Even after your car has been expertly repaired following an accident, its value will never be the same. That drop in its market price is known as diminished value, and it's a real financial loss you're entitled to recover.

What Is Diminished Value and Why Does It Matter?

Let’s run a quick thought experiment. Imagine two identical cars for sale on a lot—same make, model, year, and mileage. The only difference is that one has a squeaky-clean vehicle history report, while the other was in a collision six months ago.

Which one are you buying?

If you're like most people, you'd pick the one without the accident history. Or, at the very least, you'd expect a hefty discount on the one that's been wrecked. That price difference right there? That’s the diminished value in a nutshell. It’s the immediate, and permanent, drop in what someone is willing to pay for your car simply because it now has a permanent blemish on its record.

Think of it this way: a rare book that’s been torn and then meticulously glued back together will never be worth as much as a pristine copy. The damage is part of its story forever. The same goes for your car.

Perfect Repairs Don't Erase the Stigma

The simple truth is that no repair job, no matter how flawless, can completely erase the fact that your vehicle was in an accident. That collision is now a permanent part of its history, and it will show up on reports from services like CarFax or AutoCheck for any future buyer to see.

This history creates doubt. A potential buyer will always wonder if there’s hidden frame damage or if the repairs will hold up over time. That uncertainty directly translates into a lower resale value. This is a very real financial loss, and it’s completely separate from the money paid to the body shop for the repairs.

The at-fault driver's insurance company is responsible for making you whole again, which should include compensating you for this lost equity. Depending on the car and the severity of the damage, this loss can easily be 10% to 30% of the vehicle's pre-accident value. For a deeper look at how these numbers vary, you can find more details about diminished value claims in your state.

