Even after your car has been expertly repaired, it has lost something significant: its value. Diminished value is the permanent drop in your car’s resale price simply because it now has an accident on its record. The good news is you can often recover this financial loss from the at-fault driver's insurance company.

Understanding Diminished Value and Its Impact

Let’s put this in real-world terms. Say you're in the market for a used car and you find two identical options—same make, model, year, and mileage. One has a squeaky-clean vehicle history report, but the other was in a major collision and then repaired.

Which one are you going to buy? Most people would go for the one without the accident history. Or, at the very least, they’d expect a hefty discount on the one that was wrecked.

That discount is the diminished value. It’s a very real financial hit that has nothing to do with the quality of the bodywork. The car could look brand new, but its history now carries a permanent stain that scares away potential buyers and lowers its market price.

The Stigma of an Accident Report

The problem boils down to the "stigma" that's now permanently attached to your car's history report. Once an accident is on the books, it’s there for good. This creates doubt for future buyers who will always wonder if there’s hidden, long-term damage lurking beneath the surface, no matter how perfect the repairs look.

This loss isn't theoretical—it's immediate. A significant collision can tank your car’s trade-in value by 10% to 25%. For example, a 2018 Honda Accord worth $20,000 before a crash could suddenly be worth only $15,000 after repairs—a huge 25% loss. A 2017 Toyota Camry might drop from $18,000 to $13,500. You can get a better sense of how different vehicles are impacted by exploring post-collision depreciation data.

Recovering Your Financial Loss

Here’s the critical part: if the accident wasn't your fault, this isn't a loss you have to eat. The at-fault driver's insurance has a duty to make you "whole" again, and that includes paying you for the value your car has lost.

A diminished value claim isn't a complaint about the repair shop. It’s about getting compensated for the irreversible drop in your car’s market value caused by the accident itself.

Getting a handle on this concept is the first and most important step. Your vehicle has been damaged in a way that goes beyond dents and scratches, and a diminished value claim is how you get compensated for that hidden financial injury.

How Insurance Companies Calculate Your Loss

When you file a diminished value claim, the insurance company isn't just pulling a number out of thin air. They have a go-to method for calculating what they think they owe you, and it's almost always based on a formula designed to keep their payout low. Knowing how they get their number is your first step in successfully challenging it.

The most common tool in their arsenal is a formula known in the industry as Rule 17c. It originally came out of a Georgia court case but has since become the standard playbook for adjusters nationwide. It’s a multi-step calculation that gives them a quick, standardized figure for your car’s lost value.

