One of the first questions people ask after a car accident is, "How long is this going to take?" It's a completely fair question. The honest answer is: it depends. A straightforward claim for a minor fender-bender might wrap up in just a few months. But for more complicated accidents with serious injuries, you could be looking at a year or even longer.

The timeline for your specific case really hinges on its unique details.

The Car Accident Settlement Timeline at a Glance

Getting a handle on the settlement timeline can feel like trying to guess the weather. While every situation is different, the process does follow a predictable path. It's helpful to stop thinking of it as one big, unknown event and start seeing it as a series of steps.

For a standard claim—where the injuries are minor and it’s pretty clear who was at fault—you can generally expect the whole process to take between 3 and 6 months. That window covers everything from the day you file the claim to the moment you have a settlement check in hand. You can find more detailed breakdowns of how these timelines work by exploring additional data on car accident settlements.

Breaking Down the Stages

So what actually happens during those months? Let's walk through the key phases of a settlement. The table below gives you a clear look at each stage, how long it usually takes for a more straightforward case, and what’s happening behind the scenes. This gives you a solid framework for what to expect.

A settlement is a marathon, not a sprint. Each stage, from initial evidence gathering to final negotiations, builds upon the last. Rushing the process often means leaving money on the table, especially before the full extent of your injuries and damages is known.

Keep in mind, this timeline is just a baseline. We'll get into the specific things—like how badly you were hurt or if the insurance companies are arguing over who's to blame—that can stretch these estimates out.

Estimated Car Accident Settlement Timeline by Stage

Here's a breakdown of the typical timeline for a standard car accident claim. This table shows the duration for each major phase of the process, helping you see how all the pieces fit together.

| Settlement Stage | Typical Duration (Minor Injuries) | Key Activities |

|---|---|---|

| Initial Report & Treatment | 1-3 Weeks | Reporting the accident, seeking medical care, notifying insurers. |

| Investigation & Evidence | 2-8 Weeks | Insurer investigates, you gather medical records and document losses. |

| Demand & Negotiation | 4-16 Weeks | Submitting a demand letter, insurer review, back-and-forth offers. |

| Finalization & Payout | 2-6 Weeks | Signing a release agreement, check processing, and fund disbursement. |

As you can see, the negotiation stage is often the longest part of the journey. This is where patience really pays off, ensuring you don't settle for less than you deserve.

The Key Factors That Control Your Settlement Timeline

If you're asking, "How long will my car accident settlement take?" the honest answer is: it depends. There’s no simple, one-size-fits-all timeline. Think of it less like a fixed schedule and more like a journey with its own unique twists and turns.

So, why did your neighbor’s fender-bender case wrap up in a few months while yours seems to be dragging on? It almost always boils down to a handful of critical factors. Getting a handle on these will help you set realistic expectations and understand why patience is often your greatest asset in securing a fair outcome.

The Severity of Your Injuries

Without a doubt, the single biggest factor dictating your settlement timeline is the seriousness of your injuries. A claim for minor whiplash that clears up after a few physical therapy sessions is a world apart from a case involving complex surgery or a long-term disability.

You should never, ever settle a claim until you've reached what's known in the medical and legal fields as Maximum Medical Improvement (MMI). This is the crucial point where your doctors determine that your condition has stabilized and you've recovered as fully as you're expected to.

Reaching MMI is a non-negotiable milestone. It's only then that you can truly know the full financial impact of the accident—past, present, and future. Settling before you get to this point is a massive gamble, and you could be left covering future medical costs out of your own pocket.

Rushing the process means you’re negotiating blind, without knowing the true value of your claim. This medical discovery phase is precisely why cases involving significant injuries rightfully take much longer to resolve.

Arguments Over Who Was at Fault

Another major variable is any disagreement over who caused the accident. If liability is clear-cut—say, you were hit from behind while stopped at a red light—the path to settlement is usually much smoother. The other driver's insurance company has very little ground to stand on.

However, the moment fault is questioned, the timeline can stretch out dramatically. This is common in situations like:

- Intersection crashes, where both drivers insist they had the green light.

