The repairs are finished and your car looks great, but it's now worth a lot less than it was just before the crash. This is the reality of diminished value—it's the silent financial hit your vehicle takes, even when the repairs are picture-perfect. This drop in market value is permanent, all because the car now has an accident on its record.

Your Car's Hidden Financial Loss After an Accident

Picture two identical used cars sitting side-by-side on a dealer's lot. Same make, model, year, and mileage. The only difference? One has a clean vehicle history report, while the other shows it was in a major collision.

Even if the repairs on the second car were flawless, a smart buyer will almost always pick the one with no accident history. If they do consider the repaired car, they’ll demand a serious discount. This simple scenario is the very definition of diminished value. It's not about how well the car was fixed; it’s about the permanent stigma that comes with an accident history.

This loss is real, tangible, and something you can often recover from the at-fault driver's insurance company.

Before we dive deeper, let's break down the core concept.

Diminished Value at a Glance

| Concept | Explanation |

|---|---|

| Core Idea | The reduction in a vehicle's market value after it has been damaged and repaired. |

| Why It Happens | Buyers are less willing to pay full price for a car with an accident history, regardless of repair quality. |

| Who Is Responsible | Typically, the at-fault party's insurance is responsible for covering this loss. |

| Your Goal | To file a claim to be compensated for this "hidden" financial damage. |

This table captures the essence of what you're up against, but the real-world numbers can be shocking.

The Financial Hit Is Bigger Than You Think

The financial fallout from diminished value can be substantial. On average, a vehicle involved in a significant accident can lose between 10% and 25% of its pre-accident trade-in value.

Let's put that into perspective. Say your 2018 Honda Accord was worth $20,000 before the collision. After repairs, its new accident history could slash its market value down to just $15,000. That's a $5,000 loss that has nothing to do with the quality of the bodywork.

This financial damage shows up in a few critical ways:

- Lower Resale Value: When it’s time to sell or trade in your car, you'll be offered a lot less than you would have without the accident on its record.

- Reduced Trade-In Equity: Diminished value directly eats away at your vehicle's equity, leaving you with less cash to put toward your next car.

- An Uncompensated Loss: If you don't file a successful claim, this loss comes straight out of your pocket, even though the accident wasn't your fault.

A vehicle's history is a permanent part of its identity. An accident record creates doubt in a buyer's mind, and that doubt always translates to a lower market price.

Recognizing this hidden loss is the first and most important step. Even small cosmetic issues can have an outsized impact on what someone is willing to pay, which is why it's worth understanding how dents and scratches impact a car's value.

Throughout this guide, we'll walk you through the process of identifying and reclaiming the value your vehicle has lost.

The Three Types of Diminished Value Explained

When we talk about the diminished value of a car after an accident, it's not some vague, catch-all term. It’s actually an umbrella concept that covers three specific kinds of financial loss. Each one comes into play at a different point in the accident and repair process.

Think of it like this: if you had a brand-new designer handbag and it got a deep scratch, even a master craftsman's repair wouldn't make it "new" again. The bag is functional, but its history is forever changed, and its resale value takes a hit. Your car is no different.

Let's unpack these three distinct types of diminished value. Understanding which one applies to your situation is the key to building a solid claim.

Inherent Diminished Value

This is the big one—the most common and unavoidable type of loss. Inherent diminished value is the instant drop in your car’s market value simply because it now has an accident on its record. Even with absolutely perfect repairs from the best technicians using factory parts, the vehicle is permanently stigmatized.

Picture two identical SUVs for sale on a used car lot. Same year, same mileage, same condition—at least on the surface. But when you pull up a CarFax report, you see one was in a moderate front-end collision. Which one do you buy?

Nearly every buyer would pick the accident-free vehicle or demand a hefty discount on the one that's been wrecked. That price gap is its inherent diminished value. It's a loss driven entirely by market perception and the car's documented history, something no amount of bodywork can ever erase.

Key Takeaway: Inherent diminished value exists no matter how good the repairs are. It’s the market’s response to the fact that an accident happened in the first place.