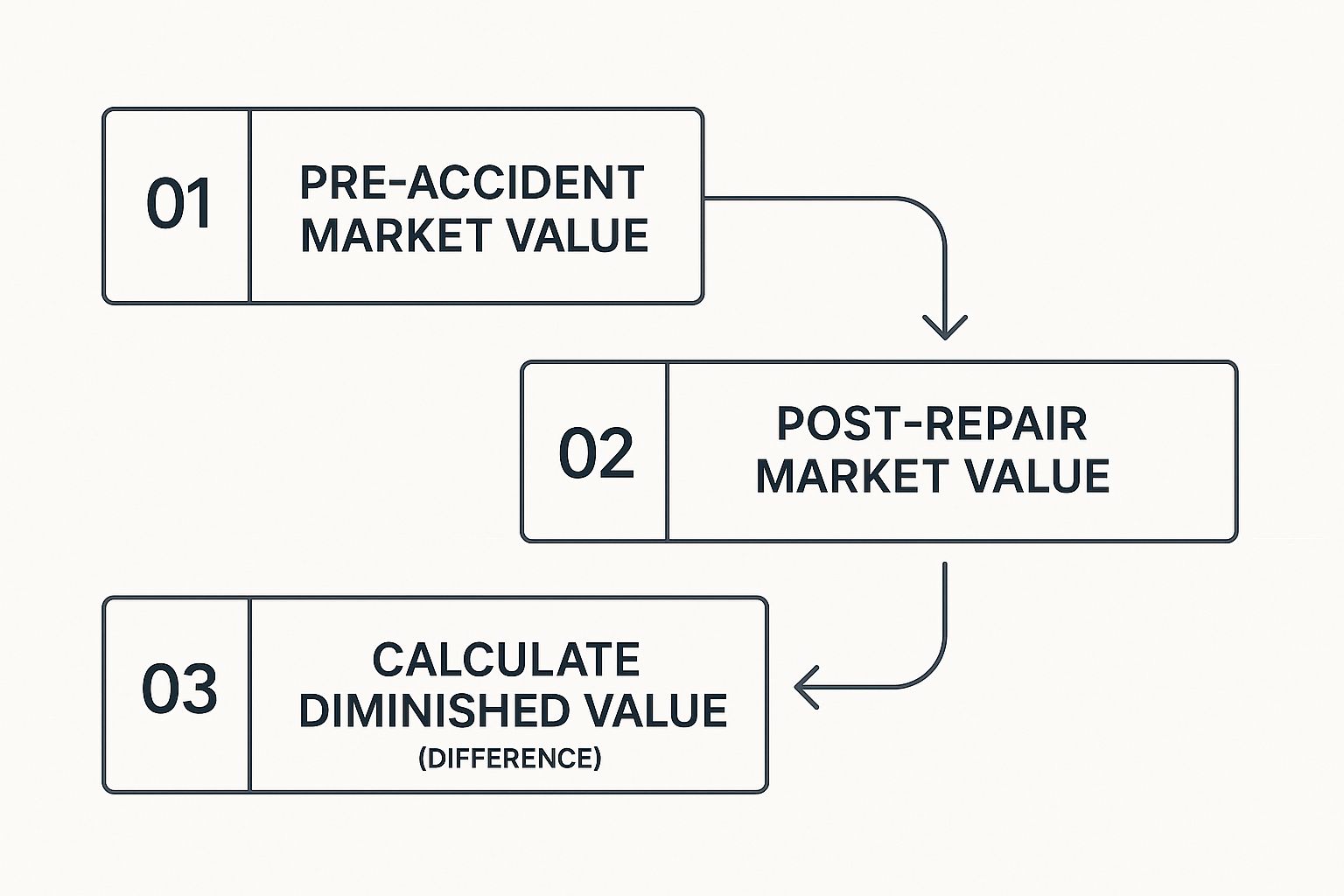

This chart breaks down the basic idea behind the calculation.

Simply put, the loss is what your car was worth right before the crash versus what it’s worth right after the repairs are done.

Breaking Down the Rule 17c Formula

At its heart, the Rule 17c formula is all about applying caps and deductions to your vehicle's pre-accident value. Let's walk through a real-world example to see just how it works. We’ll use a common vehicle, a Toyota RAV4.

First, the adjuster finds your car's Actual Cash Value (ACV)—its market value a moment before the accident. For our example, let's say your RAV4 was worth $30,000. The formula immediately puts a ceiling on the claim by capping the maximum diminished value at 10% of the ACV.

- Step 1: The 10% Cap

- $30,000 (ACV) x 10% (Cap) = $3,000

This $3,000 is the absolute most you could get under their formula. But they don't stop there. The next steps are all about whittling that number down.

Applying Damage and Mileage Modifiers

Now, the adjuster applies a damage multiplier. This is a subjective rating on a scale from 0 to 1 that’s supposed to reflect the severity of the damage. Here’s a typical breakdown:

- 1.0: Severe structural damage

- 0.75: Major panel damage

- 0.50: Moderate panel damage

- 0.25: Minor panel damage

- 0.00: No structural damage or only cosmetic issues

Let's say your RAV4 had moderate damage to a door and the quarter panel. The adjuster might assign a 0.50 multiplier, which instantly slashes your potential payout in half.

- Step 2: The Damage Hit

- $3,000 (Base Loss) x 0.50 (Damage Multiplier) = $1,500

Finally, they apply a mileage multiplier to shrink the payout even more. Their thinking is that cars with more miles have already lost more of their value, so an accident doesn't hurt them as much financially.

- 1.0: 0-19,999 miles

- 0.8: 20,000-39,999 miles

- 0.6: 40,000-59,999 miles

- 0.4: 60,000-79,999 miles

- 0.2: 80,000-99,999 miles

- 0.0: 100,000+ miles

If your RAV4 had 45,000 miles on the odometer, they would use a 0.6 multiplier.

- Step 3: The Mileage Hit

- $1,500 x 0.60 (Mileage Multiplier) = $900

And just like that, the insurer’s math takes a $30,000 vehicle that suffered a real loss in market value and concludes you're only owed $900.

Think of the insurer's calculation as their opening offer, not the final word. This formula is an internal tool built to minimize what they pay, and it rarely lines up with how real buyers in the open market view a car with an accident history.

This is exactly why an independent appraisal almost always comes back with a higher number. While the quality of repairs certainly matters, it can't erase the accident from the vehicle's history report. Studies have shown that even a perfectly repaired car can lose 20% or more of its value. If the repairs are shoddy, that loss can shoot up to 50%.

