When an insurance adjuster tells you your car is a total loss, that's not the end of the conversation. It's the beginning of a negotiation. You absolutely do not have to accept their first offer. The key to getting a fair payout is understanding exactly how they came up with their number—and then being ready to counter it with your own well-supported evidence.

What It Means When Your Car Is a Total Loss

Hearing your car is "totaled" can feel like a gut punch, but for the insurance company, it's just a math problem. A car becomes a total loss when the cost of repairs plus its scrap value is more than what the car was worth right before the accident. The entire negotiation revolves around that pre-accident value, known as the Actual Cash Value (ACV).

Don't take it personally. This is purely a business calculation for the insurer, and they have a specific formula they follow to make the call.

The Total Loss Formula in a Nutshell

Insurance companies use something called a Total Loss Threshold (TLT) to make their decision. This is simply a percentage of your vehicle’s ACV. While many states have laws setting this threshold, insurers often use their own internal standard, which is usually between 60% and 80%.

Here’s a real-world example: Let’s say your car's ACV is determined to be $15,000. The insurance company estimates they can sell the wrecked car at a salvage auction for $4,000. They subtract that salvage value from the ACV, leaving a repair threshold of $11,000. If the repair estimate comes in higher than $11,000, they’ll declare it a total loss.

Expert Insight: The insurer's primary goal is to settle the claim for the least amount of money possible. Their initial ACV offer is just that—an offer. It's often based on generic data from valuation reports that might overlook your car's excellent condition, recent upgrades, or the hot market for that specific model in your area.

Understanding the Initial Steps

After declaring the vehicle a total loss, the adjuster will send you their ACV offer along with a detailed valuation report. This report is usually generated by a third-party company like CCC Intelligent Solutions. Think of this report as their opening argument, and it's your job to pick it apart.

Here’s what to look for immediately:

- Vehicle Details: Did they get the trim level right? A Ghia is not the same as a base model. Is the mileage accurate? Small errors here can add up to big money.

- Condition Rating: They almost always rate cars as "average." Was your car meticulously maintained? A higher condition rating directly translates to a higher value.

- Comparable Vehicles ("Comps"): The report will list similar vehicles for sale to justify their offer. Are these "comps" actually comparable? Are they from your local market, or are they cherry-picked from hundreds of miles away where prices are lower?

The initial process can feel like a whirlwind, but a successful negotiation is built on careful, methodical preparation. Understanding how the insurance company operates is your first real step toward a fair settlement. To truly level the playing field, consider getting an independent total loss vehicle appraisal to build a powerful, evidence-based case for your counteroffer.

To help you navigate the jargon you're about to hear, here’s a quick-reference table of the most important terms.

Key Terms in a Total Loss Claim

| Term | What It Really Means for You |

|---|---|

| Actual Cash Value (ACV) | This is the magic number. It's the fair market value of your vehicle moments before the accident occurred. This is what you're negotiating. |

| Total Loss Threshold (TLT) | The percentage of your car's value that repairs must exceed for it to be declared a total loss. It's the insurer's line in the sand. |

| Comparable Vehicles ("Comps") | Vehicles the insurer uses to justify their ACV offer. Your job is to make sure these are truly similar in make, model, year, trim, and location. |

| Salvage Value | The amount the insurance company expects to get by selling your wrecked vehicle for parts or scrap. This is subtracted from the ACV to help determine the TLT. |

| Valuation Report | The document from a third-party service (like CCC) that details your vehicle's features, condition, and the comps used to calculate the ACV. Scrutinize this! |

Familiarizing yourself with these concepts will give you more confidence when you pick up the phone to speak with your adjuster. You'll be speaking their language, which is a powerful advantage.

Getting Your Evidence Together: How to Build a Rock-Solid Case

Think of the insurance adjuster's first offer as exactly that: an opening bid. It's not the final word. Their number comes from third-party valuation reports that are notorious for missing the details that made your specific car special. To get the fair settlement you deserve, you need to build a counter-offer so thoroughly documented that they simply can't ignore it.

You're essentially becoming a private investigator for your own car. Your job is to prove its true Actual Cash Value (ACV) using cold, hard facts. The adjuster has their report; you're going to have a file of your own, packed with real-world proof of what your vehicle was actually worth right before the accident.