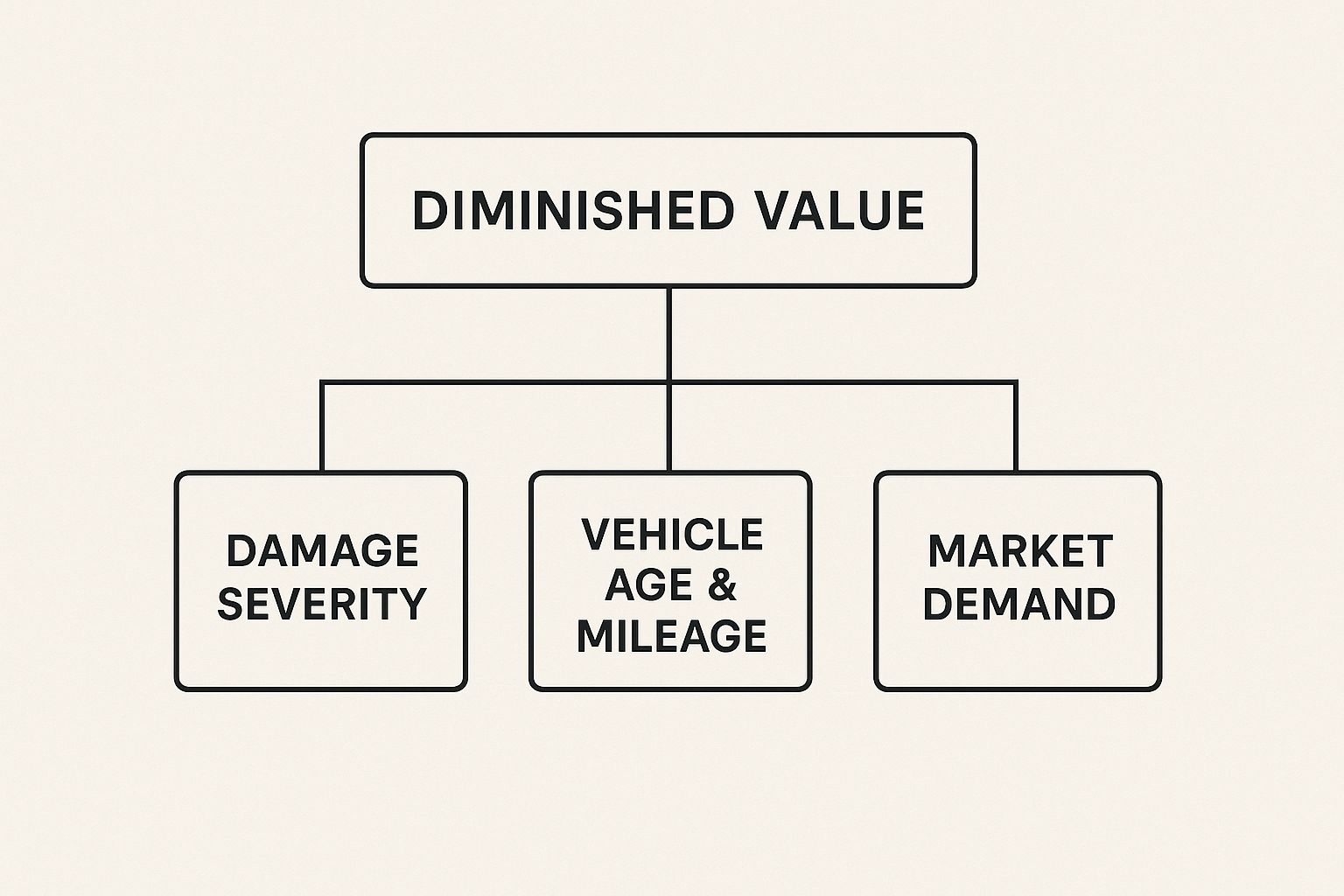

This infographic breaks down the key factors that determine how much value is lost.

As you can see, the hit your car takes depends heavily on the crash severity, the vehicle's age and mileage, and its general desirability in the market.