The simple truth is that vehicle history reports are available to anyone, and given the choice, buyers will always pay more for a car without a checkered past.

Seeing the math behind their lowball offer is powerful. It shows you exactly where their numbers come from and proves they don't reflect what your vehicle is truly worth now. For a closer look at how your car's pre-accident value is determined in the first place, check out our guide on the actual cash value formula.

Navigating State Laws for Your Claim

Proving your car lost value is one thing, but actually getting paid for it hinges on your state’s specific laws. The legal side of things can feel a bit tangled, but it all boils down to two critical pieces of the puzzle: who you can file a claim against and how long you have to do it.

The first thing you need to figure out is whether you're dealing with a first-party or third-party claim. These terms just describe whose insurance company you’re talking to.

- First-Party Claim: This is when you file with your own insurance company. Think of situations where you were at fault or in a no-fault state.

- Third-Party Claim: This is when you file against the at-fault driver's insurance company. You're the "third party" to their policy.

This one distinction is probably the biggest hurdle you'll face when trying to get a diminished value payout.

First-Party vs. Third-Party Claims

When it comes to diminished value, the rules for first-party and third-party claims might as well be from different planets. The good news is that nearly every state allows you to file a third-party diminished value claim. The logic is simple: someone else’s mistake damaged your property and reduced its value, so their insurance company is on the hook to make you whole again.

First-party claims are a much tougher sell. The vast majority of states won't let you claim diminished value from your own insurer. Why? Because your policy is a contract to repair your car, not to guarantee its resale price.

Georgia is the famous exception to this rule. It's one of the only states where courts have sided with policyholders suing their own insurance companies for diminished value. For pretty much everyone else, the only viable route is through the at-fault driver's policy.

This is exactly why determining who was at fault is so important. If the other driver was negligent, the door to a third-party claim swings wide open.

State Claim Eligibility at a Glance

To give you a quick reference, this table breaks down the general rules for diminished value claims across the country.

| State Grouping | Claim Against At-Fault Driver | Claim Against Your Own Insurance | Notable States |

|---|---|---|---|

| Most States | Yes | No | California, Texas, New York, Florida |

| Exceptions | Yes | Yes (court-mandated) | Georgia |

| No-Fault States | Depends on severity & fault | Generally No | Michigan, Florida |

Remember, this is a simplified guide. Always check the specific laws and recent court rulings in your state, as things can and do change.

The Clock Is Ticking: Statutes of Limitations

On top of knowing who to file against, you have to know when to file. Every state has a legal deadline for property damage claims called a statute of limitations. Miss this window, and your right to recover that money is gone for good.

These deadlines aren't the same everywhere, and the differences can be huge.

- In California, you have a generous three years from the date of the accident.

- In Texas, the window is a bit tighter at just two years.

- In Florida, you get up to four years to pursue your claim.

Because these timelines vary so much, it's crucial to look up the statute of limitations in your state right after an accident. For example, our guide on filing a diminished value claim in Washington digs into the specific rules and deadlines for that state.

Too many drivers leave this money on the table simply because they don't know they can claim it. In 2022, while 4.54% of drivers with collision coverage filed a claim, a huge portion of them probably never even tried to get paid for their car's lost market value. Even a perfect repair can't erase an accident from a vehicle's history report, and that history will always make a potential buyer nervous. If you wait too long, you could be giving up thousands of dollars.

Your Step-by-Step Guide to Filing a Claim

Dealing with the fallout from an accident is a nightmare. The last thing you want is a complicated insurance battle. But when it comes to the diminished value on your car after an accident, getting what you're owed is a process you can absolutely manage. Think of it like you're building a case—get the right pieces in place, and you can confidently go after the compensation you deserve.

Let's walk through the whole thing, from gathering your documents to going head-to-head with an insurance adjuster. Here’s exactly what you need to do.

Phase 1: Assembling Your Core Evidence

Before you even pick up the phone to call the insurance company, your first move is to get your paperwork in order. This isn't just busywork; this file is the bedrock of your entire claim. It proves what happened, who was at fault, and the real financial hit you’ve taken.

Your goal is to create a complete story of the accident and its consequences. Start pulling together these essentials:

- The Official Police Report: This is your golden ticket, especially for a third-party claim. It’s an objective account that officially points the finger at the at-fault driver.

- Repair Invoices and Estimates: Every single piece of paper from the body shop is critical. These documents spell out the extent of the damage and prove that quality repairs were done.

- Photographs and Videos: Visuals are powerful. You’ll want pictures from the scene of the accident, of course, but don't forget to take detailed "after" photos of the repaired areas to show the scope of the work.

