Understanding Your Hidden Right to Compensation

Here’s a little secret your insurance company probably won't be advertising: even after your car is perfectly repaired after an accident, its resale value has likely taken a serious hit. This drop in what your car is worth on the market is called diminished value, and you have a right to be paid back for it. Most drivers assume that once the repair shop is paid, the case is closed. They move on, completely unaware they might be leaving thousands of dollars behind—a costly mistake that quietly benefits the insurance provider.

An insurance diminished value claim is your way to get that lost money back. The idea behind it is straightforward. A vehicle with an accident on its record is simply worth less to a potential buyer, no matter how flawless the repairs are. A 2023 analysis confirmed what any smart car buyer already knows: a collision history makes people hesitant to pay top dollar. You can dig into the details of why a repaired car is worth less by reading the study from the National Association of Insurance Commissioners.

The Three Faces of Diminished Value

To file a successful claim, it helps to know exactly what kind of value loss you’re trying to recover. It's not a one-size-fits-all situation; diminished value comes in three main flavors.

| Type of Diminished Value | Description | Common Scenarios |

|---|---|---|

| Inherent Diminished Value | This is the automatic drop in value just because the vehicle now has an accident on its record. This assumes the repairs were done perfectly. | This is the most common basis for a claim. A CARFAX or AutoCheck report now shows a collision, making future buyers cautious. |

| Repair-Related Diminished Value | This is the value lost because of shoddy repair work. Think mismatched paint, cheap aftermarket parts, or mechanical problems that weren't there before. | You spot that the new door panel doesn't quite line up, or the paint shade is just slightly off in the sunlight. |

| Immediate Diminished Value | This is the loss in the car's value right after the crash, before any repairs have been done. | This type is less common for claims because the at-fault driver's insurance is responsible for paying for the repairs, not the unrepaired damage itself. |

For the vast majority of people filing an insurance diminished value claim, the focus will be squarely on inherent diminished value. This is the financial hit your car takes simply because it now has a permanent blemish on its history.

Recognizing a Legitimate Claim

So, how do you know if you have a solid case? The biggest factor is who was at fault for the accident. As a general rule, you can only file a diminished value claim against the at-fault driver's insurance policy. If you caused the wreck, your own insurance almost certainly won't cover your car's loss in value.

Let's look at a real-world example. Sarah’s one-year-old luxury SUV, worth $65,000, was rear-ended at a stoplight. The repairs were top-notch and cost $12,000, which the other driver's insurance covered. Six months later, when Sarah went to trade it in, the dealership offered her $8,000 less than the going rate for an identical model, pointing directly to the accident on its vehicle history report. That $8,000 gap is her inherent diminished value.

Because she wasn't at fault, Sarah has a legitimate claim. Newer, high-end vehicles often see the biggest percentage drop in value because buyers in that market expect a flawless history. While an older economy car with high mileage might see a smaller dip, the principle is the same: the insurance company made you whole on the repairs, but not on the value of your asset.

Calculating Your True Claim Value Like a Professional

Figuring out the exact dollar amount of your car's lost value is where many people get tripped up. It's easy to just accept the first, often low, offer from an insurance adjuster. Let's be honest, insurance companies use standard formulas, but these are built to protect their profits, not to give you the best possible payout. To get what you're rightfully owed for an insurance diminished value claim, you need to approach the calculation with the same focus as a professional.

This isn't about pulling a number out of thin air. Several critical factors determine the real loss in value:

- Vehicle Age and Mileage: A newer car with low miles will always take a bigger hit in value after an accident compared to an older, high-mileage vehicle.

- Severity of Damage: A minor fender bender is one thing; a major collision with frame damage is another. The higher the repair cost, the greater the diminished value.

- Market Desirability: Is your car a popular model? A sought-after truck or luxury sedan might hold its value better than a less popular car, even after an accident.

- Pre-Accident Condition: If your car was in mint condition, your maintenance records and pre-accident photos are powerful evidence to support a higher claim.

Common Calculation Methods

Insurance adjusters love a formula called Rule 17c. It starts by capping the potential diminished value at 10% of the car's pre-accident market value (based on guides like Kelley Blue Book or NADA). From there, they chip away at that number using "modifiers" for the damage severity and mileage. While it gives them a number to start with, it almost always undervalues the actual market loss.

