When you hear the word "totaled," it's easy to picture a twisted heap of metal. But in the world of insurance, it's really just about the numbers. The entire process hinges on one key figure: your car's Actual Cash Value (ACV) at the moment right before the crash.

This isn't what you originally paid, and it's certainly not what a brand-new replacement would cost. The ACV is the fair market price your specific car could have sold for, and it's the foundation for the settlement offer you'll receive from the insurance company.

What Does a Totaled Car Really Mean for You?

When an insurance adjuster declares your vehicle a "total loss," they're making a purely financial calculation. It simply means the estimated cost to fix the damage is more than the car is worth, at least in their eyes.

Every insurer uses a "total loss formula" to make this call. While it can vary by state, the threshold is typically when repair costs hit 70% to 80% of the car's pre-accident ACV.

Let's say your car's ACV is pegged at $15,000. If the body shop comes back with a repair estimate of $12,000, that's 80% of the value. At that point, the insurer will almost certainly total it. From their perspective, it’s cheaper to give you a check for $15,000 (less your deductible) and sell the damaged car for salvage than it is to sink $12,000 into repairs.

The Role of Actual Cash Value

That ACV number is everything. It’s the figure you’ll be negotiating, so you need to understand what goes into it. Adjusters look at a few key things:

- The Basics: Year, make, model, and trim level set the baseline.

- Mileage & Condition: This is huge. A low-mileage, garage-kept car is worth far more than the same model with high mileage and visible wear.

- Recent Upgrades: Did you just put on a set of new tires or have major engine work done? If you have receipts, these can increase the value.

- Your Local Market: They’ll pull "comps"—comparable vehicles for sale in your immediate area—to see what a car like yours is actually selling for.

Key Takeaway: A total loss is an economic decision, not an emotional one. Your entire negotiation power comes from being able to prove your car's true Actual Cash Value. This is why knowing these details is so critical.

Why Modern Tech Makes Totaling More Common

The sophisticated technology in newer cars is a double-edged sword when it comes to accidents. All those amazing safety features—lane-keep assist, adaptive cruise control, blind-spot monitoring—rely on a complex web of sensors and cameras hidden in bumpers, mirrors, and windshields.

A simple fender bender that might have been a $1,000 fix on a ten-year-old car can easily become a $4,000 repair on a new one. Suddenly, you aren't just replacing a piece of plastic and matching paint. You're replacing and recalibrating extremely sensitive electronic components that have to be perfect to function safely.

This massive jump in repair costs means it takes a lot less damage to push a car over the total-loss threshold. We're seeing this trend across the board. Major salvage auction platforms like Copart reported record-high total loss rates in early 2025. A big reason for this is that advanced driver-assistance systems (ADAS) make even minor repairs incredibly expensive, tipping the financial scales toward a total loss much faster. You can find more details on this by digging into recent automotive industry news.

Calculating Your Car's Actual Cash Value Accurately

So, your car has been declared a total loss. The first settlement offer you get from the insurance adjuster is exactly that—an offer. Think of it as their opening bid in a negotiation, and your strongest leverage comes from knowing what your car was really worth.

To effectively counter a lowball figure, you need to calculate your vehicle’s true Actual Cash Value (ACV). This isn't what you paid for it or what a brand-new one costs. ACV is its fair market value in the moments right before the accident happened. Understanding how this number is built is your first step toward getting the payout you deserve.

The Core Components of Your Car's Value

To get to the bottom of your car’s ACV, you have to look at it the way an adjuster does—as a collection of value-driving factors. The insurance company's valuation software will crunch these numbers, but it’s on you to do your own homework and make sure their math is correct.