Having all this organized from the get-go makes every other step easier. It signals to the adjuster that you're prepared, serious, and that your claim is based on facts, not feelings.

Phase 2: Crafting a Powerful Demand Letter

With your evidence locked and loaded, it’s time to officially put the at-fault driver's insurance company on notice. You do this by sending a formal demand letter. This is more than just a quick note; it's a professional document that lays out your case and clearly states the exact amount of money you’re seeking.

Keep your letter direct, concise, and firm. To make it effective, be sure to include these key pieces of information:

- Your Information: Your full name, contact info, and the date.

- Claim Details: The at-fault driver's name, their insurance policy number, and the claim number for the accident.

- Vehicle Information: Your car's year, make, model, and VIN.

- The Demand: The specific dollar amount you are claiming for diminished value. This shouldn’t be a random guess—it needs to be backed by an independent appraisal report, which you should mention is attached.

Your demand letter is your opening move. It sets a serious tone and presents your case with authority, all supported by an expert’s professional opinion.

When an adjuster receives a well-written letter backed by a credible appraisal, they know you mean business. It tells them you've done your homework and won't be easily put off by their standard lowball formulas.

Phase 3: Navigating the Negotiation Process

Once you’ve sent your demand, the ball is in their court. Let's be realistic: they almost never accept your first number. You should fully expect a counteroffer, and it will almost certainly be for less than you asked for. Don't let it throw you off; this is just how the game is played.

When the adjuster calls, stay cool and professional. Your first question should be, "Can you please explain how you arrived at that number and send me the justification in writing?" Often, they’ll be using the flawed Rule 17c formula or some other internal calculation designed to pay out as little as possible.

This is where your prep work really shines. You can push back on their low offer using your independent appraisal as your trump card. Try these tactics:

- Lean on Your Appraisal: Remind them that your number comes from a certified, independent expert who assessed the actual market value loss for your specific car in your local area.

- Question Their Method: If they used a generic formula, politely point out its shortcomings. Ask how it could possibly account for your local market or the specific damage to your vehicle.

- Hold Your Ground: Don't cave just to get it over with. Calmly state that their offer doesn't make you whole for your loss and that you expect a figure that reflects the real-world evidence you’ve provided.

Successfully handling the diminished value on a car after an accident takes a little patience. But by following these steps, you build a rock-solid, evidence-based case that dramatically increases your odds of getting the money you’re rightfully owed.

Proving Your Loss with a Professional Appraisal

After a car accident, it’s easy to feel like you and the insurance adjuster are on opposite sides of a negotiation. And you are. Your goal is to be made whole for your loss, but the insurer's goal is to close the claim for as little money as possible.

Relying on their internal calculations is like letting the other team's coach referee the game—you simply aren't going to get a fair call. This is where a professional, independent appraisal becomes your most powerful tool. It’s not just a second opinion; it's the objective, expert evidence you need to prove your car's true financial damage.

An appraisal completely changes the conversation. It shifts your claim from a subjective disagreement over opinions to a factual negotiation based on hard data. You're no longer arguing against the insurer’s vague, self-serving formula; you're presenting a detailed report grounded in real-world market data for your exact car, in your specific area.

What a Credible Appraisal Report Includes

A legitimate diminished value appraisal is much more than a number scribbled on a piece of paper. It's a comprehensive, evidence-based document that systematically builds an undeniable case for your car’s lost value. Think of it as an expert witness report that methodically dismantles the insurance company’s lowball offer.

A rock-solid report will always contain these key elements:

- Detailed Vehicle Information: This covers the basics like the VIN, mileage, and optional features, but it also establishes your vehicle's specific pre-accident condition.

- Thorough Market Analysis: The appraiser dives deep, researching comparable vehicles in your local market—both with and without accident histories—to establish a clear pre-accident value versus a post-repair value.

- Dealer Statements: The best appraisals often include statements or survey results from managers at local dealerships, confirming they would pay significantly less for an identical vehicle with an accident on its record.

- Photographic Evidence: The report should include photos that document the repaired areas, connecting the physical damage to the resulting financial loss.

This level of detail gives you the undeniable proof you need to show that diminished value is a real, quantifiable loss.

Finding a Qualified Independent Appraiser

Not all appraisers are the same, and picking the right one is absolutely critical to your claim’s success. The last thing you need is a flimsy report that an experienced insurance adjuster can easily pick apart. Your mission is to find a certified, independent expert with a proven track record in fighting—and winning—diminished value claims.