For instance, a $40,000 SUV would have a starting cap of $4,000 under this rule. But after the adjuster applies multipliers for "moderate" damage and average mileage, their offer might drop to just $1,500. This method completely ignores the real-world thinking of buyers, who would almost always pick an identical car with a clean history over yours.

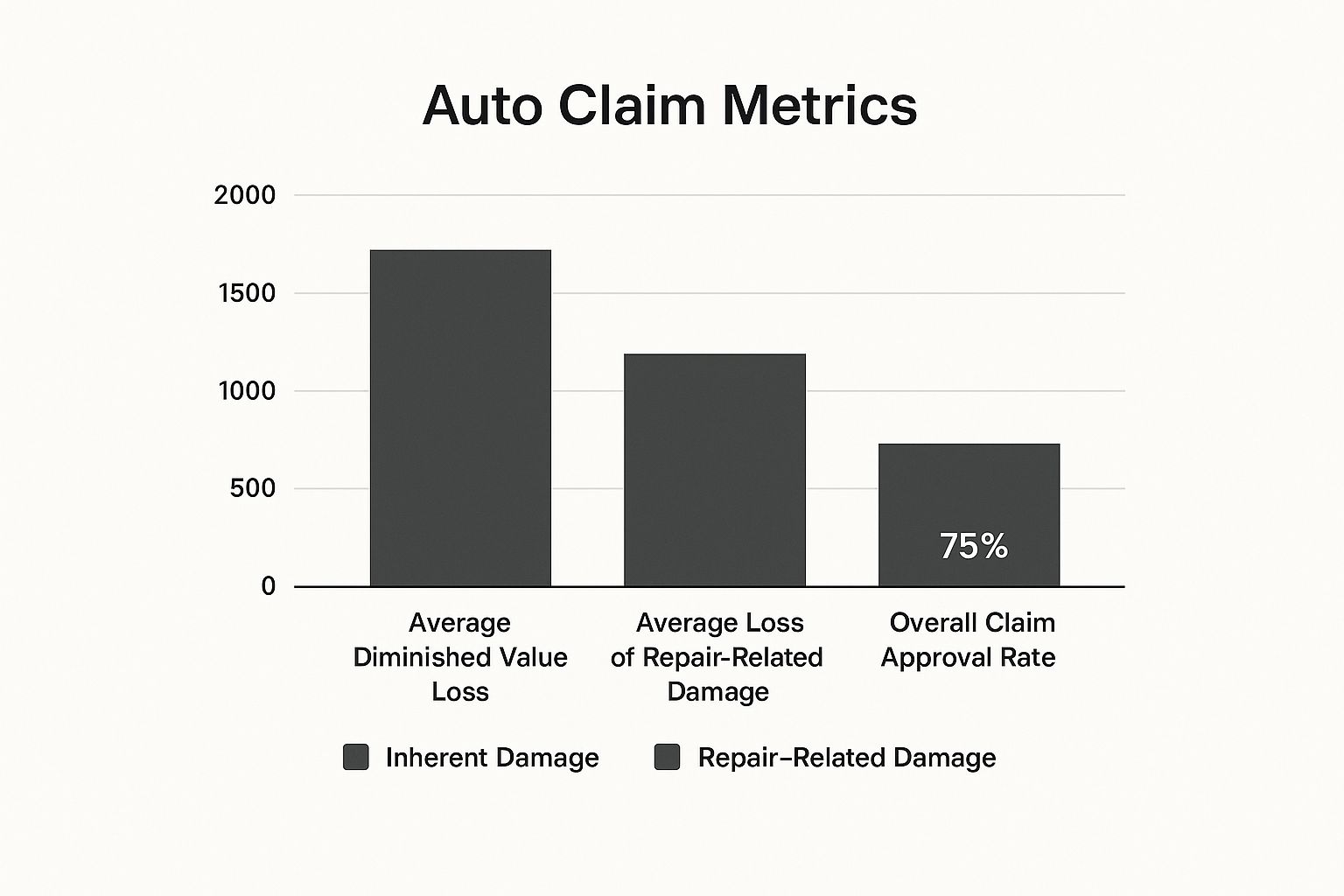

This infographic shows where the value loss comes from and how often claims are approved.

