Understanding What You're Really Fighting For

Let's get one thing straight right away: diminished value is not a mythical concept or some made-up fee. It’s the very real, provable financial hit your car takes after an accident, even if the repairs are picture-perfect. Think about it. If you were looking at two identical used cars, but one has a major accident on its CARFAX report, which one would you pay top dollar for? Exactly. That gap in price is the diminished value, and that's what you're trying to get back.

Insurance companies often want you to feel like you're asking for extra money or a "bonus." The reality is you're just asking to be made financially whole, to be put back in the position you were in moments before the crash. Their job is to settle claims for as little as possible, so they often downplay or completely ignore this loss. Grasping this simple fact changes everything. You're not asking for a favor; you're an informed claimant demanding what's rightfully owed to you. This mental shift is your first and most important tool when you start to negotiate.

The Three Faces of Value Loss

Getting a handle on the specific type of diminished value your car has suffered will make your claim much stronger. While a professional appraiser will nail down the specifics, it helps to know the lingo yourself.

- Inherent Diminished Value: This is the big one and the most common. It's the automatic drop in your car's market value just because it now has an accident history. This applies even if the repairs are flawless.

- Repair-Related Diminished Value: This comes into play when the repair work itself is shoddy. We're talking about mismatched paint, body panels that don't quite line up, or the use of cheap, non-original parts. This is a separate loss on top of the inherent value loss.

- Immediate Diminished Value: This refers to the value of your car right after the accident but before any repairs have been done. It’s less frequently used in claims because the at-fault driver's insurance usually covers the cost of repairs directly.

Why Your Claim Is Legitimate

The idea of getting this money back isn't new; it's a well-established principle. A car with an accident in its past is simply worth less, even if it looks and drives perfectly. This is particularly true if the body shop used aftermarket parts instead of original equipment manufacturer (OEM) parts, which can significantly damage its resale appeal.

As noted in industry publications, a diminished value claim is your right to recover the difference between your car’s pre-crash worth and its post-repair value from the at-fault party's insurer. You can read a helpful consumer advisory to learn more about filing for your car's lost value. If you're curious about what your specific loss might be, getting a free diminished value assessment can give you a solid starting point.

Building Your Evidence Like a Detective

When you're ready to negotiate your diminished value claim, you can't just throw a messy folder of receipts at the insurance adjuster and hope for the best. You need to approach this like a detective building a case. Your mission is to gather undeniable proof that tells a clear story of your car's lost value. Remember, the insurance company wants to minimize its payout, so your evidence has to be so strong that denying or lowballing your claim becomes a bad option for them.

This isn't just about snapping a few photos of the dented bumper. It's about creating a complete record that leaves no room for an adjuster's doubts.

Your Essential Documentation and Photo Checklist

To build a rock-solid case, you need to be thorough. Think of it as walking the adjuster through the entire incident, from the crash itself to the final, repaired vehicle.

- Pre-Repair Photos: Get pictures of the damage from every possible angle. Take wide shots to show the overall impact, close-ups of specific dents and scratches, and even photos from underneath the car if you can. These initial pictures are crucial for showing how severe the original impact really was.

- During-Repair Photos: This is a pro tip that many people miss. If you can, swing by the body shop and take pictures while your car is taken apart. Photos of the internal structure being straightened or new parts being welded in are incredibly powerful. They prove the damage was much more than just cosmetic.

- The Final Invoice: Don't just keep the summary page. You need the full, itemized repair bill. This document lists every single part that was replaced and every hour of labor billed. Look closely to see if they used cheaper aftermarket parts instead of original equipment manufacturer (OEM) parts.

- The Police Report: This is your official, third-party confirmation of what happened and who was at fault. It's a foundational piece of your evidence.

Before you start assembling your documents, it's helpful to see what's absolutely necessary versus what's just nice to have. This checklist breaks it down.

| Document Type | Required/Optional | Impact Level | When to Obtain |

|---|---|---|---|

| Police Accident Report | Required | High | Immediately after the accident |

| Itemized Repair Invoice | Required | High | When you pick up your car from the shop |

| Photos of Damage (Pre-Repair) | Required | High | At the scene of the accident, if possible |

| Proof of Repairs (Post-Repair Photos) | Required | Medium | When you pick up your car from the shop |

| Photos of Damage (During Repair) | Optional | High | During the repair process (coordinate with shop) |

| Vehicle Title & Registration | Required | Low | Have on hand before filing the claim |

| CarFax/Vehicle History Report | Optional | Medium | Before the accident and after repairs are noted |

| Professional Appraisal Report | Optional (but recommended) | Very High | After repairs are complete, before sending demand |

As you can see, while some documents are optional, things like in-progress photos and a professional appraisal can dramatically increase the strength of your claim. They shift the argument from your opinion to expert-backed fact.

