When your insurance adjuster tells you your car is a "total loss," it can be a gut-wrenching moment. But what does that term actually mean?

A total loss estimate is simply the insurance company's calculation showing that it costs more to fix your car than what the car was worth right before the accident. It's the financial tipping point where they decide to pay you for the vehicle's value instead of paying for repairs.

What a Total Loss Estimate Really Means for You

Hearing the words "total loss" often makes people think their car was completely destroyed, but that's not always the case. It’s a business decision, not a judgment on whether the car could be fixed.

Think of it this way: imagine a nasty storm damages your old garden shed. If getting a handyman to repair the roof and replace the walls costs more than the shed was worth in the first place, you’d probably just buy a new one. Insurance companies think the same way about your car.

The decision comes down to two numbers: the estimated cost of repairs versus your vehicle’s Actual Cash Value (ACV)—its market value just before the crash. If the repair bill climbs past a certain percentage of that ACV, the car gets branded a "total loss."

Understanding the Core Concepts

The whole process can feel a little overwhelming, but it really just boils down to a few key terms. Getting a handle on these now will make your conversations with the insurance adjuster much clearer and put you in a better position to negotiate.

Let's break them down.

- Actual Cash Value (ACV): This is the most important number in your entire claim. It’s what your specific car—with its exact age, mileage, and condition—was worth on the open market moments before the accident. It’s not what you originally paid for it or what a new one costs today.

- Repair Estimate: This is the total projected cost to bring your car back to its pre-accident state. It includes everything from labor and parts to paint and finishing work.

- Salvage Value: Even a totaled car has some value. Its undamaged parts and scrap metal can be sold. This residual amount is the salvage value, which the insurer gets back by selling the car to a salvage yard.

- Total Loss Threshold: Each state sets its own rule for this. It's a specific percentage (often 75%), and if the repair costs exceed that percentage of the car's ACV, the insurer is legally required to declare it a total loss.

A total loss isn't about how bad the wreck looked. It's a purely financial decision where the math says repairs don't make sense. Grasping this simple fact is your first step toward getting the fair settlement you deserve.

To help you navigate your claim, here's a quick rundown of the terminology you're likely to hear from your adjuster.

Total Loss Terms at a Glance

This table is a quick reference for the key terms you'll encounter during your total loss claim.

| Term | What It Means for Your Settlement |

|---|---|

| Actual Cash Value (ACV) | The starting point and most important number for your settlement check. |

| Repair Estimate | The figure used to see if your car crosses the total loss threshold. |

| Salvage Value | The amount the insurer recoups, which is factored into their calculations. |

| Total Loss Threshold | The state-mandated rule that forces the "total loss" decision. |

| Comparable Vehicle | A similar car used by the insurer to help determine your vehicle's ACV. |

Knowing these terms gives you a solid foundation for the road ahead.

In this guide, we'll dig deeper into how all these pieces fit together. We’ll show you how insurers calculate ACV, what you can do to challenge their offer, and what your options are once the final decision is made.

How Insurers Calculate Your Car's Actual Cash Value

When your car is declared a total loss, the entire settlement boils down to one number: its Actual Cash Value (ACV). This isn't just a figure an adjuster pulls out of thin air. It’s a calculated value meant to represent what your specific car was worth right before the accident happened.

The whole process starts with a basic formula. If you want to make sure you're getting a fair offer, you first need to understand how they get to their number.

ACV = Replacement Cost – Depreciation

Looks simple, right? But the devil is in the details—specifically, how the insurance company defines "replacement cost" and calculates "depreciation." Let's pull back the curtain on what these terms really mean for your payout.

Unpacking Replacement Cost

The phrase "replacement cost" is a bit of a curveball. It doesn’t mean the cost of a brand-new car off the lot. Instead, it’s the price of a similar used vehicle currently for sale in your local area.

Insurers hunt for what they call "comparable vehicles" or "comps." Think of these as automotive twins to your old car—the same make, model, and year, with similar mileage and options.

For example, let's say you had a 2021 Honda CR-V EX. The insurance company isn't going to look at shiny new 2025 models. They'll be scanning local dealership websites and private sale listings for other 2021 CR-V EX models to see what they're selling for. That price becomes the starting point for their calculation.

The Role of Depreciation

Once they have that baseline replacement cost, they start subtracting. This is where depreciation comes in, which is the natural drop in a car's value from everyday wear and tear. This is also where the unique history and condition of your specific car become incredibly important.

Here are the main things they'll look at to calculate depreciation:

- Mileage: A car with 80,000 miles on the odometer will naturally be worth less than an identical one with only 40,000 miles.

- Overall Condition: The adjuster’s report will list any pre-existing dings, scratches, worn-out tires, or stains on the upholstery. Every little imperfection chips away at the final value.