- Lane-change accidents, with conflicting stories about who had the right of way.

- Multi-car pile-ups, where sorting out the sequence of impacts is a complicated puzzle.

When liability is in dispute, the insurance adjuster has to dig much deeper. This means tracking down and interviewing witnesses, poring over the police report, and sometimes even bringing in accident reconstruction experts. All this back-and-forth can easily add weeks or even months to the initial investigation.

The Strength of Your Evidence

The quality and organization of your evidence have a direct impact on how quickly your claim moves forward. A claim that is backed by strong, well-organized documentation is much harder for an insurer to delay or lowball.

This includes everything from the initial police report and photos from the scene to your complete medical records and proof of lost income. When the value of a badly damaged car is in dispute, getting professional help is key; certified appraisers can provide expert total loss appraisal services to ensure you're offered fair market value. Ultimately, strong evidence builds a powerful narrative that pressures the insurance company to make a fair offer sooner rather than later.

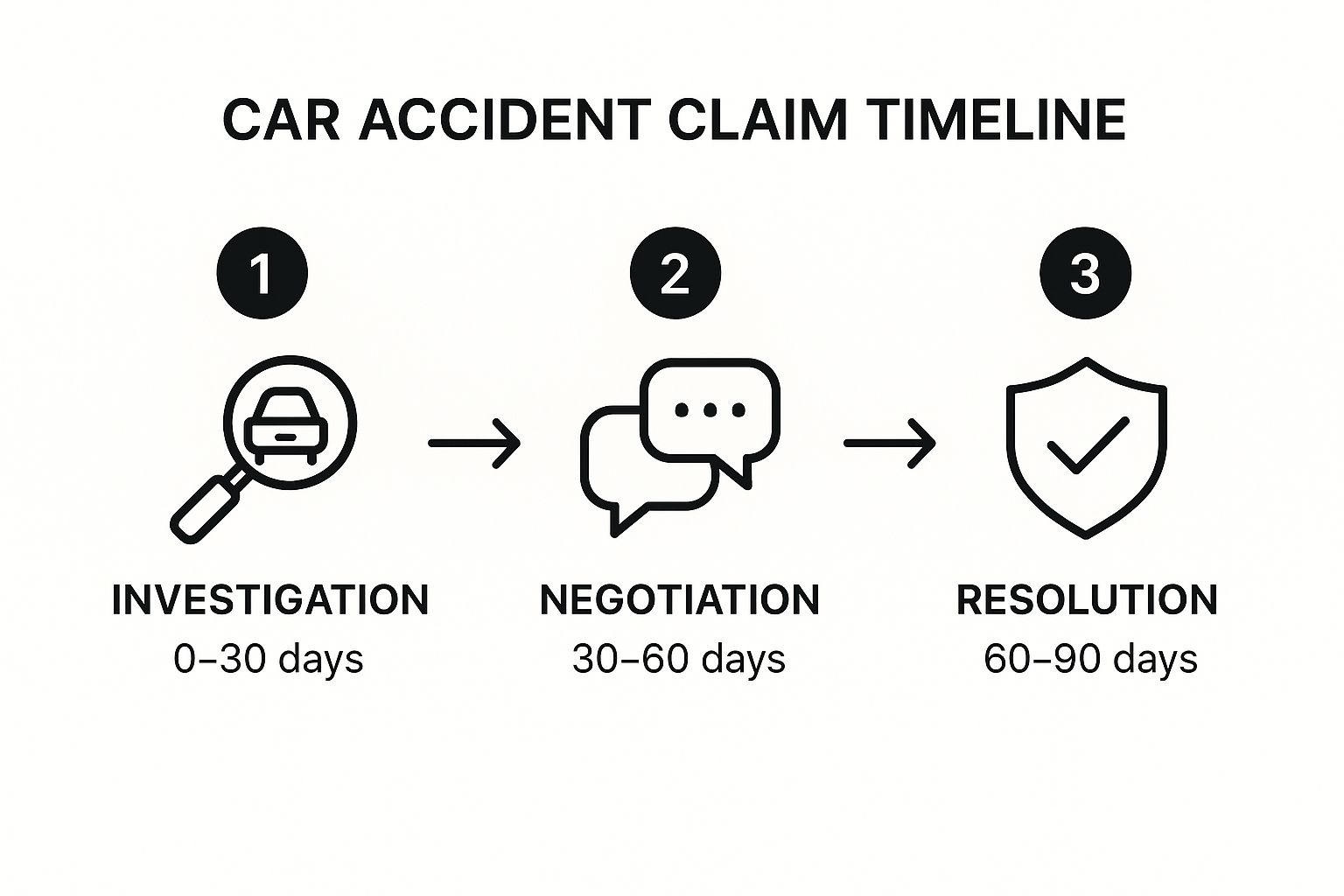

Understanding the 3 Phases of a Car Accident Claim

So, how long does a car accident claim actually take? It's the first question on everyone's mind after a crash. The truth is, it’s less of a single sprint and more of a three-part journey. Thinking about it this way helps demystify the process and manage your expectations. I like to break it down into three distinct acts: building your case, the back-and-forth of negotiations, and finally, closing the deal.

Each stage has its own timeline, and understanding them is key to navigating the entire settlement process.

As you can see, the path from the initial crash to the final check has a few steps, and the negotiation phase is often where the clock seems to tick the loudest.

Phase 1: Investigation and Building Your Case

This is where it all begins. Right after the accident, the focus shifts to laying a strong foundation for your claim. It’s all about gathering the proof needed to show who was at fault and what losses you've suffered because of their negligence. This isn't just about filling out a form; you're essentially building a story backed by undeniable facts.

During this stage, the crucial tasks include:

- Capturing the Scene: Taking clear photos, swapping information with witnesses, and most importantly, getting a copy of the official police report.

- Getting Medical Care: This creates a direct, documented link between the accident and your injuries. Don't skip it.