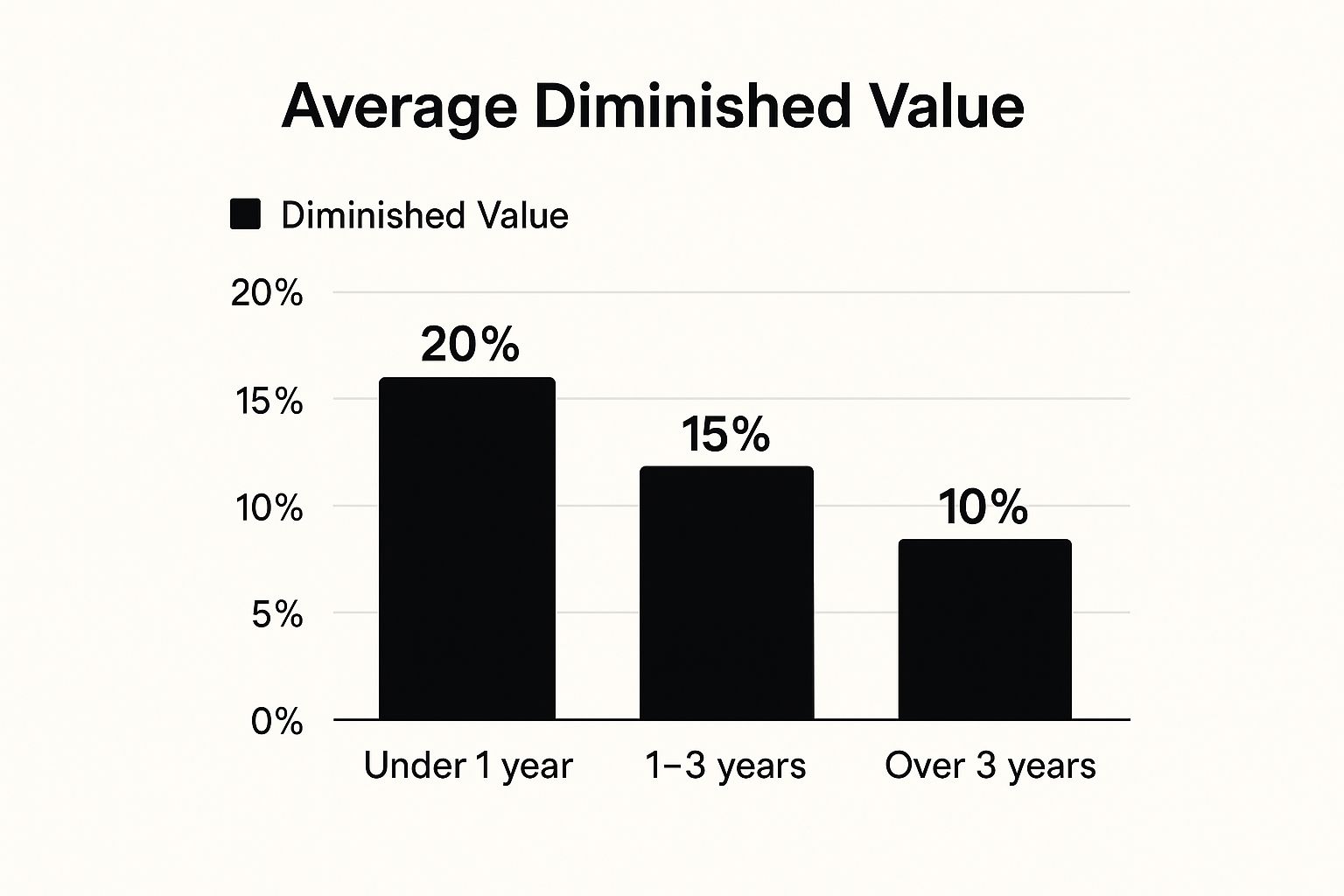

This infographic clearly shows how much a newer car's value can plummet after an accident. This is the kind of hard data you want on your side.