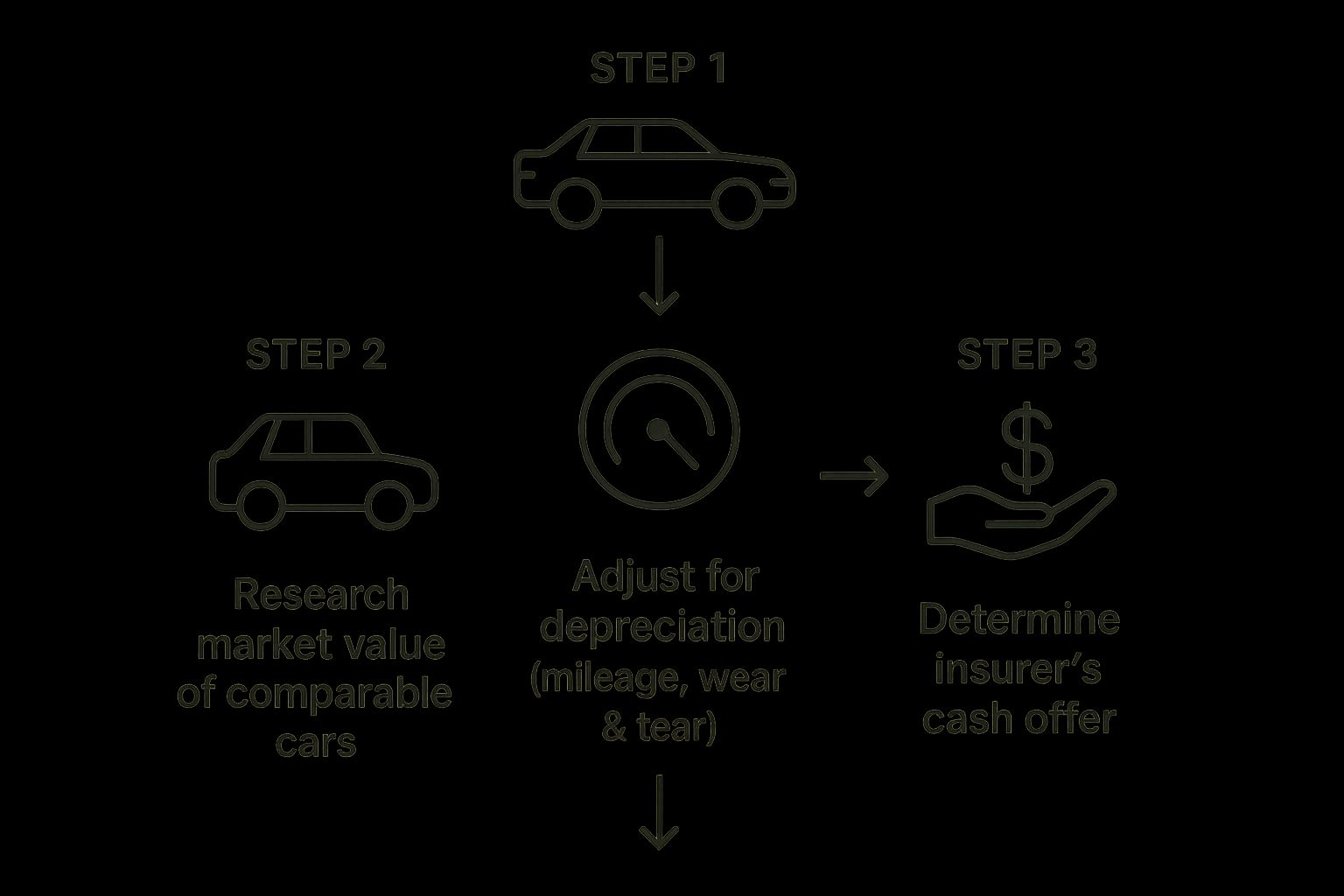

This is a simplified look at how a car's value is calculated, which is the basic framework for both the insurance company's offer and your counter-offer.

As you can see, the market research and specific adjustments are where the numbers can really shift. This is precisely where your evidence comes into play and can make a huge difference in the final payout.

Gather Your Ammunition: Proof of Value

First things first, you need to collect every single piece of paper that proves your car was better than "average." Every receipt, every invoice is another reason why your car was worth more than the cookie-cutter vehicle in the adjuster's report.