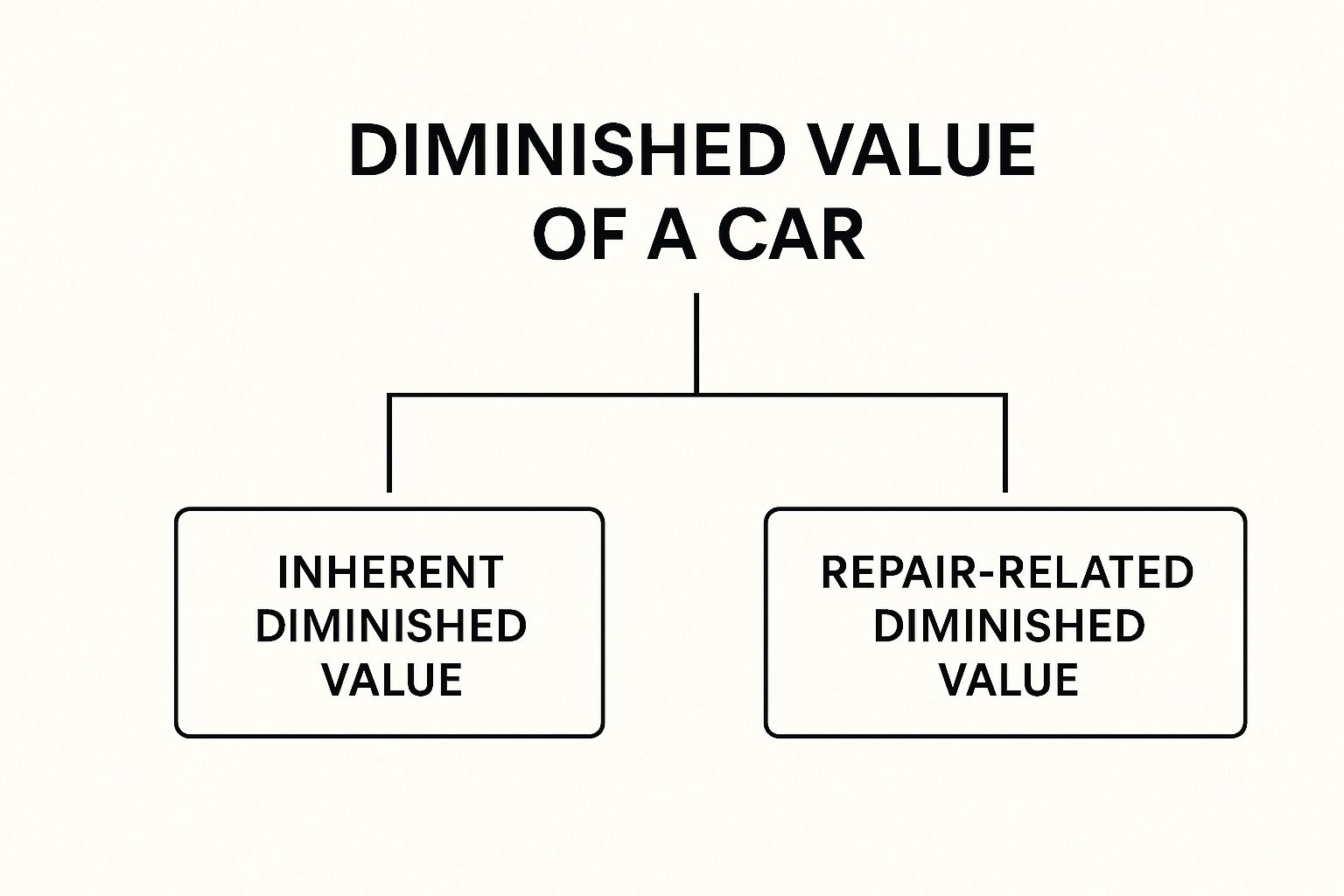

As you can see, diminished value isn't just one single concept. It actually breaks down into a few distinct categories based on the quality of repairs and the market's perception.

The Three Types of Diminished Value Explained

Getting familiar with the different kinds of diminished value is crucial for building a solid claim. Each type pinpoints a specific way your vehicle has lost money.

The table below breaks down the three main categories you'll encounter.

| Type of Diminished Value | When It Applies | Example Scenario |

|---|---|---|

| Inherent Diminished Value | The most common type. It assumes perfect repairs but acknowledges the automatic loss in value from the accident history itself. | Your car gets rear-ended. The body shop does a fantastic job, and it looks brand new. Still, its CarFax report now shows an accident, making it worth $2,500 less. |

| Repair-Related Diminished Value | This applies when the repairs are subpar, causing an additional loss in value on top of the inherent loss. | The new paint on the bumper doesn't quite match the rest of the car, and the shop used a cheaper aftermarket headlight instead of an original one. |

| Immediate Diminished Value | This is the loss in value immediately after the accident, before any repairs are made. It's often used when a vehicle is a total loss. | Your car is damaged, and its resale value is measured as-is before it's taken to the shop. This is less common in claims where the vehicle is repaired. |

Essentially, most claims focus on Inherent Diminished Value. This is the unavoidable financial hit your car takes just by having an accident on its record. Any shoddy repair work just makes the situation worse.

Diminished Value vs. Normal Depreciation

One of the first hurdles you'll face when filing a diminished value claim is the insurance adjuster. They often try to muddy the waters by lumping your specific loss in with the normal depreciation every car experiences. This isn't an accident; it's a tactic.

They want you to think it's all the same, hoping you'll give up or accept a lowball offer. That’s why your first line of defense is knowing the difference—and it's a big one.

Let’s break it down with an analogy. Normal depreciation is like a slow, predictable leak in a tire. You know it's going to happen over time. Every mile you drive, every year that passes, a little bit of value seeps out. It’s the expected loss from age, mileage, and regular wear and tear.

Diminished value, however, is like hitting a massive pothole that instantly bends the rim. It's not a slow leak; it's a sudden, violent event that immediately damages your car's worth. The accident is that pothole.

The Predictable Path of Depreciation

Every car starts losing value the second you drive it off the lot. That's just a fact of life. This slow, downward slide is driven by factors that have nothing to do with a collision.

Here's what fuels normal depreciation:

- Age: Newer models with better tech come out every year, making older cars less desirable.

- Mileage: The more miles on the odometer, the more wear on the engine, transmission, and everything else.

- Wear and Tear: Faded paint, scuffed seats, and worn tires are all part of a car’s life story.

- Market Demand: Some cars, like a popular truck or a reliable sedan, hold their value better than others.

A car’s value is supposed to follow a smooth depreciation curve, gradually decreasing over its lifespan. An accident shatters that curve. It creates an instant, vertical drop in value that top-notch repairs can’t fully restore.

For a deeper dive into the factors that affect a car's worth over its lifetime, you can learn more about understanding normal car depreciation. This predictable loss is the baseline we work from, but it's not what your claim is about.

The Unpredictable Impact of an Accident

Unlike the steady march of time, diminished value is a direct financial injury caused by someone else's negligence. It’s the loss that happens because of the collision.

Even if your car looks perfect after repairs, its history is permanently scarred. That accident report will follow it forever, and any savvy buyer will use it to negotiate a lower price. That difference in price is your diminished value.

This is the key distinction. Your claim isn't for the value your car lost last year. It’s for the value it lost the very instant it was hit.