As you can see, the biggest hit comes from "inherent diminished value"—the simple fact that the vehicle was in an accident.

A much better way to calculate your claim is to use real-world data. Look for comparable vehicles for sale in your area. Find listings for cars with clean histories and similar ones with accident histories. Document everything with screenshots, making sure to capture the VIN, mileage, and asking price. When you present this evidence to an adjuster, it shows you've done your homework and are basing your claim on market reality, not their self-serving formula.

To help you understand the options, here’s a breakdown of the common methods for calculating diminished value.

| Method | Accuracy Level | Typical Payout Range | Best Used For | Time Required |

|---|---|---|---|---|

| Rule 17c | Low | 1-5% of car's value | The insurance company's initial offer. | Quick (minutes) |

| Market Research | Medium | 5-15% of car's value | Straightforward claims on common vehicles. | Moderate (hours) |

| Professional Appraisal | High | 10-25% of car's value | High-value, luxury, or classic cars. | High (days to weeks) |

This comparison makes it clear: while quick formulas are easy, they leave money on the table. Investing time in research or hiring a professional yields a much fairer result.

When to Bring in a Professional Appraiser

If you have a straightforward claim on a common vehicle, calculating the value yourself can work. However, if you're dealing with a high-value luxury car, a classic, a heavily modified vehicle, or if the insurer's offer is just insultingly low, hiring a certified appraiser is a smart move. An independent appraiser doesn’t use the 17c formula. Instead, they perform a deep dive into your specific car and the local market conditions.

Their detailed report serves as expert testimony, giving you serious leverage in your negotiations. The cost for a professional report is usually just a fraction of the difference between the insurer's initial lowball offer and a fair settlement. Reports from various markets show that average diminished value claim payouts typically fall between 10-15% of the car's pre-accident value. For a $30,000 car, that could mean a realistic claim of $3,000 to $4,500. You can find more details on how these averages are calculated from market data. If you're concerned about the cost, this guide on diminished value appraisal costs can help you see how it fits your budget. An appraisal is your best weapon against an adjuster who is banking on you not knowing the rules of the game.

Building Bulletproof Evidence That Adjusters Can't Deny

An insurance adjuster might look at dozens of claims a day. The ones that get paid quickly and fairly all have one thing in common: solid, undeniable evidence. When you file an insurance diminished value claim, you’re making a clear statement: "My car is worth less because of your policyholder's negligence, and I have the proof." Without that proof, your claim is just an opinion, which is easy for an adjuster to dismiss. A well-documented case, however, tells a compelling story they simply can't ignore.

The foundation of your claim is a detailed record of your car’s life, both before and after the collision. You need to become a bit of a detective, building a case file. Start with the "before" picture. Pull together pre-accident maintenance records to show the vehicle was well-cared for, a clean vehicle history report, and any photos you might have of the car in its prime. This establishes a high-value baseline, making the drop in value after the accident much more apparent.

Documenting the Damage and Repairs

Once the accident happens, your role as a documentarian becomes even more important. The quality of the evidence you gather from this point on can literally make or break your claim.

- Photography is Key: Don't just take a few quick snaps. You need dozens of high-resolution photos from every possible angle. Get wide shots to show the overall vehicle, then zoom in on the impact zone and any internal damage. Capture pictures of bent frames, deployed airbags, and even scuffed interior panels. The more detailed your visual record, the harder it is for an adjuster to downplay the severity of the accident.

- The Repair Estimate: This document is far more than just a bill; it's the official story of the damage. You must get the final, itemized repair invoice from the body shop. Make sure it details every single part that was replaced, every hour of labor, and specifies if any non-OEM (Original Equipment Manufacturer) parts were used. Using aftermarket parts can sometimes give your diminished value argument extra weight.

- Communicate with the Body Shop: Build a good rapport with your repair shop. Ask the technician to point out and explain any structural or frame damage, as this is a huge factor in value loss. A simple note or statement from the shop manager confirming the severity of the repairs can be a powerful piece of evidence to add to your file.