Start digging through your files for receipts covering any significant work or upgrades you've made. These aren't just pieces of paper; they represent real money you invested, which directly boosts your car's value.

- New Tires: Did you just drop $800 on a new set of Michelins? A car with brand-new tires is worth more than one with bald ones. Find that receipt.

- Major Repairs: If you recently replaced the transmission or had a major engine service, that’s a massive value-add. Pull the invoices from the repair shop.

- Consistent Maintenance: A stack of receipts for regular oil changes and scheduled services proves your car was meticulously cared for, justifying a higher condition rating than "average."

- Upgrades & Add-ons: Even if your policy has limits on custom parts, things like a premium sound system, a new head unit with Apple CarPlay, or a remote starter should absolutely be factored in.

Don't ever assume the adjuster knows about these things. They won't. You have to spell it out for them and back it up with proof. Hand them a file that leaves no room for debate.

Find Your Own "Comps" (Comparable Vehicles)

This is the most important part of building your case. The insurance company will give you a list of "comparable" vehicles they used to determine your car's value. Your job is to find your own, better list.

The key here is finding vehicles that are truly comparable and, crucially, local. A similar car for sale 500 miles away where the market is cheaper is completely irrelevant. You need to anchor your value in your local market.

Get online and start digging. Search dealer websites and private party listings on platforms like AutoTrader or even Facebook Marketplace, all within a 50- to 100-mile radius of your home. You’re looking for the retail asking price—what a buyer would have to pay to get that car—not some lowball trade-in value.

Save screenshots or print out the listings for every good match you find. Pay very close attention to the details:

- Exact Trim Level: A Honda Accord EX-L is worth thousands more than a base LX model. Make sure your comps are an exact match.

- Similar Mileage: Find cars with odometers as close to yours as possible. A 20,000-mile difference can change the value significantly.

- Condition: If your car was in excellent shape, look for listings described as "excellent," "like new," or "garage kept."

Just finding a handful of strong, local comps with higher asking prices is often enough to poke serious holes in the adjuster's initial valuation. It immediately shifts the conversation and forces them to justify why their numbers are right and your real-world evidence is wrong.

How To Challenge The Insurer's Valuation Report

When the adjuster sends over their valuation report, your work is just getting started. Don't just skip to the final number and sigh. This document, typically generated by a third-party service like CCC or Audatex, is the entire basis for their offer—and in my experience, it’s almost always full of mistakes.

To successfully negotiate your total loss settlement, you have to put on your detective hat. Every error, omission, or questionable assumption you find is a bargaining chip you can use to get a fairer payout. The adjuster is counting on you to accept their report without a fight. Let’s prove them wrong.

Spotting Common Valuation Errors

Think of the insurance company's report as their opening bid, not the final word. These reports are often built using generic data that completely misses the unique details of your car. I see the same costly mistakes pop up time and time again.

Here’s what to look for:

- Incorrect Trim Package: This is a big one. They might list your fully-loaded Limited model as a base-level LE. That single error can easily cost you thousands of dollars.

- Wrong Options: Go through the options list with a fine-tooth comb. Is your premium sound system, sunroof, or technology package listed? Every missing factory-installed feature drags down the value.

- Inaccurate Condition Rating: Adjusters love to default to an "average" condition rating. It's their standard move. But if your car was meticulously maintained, garage-kept, and had a spotless interior, "average" is an insult. You need to gather proof that your car was "above average" or even "excellent."

- Distant or Poor Comps: Take a hard look at the "comparable" vehicles they used to set the price. Are they from a cheaper market 200 miles away? Are they base models when yours had all the bells and whistles? Using bad comps is one of the most common tricks in the book to lowball an offer.

Key Takeaway: The insurer's report is intentionally built to support the lowest possible offer. It's on you to pick it apart, find the flaws, and show them what your vehicle was really worth right before the accident.

Leveraging Regulations In Your Favor

When you push back, you're not just complaining. You're actually asking the insurance company to comply with its own industry regulations. Insurers are legally required to act in good faith, and understanding this gives you a powerful advantage.

For example, the National Association of Insurance Commissioners (NAIC) has a model act that many states follow. This act requires insurers to settle total loss claims based on the vehicle's actual cash value (ACV) or by offering a comparable replacement vehicle. Pointing out their regulatory duties can be a surprisingly effective negotiation tool. You can learn more about these insurance regulations at IRMI.com.

