Hearing that your car is a "total loss" is a gut punch. It’s a jarring moment that can leave you feeling stressed, confused, and worried about what comes next.

The insurance company’s declaration means they think it costs more to fix your car than it was worth right before the accident. But here's the crucial thing to remember: their initial assessment is just that—an assessment. It’s a first offer, not the final word. This is precisely where a total loss appraisal becomes your best tool for getting the fair settlement you deserve.

Your Guide to a Total Loss Declaration

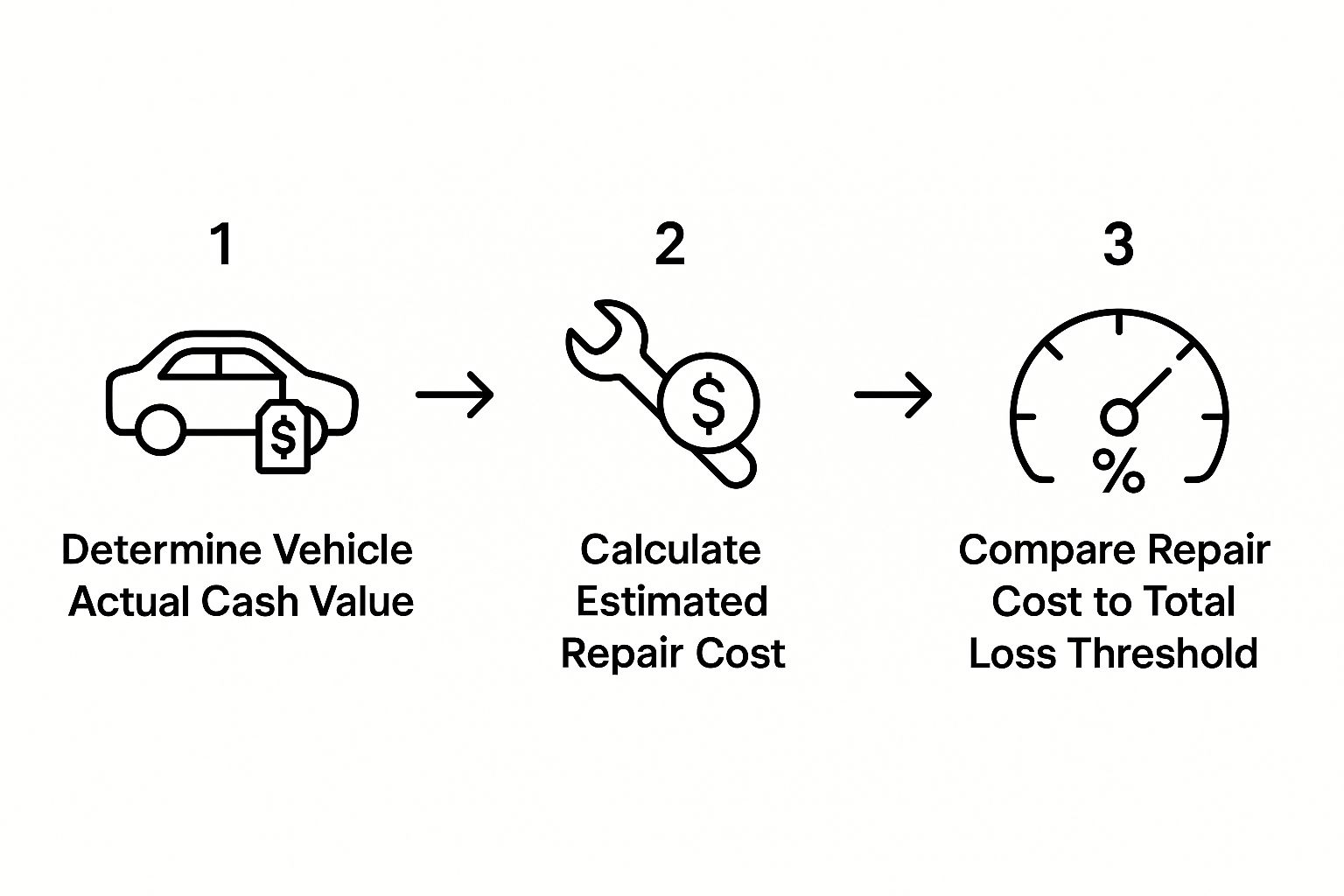

So, how does an insurance adjuster decide to "total" your car? It's mostly a math problem. They pit the estimated repair costs against your vehicle's Actual Cash Value (ACV)—what it would have sold for just moments before the crash.