Proving the Market Value Loss

With the damage and repairs fully documented, you now have to prove the actual loss in market value. This is where you directly challenge the insurer's generic, often lowball, formulas. Your goal is to show what a real person would pay for your car now versus what they'd pay for an identical one with no accident on its record.

To do this, you need to collect sales data for similar vehicles in your local market. Search online listing sites like Autotrader or Cars.com for cars of the same make, model, year, and with similar mileage. Be sure to save screenshots of:

- At least 3-5 listings for cars that have a clean accident history.

- Any listings you can find for cars with a documented accident history.

The price gap between these two sets of vehicles is your real-world diminished value. When you present this data clearly and logically, your claim transforms from a simple request into a well-supported demand. For an even stronger case, a professional appraisal can package all this evidence into a formal report that adjusters find very difficult to dispute. You can learn more about the components of a diminished value report to see how it can strengthen your position.

Filing Your Claim Like an Insurance Professional

How you present your insurance diminished value claim matters just as much as the evidence you've gathered. An adjuster's main goal is to close files quickly and for the least amount of money. When you approach them with a professional, organized, and confident claim, it sends a clear signal: you know your rights and won't be brushed aside with a lowball offer. It all kicks off with how you first make contact and the demand letter you send.

Crafting a Winning Demand Letter

Think of your demand letter as your opening move in a chess match. It's more than just a note asking for money; it's a formal, structured presentation of your case. It’s your chance to lay out the facts, your evidence, and your calculated loss in a professional summary. A well-written letter commands respect and sets a serious tone for the negotiation ahead.

Your demand letter should always include these key elements:

- A Clear Narrative: Give a brief but clear account of the accident. Include the date, location, the other driver's information, and their insurance claim number.

- Your Calculated Loss: State the exact dollar amount you're claiming for diminished value. Be sure to mention how you arrived at this figure (e.g., market comparison, professional appraisal) and attach all your supporting documents.

- A List of All Attached Documents: Create a clear, itemized list of every piece of evidence you're including. This could be the police report, the final repair invoice, market research printouts, pre-accident service records, and your professional appraisal report.

This is a business transaction, so keep emotion out of it. Stick strictly to the facts. The objective is to establish yourself as a credible and thoroughly prepared claimant right from the first interaction.

Navigating the Process and State-Specific Rules

After sending your demand letter, the waiting game begins. But this isn't a time to be passive. Professional follow-up is crucial. I’m not suggesting you call them every day—that can come across as desperate. Instead, a polite email or phone call every 7-10 business days to check on the status shows you're serious and organized. Make sure to log every single communication: who you spoke with, the date, and a summary of the conversation.

It’s also incredibly important to understand that the rules for an insurance diminished value claim can differ quite a bit from state to state. For instance, Georgia has a reputation for being friendly to claimants, while other states have more restrictive laws or legal precedents that can make it tougher. Some states also have a shorter statute of limitations, which means you have a very limited window to file. Your first stop should always be your state's department of insurance website to look up the guidelines for third-party claims.

In most situations, you'll be filing against the at-fault driver's insurance policy. Insurers often have internal procedures for these third-party claims that are designed to create friction and discourage you. Some might issue an immediate denial, hoping you'll simply give up. Others might employ delay tactics, dragging the process out. By presenting your claim professionally and following up with polite persistence, you show them you understand the game and have the patience to see it through to a fair settlement.

Negotiating Your Settlement Like a Professional

This is the moment where all your preparation pays off. Once you've sent in your detailed demand letter, you can expect the insurance adjuster to come back with a settlement offer. Let's be real: their first offer is almost always a lowball. They're not trying to be unfair just for the sake of it; it's a tactic to see if you'll accept a quick and easy payout. Your job is to stay calm, professional, and firm. Don't let it get to you. Instead, think of this as the opening move in a business discussion where you're holding all the cards (and the evidence).

Countering the Initial Offer

When that low offer comes in, your response should be polite but confident. Just accepting it is out of the question. The key is to restate your case without turning it into a heated argument.

- Acknowledge and Reiterate: Start by thanking the adjuster for their offer, but clearly state that it doesn't cover your vehicle's true loss in market value.