Once you’ve found clear errors in their report, you can politely explain that their valuation doesn’t seem to reflect a true ACV, as required by law. This changes the conversation from a simple price dispute to a discussion about their legal obligation to give you a fair settlement. For more specific tactics, check out our detailed guide on how to challenge a low total loss offer.

Crafting and Presenting a Winning Counteroffer

You’ve done the hard work. You've picked apart the insurance company's report and lined up your own solid evidence. So, what’s next? It's time to transform that research into a counteroffer that the adjuster can't ignore.

Here’s a secret from my years of experience: just calling and asking for more money is a dead end. You need to build a professional, evidence-based case that makes it difficult for them to say no.

Your mission is to make saying "yes" the path of least resistance for the adjuster. The best way to do this is by organizing your findings into a clear, persuasive demand letter or email. This document officially kicks off your negotiation, clearly stating your position and backing it up with undeniable proof.

Structuring Your Demand

Think of your demand letter as your opening argument. Keep your tone firm and businesslike—leave emotion out of it. Kicking things off with anger or frustration will only put the adjuster on the defensive. Instead, politely state that you've reviewed their settlement offer and, based on your research, their valuation has missed the mark.

Next, you'll present your counteroffer. This isn't a number you just dream up; it should be the average retail asking price of the strongest local comparable vehicles you found. Anything less is leaving money on the table.

Your demand letter must include a few key things:

- A Clear Summary: Start with a short paragraph stating that you disagree with their Actual Cash Value (ACV) and present your new, evidence-supported number.

- Your Evidence Packet: Attach everything. I mean everything. Your list of superior local comps, receipts for those new tires or the recent brake job, and photos showing your car's pristine condition.

- A Direct "Ask": Clearly state the exact settlement amount you are requesting. It’s also a good idea to mention you’re hoping to resolve the claim fairly and without unnecessary delay.

This methodical approach signals to the adjuster that you're not just another disgruntled claimant. You're prepared, you’ve done your homework, and you expect them to address your points one by one.

Expert Tip: Put it in writing. Always. After any phone call, send a quick follow-up email confirming what was discussed. "Per our conversation, you stated…" This creates a paper trail that is absolutely invaluable if things get complicated.

Communication and Escalation Tactics

Once your counteroffer is sent, the real negotiation begins. Throughout every email and phone call, remain polite but firm. The adjuster is just a person doing their job, and you'll get much further with professionalism than with hostility. It's a simple truth that's easy to forget when you're frustrated.

What if the adjuster won't budge? Or if they dismiss your evidence with a vague, unhelpful response? Don't back down. It's time to escalate.

Politely ask to speak with their supervisor. A manager often has more discretion and authority to approve a higher payout. They are also motivated to resolve disputes before they turn into bigger headaches for the company. Knowing when and how to go up the chain of command is one of the most effective ways to win your total loss settlement negotiation.

By taking this structured path, you shift the dynamic from a heated argument to a straightforward business transaction. Presenting a well-supported case and using smart communication tactics will dramatically increase your odds of walking away with the fair settlement you’re entitled to.

Advanced Tactics When the Adjuster Says No

https://www.youtube.com/embed/hgeuTULUdEQ

You’ve done everything right. You’ve presented a solid, evidence-based counteroffer, but the adjuster just won’t budge. This is the point where most people get frustrated and give in, but from my experience, this is often just part of the process.

Don’t get discouraged. Hitting a wall like this is common. The real key to successfully negotiating your total loss settlement is knowing what to do when the easy conversation stops and the real negotiation begins.

Invoke the Appraisal Clause

Buried in the fine print of your auto insurance policy is a powerful tool you probably didn't know you had: the appraisal clause. Think of it as your ultimate trump card when you and the insurance company are at a complete standstill over your vehicle's value.

Invoking this clause essentially takes the decision out of the adjuster's hands. It triggers a formal, structured process:

- You hire your own certified appraiser. This is an expert who works for you and performs a truly independent valuation of your totaled car.

- The insurance company hires an appraiser. They'll bring in their own expert to do the same.

- The two appraisers try to reach an agreement. If they can't agree on a number, they'll together select a neutral third party, called an "umpire," whose decision is typically binding.