When an insurance adjuster looks at your vehicle, they're weighing several key elements to determine its pre-accident value. These are the building blocks of your settlement offer, and understanding each one is crucial for your negotiation.

| Valuation Factor | How It Impacts Your Car's Value |

|---|---|

| Make, Model & Year | This sets the foundation. A 2022 Honda CR-V obviously starts at a much different baseline than a 2018 Ford Fusion. |

| Mileage | Less is more. A car with 50,000 miles is worth significantly more than the same model with 120,000 miles. |

| Pre-Accident Condition | This is where things get subjective. Was your car "excellent" with a pristine interior, or "fair" with noticeable wear and tear? Be honest, but be prepared to defend your rating. |

| Recent Upgrades | Did you just get new tires? Upgrade the sound system? Receipts for recent improvements add real, provable value. |

| Geographic Location | A 4×4 truck is more valuable in snowy Colorado than in sunny Florida. Local market demand matters. |

Don't just take the insurer's word on these, especially the condition report. This is where your own documentation becomes your best friend.

My Advice From The Field: I've seen countless cases won because the owner had proof. Dig up recent, date-stamped photos of your car (inside and out) and pull together your maintenance records. This evidence proves you took exceptional care of your vehicle and justifies a higher valuation than "average."

If you want to get a better handle on how appraisers view these details, digging into professional auto appraisal insights can give you the language and framework to challenge an insurer’s numbers.