So, when the adjuster tells you, "We don't pay for depreciation," you'll be ready. You can confidently reply, "I'm not asking you to. I'm demanding compensation for the diminished value—the immediate loss in market value caused by your insured driver."

Knowing this simple but powerful difference puts you in control of the conversation and keeps your claim on solid ground.

How to Calculate Your Diminished Value

This is where the rubber meets the road. Turning that abstract idea of "lost value" into a hard dollar amount is the whole point of a diminished value claim. But be warned: how you calculate that number makes all the difference.

Insurance companies have their preferred methods, and—no surprise—they tend to favor their own bottom line. To get what you're truly owed, you need to understand their playbook and know when it’s time to call in an expert.

The Insurer's Go-To Formula: Rule 17c

When you file a claim, the insurance adjuster will likely pull out a formula known as “Rule 17c.” It sounds official, but it's not a law. It's just a quick and easy calculation that originated from a single court case years ago, and insurers love it because it almost always spits out a lowball number.

Here's how it generally works. First, the formula caps your maximum possible loss at 10% of your car’s pre-accident value (think NADA or Kelley Blue Book). Then, it starts chipping away at that number with a couple of modifiers.

The Rule 17c formula typically works like this:

- Base Loss Cap: Your claim is immediately capped at 10% of your car’s fair market value before the crash.

- Damage Multiplier: This 10% figure is then multiplied by a factor from 0.00 to 1.00. Minor dents might get a 0.25 multiplier (a huge reduction), while serious frame damage might get a 1.00 (no reduction).

- Mileage Penalty: Finally, that new, lower number is reduced again for high mileage. If your car has over 100,000 miles, the formula might slice the remaining value in half.

The biggest problem with Rule 17c is that it’s completely disconnected from reality. It's a blunt instrument that ignores what a real buyer in your local market would actually pay for a car with an accident history.

This cookie-cutter approach doesn't care about your car's specific make and model, its condition, or the unique stigma attached to its repair history. It's designed for one thing: minimizing the payout. If you're curious what an insurer might offer, you can play around with a diminished value claim calculator to see a rough estimate based on this logic.

The Superior Method: Hiring an Independent Appraiser

While a formula can give you a ballpark figure, the only truly accurate way to pin down your car's diminished value is to hire a licensed, independent appraiser.

Think of it this way: the insurance company's formula is their opinion. An independent appraiser’s report is expert testimony backed by hard evidence.

These professionals don't rely on arbitrary multipliers. Instead, they conduct a detailed market analysis. They’ll compare your repaired vehicle to identical, accident-free cars for sale in your area. They’ll even call local dealership managers to ask point-blank, "How much less would you offer for this car on a trade-in, knowing it was in a wreck?"

The result is a comprehensive report that stands up to scrutiny—one that reflects your actual, real-world financial loss.

To see just how different these two approaches are, let's compare them side-by-side.

Comparing Diminished Value Calculation Methods

| Method | Who Uses It | Pros | Cons |

|---|---|---|---|

| Rule 17c | Insurance Companies | Fast and simple to calculate. | Inaccurate; uses arbitrary caps and multipliers; ignores market realities; produces a lowball figure. |

| Independent Appraisal | Vehicle Owners & Attorneys | Based on real-world market data; highly credible and defensible; customized to your specific vehicle and accident. | Requires an upfront cost; takes more time and effort than a simple formula. |

Ultimately, while the insurer's formula is a starting point for negotiation, a professional appraisal is the evidence you need to finish the conversation on your terms.

Preparing Your Documentation for an Accurate Appraisal

Whether you’re pushing back against a low offer or arming your appraiser with everything they need, solid paperwork is your best friend. A well-organized file shows the insurance company you’re serious and prepared.

Get these documents together before you make the call:

- Pre-Accident Value: A printout from a site like KBB or NADA showing your car’s value right before the accident.

- Official Accident Report: The police or collision report is crucial for establishing fault and the facts of the crash.

- Detailed Repair Invoices: The final, itemized bill from the body shop. This is proof of every single part and labor hour that went into the repair.

- Photographs: Collect photos of the damage before repairs and clear pictures of the finished work.

- Proof of "Loss of Use": Did you need a rental car? Keep those receipts. While not a direct part of the DV calculation, it helps build the full picture of your financial losses.

Having this information ready from the start makes the entire process smoother and significantly strengthens your position.

Filing Your Diminished Value Claim Step by Step

You’ve done the hard work of calculating your car's lost value and gathering the evidence. Now, you’re no longer just someone who was in an accident; you're the architect of your own financial recovery. It’s time to put that preparation into action.