If the repairs cross a certain percentage of the ACV, they'll write it off. That percentage, known as the total loss threshold, changes depending on your state and insurance policy.

But this calculation isn't always cut and dry. The insurer's first offer comes from their own valuation reports, which are notorious for undervaluing vehicles. You don't have to just sit back and accept the first number they throw at you. You have rights, and you have options.

Why Your Involvement Matters

The most important thing you can do is understand that the insurer's offer is the start of a negotiation, not the end of one. The insurance company wants to close your claim quickly and for the lowest cost possible. Your goal is to get back on your feet financially—to receive enough money to buy a comparable replacement vehicle. As you can imagine, those two goals don't always line up.

When you take an active role, you can make sure the final settlement reflects what your vehicle was actually worth. This means you need to:

- Scrutinize the insurer's valuation report for mistakes or lowball comparisons.

- Gather your own proof of your car’s condition, features, and recent maintenance.

- Build a case and present a fact-based counter-offer.

- Know when it’s time to call in an independent expert for a total loss appraisal.

A total loss declaration isn't a final verdict. It's the starting line for a settlement process. The key to a fair outcome is your active participation, ensuring the final number is based on your vehicle's real market value, not just the insurer's initial math.

Market Trends Impacting Your Settlement

The car market has been on a rollercoaster lately, and that directly affects your total loss claim. Skyrocketing prices for both new and used cars, thanks to supply chain hiccups and inflation, have made everything more complicated.

You might think higher market values are a good thing, but it's a double-edged sword. With vehicles worth more, even moderate damage can push repair costs over the total loss threshold. Add to that the expensive sensors, cameras, and computers in modern cars, and repair estimates can balloon quickly.

This combination means more cars are being declared total losses than ever before. In fact, some reports show that over 30% of auto claims in the U.S. now end up as a write-off. You can learn more about how market conditions affect total loss settlements and why your vehicle's appraisal might be higher than you'd guess. In this environment, it's absolutely vital to double-check the insurance company's figures and fight for an appraisal that truly reflects today's market.

How to Analyze the Insurer's Valuation Report

When your insurance company totals your car, they’ll send you a valuation report. This document is the absolute cornerstone of your claim, laying out exactly how they arrived at their settlement offer. But here’s the thing: it’s not a statement of fact. It’s their opening bid in a negotiation.

Think of it as their argument for why your car is worth what they say it is. Your job is to analyze that argument, find the weak spots, and come back with a stronger one based on real-world data. Learning to read this report like a pro is the single most important step you can take to get a fair payout.

Deconstructing the Report Components

That report, likely generated by a third-party service like CCC ONE or Audatex, is more than just a final number. You need to pull it apart piece by piece. It's like checking a contractor's invoice—you don't just look at the total; you check the cost of every single material and hour of labor.

The heart of the report is its list of "comparable vehicles," or "comps." These are supposedly similar cars recently sold or listed for sale in your area, and they form the baseline for your vehicle's value. The quality of these comps is everything.

From that baseline, the insurance company will make adjustments. They'll add or subtract value for key differences between your car and the comps:

- Condition Adjustments: They'll grade your car's pre-accident condition, often on a scale like "fair," "good," or "excellent."

- Mileage Adjustments: They’ll dock value for higher-than-average mileage or (hopefully) add value for low mileage.

- Option and Feature Packages: This is where they account for your sunroof, leather seats, premium sound system, or advanced safety features.