An independent appraiser works for you, not the insurance company. Their only job is to determine the true, unbiased loss in your vehicle’s market value.

When you're vetting potential appraisers, you have to ask the right questions to separate the real pros from the amateurs.

Here are a few major red flags to watch for:

- They Don't Physically Inspect the Vehicle: A truly credible appraisal almost always requires a hands-on inspection of the repairs. A purely online evaluation might not hold up when the insurance company pushes back.

- They Promise a Specific Payout: An ethical appraiser can't guarantee a result. Their job is to deliver an accurate, defensible number—not to promise a specific settlement amount.

- Their Reports are Thin on Data: If they can't clearly explain their methodology or back it up with market data, their valuation is just an opinion, not an expert analysis.

To better understand what a solid report looks like, you can learn more about what a professional diminished value appraisal should include. Investing in a well-documented report from a qualified expert can pay for itself many times over. It’s the key to forcing the insurer to negotiate on facts, not flawed formulas, and getting the fair settlement you deserve.

Got Questions About Diminished Value? We've Got Answers.

Even after you get the hang of what diminished value is, the actual process of filing a claim can feel a bit overwhelming. It’s natural to have questions, and unfortunately, that uncertainty is often what stops people from getting the money they’re rightfully owed.

Let’s clear the air. Here are the most common questions—and persistent myths—that come up, answered in plain English so you can move forward with confidence.

Can I Claim Diminished Value If I Caused the Accident?

In nearly every case, the answer is no. This is a huge point of confusion, but it makes sense once you understand the insurance policies at play.

Your own auto policy is a contract designed to get your car repaired and back to its pre-accident physical condition. It doesn’t promise to protect its resale value.

That's why a diminished value claim is almost always a third-party claim. You're seeking compensation from the at-fault driver's insurance company. Their client's negligence is what caused your financial loss, and their policy is responsible for making you "whole" again—which includes paying you for that drop in market value.

How Do My Car's Age and Mileage Affect My Claim?

A car's age and mileage are two of the biggest players in any diminished value claim. They have a massive impact on both the amount of value lost and the strength of your case.

Think about it this way: a brand-new luxury SUV with only 5,000 miles on the clock has a ton of value to lose. An accident on its record will send its resale price plummeting, making for a very strong claim.

On the flip side, a 12-year-old commuter car with 180,000 miles has already depreciated quite a bit. An accident will still ding its value, but the financial loss will be much smaller. That might make the claim less practical to pursue.

A vehicle’s pre-accident condition is the bedrock of any claim. The newer the car and the lower the mileage, the more inherent value there was to lose—and the larger your potential diminished value settlement will be.

It’s all about setting realistic expectations. A professional appraiser uses your car's specific profile to calculate a loss amount that's both accurate and defensible.

What If the Insurer Denies My Claim or Offers Too Little?

Getting a denial or a laughably low offer is frustrating, but don't panic. It's almost never the final word. In fact, you should probably expect it—it's just the opening move in a negotiation.

Whatever you do, don't just accept their first offer. It’s a business tactic, not an honest assessment of your loss. Instead, push back professionally and methodically.

- Reject Their Offer in Writing. Send a clear email stating that you don't accept their offer because it fails to properly compensate you for your vehicle's lost market value.

- Show Your Work. This is where your independent appraisal becomes your most powerful tool. Attach the report and explain that your demand is based on this expert analysis of your local market.

- Make Them Show Theirs. Ask the adjuster for a detailed, written breakdown of how they arrived at their number. This forces them to justify their math, which is often based on a flawed, generic formula like Rule 17c.

If they still won't budge, you have more options. You can file a complaint with your state's department of insurance or, for larger claims, take the at-fault driver to small claims court. Sometimes, that's what it takes to get them to negotiate in good faith.

Do I Have to Sell My Car to Be Compensated?

No, absolutely not. This is probably the single biggest myth out there, and it's completely false. You don’t have to sell your car—or even plan on selling it—to get paid for its lost value.

The financial damage was done the moment that accident became part of your car’s history report. That drop in fair market value is real and immediate, whether you keep the car for another week or another ten years.

You’re claiming inherent diminished value. That's the automatic loss a vehicle suffers just for having an accident in its past. You're being compensated for a loss that has already happened, not some potential future loss. You're entitled to that money right now.

Don't let an insurance company's lowball offer dictate what you're owed. If you need an expert to prove your vehicle's true loss in value, the team at Total Loss Northwest can help. We provide certified, independent auto appraisals that stand up to insurer scrutiny and get you the fair settlement you deserve. Learn more and get the support you need at https://totallossnw.com.