrete, real-world financial loss your vehicle takes on the moment an accident becomes a permanent part of its story.

Even with flawless repairs and genuine factory parts, the car's market value still takes a dive. Any informed buyer will simply not pay top dollar for a vehicle with a checkered past. This is the fundamental concept you need to grasp.

Key Takeaway: Diminished value isn't about the quality of the repair work. It's about the permanent drop in your car's market value that happens as soon as an accident is recorded on its history. This is a loss the at-fault driver's insurance is legally obligated to cover.

The Three Types of Diminished Value

When you get ready to file a claim, it helps to know that this loss isn't just one vague idea. It’s actually broken down into three specific types. Knowing which one—or ones—apply to your situation is key to building a solid case.

To make this crystal clear, here’s a quick breakdown of what you might be facing.

Quick Guide to Types of Diminished Value

| Type of Diminished Value | What It Means | Common Scenario |

|---|---|---|

| Inherent Diminished Value | The automatic loss in value simply because the vehicle now has an accident history. It assumes quality repairs. | Your car is perfectly repaired after a rear-end collision, but its vehicle history report now shows a "moderate damage" event, lowering its resale value. |

| Repair-Related Diminished Value | An additional loss in value due to subpar or poor-quality repairs. | The body shop used aftermarket parts that don't fit right, or the new paint is a slightly different shade than the original factory color. |

| Immediate Diminished Value | The loss in value right after the accident but before repairs have been completed. This is a temporary state. | The value of your wrecked, undrivable car as it sits at the tow yard. This converts to other types of DV once repaired. |

As you can see, each type addresses a different part of the financial damage.

For the vast majority of claims, inherent diminished value is what you'll be focused on. You're making a case for the simple fact that your car, through no fault of your own, will now fetch less money from any future buyer. The at-fault driver's insurance is responsible for making you "whole," and that means paying for this very real financial hit. If they don't, you're the one left holding the bag when it's time to sell or trade in your car.