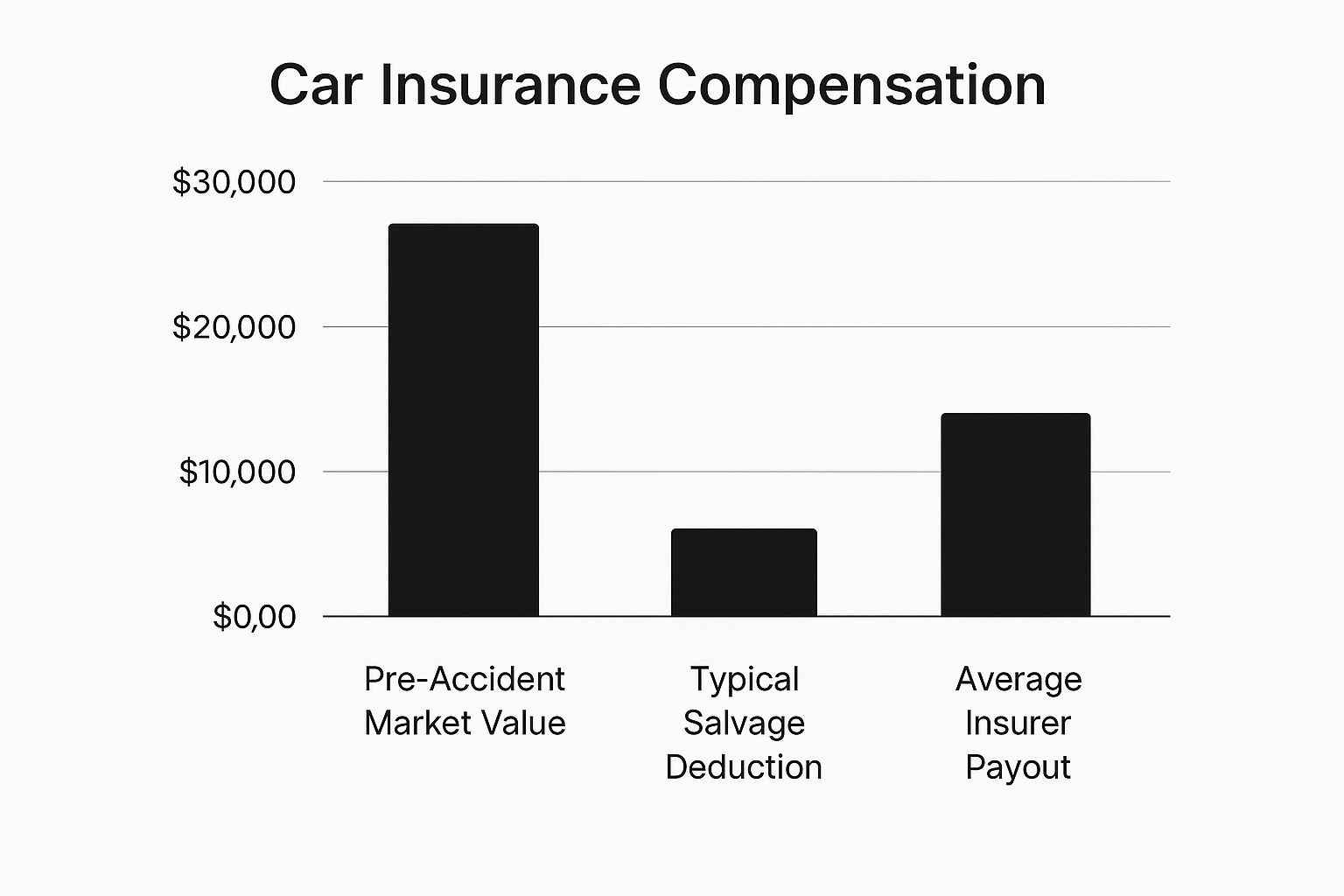

The chart below shows how that pre-accident market value gets whittled down to a final payout.

As you can see, the initial value is often reduced by deductions like the salvage value, leading to the final check from the insurer.

Using Valuation Tools to Your Advantage

Your go-to resources for this research will be online guides like Kelley Blue Book (KBB) and Edmunds. But there’s a right way and a wrong way to use them. Don't just plug in your information and accept the first number you see.

Here's a more strategic approach:

- Generate reports for both the "private party" sale value and the "dealer retail" value.

- The private party value is what you likely could have sold it for yourself.

- The dealer retail value is what a car lot would ask for the same vehicle.

- Your car's true ACV almost always falls somewhere between these two figures.

It's also critical to look beyond just your car and consider the wider market. For example, recent economic shifts have made used car values jump. Projections show that by May 2025, the average total loss market value in the U.S. will be 8.5% above the historical growth rate. In Canada, it's projected to be even higher at 13.2%.

This data proves your totaled car’s worth is tied to current, often inflated, market trends—not just its age. Armed with valuation reports and local sales data, you build a powerful, evidence-based case. You're no longer just arguing; you're presenting facts.

How Today's Market and Onboard Tech Affect Your Payout

When an insurance company calculates what your totaled car is worth, they aren't just looking at its age and mileage. The value of your vehicle is a moving target, heavily influenced by real-world economic forces you might not even think about. Things like global supply chain hiccups and national inflation can directly pump up your car's value—and your final settlement offer.

Understanding these outside pressures is your secret weapon in any negotiation. In a crazy market, an insurer's first offer might be based on stale data, potentially leaving a lot of money on the table. Your goal is to frame your car's value in the context of what's happening right now to get what you're truly owed.

The Used Car Boom and Your Bottom Line

We’ve all seen it: the used car market has been on a wild ride, with prices surging like never before. When new car factories slow down because of things like microchip shortages, the demand for good, reliable used cars goes through the roof. It's classic supply and demand, and it works in your favor here.

Your car’s Actual Cash Value (ACV) is supposed to reflect what it would cost to buy a similar vehicle in the current market. If comparable models are selling for thousands more than they were a year ago, your car’s value has shot up, too. This is a critical point to hammer home with the adjuster.

Expert Takeaway: An insurance company's valuation report might be leaning on data that's several months old. In a market that changes this fast, that could easily undervalue your car by 10% or more. It's up to you to show them current, local market proof that reflects today's much higher prices.

How Modern Tech Drives Up Repair Costs—and Your Car's Value

Another huge factor pushing both values and total loss declarations upward is all the sophisticated tech packed into modern cars. What looks like a simple fender bender can now turn into a shockingly expensive repair.

It's not about just popping on a new plastic bumper cover anymore. Today's bumpers are loaded with delicate and expensive equipment:

- Parking Sensors: These need to be placed perfectly and calibrated to work correctly.

- Blind-Spot Monitors: The radar units for these are often tucked into bumper corners or quarter panels, and they aren't cheap.