The data highlights a key point: a car that's less than a year old can lose up to 20% of its value after a wreck. That's a much bigger financial hit compared to an older vehicle and a powerful statistic to include in your demand letter.

Creating a Compelling Narrative

Once you have all your documents, arrange them in chronological order. This turns your pile of papers into a story that's easy for the adjuster to follow and difficult to dispute. Start with the police report, move to your initial damage photos, include any shots from inside the body shop, and finish with the detailed repair invoice.

This logical flow builds a powerful argument. The single biggest mistake people make is sending in an incomplete file. Every missing piece of evidence is a chance for the insurer to question your claim's severity and offer you less money. Your job is to close every one of those loopholes.

Getting an Appraisal That Actually Matters

Let's talk about a tough lesson many people learn the hard way: not all appraisals are created equal. If you think a report from your local mechanic will hold any weight with an insurance company, you're in for a disappointment. An adjuster will likely glance at it and toss it aside. To have any real chance in a diminished value negotiation, your appraisal needs to come from an independent, certified expert who specializes in this exact type of claim.

There’s a reason insurance companies have their own list of "approved" appraisers. These individuals often produce reports that—surprise, surprise—find very little loss in value. They might rely on questionable formulas or completely ignore the real-world factors that make a car worth less after an accident. You can’t fight their system with a generic report. You need a true professional on your side who can build a solid case and defend it.

Finding a True Diminished Value Expert

So, how do you find a real pro and not just someone who calls themselves an appraiser? Your search should start with licensed and certified auto appraisers, but don't just stop there. You need to find someone who lives and breathes diminished value claims.

When you start contacting potential appraisers, you should treat it like an interview. This is your chance to vet them and see if they have the expertise you need. Here are a few pointed questions to ask:

- What is your specific methodology for calculating diminished value? A genuine expert will confidently walk you through their process. It should involve deep dives into market data, not just plugging numbers into a generic calculator.

- How many diminished value claims have you provided appraisals for? Experience is everything. You want someone who has handled hundreds, if not thousands, of these cases.

- Are you willing to speak with the insurance adjuster to defend your report? An appraiser who is confident in their valuation will have no problem backing it up. Any hesitation here is a huge red flag.

- Can you provide a sample report? A high-quality report is your goal. It should be incredibly detailed, referencing specific market comparisons and clearly explaining why the car’s value has dropped.

The Power of a Professional Report

A well-crafted appraisal report is the single most powerful tool in your arsenal. It’s what turns your personal opinion into a fact-based, documented demand. The report needs to clearly state your car's value before the accident, its value after the repairs, and a detailed breakdown of how the appraiser determined the final loss amount.

For example, a strong report will point to similar vehicles for sale in your market, showing how an accident history affects their asking prices. It will also factor in the extent of the damage and whether original manufacturer or aftermarket parts were used for the repair. For high-end vehicles, getting a second appraisal can sometimes be a smart play to strengthen your position. For more helpful information, you can explore various auto appraisal insights from experienced professionals. At the end of the day, paying for a quality appraisal isn't an expense; it's an investment in getting the settlement you deserve.

Using Legal Precedents to Your Advantage

Knowing your rights completely changes the dynamic of your negotiation. Insurance companies are pros at handling claims, and they often operate on the assumption that you don't understand the legal foundation supporting your claim for diminished value. When you mention established legal precedents, you signal to the adjuster that you’ve done your homework and aren't just making an emotional appeal. This isn't about playing lawyer; it's about showing you know the rules of the game they're playing.

For example, an adjuster might try to tell you that since your car was perfectly repaired, they owe you nothing more. This is a common tactic. Having a basic grasp of case law helps you confidently push back. It proves that your claim is rooted in legal history, not just your opinion, forcing the adjuster to take it more seriously. This knowledge gives you a firm foundation, which is especially important when you get a lowball offer or an outright denial.

Landmark Cases That Strengthen Your Claim

While the specifics vary by state, certain court decisions have set powerful precedents that shape how insurers handle diminished value claims across the country. One of the most important is the Georgia Supreme Court decision in State Farm Mut. Auto. Ins. Co. v. Mabry (2001). This groundbreaking case established that an insurer is responsible for paying for the loss in value in addition to the repair costs, even if the policyholder doesn't specifically ask for it. The ruling confirmed that diminished value is a real, separate loss from the physical damage.

You can see how different states handle these claims by checking out this comprehensive diminished value legal overview.