These adjustments are precisely where most of the money gets lost. An insurer might unfairly knock your car's condition down a peg or completely overlook a valuable options package. That’s why a line-by-line review is so critical. If you want more expert tips on what to look for, these auto appraisal insights can be a huge help.

The valuation report isn't a bill—it's an argument. Your job is to find the weak points in that argument by questioning the comparable vehicles, condition ratings, and adjustments. A single error can change the final settlement amount significantly.

Spotting Common Red Flags and Errors

Insurers and their valuation partners are dealing with huge volumes of claims, and mistakes happen. Some are honest oversights, but others feel a bit more strategic, conveniently lowering the payout. You need to put on your detective hat and hunt for them.

When you get their report, start by looking for some common errors. These are often the easiest to spot and can have a big impact on the final number.

Common Errors in Insurer Valuation Reports

| Error Category | What to Look For | Why It Matters |

|---|---|---|

| Vehicle Mismatches | Is your top-tier "Limited" trim being compared to a base "LX" model? Did they miss your car's All-Wheel Drive? | Trim levels and drivetrains can create value gaps of thousands of dollars. A base model is not a valid comparison for a fully loaded one. |

| Inaccurate "Comps" | Are the comparable vehicles from dealerships hundreds of miles away or even in another state? | Vehicle values are highly regional. A car's price in a different market has no bearing on its actual cash value in your local area. |

| Missed Options & Packages | Your car had a $2,000 panoramic sunroof and a premium audio package that their comps lack. | If they didn't add that value back to your vehicle's baseline, their offer is missing a significant chunk of what you're owed. |

| Unfair Condition Rating | Was your garage-kept, meticulously maintained car rated as merely "average" or "fair" without clear photos or justification? | A single-grade drop in condition can easily shave $1,000 or more off the value. The insurer must prove your car was in subpar condition. |

| Improper Mileage Adjustment | Did your car have exceptionally low mileage for its age? Did they give you proper credit for it? | Low mileage is a major value-add. They should be making a positive adjustment that accurately reflects its market desirability. |

Scrutinizing these details is not about being difficult; it’s about ensuring accuracy. After all, the insurance policy is a contract to make you whole, and that starts with getting the numbers right. Every detail in a total loss appraisal matters.

Building Your Case for a Fairer Settlement

So, you’ve taken apart the insurance company's valuation report and found the holes in their math. Good. But that’s just step one. Now, you need to switch from defense to offense and build a rock-solid, evidence-based case for what your car was really worth.

This isn't about getting emotional or making demands. It’s about presenting cold, hard facts that simply can't be ignored.

Think of it like selling a house. You wouldn't just take the first lowball offer that comes along. Of course not. You’d gather up proof of recent upgrades, find similar homes that sold for more, and show off the property's best features. It's time to do the exact same thing for your vehicle.

When you show up prepared, the entire conversation shifts. You’re no longer just another person accepting a check; you're a well-informed negotiator armed with the same kind of data the insurer uses—only your data is more accurate and tailored to your actual car.

Gather Your Own Comparable Listings

The heart of the insurer’s report is its list of "comps," and frankly, this is often the shakiest part of their valuation. Your first mission is to find better ones. You’re looking for real-world examples of what it would cost to walk out and buy a car just like yours, in your area, today.

Fire up your browser and head to sites like Autotrader, Cars.com, and even Facebook Marketplace. Be surgical with your search filters:

- Model and Trim: Make sure you’re comparing apples to apples. If you had a Honda Accord "Touring," don't let them value it like a base "LX" model.

- Year and Mileage: Stick to vehicles from the same model year with a similar odometer reading.

- Geographic Radius: This one is critical. Keep your search within a 50- to 75-mile radius of your home. The price of a car in another state is completely irrelevant to your local market.

- Drivetrain and Engine: An All-Wheel Drive (AWD) model has a different value than a Front-Wheel Drive (FWD) one. Don't let them mix these up.

Your goal is to find at least five to seven strong examples. Save screenshots or print the listings, focusing on cars being sold by dealerships, as their asking prices are generally seen as more credible than private party sales. This collection of local, relevant comps is your single most powerful weapon.