Repair-Related Diminished Value

While inherent diminished value assumes flawless repairs, repair-related diminished value is what happens when the fix is anything but. This loss is a direct consequence of subpar workmanship, cheap materials, or the use of aftermarket parts instead of genuine ones from the original manufacturer (OEM).

The signs of a bad repair job can be obvious or subtle:

- Mismatched Paint: You can see a slight difference in the color or finish of a new body panel, especially in direct sunlight.

- Uneven Panel Gaps: The spaces around the doors, hood, or trunk are inconsistent, a dead giveaway that things weren't put back together correctly.

- Unseen Structural Flaws: Frame damage that wasn't properly straightened can cause chronic alignment problems, uneven tire wear, and even compromise the car's safety.

- Aftermarket Parts: Using cheaper, non-OEM parts can affect performance and durability, and it's a huge red flag for savvy buyers of luxury or newer cars.

Unlike inherent loss, this type of diminished value is completely on the repair shop. When a potential buyer or a trade-in appraiser spots these issues, they become powerful bargaining chips to drive down the car's price.

Immediate Diminished Value

The third category, immediate diminished value, is a bit more technical. It's the on-paper loss in value right after the crash, before any repairs have been done. In simple terms, it's what your car is worth in its mangled, post-accident state.

This calculation is most often used by insurers to determine if a vehicle is a total loss—meaning the cost to fix it is more than the car is worth. For most everyday claims, you'll be focusing on inherent and repair-related diminished value, since those reflect the loss you're left with after your car is back on the road.

Grasping these differences is critical. In 2022, about 4.54% of policyholders with collision coverage filed claims where diminished value was a real factor, but far too many drivers don't know they can—and should—pursue that lost value. By identifying the specific type of loss you've suffered, you can make a much stronger, more precise case to the insurance company.

How to Calculate Your Car's Diminished Value

So, how do you actually figure out the diminished value of a car after an accident? It can feel a bit like trying to grab smoke—how do you put a hard number on something as fuzzy as "market perception"?

Insurance companies have a go-to method, but it's important to understand that their formula is just one way of looking at it, and it's usually the one that saves them the most money.

Most adjusters will pull out a formula known internally as "Rule 17c." It’s not a law, but it’s a standardized calculation many insurers use to produce a quick, low-ball offer. Knowing how it works is your first step toward pushing back effectively.

Unpacking the Infamous Rule 17c

Think of Rule 17c as a rigid, step-by-step math problem designed to put a neat and tidy number on your loss. It’s a predictable process that almost always works in the insurer's favor.

Here’s the basic breakdown:

- Find the Ceiling: The calculation starts by capping the maximum possible diminished value at 10% of your car’s pre-accident value. For a car worth $30,000, the absolute most you could get is $3,000.

- Apply a Damage Modifier: This $3,000 figure is then multiplied by a "damage severity" score, usually a number between 0 and 1, which the adjuster assigns based on their assessment.

- Apply a Mileage Modifier: Finally, they multiply that new number by another modifier based on your car's mileage. Higher mileage means a lower payout.

What you're left with is a figure the insurance company can present as a "fair" settlement. But this cookie-cutter approach has some serious blind spots.

Crucial Insight: The Rule 17c formula completely ignores real-world factors. It doesn’t care about local market demand, your vehicle's desirability, or the specific stigma that comes with something like frame damage. It's a one-size-fits-all solution for a problem that is anything but.

Because of this, you should always treat the insurer’s first number as exactly what it is: a starting point for negotiation, not the final word.

Beyond the Formula: A Better Approach

A far more accurate and credible way to calculate diminished value is to conduct a comparative market analysis. This is how real buyers and car dealers figure out what a car is actually worth. It’s not about abstract formulas; it’s about what the market says.

This method involves finding real-world examples of cars just like yours—some with a clean history and others with an accident on record. By looking at the difference in asking prices, you can build a powerful, evidence-based case for your car’s true loss in value.

Here’s what a proper analysis looks like:

- Vehicle Comparison: An appraiser finds vehicles of the same make, model, year, and trim level for sale in your area.

- Condition Matching: They then account for differences in mileage, options, and overall condition to create a true apples-to-apples comparison.