This entire process sidesteps the company's biased valuation software and forces the issue to be decided by independent professionals. It's an incredibly effective way to break a stalemate when an adjuster is stuck on an unreasonably low number.

Expert Tip: You can't just casually mention the appraisal clause on the phone. You must formally notify your insurance company in writing that you are exercising this right as defined in your policy.

Use Market Forces to Your Advantage

Sometimes, an adjuster isn't being difficult on purpose—they're just stuck using outdated data from their system. Your job is to bring them into the present reality. It’s about more than just finding a few comps; you need to build a narrative that explains why the market is the way it is.

For example, think about the massive semiconductor chip shortage that began in 2020. It crippled new car manufacturing, which sent used car prices through the roof. An insurer’s valuation from six months prior would be completely irrelevant. Their payout has to reflect the current, inflated cost to actually replace your vehicle today.

You can frame your argument around these real-world supply and demand dynamics. Point out that their offer doesn't account for these well-documented market shifts. For a deeper dive, you can learn more about how market trends influence your insurance payout.

When to Bring in the Big Guns

What if you've tried all these tactics and the insurance company is still lowballing you or seems to be acting in bad faith? At this point, it's time to escalate beyond the claims department.

You have two primary options:

- File a Complaint with the Department of Insurance: Every state has a Department of Insurance (DOI) that regulates insurance companies. Filing a formal complaint is free and can put serious regulatory pressure on the insurer. A call from the DOI gets their attention in a way you simply can't.

- Hire a Public Adjuster: Unlike the company adjuster, a public adjuster is a licensed professional who works directly for policyholders. They’ll take over the entire negotiation on your behalf. They do charge a fee—usually a percentage of the final settlement—but a good one can often increase the payout enough to more than cover their cost.

Hitting a negotiation roadblock doesn't mean you've lost. It just means it's time to change your strategy and use the more powerful tools available to you.

Answering Your Top Total Loss Questions

Even after you've done all your homework and are deep in the negotiation process, some tricky questions inevitably surface. Let's face it, the total loss process has its own strange rules that can leave anyone scratching their head. I want to tackle some of the most common ones I hear from clients to help you feel more confident as you push for a fair settlement.

Can I Keep My Totaled Car?

Yes, you almost always have this option. The official term for it is "owner retention." It’s not as simple as just saying, "I'll keep it," though. There's a catch.

Here’s how it works: The insurance company determines the full settlement amount, just like they normally would. Then, they subtract the car's salvage value—that's what they would have pocketed from selling your wrecked car at a salvage auction. You get the leftover cash, and you get to keep the car.

But be warned. Your vehicle will be branded with a salvage title. This title makes it incredibly difficult to get proper insurance, register it for the road, or ever sell it down the line. Plus, you’re on the hook for all the repairs needed to make it safe and legal to drive again.

What if I Owe More Than the Settlement Offer?

This is a gut-wrenching and surprisingly common scenario. It’s known as being "upside down" or having negative equity. The hard truth is that your standard auto policy only covers the vehicle's Actual Cash Value (ACV). It has absolutely nothing to do with how much you still owe on your loan.

You are still on the hook with your lender for the entire remaining balance. After the insurance company pays you, that difference has to come straight out of your own pocket.

This is the exact reason Guaranteed Asset Protection (GAP) insurance exists. If you bought a GAP policy when you financed the car, it's designed to pay off that difference between the ACV settlement and your loan balance. It’s time to dig through your purchase paperwork and find that policy.

How Long Does the Insurance Company Have to Settle?

There isn't a single, universal deadline that applies everywhere, but most states have laws requiring insurers to settle claims in a "reasonable" time frame. In practice, this usually means somewhere around 30 to 45 days once they have all your documentation.

Of course, "reasonable" can be a flexible term. Delays happen all the time, especially if you're disputing the value or if the insurer is swamped after a major storm or natural disaster.

If you feel like the company is intentionally dragging its feet, start documenting everything. Keep a log of every call, save every email, and note who you spoke to and when. If the delay gets out of hand, this log becomes powerful evidence when you file a formal complaint with your state's department of insurance.

Are you getting a lowball offer on your total loss claim? Don't accept it. At Total Loss Northwest, our certified independent appraisers fight for the true market value you're owed. We invoke the Appraisal Clause to force a fair settlement based on real-world data, not the insurance company's biased software. Get the fair payout you deserve.