Document Every Detail of Your Car's Value

Beyond finding replacement vehicles, you have to prove what made your specific car special. This is where good record-keeping really pays off. You need to build a portfolio that tells the story of your vehicle's condition and all the money you invested in it.

An insurance company's valuation software can't see the new set of $800 Michelin tires you just bought or know that you changed the oil every 3,000 miles. Providing proof of these details is essential for correcting their baseline valuation and is a key part of any good total loss appraisal.

Put together a folder—digital or physical—and fill it with this ammunition:

- Maintenance Records: Dig up every receipt for oil changes, tire rotations, brake jobs, and any other service. This paper trail proves a history of exceptional care and justifies a higher condition rating than the "average" one they probably assigned your car.

- Recent Upgrades and Repairs: Did you install a new battery six months ago? Buy a premium set of WeatherTech floor mats? Every single receipt for parts or labor adds directly to your car’s value.

- Original Window Sticker: If you have it, the original Monroney sticker is pure gold. It lists every single factory-installed option, package, and feature, ensuring nothing gets missed.

- Pre-Accident Photos: Find photos or videos that show your car in its clean, well-maintained state before the crash. A picture is worth a thousand words when you're trying to dispute an unfair "average" or "fair" condition rating.

Walking the adjuster through this organized file changes the nature of your claim. You're not just complaining; you are providing a detailed, factual correction to their report. If you feel like you’re hitting a wall or the adjuster isn’t taking your evidence seriously, it might be time to get an expert opinion. You can get a free total loss claim review to better understand your position and options.

So, you've tried negotiating with the insurance adjuster, but you've hit a wall. It can feel like you're out of options, but your policy has a powerful, often-overlooked tool for this exact situation: the appraisal clause.

This isn't some aggressive legal maneuver; it's a standard part of your contract designed to resolve disagreements fairly. Think of it as a built-in tiebreaker. The clause allows both you and the insurer to bring in independent experts who can determine your vehicle’s true fair market value, moving the conversation away from arguments and toward facts.

The whole point is to get the number right. You hire your appraiser, the insurance company hires theirs, and these two professionals work to land on a binding value. It's a structured process that puts you back on a level playing field.

How to Formally Invoke the Clause

Using the appraisal clause isn't as simple as mentioning it on a phone call. It’s a formal step that shows the insurer you're serious about disputing their offer. You’ll need to send a written letter to the insurance company—usually addressed to the adjuster on your claim—clearly stating your demand to exercise this right.

Your letter should be firm yet professional. If you can, reference the specific language in your policy. The best way to send it is via certified mail with a return receipt requested. This small step gives you a paper trail and proof of when the insurer officially received your demand.

Once that letter is sent, the process is officially in motion. Both sides are now contractually obligated to move forward with the appraisal.

Choosing Your Champion: An Independent Appraiser

Once you've invoked the clause, your next move is crucial: hiring a qualified independent appraiser. This person is your expert advocate. Their job is to build an airtight case for your vehicle's real-world value, completely separate from the insurance company's influence.

The insurer will hire their own appraiser, too. The two experts will then share their findings and try to negotiate an agreed-upon amount. In many situations, two competent professionals can look at the same data and reach a fair conclusion without any more back-and-forth.

This infographic breaks down the typical decision-making process an insurer uses when deciding if a car is a total loss.

The key takeaway is that it all comes down to a simple comparison: your car's value versus the cost to fix it. This is a delicate balance, and as you'll see, market conditions can change the math dramatically.

The Role of the Umpire

But what if the two appraisers just can't see eye to eye? The appraisal clause has a plan for that, too. It’s called the umpire. The umpire is a neutral, third-party referee brought in to break the deadlock.

If the two appraisers can't agree, they will mutually select an umpire. This person reviews both appraisal reports and makes a final, objective decision. A settlement becomes binding as soon as any two of the three parties—your appraiser, the insurer's appraiser, or the umpire—sign off on a final value.