Filing a claim for the diminished value of a car is a methodical process. Think of it like building a legal case—each step lays the groundwork for the next. If you follow this roadmap carefully, you’ll dramatically boost your odds of getting the settlement you deserve.

Step 1: Confirm Your Eligibility

Before you dive in, you need to make sure you're actually eligible to file a claim. This is a crucial first step that can save you a lot of time and frustration down the road.

Eligibility really boils down to two things. First, you must not be the at-fault driver. Diminished value is almost always a third-party claim, meaning you file it against the insurance of the person who hit you. Their mistake is what caused your car's value to drop.

Second, your state's laws matter. Most states are on your side and allow for these types of claims, but a few have some tricky restrictions. A quick search for "diminished value laws in [Your State]" will give you a clear picture of where you stand.

Step 2: Notify the At-Fault Insurer

Once you know you're eligible, it’s time to officially inform the at-fault driver's insurance company that you intend to file a diminished value claim. Don't do this over the phone. A verbal conversation can easily be forgotten or misinterpreted.

Instead, send a formal letter or email. This creates a paper trail and shows you mean business. Keep it short and sweet for now.

Your notification should include:

- Your name and contact details.

- The date of the accident and the property damage claim number.

- A clear statement that you are making a claim for your vehicle’s diminished value.

- A quick note that you will be sending supporting documents, including an expert appraisal, very soon.

This initial contact sets a professional tone and lets the insurer know you understand your rights from the get-go.

Step 3: Assemble Your Demand Packet

This is where all your preparation comes together. Your "demand packet" is the collection of all your evidence, organized into a powerful, undeniable case for your loss. The goal is to make it so thorough that the insurance adjuster has very little room to push back.

Think of it as anticipating every question they might have and providing the answer before they can even ask.

Your demand packet is more than just paperwork; it’s the story of your financial loss. It should logically walk the adjuster from the car's pre-accident condition to its post-repair loss in market value, with every step backed by credible evidence.

The absolute star of this packet is your independent appraisal report. This document is your expert testimony. You’ll include it along with everything else you’ve gathered—the repair invoices, the official accident report, and proof of your car's pre-accident value.

Step 4: Write and Send Your Demand Letter

The demand letter acts as the cover letter for your entire evidence packet. It’s a formal document that lays out the facts, summarizes your argument, and makes a specific demand for payment. This isn’t the place for emotion; keep it professional, factual, and firm.

For a deep dive into writing a powerful letter, you can check out our detailed guide on how to write a compelling insurance demand letter.

Your letter should hit these key points:

- Introduction: State the claim number and clearly say you are seeking compensation for your car's diminished value.

- Evidence Summary: Briefly mention the documents you’ve enclosed, pointing to the independent appraisal as the foundation for your claim amount.

- The Demand: State the exact dollar amount you are demanding—this should be the figure directly from your appraisal.

- Call to Action: Give the insurer a reasonable deadline to respond, usually 15 to 30 days.

Send the whole package—the letter and all your proof—using certified mail with a return receipt. This gives you legal proof that they received it. Once that’s done, the ball is officially in their court.

Overcoming Common Insurance Company Roadblocks

Once you’ve sent in your demand letter and appraisal, get ready for the next phase. Insurance companies are in the business of minimizing payouts, so don't be surprised when you get some pushback. This isn't a sign that your claim is weak; it's just how the game is played. Now is the time to stand your ground, armed with solid evidence.

The best way to win this negotiation is to know their playbook. You’re going to hear a few standard lines designed to make you second-guess yourself. If you're prepared for them, these roadblocks become nothing more than minor hurdles.

"Your Car Was Restored to Pre-Accident Condition"

This is the most common argument you'll face, and it's built on a faulty premise. The adjuster is intentionally mixing up your car's physical condition with its market value. They are two very different things.

Your response can be straightforward: "I agree the repairs did a great job restoring the car's function and appearance. My claim, however, is for Inherent Diminished Value. This is the loss in resale value that happens simply because the vehicle now has an accident history tied to its VIN." You can gently remind them that no body shop can erase a CarFax report, which is what savvy buyers look at first.

"We Don't Pay for Diminished Value"

This one is usually a bluff. Unless you’re in one of the very few states that explicitly bars third-party diminished value claims, this statement is just not true. It's a tactic to get you to drop the claim before it even gets started.

Politely flip the script and put the burden of proof back on them. A good response is, "I understand. Could you please point me to the specific state law or court case that prevents you from covering this type of property damage?" Nine times out of ten, they can't, and they'll have to move on from this weak argument.