- Point to Your Proof: Gently guide them back to your strongest evidence. For instance, you could say, "As the market analysis I sent over shows, similar cars with an accident on their record are selling for $4,500 less than clean-title ones."

- Make a Smart Counteroffer: Don't just repeat your initial demand. Showing a little flexibility demonstrates that you're willing to negotiate. If you asked for $5,000 and they came back with $1,500, a reasonable counter could be in the ballpark of $4,700.

Handling Delay Tactics

Insurance adjusters are often experts at using the clock to their advantage. They know that dragging out the process can frustrate people into accepting a lower settlement just to be done with it. It’s a well-known strategy. In fact, a 2022 Accenture report showed that 60% of unhappy insurance claimants pointed to slow settlements as a primary problem. You can read more about the findings from this global insurance study to see just how common this is.

To fight back against delays, you need to be politely persistent. Keep a log of every email and phone call. If you haven't heard from your adjuster in over a week, it's perfectly acceptable to ask to speak with their manager. Escalating your insurance diminished value claim can often get your file the attention it needs to move forward.

When to Escalate and Finalize

What if you've gone back and forth a few times and the adjuster won't move from an offer that's clearly too low? It's time to think about your next move. Sometimes, simply mentioning that you're considering contacting your state’s insurance commissioner can suddenly make a more reasonable offer appear.

The goal here is a fair compromise. You need to know when an offer has shifted from a lowball to a solid settlement. If your professional appraisal put your loss at $4,000, an offer of $3,500 might be a great result to accept. A professional can be a huge asset in this final stage, and you can learn more about the benefits of a professional diminished value appraisal on our blog. Once you agree to a final number, always get the settlement offer in writing before you sign any release forms.

Avoiding Costly Mistakes That Destroy Claims

Navigating an insurance diminished value claim means learning from the expensive failures of others before they become your own. Many perfectly good claims are sunk by simple, avoidable errors in timing, preparation, or how you talk to the adjuster. Getting familiar with these traps is your best defense against leaving serious money behind or having your claim denied flat out.

One of the biggest blunders is thinking the process is over once the repairs are done. A diminished value claim is a separate action you must take. Another critical mistake is cashing the final repair check from the at-fault driver's insurance without a second thought. Some of these checks have fine print on them saying that by cashing it, you release the company from all future liability. This could kill your diminished value claim on the spot. Always read the memo line and any paperwork that comes with a check before you deposit it.

State Rules and Bad Timing

The rules for diminished value claims are not the same everywhere; they can change dramatically from one state to another. This is a classic trap that catches many people off guard. Some states are known for being friendly to these claims, while others have laws or past court decisions that make winning a claim tough, if not impossible. On top of that, every state has a statute of limitations for property damage claims—this is your absolute deadline for filing. If you miss it, your right to claim that money is gone for good.

The table below gives you a glimpse into how different state laws can be. It's crucial to look into your specific state's rules before you do anything else.

State-by-State Diminished Value Claim Requirements

Overview of how different states handle diminished value claims, including which states are most favorable to claimants

| State | Claim Allowed | At-Fault Required | Time Limit (Years) | Average Success Rate |

|---|---|---|---|---|

| Georgia | Yes | Yes | 4 | High |

| California | Yes | Yes | 3 | Moderate |

| Texas | Yes | Yes | 2 | Moderate-High |

| New York | No (Generally) | N/A | N/A | Very Low |

| Florida | Yes | Yes | 4 | Moderate |

Disclaimer: This is a general overview; laws can and do change. Always confirm the current regulations in your state.

As you can see, where you live matters a lot. A claim that might sail through in Georgia could be a non-starter in New York.

Negotiation and Preparation Blunders

Even if you have a strong case on paper, a lack of preparation can ruin your chances. A common misstep is not gathering objective, third-party proof of your loss. You can't just tell an adjuster, "My car is worth less now." You have to prove it with hard data, like market comparisons or, even better, a professional appraisal report. The adjuster's goal is to close your claim for as little money as possible, and without solid evidence, they have no reason to offer you a fair amount.