- The Paperwork Trail: This means collecting every single medical bill, receipts for things like prescriptions or transportation, and documents from your employer showing any lost wages.

Getting this part right from the start is absolutely critical. Being organized and thorough here can make all the difference. Knowing what steps to take after a car accident can help you avoid major headaches and delays later on.

Phase 2: Demands and Negotiations

Once all your damages are tallied up—and especially after your doctor says you've reached Maximum Medical Improvement (MMI)—the claim moves into the negotiation phase. This is when your attorney will typically draft and send a formal demand letter to the insurance company.

Think of this letter as the opening argument. It’s a detailed package that lays out the facts, proves the other driver’s fault, breaks down your injuries and financial losses, and presents a specific dollar amount you’re demanding to settle the case.

A key thing to remember: The insurance adjuster's first offer is almost never their best one. It's just their opening move in a negotiation. Having patience during this back-and-forth is vital if you want to walk away with a fair settlement.

The insurer will review the demand and come back with a counteroffer, which is almost always significantly lower. This is what kicks off the negotiation dance, a process that can last anywhere from a few weeks to many months, depending on how complex the case is and how reasonable the insurance company decides to be.

Phase 3: Finalizing the Settlement and Getting Paid

The final phase kicks in as soon as you and the insurer agree on a settlement figure. But hold on—the money doesn't appear in your account the next day. This is a huge misconception that often leads to frustration.

First, you'll need to sign a settlement release agreement. This is a legal document that officially ends your claim, meaning you can't seek more money for this accident in the future.

Even after you sign, it can still take several weeks to get your funds. The insurance company usually sends the check to your attorney, who then deposits it into a special trust account. That check has to clear the bank, which can take another week or so. Only then can your lawyer pay any outstanding medical liens or fees and cut you a check for the final amount. This last step ensures all the legal and financial loose ends are tied up before your case is officially closed for good.

How State Laws Impact Your Claim Timeline

The timeline for your settlement isn't just shaped by the specifics of your crash—it's also heavily influenced by where you live. Every state has its own set of rules for handling insurance claims and determining who was at fault, and these laws can either speed things up or grind them to a halt.