- Accident History Impact: The key is to compare the market price of the clean-history cars to those with a documented accident similar to yours.

This process gives you a number grounded in reality. If you want a quick estimate to see what you might be looking at, a high-quality diminished value claim calculator can give you a solid ballpark figure before you hire a professional.

Ultimately, a detailed report from a certified appraiser is your best weapon. It swaps the insurance company's self-serving formula for undeniable market facts, giving you the leverage you need to get a fair settlement.

How to Navigate the Insurance Claim Process

Filing a claim for your car's diminished value after an accident can feel like you're about to step into a bureaucratic maze. But it doesn't have to be that complicated. With the right approach, you can successfully get back the money you're owed. This isn't about luck; it's about being prepared, organized, and persistent.

First, let's get a key rule straight. You can almost always only file a diminished value claim if you weren't the one at fault. This means you’ll be filing what’s called a third-party claim against the other driver’s insurance. Their policy is on the hook not just for fixing your car, but for making you "whole" again—and that includes paying you for the hit your car’s market value has taken.

When Is the Right Time to File Your Claim?

Timing is everything here. You might feel an urge to get the ball rolling right after the crash, but the best time to officially file your diminished value claim is after all the repairs have been completed.

Why the wait? It's simple. Filing after the work is done lets you show the insurance company the full story. The final repair bill is hard evidence of how serious the accident was, and it allows you to see for yourself how good (or not so good) the repair job was. Trying to file sooner gives the insurance company an easy way to dismiss your claim as just speculation.

Think of it this way: a diminished value claim is for the permanent loss in value after the car has been fixed. Filing before repairs are done is like trying to sell a house before you know the full extent of its foundation damage. It’s jumping the gun, and it weakens your position.

So, once you have your car back from the shop, it’s go-time. A strong claim is a well-documented one. You’ll need more than your word to convince an adjuster to write that check.

Your Evidence-Building Checklist

It’s helpful to think of yourself as a detective building a case. Every document, photo, and report you gather makes your claim stronger and makes it that much harder for the insurance company to push back or lowball you. The goal is to leave no room for doubt.

Here’s the essential documentation you’ll want to have in hand:

- The Official Police Report: This is your foundation. It establishes who was at fault, which is what makes your third-party claim possible in the first place.

- Photos and Videos: A picture really is worth a thousand words. Collect photos from before the accident (if possible), right after the crash happened, and after the repairs are finished. This visual timeline tells a powerful story.

- Complete Repair Invoices: Make sure you get a detailed, itemized list of every single part that was replaced and all the labor costs. This invoice is undeniable proof of the accident's severity.

- Pre-Accident Value Assessment: You need a baseline. Use trusted resources like Kelley Blue Book or NADA guides to establish what your vehicle was worth the moment before the collision.

- A Professional Diminished Value Appraisal: This is your ace in the hole. An independent, certified appraisal gives you an expert, unbiased calculation of exactly how much value your car has lost.

Once you have this evidence packet put together, you’re ready to officially submit your claim to the at-fault driver's insurance company. Just be prepared for a bit of a fight.

Getting Past the Initial Pushback

It’s incredibly common for an insurance adjuster’s first response to be a flat-out "no." They might say their company doesn't cover diminished value, or that their job was done once they paid the repair bill. Do not take this as the final answer.

More often than not, this initial denial is a standard play from their book. They're testing you to see if you're serious. Your job is to respond calmly, professionally, and with the mountain of evidence you've just collected.

Here’s how to handle it when they try to shut you down:

- Stay Professional: Keep every conversation and email polite and based on the facts. Getting emotional won't help your cause.

- Present Your Appraisal: The moment they deny your claim, counter by sending them the professional appraisal report. This changes the conversation from their opinion to an expert’s documented findings.

- Follow Up Consistently: Adjusters are juggling dozens of cases. A gentle but firm follow-up email or call shows them you mean business and aren’t going to just disappear.

- Put Everything in Writing: After any phone call, send a quick email summarizing what you talked about. This creates a paper trail and keeps everyone on the same page.

Getting through this process takes some patience. But by following these steps and building a rock-solid case, you dramatically improve your odds of getting back the money your car rightfully lost in value.