- Forward Collision Cameras: These are usually mounted to the windshield. Replacing the glass means a complex recalibration process that can add hundreds of dollars to the bill.

A seemingly minor collision that takes out these systems can easily tack thousands onto the repair estimate. This is a big reason why insurers are quicker to total out cars these days, especially when you factor in rising used car prices. The combination of high replacement costs and expensive repairs for features like Advanced Driver Assistance Systems (ADAS) is a powerful one-two punch. To get a better handle on this, you can explore more about how market trends affect appraisals.

Turning a Volatile Market to Your Advantage

So, how do you actually use all this information to argue for a bigger payout? It’s all about connecting the dots for the insurance adjuster with cold, hard facts. You can't just say, "Hey, used cars are expensive now." You have to prove it.

Here’s how you can build a stronger case:

- Bring the Receipts: Find recent news articles or auto industry reports that specifically talk about the rise in used car prices. Print them out or have the links ready.

- Itemize the Tech: If your car had ADAS features, call them out. Mention the high cost of not just replacing but also recalibrating those specific sensors, radars, and cameras. A pre-repair estimate that breaks these costs down is gold.

- Keep It Fresh: The comparable vehicle listings you use to prove your car's value need to be recent—from the last 30 days at most. Stress that these are real-time prices from your local area, not old numbers from a database.

When you lay out your argument this way, you change the entire dynamic. You're no longer just haggling over a few scratches on your old car; you're educating the adjuster on the economic realities that dictate its true, current value. This shows you've done your homework and makes it much tougher for them to stick to a lowball offer.

Building Your Case with Compelling Evidence

Getting a fair payout for your totaled car comes down to one thing: proof. An opinion is worthless in this fight. The insurance adjuster is armed with their own reports and data, so you need to show up with a stronger, evidence-backed argument of your own. Think of yourself as an attorney building a case—every piece of documentation you gather strengthens your position and proves the number you're asking for.

Your mission is to make it impossible for the adjuster to stick to their lowball offer. When you present them with a stack of credible facts they can't dispute, you change the entire conversation. This prep work is often the difference between taking a disappointing first offer and walking away with a check that reflects what your vehicle was really worth.

Hunt Down Local "Comps"

The absolute bedrock of your evidence is finding "comps"—comparable vehicles currently for sale right in your backyard. This is, without a doubt, the most powerful tool you have. Why? Because it grounds your claim in the reality of your local market, not some vague national average pulled from a database an adjuster is using. An adjuster in Seattle has no business using a car for sale in Miami to value your vehicle.

You need to find several listings for cars that are as close to a clone of yours as possible. Here’s what to zero in on:

- Make, Model, Year, and Trim: This is non-negotiable. A Honda Accord LX is not a comp for an EX-L. The details matter.

- Similar Mileage: Try to find listings within 10-15% of your car's mileage when it was wrecked.

- Same General Condition: If your car was pristine, look for comps listed as "excellent" or "very good."

- Local Listings: Stick to dealerships and private sellers within a 50-75 mile radius.

Pro Tip: Don't just bookmark the links. You have to take screenshots of the entire online ad—the asking price, VIN, mileage, description, and all the photos. Online listings vanish in a heartbeat, so preserving this evidence is the only way to prove your car's market value at that moment.

Prove Your Car Was in Great Shape

Was your car your baby? Meticulously maintained, with a spotless interior and a gleaming, waxed finish? Now you have to prove it. The adjuster's default setting is to rate your car's condition as "average," a simple checkbox that automatically drags down its value. Your job is to present hard evidence that bumps it up to "good" or even "excellent."

Scour your files and phone for any proof that shows your vehicle's pre-accident condition was better than just average.

- Pre-Accident Photos: Recent, date-stamped photos are pure gold. Dig up pictures from vacations, family gatherings, or even just a sunny afternoon when you washed it.

- Maintenance Records: A thick stack of receipts for oil changes, tire rotations, and regular service shows a clear history of responsible ownership. This speaks volumes.