Think of it this way: you're playing a game, but the rulebook changes the moment you cross state lines. Some rules create a clear and predictable path to getting your claim resolved, while others add frustrating layers of complexity. Getting a handle on your state's specific laws is essential if you want to set realistic expectations for how long it will take to settle your car accident claim.

State-Mandated Deadlines for Insurers

To protect consumers from endless delays, some states have put their foot down. They've passed laws, often called fair claims practices, that force insurance companies to act within specific timeframes. In short, they put the insurer on a shot clock.

California is a perfect example, with some of the strongest consumer protections in the nation. Under the state’s Fair Claims Settlement Practices Regulations, an insurer has to acknowledge your claim within 15 calendar days. After that, the clock starts ticking on a 40-day period for them to investigate and make a decision. Once they approve the claim, they have another 30 days to get the payment out the door.

These deadlines create a clear, enforceable timeline that keeps the process moving forward. You can dig deeper into these specifics by exploring insights on California's claim settlement timelines.

When a state sets clear deadlines, it empowers you and your attorney. It transforms the process from an open-ended waiting game into a structured sequence with predictable milestones, holding the insurance carrier accountable at every step.

This kind of regulation can make a huge difference in straightforward cases. It takes away the insurance company's ability to use intentional delays as a tactic to wear you down. But remember, not every state has these rules, which is why settlement times can vary so dramatically from one place to another.

How Fault Laws Complicate the Timeline

Another massive legal factor is how your state assigns fault for an accident. The system your state uses—especially if it's "comparative negligence" or "contributory negligence"—can turn a simple case into a drawn-out argument over who was to blame.

Here’s how these systems generally work:

- Pure Comparative Negligence: In these states, you can recover damages even if you were 99% at fault, but your final award is reduced by your share of the blame.

- Modified Comparative Negligence: This is more common. You can only get compensation if your fault is below a certain threshold, usually 50% or 51%, depending on the state.

- Contributory Negligence: This is the harshest rule, used only in a handful of states. If you are found to be even 1% at fault, you get nothing.

When these fault rules are in play, you can bet the insurance company will spend a lot of time and effort trying to pin some of the blame on you. Why? Because shifting even a tiny percentage of fault can save them a fortune or let them deny your claim completely. This adds a whole new phase of investigation and negotiation, stretching out your settlement timeline.

Proactive Steps to Expedite Your Settlement

While a lot of the settlement timeline is out of your control, you're not just a passenger on this ride. By taking a few smart, proactive steps, you can prevent needless delays and give your claim the push it needs to move forward. It’s the difference between passively waiting and actively managing your case.

This really boils down to being organized, responsive, and strategic right from the start. When you give your attorney and the insurance company everything they need, when they need it, you eliminate the most common hurdles that slow things down.

Build an Undeniable Case from Day One

The foundation of a strong claim is solid documentation. The more thorough you are right after the crash, the less time an insurance adjuster has to spend digging for information or poking holes in your story.

Here's what you absolutely must do:

- Seek Immediate Medical Attention: This is the most important step. It’s not just for your health; it creates a clear, time-stamped medical record linking your injuries directly to the accident. This makes it incredibly difficult for an insurer to argue your injuries came from somewhere else.

- Document Everything Meticulously: Start a folder—physical or digital—and fill it with the police report, photos from the scene, every medical bill and record, and proof of lost wages. No detail is too small.

- Respond Promptly: When your lawyer or the adjuster asks for something, get it to them quickly. A delay on your end can bring the entire process to a screeching halt.

Think of it this way: your goal is to hand the insurance company a case so well-supported and neatly packaged that there's little room for questions. A clean file with no loose ends encourages them to make a fair offer faster, simply because it's the path of least resistance.

Maintain Momentum and Communicate Effectively

After your claim is filed, the key is to stay engaged so it doesn't get buried on someone's desk. This doesn’t mean you should call the adjuster daily, but it does mean being an organized and active participant in your own case.