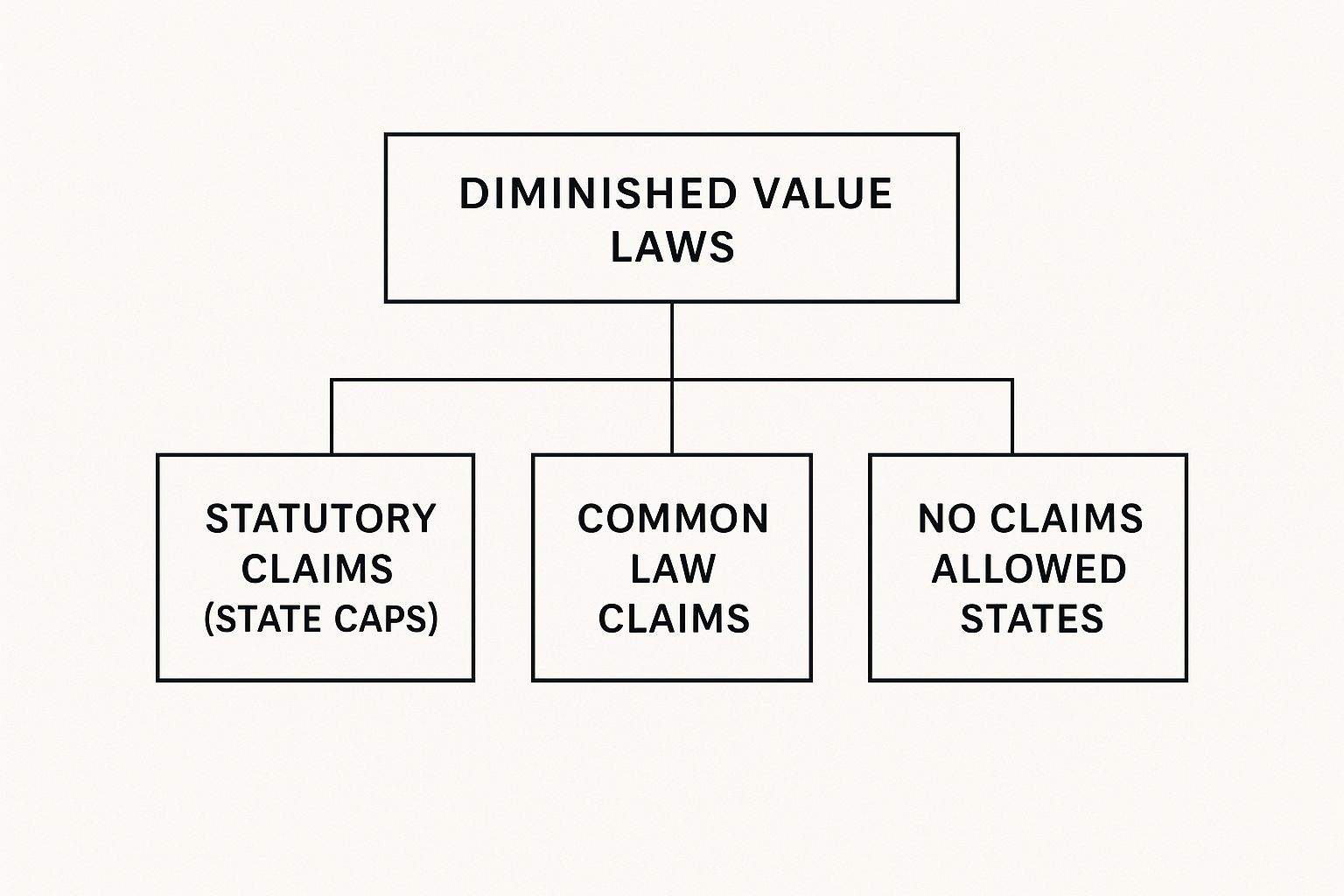

Navigating State Diminished value Laws

Your ability to get paid for your car’s lost value isn't the same everywhere—it’s a patchwork of state-specific rules. The success of your claim lives or dies based on the diminished value laws in your state. Think of it this way: getting the repair bill covered is straightforward, but claiming the lost market value is a different game entirely, with rules that can change the second you cross a state line.

The first and most critical question to answer is whether you're filing a first-party or third-party claim. This single distinction lays the foundation for your entire approach.

- Third-Party Claim: This is when you file against the at-fault driver's insurance. You are the "third party" in this situation. The good news is that the vast majority of states allow you to go after inherent diminished value in a third-party claim.

- First-Party Claim: This is when you file with your own insurance company, usually because you were at fault or the other driver was uninsured. Most states do not allow these claims. The common argument from insurers is that your policy covers the cost to repair the vehicle, not to restore its pre-accident market value.

This difference is everything. If someone else hits you, the path forward is usually much clearer. If you caused the accident, your odds of a successful claim are slim to none in most places.

The Legal Landscape of Diminished Value

State laws on this are constantly being challenged and refined in courtrooms. The legal ground isn't static; it's shifting as more people become aware of their rights and push for more transparent insurance practices.

As consumer rights get more attention, many states have started to strengthen laws that clarify your right to compensation. The big trends are clearing up the gray areas around third-party claims and pushing for independent appraisals over the insurance company's simplistic formulas.

This infographic gives you a bird's-eye view of how different states handle diminished value.

As you can see, your rights really depend on whether your state leans on old court rulings (common law), has specific laws on the books (statutes), or just shuts these claims down.

Strong, Restrictive, and Prohibited States

To make sense of it all, we can group states into three main buckets based on how they treat third-party diminished value claims.

-

Consumer-Friendly States: These states have solid legal precedent or specific laws that fully back a car owner's right to be paid for inherent diminished value. Georgia is famously the strongest state for consumers because it's the only one that even allows first-party claims in certain situations. States like Oregon and Washington also have established case law that makes diminished value a standard part of any third-party claim.

-

Restrictive States: In these states, filing a claim is doable but often an uphill battle. The laws might be vague, or insurers have more power to push back and deny claims at first. To win here, you’ll need rock-solid proof, a professional appraisal, and the willingness to negotiate hard.

-

Prohibited or Difficult States: A handful of states make it nearly impossible to get paid. Michigan, with its no-fault insurance system, is a perfect example where diminished value claims are generally not recoverable. The legal system in these places simply isn't set up to recognize this kind of financial loss.

Crucial Point: These state-by-state differences are exactly why a cookie-cutter approach just doesn't work. A strategy that sails through in a friendly state like Oregon might be dead on arrival somewhere else. For a detailed look at how to apply these ideas in a specific state, check out our guide on how to file a diminished value claim in Oregon.

At the end of the day, the law in your state is the final word. It dictates if you can even file, what proof you'll need, and which arguments will stand up to an adjuster's denials. Knowing where you stand legally is the key to setting realistic expectations and building a case that works.