- Receipts for Recent Parts: Did you put on new tires, get a brake job, or replace the battery in the last year? Every single receipt adds tangible, documented value back to your claim.

For example, that set of premium Michelin tires you bought three months before the crash for $900 isn't just a talking point. It's a specific, documented upgrade. When you hand over that receipt, the adjuster is forced to account for it, because it's a wear-and-tear item you recently paid full price to replace.

Package Your Evidence for Impact

Once you've got all your proof, don't just email a jumble of random files. Organize it all into a clean, professional package. When you make your argument easy to follow, you show the adjuster you're serious and methodical.

| Document Type | What It Proves to the Adjuster |

|---|---|

| Local Comps (Screenshots) | Establishes the real-time, local market value of your exact vehicle. |

| Maintenance & Service Records | Shows the car was well-cared for, justifying a higher condition rating. |

| Receipts for Recent Upgrades | Adds specific, provable dollar amounts back into the ACV calculation. |

| Pre-Accident Photographs | Provides visual proof that contradicts their default "average" rating. |

Presenting a package like this completely changes the dynamic. You’re no longer just another claimant asking for more money out of thin air. You are a prepared, organized individual presenting a fact-based rebuttal to their initial offer. This approach makes it incredibly difficult for them to dismiss your claim and dramatically increases your chances of getting a fair settlement.

Negotiating With Insurance Like a Pro

This is where all your hard work pays off. The goal isn't to be argumentative; it's to be authoritative. You've gathered the facts, researched the market, and built a solid case for your car's true value. Now, you just need to have a calm, evidence-based conversation with the insurance adjuster.

Think of the adjuster's first offer as exactly what it is: a starting point. It’s a number generated by their software based on their data, but it often misses the nuances that make your car unique. Your job is to fill in those gaps with the compelling evidence you’ve collected. Treat it like a business meeting where you're simply presenting a more accurate valuation.

Presenting Your Case Effectively

The way you handle the first conversation after getting their initial offer sets the tone for everything that follows. Don't just call and complain that the offer is too low.

Instead, politely explain that you've reviewed their valuation report and, based on your own research, you've arrived at a different, more accurate figure. Frame the discussion around the evidence. For example, you could say, "I see your report lists my car's condition as 'average,' but I have detailed maintenance records and pre-accident photos that really show it was in excellent shape. Can I send those over for you to review?" This approach feels collaborative, not confrontational.

Key Takeaway: Your job is to show them, not just tell them. Present your findings—local comps, receipts for recent work, and proof of condition—as helpful corrections to their assessment. This immediately positions you as an organized, credible person to work with.

Dissecting the Insurer's Valuation Report

The insurance company will give you a valuation report that breaks down how they landed on their offer. This document is your roadmap for the negotiation. Don't just skip to the final number at the bottom; you need to go through it line by line to spot the inevitable inaccuracies.

From my experience, here are the most common places adjusters get it wrong:

- Incorrect Trim or Options: It's incredibly common for them to value a high-end EX-L model as a base LX. Double-check that every single factory option, from the sunroof to the premium sound system, is listed and valued correctly.

- Unfair Condition Rating: This is a big one. They often default to "average" or "fair" condition without any real justification. Use your photos and service records to push for a "good" or "excellent" rating. It can make a huge difference in the final value.

- Out-of-Market Comparables: Scrutinize the "comps" they used to value your car. Are they actually local? If they pulled a vehicle from 200 miles away in a completely different market, you have a solid reason to challenge it.

When you find a mistake, point it out with specifics. Saying, "Your report is missing the factory Tech Package, which my research shows adds about $1,500 to the retail value," is far more powerful than a vague complaint.

Knowing When to Escalate Your Claim

So, what do you do if you’ve laid out all your evidence and the adjuster still won't budge? If you hit a wall, it might be time to escalate.

Your first move should be to politely ask to speak with a claims supervisor or manager. A manager often has more authority to approve a higher settlement and can override the adjuster.