This three-person system is designed to keep things fair and prevent a stalemate. It creates a system of checks and balances that ensures the final number is based on evidence, not just who argues their case the loudest.

It's also worth noting how much outside economic forces can impact total loss claims. For example, while 27% of collision claims were deemed total losses in the first nine months of 2022, that figure dropped to 18.0% by the third quarter of 2023. Why the change? Soaring new vehicle prices made it more cost-effective for insurers to repair cars instead of replacing them. As market values shift, so does the math behind every total loss appraisal. You can see how these trends affect claims by reviewing the full analysis on InsuranceJournal.com.

How to Choose a Qualified Independent Appraiser

When you decide to invoke the appraisal clause, you're essentially challenging your insurance company to a duel. But your success in this duel comes down to one thing: the expert you bring to the fight. Choosing the right independent appraiser isn't just checking a box; it's the single most important decision you'll make in getting a fair total loss settlement.

Think about it. The insurance company already has its champion—a professional appraiser who lives and breathes their system. You need your own champion. You need someone with the street smarts, credibility, and sheer determination to build an ironclad, evidence-based valuation for your vehicle. A truly great appraiser doesn't just pull a higher number out of thin air; they prove it with undeniable facts.

Credentials and Experience That Matter

Let's be clear: not all appraisers are created equal. You aren't just looking for someone who can look up car values online. You need a specialist in vehicle valuation who has a deep, hands-on understanding of the appraisal clause process. Their entire job is to create a report so thorough and well-researched that the insurance company’s appraiser has no choice but to take it seriously.

When you're vetting potential appraisers, here's what really counts:

- Verifiable Certifications: Look for credentials from recognized industry organizations. This is your proof that they’ve met professional standards for training and ethics.

- Specific Total Loss Experience: Don't be shy. Ask them how many total loss appraisals they handle each year. You want someone who is in the trenches with these specific claims every day, not a generalist who dabbles.

- Knowledge of Your Vehicle Type: An expert on classic Porsches might be lost when valuing your F-150, and vice versa. Make sure their experience aligns with the kind of vehicle you lost.

A qualified appraiser's loyalty is to the facts—not to you, and not to the insurer. Their mission is to find the vehicle’s true Actual Cash Value using objective market data. That's what makes their report unbiased and defensible.

Key Questions to Ask a Potential Appraiser

Before you hire anyone, you need to interview them. Their answers will tell you everything you need to know about their process and professionalism. Treat it like you're hiring any other expert—you deserve to know exactly what you’re paying for. Getting a clear picture of the professional appraisal services provided is crucial before you sign anything.

Here’s a simple checklist of questions to ask:

- What is your exact process? Have them walk you through their methodology, from the initial vehicle inspection all the way to the final report. A real pro will have a clear, step-by-step system they can explain easily.

- What is your fee structure? This is a big one. Reputable appraisers work on a flat fee. This is critical because it ensures their payment isn't tied to the settlement amount, keeping them objective.

- Can you provide a sample report? Ask to see a redacted report from a previous case. This is your window into the quality of their work. Is it detailed? Is the evidence solid?

- How do you determine comparable vehicles? They should be able to clearly explain how they find "comps." You want to hear them talk about local, recent, and truly similar vehicle listings.

Red Flags to Watch Out For

Just as important as knowing what to look for is knowing what to run from. A few classic warning signs can help you dodge unqualified or unethical players who could do more harm than good.

Be very wary of any appraiser who:

- Guarantees a specific settlement amount. This is the biggest red flag of all. No ethical appraiser can promise an outcome before they've even started the research. It's impossible and dishonest.

- Charges a percentage of the settlement increase. This creates a massive conflict of interest. A fixed fee ensures their valuation is driven by facts, not by a bigger payday for themselves.

- Lacks a professional website or clear contact information. In this day and age, a legitimate business should be transparent and easy to get in touch with.

By taking the time to select a qualified, unbiased, and seasoned appraiser, you’re not just hiring help—you’re bringing in a powerful advocate dedicated to getting you the true value your vehicle was worth.