How to File a Successful Diminished Value Claim

Knowing you're owed money for diminished value is the easy part. Actually getting a check from the insurance company? That’s a different story. Filing a successful claim isn't about making angry phone calls; it's about building a rock-solid case that an adjuster simply can't ignore.

Think of it like you're a detective. Your mission is to gather undeniable proof that your car lost value, then present it so clearly and professionally that there’s no room for argument. The more organized you are, the more seriously they’ll take you.

Step 1: Assemble Your Evidence

Before you even pick up the phone, you need to gather your proof. An organized file of documents is the bedrock of your claim. Without it, your request is just an opinion.

Get a folder—seriously, a physical or digital one—and start collecting everything related to the accident and repairs. This one small step will save you a ton of headaches down the road.

Your evidence file needs to include:

- The Police Report: This is your official proof of who was at fault, which is absolutely essential for a third-party claim.

- Repair Invoices: Grab every receipt and the final, itemized bill from the body shop. This shows exactly what was damaged and fixed.

- Photos and Videos: Visuals are powerful. You need "before" pictures of the accident scene and the damage, and "after" photos of the completed repairs.

- Proof of Value: Dig up documents that show your car's pre-accident condition and value, like the original bill of sale or recent service records.

Step 2: Get an Independent Appraisal

This is, without a doubt, the most important step. The insurance company has its own way of calculating diminished value, and—shocker—it’s usually a formula designed to pay you as little as possible. Never rely on their number.

An independent, certified appraisal is your secret weapon. It's a formal report from an unbiased expert that details your car's specific loss in market value.

A good diminished value report from a certified appraiser isn’t just a number; it’s a detailed argument. It breaks down why your specific vehicle lost value, considering the severity of the damage, your local market, and sales of similar cars. It gives you a realistic, defensible figure to anchor your claim.

Hiring a professional appraiser signals to the insurance company that you mean business. It shifts the conversation from their flimsy internal formula to a real-world discussion based on facts.

Step 3: Write a Persuasive Demand Letter

With your appraisal and evidence file ready, it's time to make your official request. A demand letter isn't the place to vent your frustrations. It should be a short, professional document that lays out the facts and states exactly what you're asking for.

Here’s what your letter should cover, clean and simple:

- Your Information: Name, contact info, and the insurance claim number.

- Vehicle Details: The year, make, model, and VIN of your car.

- Accident Summary: A quick, one-paragraph recap of the accident, confirming the date and that their driver was at fault.

- The Demand: Clearly state the diminished value amount you are claiming, and mention that it's based on your independent appraisal report.

- Attached Evidence: List all the documents you’re sending along with the letter (appraisal, police report, repair bills, etc.).

Send this whole package via certified mail. That way, you have proof they received it. This formal step often gets an adjuster’s attention, showing them you’re organized and won't be easily dismissed. If you feel your vehicle's value has been misrepresented and are contemplating legal action, it's crucial to understand the process when taking legal action with a lawyer's guidance.

Step 4: Navigate the Negotiation Process

Once the adjuster gets your demand letter, expect a phone call. And you can almost guarantee their first offer will be low. That’s just part of the game. Stay calm, be professional, and stick to your facts. If you want a masterclass on this part of the process, learn more about how to negotiate a diminished value claim in our detailed guide.

When they lowball you, push back politely by referencing your appraisal report. Ask them to send you a written explanation of how they calculated their number. You’ll often find they can't defend their formula against a comprehensive, market-based report like yours. This patient, fact-first negotiation is how most successful claims are won.

Proving Your Loss and Calculating Diminished Value

The heart of any diminished value claim isn't just knowing you're owed money; it's proving exactly how much. This is where the real work begins, because you can bet the insurance company has a team of experts dedicated to minimizing that number. Your job is to shift the conversation from their self-serving formulas to a fact-based calculation of your car's actual financial loss.

You can almost guarantee the insurer’s first offer will be disappointingly low. That's by design. They often fall back on a generic, one-size-fits-all calculation, with the most infamous being the "17c formula."

The Problem with the 17c Formula

Named after a Georgia court case, the 17c formula was meant to be a simple starting point. Unfortunately, it's often used by insurers as a tool to crank out consistently low offers. It works by applying a series of arbitrary percentage deductions for things like mileage and damage severity, without ever considering the realities of your specific car or the market where you live.

Here’s why it almost always fails to capture your true loss:

- It ignores your local market: Car values can vary dramatically from one region to another. A sought-after truck in Texas will have a different market value than the same truck in New York. The 17c formula doesn't care.