Why a Professional Appraisal Is Non-Negotiable

Trying to prove the diminished value of a car after an accident with an online calculator is like walking into a courtroom with a blog post as your star witness. It just won’t hold up. If you want to win your claim and get a fair settlement, you need rock-solid, undeniable proof. That proof comes from a professional, independent appraisal.

Think of a certified appraiser as an expert witness for your vehicle. They are a neutral third party, and their only job is to figure out the true financial hit your car has taken. The report they produce isn't just a number; it's a detailed, data-driven document that gives you the muscle you need to push back against the insurance company's inevitable lowball offer.

An insurance adjuster’s job is to close your claim for as little money as possible. Your appraiser's job is to establish the facts. That's a huge difference, and it's exactly why an independent report is a must-have.

What a Comprehensive Report Contains

A real diminished value appraisal is much more than just plugging numbers into some generic formula. It's a deep dive into your vehicle’s condition, the quality of the repairs, and how it now stacks up in the actual used car market.

A quality report will always include:

- A Thorough Physical Inspection: The appraiser gets hands-on with your vehicle, looking for the little things a casual glance would miss—like mismatched paint, uneven panel gaps, or lingering signs of structural work.

- Repair Quality Analysis: They’ll go through the repair invoices with a fine-tooth comb. Were cheaper aftermarket parts used instead of genuine OEM parts? That alone can tank your car’s value.

- Market Data Comparison: The appraiser pulls real-world sales data from your local area, comparing your repaired car to similar, accident-free models on the market. This creates a clear, evidence-based picture of the value that's been lost.

This meticulous process reveals the true financial damage. For instance, even with flawless repairs, a car can lose 20% of its value simply from having an accident on its history report. If the repairs are shoddy, that loss can shoot up to 50%, especially if there was frame damage or the cosmetic flaws are obvious. You can discover more about how repairs impact a car's inherent value at IRMI.com.

How to Find a Reputable Appraiser

Not all appraisers are the same. The credibility of your report hinges entirely on the expert who writes it, so choosing the right one is a make-or-break moment for your claim.

When you're looking for an appraiser, make sure they check these boxes:

- Certifications and Experience: Look for someone certified by a recognized organization who has a ton of experience dealing specifically with diminished value claims.

- Unbiased and Independent: They need to be working for you, not the insurance company. Steer clear of anyone with close ties to insurers, as you can't be sure their assessment is truly neutral.

- A Proven Track Record: Don't be afraid to ask for sample reports and check their testimonials. A good appraiser will have a long history of writing solid, defensible reports that get results for their clients.

A professional appraisal turns your claim from a simple disagreement over opinions into a negotiation based on facts. It throws out the insurer's self-serving formula and replaces it with hard data, forcing them to deal with the real-world loss you've actually suffered.

At the end of the day, a detailed, professional report is the most powerful tool you have. For a closer look at the process, check out our guide on what a diminished value appraisal entails. It’s a small investment that can stop you from leaving thousands of dollars behind.

State Laws and Legal Considerations for Your Claim

When it comes to getting paid for your car's diminished value, one of the biggest factors is completely out of your hands: where you live. The rules for these claims can change dramatically from one state line to the next, so getting a handle on the local legal landscape is the first step toward building a strong case.

The most critical piece of this puzzle is understanding the difference between a first-party and a third-party claim. This single distinction usually decides whether you can even file for diminished value in the first place.

First-Party vs. Third-Party Claims

Let’s boil it down to one simple question: who caused the accident? The answer to that question determines what kind of claim you’ll be making, and it has a massive impact on your odds of getting paid.

-

First-Party Claim: This is when you file with your own insurance company. In almost every state, you simply cannot claim diminished value from your own insurer. The logic here is that your policy is a contract to repair your vehicle, not to protect its resale value after an accident.

-

Third-Party Claim: This is when you file against the insurance company of the driver who was at fault. Most states recognize your right to be "made whole" after an accident, and that includes getting compensated for the hit your car’s market value has taken. This is where nearly all successful diminished value claims happen.