Frequently Asked Questions About Total Loss Claims

Dealing with a total loss claim can leave you with a lot of questions. Even when you think you have a handle on the big picture, the little details can cause a ton of stress and confusion. My goal here is to give you straightforward, practical answers to the questions I hear most often from people in this exact situation.

Let's clear up those lingering doubts so you can move forward with confidence. We’ll cover everything from what happens if you want to keep your car to whether your insurance rates are going to spike.

Can I Keep My Totaled Car and Still Get a Settlement?

Absolutely. In most states, you have the right to "retain salvage," but you need to know exactly what that means for your wallet and your car's future.

When you decide to keep the vehicle, the insurance company changes its payout math. They won't just hand you a check for the full Actual Cash Value (ACV). First, they figure out the car's salvage value—what a junkyard would pay them for the wreck. Then, they subtract that amount from your settlement.

Let's say your car's ACV is $15,000 and its salvage value is $2,000. Your final payout from the insurer would be $13,000. You get the car, but it will come with a "salvage title." Before you can legally drive it again, you'll have to get it professionally repaired and pass a strict state inspection. It can be a good move if you're a mechanic or have a solid repair plan, but be honest with yourself about the true cost and hassle involved.

What if I Owe More on My Car Loan Than the Settlement?

This is a tough spot to be in, and unfortunately, it's very common. When you owe more than the car is worth, you're "upside-down" on your loan. A standard auto policy only pays the vehicle's current market value (ACV), not what you owe the bank.

If the insurance settlement isn't enough to pay off your loan, you are on the hook for the remaining balance. This is where Guaranteed Asset Protection (GAP) insurance is an absolute game-changer.

If you bought GAP coverage when you financed your car, it’s designed specifically to cover the difference—the "gap"—between your insurance payout and what you still owe. Without it, that shortfall is your problem to solve.

For example, imagine your ACV settlement is $20,000, but your loan balance is $23,000. You'd have to come up with that $3,000 yourself. With GAP coverage, it would pay that $3,000 for you.

How Long Does the Total Loss Appraisal Process Take?

The timeline really depends on how smoothly things go. If the claim is simple and you accept the insurer's initial offer right away, you might have it all wrapped up in a week or two.

But the moment you decide to fight back, the clock starts over. Invoking the appraisal clause means you have to find and hire your own appraiser, who then needs time to build a proper valuation report. After that, the two appraisers have to negotiate. If they can’t find common ground, an umpire has to be brought in, which adds even more time.

- Simple, Accepted Claim: Typically 1-2 weeks.

- Disputed Claim (Using the Appraisal Clause): Usually takes 30 to 60 days.

- Highly Complex Cases: Can take longer, especially if one side is slow to respond.

When you dispute an offer, patience is a virtue. It's a longer road, but the point of a professional appraisal isn't speed—it's getting the fair and accurate settlement you deserve.

Will a Total Loss Claim Make My Insurance Rates Go Up?

This is the million-dollar question for most people. The answer boils down to one simple thing: who was at fault?

If the other driver caused the accident and their insurance is covering your total loss, your rates shouldn't go up. The claim is against their policy, not yours.

On the other hand, if you were at fault for the accident, you should brace for a rate increase when your policy renews. Your insurer just paid out a large claim, and they now see you as a bigger risk.

What about situations where no one is really "at fault"? If your car was totaled by something covered under your comprehensive policy—like a tree falling on it, a flood, theft, or vandalism—the hit to your rates is usually less severe than an at-fault collision. Still, some insurance companies may adjust your premium after paying out a major comprehensive claim.

When an insurance company's offer falls short, you need an expert in your corner. Loss Values Auto Appraisals specializes in creating detailed, evidence-based total loss appraisals that force insurers to pay what you're truly owed. We serve vehicle owners across Washington State, invoking the Appraisal Clause to ensure you get a fair and accurate settlement. Don't accept a lowball offer—put our certified expertise to work for you at https://totallossnw.com.