- It uses arbitrary modifiers: The penalties for mileage or so-called "severe" damage are often just pulled from a pre-made chart and lack any real-world justification.

- It caps the initial value: The formula usually starts by slapping a 10% cap on the vehicle's pre-accident value, guaranteeing the final number is low right out of the gate.

Relying on the 17c formula is like letting the person who crashed into you decide how much they should pay. To get what you're rightfully owed, you have to counter with a superior, evidence-backed calculation.

Building a Credible Calculation

To successfully push back against an insurer's lowball offer, you need to build your own defensible calculation. This isn't about pulling a number out of thin air; it's a methodical process based on hard evidence and real market analysis. While an independent appraiser will handle this for you, understanding the components will make you a much stronger negotiator.

These are the key factors that determine your real-world loss:

- Vehicle History and Condition: This covers the car's age, mileage, specific trim level, and its overall condition before the accident. A pristine, low-mileage vehicle is going to suffer a much greater percentage loss than an older car that already has some wear and tear.

- Severity of Damage: The extent and location of the damage are absolutely critical. Any hint of frame damage, for instance, creates a huge stigma and leads to a much higher diminished value than a minor fender bender.

- Local Market Analysis: This involves digging into what comparable vehicles are selling for in your area. A good appraiser will analyze what similar cars (same make, model, year, and condition) with clean histories are selling for versus those that now have an accident on their record.

Expert Insight: A high-quality appraisal report is your single most powerful piece of evidence. It replaces the insurer's abstract formula with a data-driven narrative, comparing your vehicle to real-world examples and providing a specific, justifiable dollar amount for your loss.

The Power of an Independent Appraisal Report

Think of an independent appraisal as a professional investigation into your car’s lost value. A certified appraiser provides an unbiased, detailed report that insurance companies simply can't ignore. It’s packed with market data, photos, and a clear, logical explanation of how they arrived at the final diminished value figure. This report becomes the anchor for your entire negotiation.

Current vehicle market dynamics make this even more important. In the U.S., the average vehicle age hit a record 12.6 years in 2024. As people hold onto their cars longer, valuing used vehicles properly becomes more complex, making an expert analysis absolutely vital. To see how these factors might affect your specific vehicle, you can explore our helpful car value after accident calculator.

Armed with a professional report, you’re no longer just asking for money—you're presenting a documented, evidence-based case for your true financial damages.

Overcoming Common Insurance Company Tactics

So, you’ve done your homework and put together a rock-solid diminished value claim. You might feel like you're heading for an easy win, but unfortunately, this is often where the real battle begins. Insurance companies are for-profit businesses, and their adjusters are trained to minimize payouts.

Being ready for their go-to moves is the key to turning a frustrating experience into a successful negotiation. Think of it like a chess match; if you know their opening gambits, you won't be caught off guard. You'll see the tactic for what it is and have your countermove ready.

"We Don't Pay for That"

This is the classic first line of defense, especially if you're filing a first-party claim against your own insurance. The adjuster might flatly state that diminished value "isn't a covered loss" under your policy. While they’ll still try this line in a third-party claim (where the other driver was at fault), the argument is much weaker.

The best response is to stay calm and stick to the facts. In a third-party claim, you can politely point out that their client's negligence caused a direct financial loss to you. Under state law, they're obligated to make you whole, and that includes compensating you for the very real drop in your car’s market value.

The Policy Exclusion Argument

This is a more sophisticated version of the first tactic. The adjuster may point to a specific endorsement or clause in the auto policy that they claim explicitly excludes payment for inherent diminished value. This has become a popular strategy for insurers in recent years.

Frankly, the legal ground here is a bit shaky and varies by state. As of 2024, many private insurers have added language defining diminished value as an "indirect loss," which their policies conveniently don't cover. This has cooled some legal challenges as the exclusions become more common. You can get a deeper dive into the insurance industry's perspective on IRMI.com.

Even so, it’s always worth pushing back. The enforceability of these clauses depends entirely on the specific wording and the laws in your state.

Common Tactics to Watch For

Beyond flat-out denials, adjusters have a few other tricks up their sleeves to wear you down. Recognizing them is the first step to not falling for them.

- Delay, Delay, Delay: The adjuster goes silent, taking forever to return calls or emails. This is almost always a deliberate strategy. They hope the frustration will make you either give up or accept the first lowball offer that comes your way. Document everything and be persistent.