The bottom line is this: if the accident was your fault, you're almost certainly out of luck for diminished value. If the other driver was at fault, you’ve got a real shot.

Knowing this is a great start, but you still need to dig into the specific rules that apply in your state.

Why Your State's Laws Matter

Some states are just plain better for consumers when it comes to diminished value. Georgia, for instance, is famous for having strong legal precedents that make it one of the easiest states to win a claim. Other states, however, might have quirky case law or statutes that throw up roadblocks.

Because the rules are so different, it’s absolutely essential to know what you’re up against. For a closer look, you can dive into the specifics of state-by-state diminished value laws to see what’s on the books where you are.

The legal environment for third-party claims can vary quite a bit, from supportive to challenging.

State-by-State Approach to Diminished Value Claims (Examples)

This table shows just how different the approach can be depending on your location.

| State Example | Stance on Third-Party DV Claims | Key Consideration |

|---|---|---|

| Georgia | Strongly Supported | Considered one of the most consumer-friendly states due to favorable case law. |

| California | Supported | Claims are allowed, but the burden of proof is high and requires solid documentation. |

| Texas | Supported with Nuances | Generally allowed, but specific formulas or appraisal methods may be challenged. |

| Oregon | Supported | Case law supports the right to recover diminished value from the at-fault party. |

As you can see, while the right to claim exists in many places, the local legal climate dictates how easy or difficult the process will be.

When to Consider Hiring an Attorney

You can often handle a straightforward diminished value claim on your own, but there are definitely times when calling in a legal professional is the right move. An attorney can make all the difference if the insurance company is playing hardball or if the amount of money at stake is significant.

Think about getting legal help if you find yourself in these situations:

- The Insurance Company Is Uncooperative: If the adjuster stonewalls you, refuses to negotiate fairly, or just flat-out denies a valid claim, a letter from an attorney can instantly change their tune.

- The Financial Loss Is Substantial: For high-end, classic, or exotic cars, the diminished value can easily reach tens of thousands of dollars. In these cases, paying for an expert to fight for you is a smart investment to protect a major asset.

- The Case Is Complex: If there’s any argument over who was at fault or other messy legal details, a lawyer can cut through the noise and make sure your rights are protected.

Common Questions About Diminished Value Claims

Even after you get a handle on the basics, a few specific questions always seem to pop up when it's time to actually pursue a diminished value claim. Getting straight answers to these common sticking points can give you the confidence you need to get the compensation you're owed. Let's tackle them head-on.

Can I File a Claim if the Accident Was My Fault?

This is a big one, and the short answer is almost always no. Diminished value is something you claim against the at-fault driver's insurance policy. Think of it as a third-party claim.

Your own policy is a contract to pay for repairs and get your car back to its pre-accident condition. It doesn't cover the hit your car’s market value takes afterward. To successfully claim that loss, you have to be the innocent party in the collision.

Is There a Time Limit to File a Claim?

Yes, and this is critical. There's a legal deadline known as the statute of limitations, and it varies quite a bit from state to state. Typically, it’s the same timeline as any other property damage claim, which could be anywhere from two to six years.

It's absolutely crucial to check the law in your state, but here’s my best advice: file your claim as soon as your car is out of the shop. If you wait, it just muddies the waters. Your car depreciates naturally over time, and it becomes much harder to prove how much value was lost specifically because of the accident.

Acting fast shows the insurance company you're serious and makes your case much stronger.

Will Filing a Diminished Value Claim Raise My Insurance Rates?

If you weren't at fault, filing a diminished value claim against the other driver’s insurance should not affect your rates. Why? Because your insurance company isn't the one paying out the money.

Rate hikes are usually tied to at-fault accidents on your record. Claiming a financial loss that you're legally owed from someone else's insurer is your right, and it shouldn't penalize you in any way.

Navigating a diminished value claim requires precision and expertise. At Total Loss Northwest, our certified appraisers provide the detailed, data-backed reports you need to challenge lowball offers and recover the full value your vehicle has lost. Don't leave money on the table—let us fight for the fair settlement you deserve. Learn more and start your claim at https://totallossnw.com.