How to Use This Information

You don't need to start quoting legal statutes to the adjuster. Instead, you can weave this knowledge into your conversation or demand letter in a natural way. Consider using phrases like these:

- "My understanding is that in my state, courts have recognized that diminished value is a compensable loss separate from repair costs."

- "Based on established precedents, a vehicle's market value is inherently reduced after a significant accident, regardless of repair quality."

Taking this approach shows you're an informed claimant who means business. It lets the insurer know you understand how to negotiate a diminished value claim effectively and won't be easily brushed aside. This simple shift in how you present your case can significantly improve your chances of getting a fair settlement.

Writing a Demand Letter That Gets Attention

You’ve gathered your evidence and have a solid appraisal in hand. Now it’s time to go on the offensive. This is where the diminished value demand letter comes into play—it's your opening move in the negotiation process. This isn't just a casual note asking for money; it's a formal, structured argument that lays out your case with confidence and authority.

A flimsy, disorganized letter gives the insurance adjuster an easy out. They might send back a ridiculously low offer or, even worse, just ignore it. But a powerful, well-crafted letter? That forces them to sit up and take your claim seriously right from the start. Your goal is to present a case so logical and backed by evidence that the adjuster concludes that paying your claim is much easier than fighting it.

Structuring a Letter That Commands Respect

Your demand letter needs to be professional, firm, and flawlessly organized. Think of it as a mini-legal brief. It must tell the complete story, from the accident itself to the direct financial loss you've experienced because of it. Keep your emotions in check—this isn't the place for angry rants. Stick to the facts and let your proof do the heavy lifting.

A well-structured letter creates a clear path for the adjuster to follow, making your argument undeniable. Here’s how to build a letter that gets results.

The Opening Gambit: Set the Scene

Start by getting straight to the point. Clearly identify yourself, the claim number, the date of the accident, and the at-fault driver. You need to explicitly state that this letter is a formal demand for diminished value.

For example, a strong opening might look like this: "This letter serves as a formal demand for compensation for the inherent diminished value of my 2023 Honda CR-V (VIN:…) resulting from the collision on [Date], under claim #[Claim Number]." This leaves no room for misinterpretation.

The Narrative and Evidence: Building Your Case

Next, provide a brief summary of the accident. Keep it short and factual, emphasizing that their insured driver was at fault, a fact supported by the police report you'll be attaching.

This section is the heart of your letter. It’s where you systematically present the evidence you've worked hard to collect.

- Refer directly to your professional appraisal report as the basis for your demand.

- Mention the itemized repair bill, pointing out the severity of the work done (e.g., "$8,500 in structural repairs").

- Note if any non-OEM (Original Equipment Manufacturer) parts were used, as this can also affect value.

To give you an idea of what works, here is a breakdown of which components in a demand letter tend to lead to better outcomes.

| Demand Letter Components and Success Rates |

| :— | :— | :— | :— |

| Letter Component | Inclusion Rate | Success Rate | Average Settlement Increase |

| Professional Appraisal Report | 85% | 92% | +35% |

| Itemized Repair Invoices | 95% | 88% | +20% |

| Police Report (Confirming Fault) | 98% | 95% | +25% |

| Clear Monetary Demand | 100% | 90% | +15% |

| Stated Deadline for Response | 70% | 80% | +10% |

Statistical analysis of demand letter elements and their correlation with successful settlements

As the data shows, attaching a professional appraisal is the single most effective element, significantly boosting both success rates and the final settlement amount.

The Ask: State Your Price

Now it's time to state exactly how much you are demanding. This figure shouldn't be pulled out of thin air; it must be the exact amount from your certified appraisal report. Don't be vague or ask for a "fair amount." Be specific and confident.

For instance: "Based on the certified appraisal from Loss Values Auto Appraisals, which is attached, my vehicle has suffered a diminished value of $4,250. I hereby demand payment in this full amount."

The Closing: Your Call to Action

End your letter with a clear call to action and a reasonable deadline. Giving the adjuster a specific timeframe, like 15 or 30 days, to respond creates urgency without being hostile. It shows you're serious and organized.

Make it clear that you are prepared to pursue other options if they fail to respond or negotiate in good faith. This lets them know you're not going to simply go away if they ignore you.

Negotiation Strategies That Actually Work

Once your demand letter is out the door, the real conversation begins. Successfully negotiating your claim is more of a strategic dance than a shouting match. Insurance adjusters are trained negotiators whose main goal is to protect their company's finances. To get the compensation you deserve, you need to show up with your own game plan. This isn't about being confrontational; it’s about being prepared, firm, and smart.