- Systematically Low Offers: Their first offer will likely be a laughably low number spit out by a formula like 17c. They're banking on your ignorance. This is precisely why your independent appraisal is your most powerful weapon.

- Using Proprietary Formulas: They might claim their figure is based on a "proprietary market analysis" that—surprise!—they can't share with you. This is a huge red flag. Always insist on a written, detailed explanation of their math.

Crucial Takeaway: An insurance company's initial "no" is not the end of the conversation—it's the beginning of the negotiation. Their tactics are designed to test your resolve. A well-documented claim backed by an independent appraisal is your best defense against these strategies.

When you hit these roadblocks, the key is to stay professional and persistent. Don't let their tactics throw you off your game. Stick to the facts laid out in your evidence and appraisal report. If the insurer simply refuses to negotiate in good faith, it might be time to escalate the claim or bring in a professional to fight on your behalf.

Your Questions About Diminished Value Answered

Diving into a diminished value claim can bring up a lot of practical questions. You get the basic idea—your car is worth less after being wrecked and repaired—but what happens when you actually try to file? It can feel a bit overwhelming.

Think of this as your field guide to the most common "what-ifs" and "how-tos." We’re getting past the theory and into the nitty-gritty of what you'll face.

Can I File a Diminished Value Claim if I Was At Fault?

This is probably the most common question, and it's a critical one. The short answer is almost always no. If you caused the accident, you generally can't file a diminished value claim against your own insurance policy.

Your collision coverage is there to pay for the repairs—to restore your vehicle's function and appearance. It’s not designed to compensate you for the hit to its resale value. Insurance policies are written very precisely to cover direct, physical damage, not the financial stigma that a crash leaves behind.

Now, if another driver was at fault, it’s a completely different story. You would file a claim against their insurance, and in most states, you absolutely have the right to be paid for your car’s diminished value. The big exception is Georgia, which is famously consumer-friendly and does allow some of these "first-party" claims.

Is There a Deadline for Filing a Diminished Value Claim?

Yes, and this is a deadline you simply can't ignore. Every state has a legal time limit for filing property damage claims, which is called the statute of limitations. If you miss this window, you lose your right to collect any money, no matter how solid your case is.

This time limit can vary wildly from one state to another. For some, it might be as short as one year from the date of the accident; for others, it could be several years. It's vital to figure out the statute of limitations in your state right away. Don't wait until the repairs are finished to start looking into it.

Crucial Tip: The clock for your diminished value claim starts ticking on the date of the accident itself, not the day you get your car back from the shop. Waiting is one of the easiest ways to forfeit your claim.

Do I Need a Lawyer for My Diminished Value Claim?

The honest answer? It depends. For many straightforward claims, you can absolutely handle the process on your own. If the value isn't astronomical and you're comfortable gathering documents and negotiating, many people successfully file and settle claims without an attorney.

However, bringing in a lawyer becomes a very smart move in a few key situations:

- You have a high-value vehicle: The more your car is worth, the more you stand to lose—and the harder the insurance company will likely fight. This is especially true for luxury cars, classics, or extensively customized vehicles.

- The damage was severe: Claims involving frame or structural damage are complex. They also lead to the biggest drops in value, making them a prime target for pushback from insurers.

- The insurance company is being difficult: If the adjuster is ignoring you, making ridiculously low offers, or flat-out denying a valid claim, a lawyer can provide the muscle you need.

Hiring an attorney signals to the insurer that you’re serious and won’t be pushed around. This simple act can often force them into a more meaningful negotiation and lead to a much fairer settlement.

Does Diminished Value Apply to a Leased Vehicle?

Yes, the vehicle has definitely lost value, but the person who files the claim changes. When you lease a car, the legal owner is the leasing company—not you. Because of this, the right to file a diminished value claim technically belongs to them.

Don't think that lets you off the hook, though. In fact, it makes the situation even more important for you to handle correctly. Your lease agreement almost certainly holds you responsible for any "excess wear and tear" or loss in market value when you turn the car in. An accident history is a perfect example of this.

You should immediately check your lease agreement and let the leasing company know about the accident. They might pursue the claim themselves, or they might expect you to cover that loss when your lease ends. Tackling this head-on is the only way to avoid a surprise bill for thousands of dollars.

When you're facing a diminished value claim, you don't have to take on the insurance company alone. Total Loss Northwest specializes in providing certified, independent appraisals that give you the leverage to demand a fair settlement. We arm you with the evidence you need to prove your true loss. Learn how our expert appraisal services can help you get what you're rightfully owed.