An insurance company's initial "no" is rarely the final word. Think of it as their opening offer in a negotiation. Your job is to show them you know the rules and you're ready to play.

Diminished value claims are a huge, often overlooked part of auto insurance settlements. The financial stakes are higher than you might think. With nearly 3% of car loans recently hitting serious delinquency and about 25% of new car loans being underwater by an average of almost $7,000, every dollar counts. These market pressures, detailed in a CCC Intelligent Solutions report, show just how vital recovering the diminished value of a car is to your financial stability.

"Your Appraisal Is Too High"

If they can't deny the claim outright, they'll attack your evidence. The adjuster will likely claim your independent appraisal is inflated and counter with a lowball offer, usually generated by their own internal, one-size-fits-all formula.

This is where your detailed appraisal report really shines. Point them directly to the specific market data and quotes from local dealerships included in your report. Make it clear that your valuation is based on real-world numbers from your local market, not some generic algorithm. This is a great point in the process to sharpen your skills on https://totallossnw.com/how-to-deal-with-insurance-adjusters/ and their negotiation tactics. It's also smart to be aware of the common insurance claim denial reasons so you can head off other potential issues.

When to Escalate Your Claim

What if the adjuster just won't budge? If they continue to stonewall, lowball, or flat-out ignore you, it's time to go up the ladder. Your first step is to politely ask to speak with a supervisor. Managers have more authority to approve a settlement and are often more motivated to resolve the issue without further conflict.

If that doesn't work, the next step is to inform them that you are prepared to file a lawsuit in small claims court. Just mentioning this can dramatically change the tone of the conversation. For the insurance company, the cost and hassle of paying a lawyer to show up in court often outweighs the amount you're claiming. Suddenly, a fair settlement starts to look like a much better option for them. It shows them you're serious and won't be easily dismissed.

Your Diminished Value Questions Answered

You’ve learned the ropes of a diminished value of a car claim—what it is, why it matters, and how to build a strong case. But as you get ready to file, you’re bound to have some specific questions pop up. Let’s tackle the most common ones head-on so you can move forward with confidence.

Can I File a Diminished Value Claim with My Own Insurer?

This is a classic point of confusion, and the answer is almost always no. You can’t file a diminished value claim against your own insurance policy.

Think of it this way: your policy is designed to cover the physical damage to your car. A diminished value claim, on the other hand, is considered a "third-party" claim. You file it against the insurance company of the driver who caused the accident because their client's negligence is what caused your car to lose market value. They're responsible for making you whole, which includes both the repair costs and the drop in resale value.

While a couple of states have some weird exceptions, the tried-and-true path is to go after the at-fault driver's insurer.

Is There a Deadline for Filing a Diminished Value Claim?

Absolutely, and it's a deadline you do not want to miss. Every state has a statute of limitations for property damage claims, which is just the legal term for the time limit you have to file a lawsuit after an incident.

This time frame can be anywhere from two to six years, depending on where you live. You need to find out your state’s specific deadline right away. If you miss it, you forfeit your right to seek compensation forever, no matter how solid your claim is. The best advice? Get the ball rolling as soon as your car repairs are finished.

Don’t view the statute of limitations as a suggestion—it's a hard legal cutoff. Procrastinating can cost you thousands of dollars, as insurance companies have no obligation to consider a claim filed even one day past the deadline.

Waiting not only puts you at risk of missing the deadline but also makes it harder to gather fresh market data and all the documents you'll need for your appraisal.

Should I Hire an Attorney for My Claim?

Whether you need a lawyer really depends on two things: how much money is at stake and how much pushback you're getting from the insurance company.

Here’s a simple way to look at it:

- For smaller claims (usually under $5,000): An attorney’s fees might gobble up a big chunk of your settlement. It often makes more sense to handle these claims yourself or take them to small claims court.

- For high-value claims (often $10,000+): If your car is a luxury model, a classic, or brand new, the diminished value can be significant. This is where an attorney's expertise can be a game-changer.

An attorney is especially helpful when the insurance adjuster is using hardball tactics, flat-out denying a valid claim, or refusing to negotiate fairly. The threat of a lawsuit is a powerful tool, and a good lawyer can often negotiate a settlement that’s far higher than what you could get on your own, easily justifying their fee.

If you're dealing with a stubborn insurance adjuster or just feel in over your head, you don't have to handle it alone. The experts at Total Loss Northwest specialize in certified, independent appraisals that insurance companies have to take seriously. We fight to get you the full, fair compensation you’re legally owed. Get the expert help you deserve by visiting https://totallossnw.com today.