A big part of this is being clear about what you've lost. For instance, if the insurance company declares your car a total loss, don’t just accept their initial number. It's crucial to understand how they arrived at that value. You can find more information on how professional auto appraisals work, which can empower you to negotiate for a fair amount.

Here's how to keep things moving:

- Organize Your Records: Keep all your documents in one place where you can find them easily.

- Keep a Communication Log: Jot down the date, time, and key points of every conversation you have with the insurer.

- Be Wary of Early Offers: Insurance companies often throw out a quick, low offer hoping you’ll take it just to be done. Resist that temptation until you know the true, long-term cost of your injuries and property damage.

By following these steps, you’re not just wondering, "how long will my settlement take?" You're actively working to shorten that timeline and steer the process toward a fair conclusion.

Common Questions About Settlement Timelines

https://www.youtube.com/embed/2wIxXmq10FE

Even after getting a handle on the basic steps, you're probably still wrestling with a few "what ifs." It's completely normal. Every accident is different, and you naturally want to know how your specific circumstances might change the answer to, "how long will my car accident settlement take?"

Let's dive into some of the most common questions we hear from clients. We'll give you direct answers to help you feel more in control of the process.

Will My Claim Settle Faster if I Don't Hire a Lawyer?

On the surface, it seems like handling a simple claim yourself would be the fastest route. But this thinking can be a real trap, especially if you have anything more than minor bumps and bruises. Insurers are famous for dangling quick, lowball offers in front of people without a lawyer, hoping they'll take the fast cash and close the book on the claim for a fraction of its real worth.

An experienced attorney knows exactly what your claim is truly worth. They take over the mountain of paperwork, deal directly with the insurance company, and negotiate from a position of strength. This actually prevents delays that often happen when people miss deadlines or submit incomplete information. While the legal process might add some time upfront, it's the only way to get a settlement that truly covers all your losses, not just a quick check that leaves you paying for things out of pocket later.

Does Going to Court Make the Settlement Process Longer?

Yes, without a doubt. The moment a lawsuit is filed, the timeline stretches out considerably. This is exactly why the overwhelming majority of car accident cases—over 95%—are settled before they ever see the inside of a courtroom.

Going to court, or "litigation," adds a whole new layer of formal, time-consuming steps that aren't part of a typical negotiation. These include:

- Discovery: A formal exchange of all evidence, documents, and information between both sides.

- Depositions: Question-and-answer sessions where witnesses and parties give sworn testimony outside of court.

- Court Motions: Legal arguments presented to a judge to decide specific issues before a trial can even begin.

Each of these stages can tack on months, and in some complex cases, even years to your claim. A lawsuit is almost always the last resort, a tool used only when an insurance company digs in its heels and flat-out refuses to offer a fair amount.

While going to court takes much longer, sometimes it's the only path left to force an insurer to pay the full and fair compensation you rightfully deserve. It's a strategic decision made when all other avenues have failed.

How Long After Signing the Release Do I Get My Money?

Once you've agreed on a settlement amount and signed the final release form, the finish line is in sight—but you're not quite there yet. The money doesn't just show up in your bank account the next day.

First, the insurance company typically takes about two to four weeks to process everything on their end and mail the settlement check to your attorney's office.

Your lawyer will then deposit that check into a special client trust account. By law, they have to wait for the funds to fully clear the bank, which can take another week or so. Once it clears, they'll pay any outstanding medical bills or liens from that account, deduct their agreed-upon fees and case costs, and then cut you a check for the final balance.

All told, you can generally expect to have your settlement money in hand within four to six weeks from the day you sign the release. This final step ensures all the i's are dotted and t's are crossed, legally and financially.

If you're dealing with an insurance company's lowball offer on a total loss claim, you don't have to accept it. At Total Loss Northwest, our certified appraisers invoke the Appraisal Clause in your policy to fight for the true market value of your vehicle. We provide the detailed, evidence-backed reports needed to secure a fair settlement. Visit us at https://totallossnw.com to learn how we can help you get what you're truly owed.