Accepting the first offer is another rookie mistake. Think of that initial number as just a starting point for the conversation. If you’ve done your homework and presented a claim backed by good evidence, you have the leverage you need to counter their lowball offer. Don't be afraid to push back and negotiate for a number that truly reflects your car's lost value.

If the talks hit a wall, you have more options. You can ask to speak with a supervisor or mention that you are considering filing a complaint with your state’s department of insurance. This signals that you're serious and often gets the ball rolling again.

Your Complete Action Plan for Claim Success

This is where the rubber meets the road. You’ve learned what an insurance diminished value claim is, figured out how to calculate your loss, and know what evidence makes your case solid. Now it’s time to turn that knowledge into a personalized action plan that will guide you from start to finish. Think of this as your strategic playbook, designed to keep you focused and on track through a process that can sometimes feel like a marathon.

Creating Your Personalized Claim Roadmap

A successful claim doesn't just happen; it comes from a deliberate, organized approach. The very first thing you should do is create a central file for your claim—this could be a physical binder or a dedicated folder on your computer. This file is where every document, every photo, and every note will live. Being organized from the get-go sends a powerful message to the insurance adjuster: you are serious and meticulous.

Next, it's important to set some realistic expectations for yourself. Consider your vehicle’s age, its mileage, and how severe the damage was. A five-year-old daily driver with 80,000 miles won't have the same diminished value as a two-year-old luxury SUV, and that’s perfectly fine. The real goal is to get a settlement that is fair for your specific car and situation. A $1,500 claim on a $15,000 car is just as much of a win as a $5,000 payout on a $50,000 one.

Use this checklist to structure your efforts right from the beginning:

- Initial Assessment: First, confirm your claim is viable. This means you weren't at fault, the car had a clean pre-accident history, and it's not excessively old or high-mileage.

- Evidence Gathering: Have you gathered all your paperwork? This should include the final repair invoice, pre-accident service records, and clear, high-quality photos of the damage.

- Value Calculation: Have you determined your financial loss? You can either do your own market analysis by comparing vehicle listings or bring in a professional for an appraisal.

- Demand Letter: Is your demand letter drafted and ready to go? Make sure it's professional, packed with facts, and includes copies of all your supporting evidence.

Staying Motivated and Knowing When to Get Help

The claims process can definitely test your patience. Adjusters might use delay tactics, hoping you’ll get fed up and either give up or accept a lowball offer. This is a common part of the game, and staying motivated is your key to getting the settlement you're entitled to.

Try setting small, manageable goals for yourself. For example, one week's goal could be just to gather all your pre-accident service records. The next week, you could focus on completing your market research on comparable vehicles. Celebrating these small victories helps keep the momentum going.

Here’s a simple guide to help you decide what to do as your claim progresses:

| If This Happens… | Your Next Action Should Be… |

|---|---|

| The adjuster goes silent for over a week. | Send a polite follow-up email requesting an update. If you still hear nothing, call and ask to speak with their supervisor. |

| You get an obviously low first offer. | Keep your cool. Respond professionally in writing, restate your evidence, and present a reasonable counteroffer. |

| Negotiations have hit a complete wall. | Mention that you are considering filing a complaint with your state's department of insurance or obtaining a professional appraisal. |

| You feel completely overwhelmed or out of your depth. | This is the clearest signal that it's time to call in an expert. A professional appraiser can take over the valuation and negotiation. |

Realizing you need professional help is a sign of strength, not weakness. For high-value vehicles, claims with complex damage, or situations where an insurer simply refuses to be reasonable, a certified appraiser becomes your most valuable ally. They can provide an expert report that breaks through a stalemate and forces the insurer to take your claim seriously.

Your action plan is a living document; it will change as you move through the process. By staying organized, setting realistic goals, and knowing when to call for backup, you put yourself in the strongest possible position to secure a fair settlement for your insurance diminished value claim.

If you're dealing with a stubborn insurer or just want an expert to handle the fight for you, Loss Values Auto Appraisals can help. We provide certified, independent appraisals for Washington vehicle owners that force insurance companies to engage with real market data, not just their internal formulas. We can also provide Diminished Value Support in all 50 states. Get the fair settlement you deserve by contacting us today.