If that doesn't work, you can invoke the Appraisal Clause in your auto policy. This powerful provision allows you to hire your own certified independent appraiser. The insurance company hires their own, and the two appraisers then negotiate a value. If they can’t agree, a neutral third-party "umpire" is brought in to make the final decision. This process takes the insurer's biased software out of the picture entirely.

Navigating this can feel overwhelming, especially if it's your first time. If you feel like you're being seriously lowballed and need a professional eye on your claim, getting a free total loss claim review can clarify your options. An expert can quickly spot the flaws in an insurer's report and help you decide if invoking the appraisal clause is the right move for you.

Common Questions About Total Loss Claims

When your car is declared a total loss, the initial shock can quickly give way to a wave of questions. It's a confusing time, and knowing the answers to a few key things can make a huge difference in protecting your finances.

Let's cut through the noise and tackle some of the most pressing concerns people face. From dealing with a car loan to deciding if you should keep the wrecked vehicle, here are the straightforward answers you need.

What Happens if I Still Owe Money on My Car Loan?

This is easily one of the most stressful parts of the process. The insurance company's payout is based on your car's Actual Cash Value (ACV), not what you owe the bank. If your loan balance is higher than the car's value, you've got what's called "negative equity," and you're responsible for paying off that difference.

For instance, say the insurance company values your car at $18,000, but you still owe $21,000 on your loan. They'll cut a check for the $18,000 (less your deductible), but you are still on the hook for that remaining $3,000.

This is exactly why Gap Insurance exists. If you have a Guaranteed Asset Protection (GAP) policy, it's designed to cover that $3,000 shortfall. It pays the difference directly to your lender, so you aren't stuck with a bill for a car you can no longer drive.

Can I Keep My Totaled Car?

In most states, yes, you can choose to keep your vehicle even after it's been totaled. This is called "owner retention." If you go this route, the insurance company calculates your settlement differently. They'll start with the ACV and then subtract two key amounts:

- Your Deductible: The standard amount you're responsible for on any claim.

- The Salvage Value: This is what the insurer expected to get by selling your wrecked car at a salvage auction.

So, if your car's ACV is $10,000, your deductible is $500, and the salvage value is $1,500, your settlement check would be $8,000. You get the smaller check and the car. This can be a smart move if the damage is mostly cosmetic or if you're skilled enough to handle the repairs yourself.

Just be aware, this isn't a simple fix. The state will issue the car a "salvage title." To get it back on the road legally, you'll have to repair it and pass a tough state inspection to get a new "rebuilt title." It's critical to understand everything about what to do after a car accident, including these title implications, before you decide.

Can I Challenge the Insurer's Decision to Total My Car?

You can, but it's an uphill battle. An insurer declares a car a total loss when repair costs hit a certain percentage of its ACV—the "total loss threshold." To fight their decision, you have to prove one of two things: their repair estimate is way too high, or their valuation of your car is way too low.

If you want to make a case, you'll need solid proof.

- Get Independent Repair Estimates: Take your car to a few trusted, independent body shops. If you can get detailed quotes that are significantly lower than the insurer's, you have a good starting point.

- Prove a Higher ACV: This means digging up hard evidence—local comparable sales, detailed maintenance records—to show your car was worth much more than their number. A higher ACV makes it mathematically harder for the repair costs to trigger that total loss threshold.

Honestly, it's a tough argument to win. Insurers often prefer to total a vehicle to avoid future headaches like supplemental repair claims for hidden damage. You're usually better off focusing your energy on negotiating a higher ACV rather than fighting the total loss designation itself.

If you feel your insurance company is lowballing your car's value or pressuring you to accept an unfair settlement, you don't have to take it. At Total Loss Northwest, our certified independent appraisers fight for the true market value of your totaled car. We ditch the insurer's biased software and build a case with detailed, evidence-backed reports to get you the settlement you deserve. Get a fair and accurate appraisal by visiting us at https://totallossnw.com.