The first call from the adjuster after they review your demand is a make-or-break moment. More often than not, they'll open with a lowball offer, sometimes one that's so low it feels insulting. It's crucial not to get emotional or offended. This is a classic opening move to test your resolve and see if you'll be an easy negotiation.

Instead of getting worked up, calmly steer the conversation back to your evidence. A powerful response is something like, "I appreciate the offer, but it's a long way from the documented loss in my certified appraisal. Could you walk me through how you arrived at your number?" This flips the script, putting the burden on them to justify their low figure with facts, not just company policy.

Tactical Communication and When to Stay Silent

Knowing how to negotiate a diminished value claim is as much about what you don't say as what you do. After you state your position or make a counteroffer, try using strategic silence. It's a natural human tendency to want to fill a quiet moment in a conversation. Let the adjuster be the one to break the silence. You’d be surprised how often they might offer a concession just to get the discussion moving again.

Here are a few more tips for communicating tactically:

- Keep a Detailed Log: Document every single interaction. Write down the date, time, the adjuster's name, and a quick summary of your conversation. This creates a paper trail and holds them accountable.

- Use Collaborative Language: When discussing your claim, frame it as a team effort. Phrases like, "My appraiser and I have concluded…" carry more weight. It's no longer just your personal opinion but a professional assessment.

- Create Justifiable Urgency: Avoid giving hard ultimatums, which can backfire. Instead, try saying, "I'd really like to get this settled in the next two weeks so we can both avoid any further action." It sounds professional and reasonable, but it clearly states your intention to move forward.

While your claim feels personal, it's part of a massive global industry. Diminished value claims are becoming more common as vehicle technology and repair expenses climb. Understanding your role in this larger financial ecosystem can give you some helpful perspective. You can learn more about the scale of global insurance claims to see how your individual case fits into the big picture.

If you feel like you're hitting a brick wall and the adjuster isn't negotiating in good faith, it may be time to call in some backup. Sometimes, simply invoking your policy's Appraisal Clause is enough to break a deadlock. This is also a common issue with total loss claims, where insurers can be just as stubborn. If you're fighting a similar battle over a totaled car, it might be worthwhile to get a free total loss claim review to explore all of your options.

Securing Your Settlement and Getting Paid

Getting a verbal "yes" from the insurance adjuster feels like you've crossed the finish line, but it’s really just the final lap. Until you have a signed agreement and the check is in hand, your negotiated settlement isn't a done deal. This final stage is where you need to stay sharp to make sure the deal you fought for is the one you actually get.

Once you and the adjuster agree on a number over the phone, your first move should be to send a follow-up email. This creates a written record of what was said and locks in the terms. Something simple like, "Per our conversation today, this email is to confirm we have agreed to a settlement of $4,250 for my diminished value claim. Please forward the settlement release forms for my review," is perfect. This little step can prevent a lot of "misunderstandings" down the road.

Reviewing the Settlement and Release Agreement

The document the insurance company sends you is a legally binding contract, often called a settlement and release agreement. It's critical to read every single word before you even think about signing. You're looking for two main things:

- The settlement amount must match the number you agreed on to the penny.

- The release clause should only apply to this specific property damage claim. Watch out for broad language that releases the insurer from "all claims, known or unknown." This could stop you from filing a future claim if a related issue, like a personal injury, shows up later.

Don't be shy about questioning anything that seems off. If a clause is confusing or seems way too broad, ask for an explanation or request that they reword it. It's your right to understand what you're signing.

What About Taxes?

You might be wondering if you'll have to pay taxes on your settlement. Generally, a diminished value settlement is seen as compensation for a loss, not as income, so it's typically not taxable. However, insurance companies paying out settlements over a certain amount may issue a Form 1099-MISC. This form is used to report "Miscellaneous Information" to the IRS.

While your settlement might not technically be taxable income, the fact that it's been reported to the IRS means you'll need to address it. If you get a 1099, it’s a good idea to talk to a tax professional to make sure you handle it correctly on your tax return.

If you’re hitting a wall trying to finalize your settlement or the insurance company is giving you the runaround, it’s not too late to bring in an expert. At Loss Values Auto Appraisals, we help Washington drivers get the full amount they're owed. We can look over your case and provide the certified documentation you need to close your claim successfully. Visit us at Total Loss Appraisals to see how we can help you get what you deserve.