- Accident History: A clean vehicle history report always helps. A car that's been in a previous accident, even if it was perfectly repaired, is often valued lower than one that hasn't.

- Regional Factors: Sometimes, where you live matters. If your car model is in high demand in your city, it might hold its value better and depreciate more slowly.

Ultimately, the ACV is a snapshot of your car’s worth in the moments right before the crash. Since this number is the foundation of your settlement, it helps to see how it differs from other terms you might hear. To go a bit deeper, you can learn more about how ACV stacks up against what is fair market value in our detailed guide.

Who Actually Generates the Valuation Report

Here’s something most people don't know: insurance companies almost never do these calculations themselves. They hire big, third-party data companies to do the heavy lifting for them.

A major player in this space is a company called CCC Intelligent Solutions (you might hear adjusters refer to it as CCC ONE). These firms operate massive databases that track vehicle sales and listings all across the country.

When you file a claim, your car’s details—VIN, mileage, options, condition—get plugged into CCC's system. The software then crunches the numbers and spits out a detailed valuation report, complete with the list of "comps" it used. This report is the document the adjuster uses to make their settlement offer.

Understanding that your offer is generated by an algorithm is a game-changer. It's not a personal opinion from your adjuster; it's a data-driven report. Knowing this gives you the power to question the data, find your own comparable vehicles, and build a solid case if you feel their ACV is coming in too low.

Key Factors That Influence Your Settlement Amount

The basic formula for a total loss payout—what the car was worth right before the crash—seems simple enough. But the real work, and where the settlement amount can swing dramatically, lies in the details. No two cars are truly identical, and an appraiser’s job is to uncover all the subtle differences that affect value.

These nuances can add or subtract hundreds, sometimes even thousands, of dollars from your final check. Knowing what adjusters look for helps you see your car through their eyes, ensuring you build the strongest possible case for its true pre-accident worth.

Positive Factors That Increase Your Offer

When an insurance adjuster evaluates your vehicle, they don't just pull a number out of thin air. They start with a baseline value for its year, make, and model, then make adjustments. Your job is to give them every reason to adjust that number up.

Think of it as telling your car’s story. You need to document every single thing that made your car better than the "average" one on the road.

- Exceptional Pre-Accident Condition: Was your car always parked in the garage? Was the paint nearly flawless? If you have photos showing off an immaculate interior or a pristine exterior, now is the time to find them. "Excellent" condition is worth more than "average."

- Low Mileage: This one’s a biggie. If your car has significantly fewer miles on the odometer than is typical for its age, it commands a higher price. A five-year-old car with 30,000 miles is in a completely different league than the same model with 75,000 miles.

- Recent Upgrades and Maintenance: Did you just drop a grand on a brand-new set of premium tires? What about a new battery, brakes, or a slick audio system? Dig up those receipts! These aren't just expenses; they are investments that add real, tangible value.

- Desirable Trim Package: A base model and a fully loaded "Limited" or "Touring" model are two very different vehicles. Features like a sunroof, leather seats, or advanced driver-assist systems all contribute to a higher market value.

A total loss valuation isn’t just about the car's year and model; it's about your specific car. Every maintenance receipt and every photo is a piece of evidence that supports a better settlement.

Negative Factors That Decrease Your Offer

Just as positive features can boost your offer, negative ones can quickly pull it down. Adjusters are trained to spot any pre-existing flaws that would have lowered your car's value on the open market, and it’s critical to know what they're looking for.

These are some of the most common deductions you’ll see on a valuation report.

- Pre-Existing Damage: That dent in the bumper you never got around to fixing, the spiderweb crack in the windshield, or any significant rust—all of it will be noted and subtracted from the car's value.

- Excessive Wear and Tear: We’re talking about things beyond normal use, like bald tires, heavily stained carpets, or faded, peeling paint. These issues signal that the car was in below-average condition before the crash.

- Salvage or Rebuilt Title History: This is a major red flag for adjusters. If your vehicle had a branded title from a previous major accident, its market value is automatically and significantly lower than a car with a clean history.

Understanding both sides of the coin helps you anticipate the adjuster's reasoning and prepare your counterpoints. Knowing your car’s strengths and weaknesses is the first step in determining if their offer is truly fair. You can get a deeper look by exploring our guide that answers the question, "how much is my totaled car worth?"

The Impact of Local Market Demand

Here’s a factor many people miss: geography matters. A car’s value isn’t based on a national average but on what similar vehicles are actually selling for right in your local area.

For instance, an all-wheel-drive SUV is a hot commodity in a snowy place like Colorado, which naturally drives up its value there. That same SUV might not fetch as high a price in sunny Florida, where a convertible would likely be in higher demand. This local market dynamic is a crucial piece of an accurate total loss valuation.

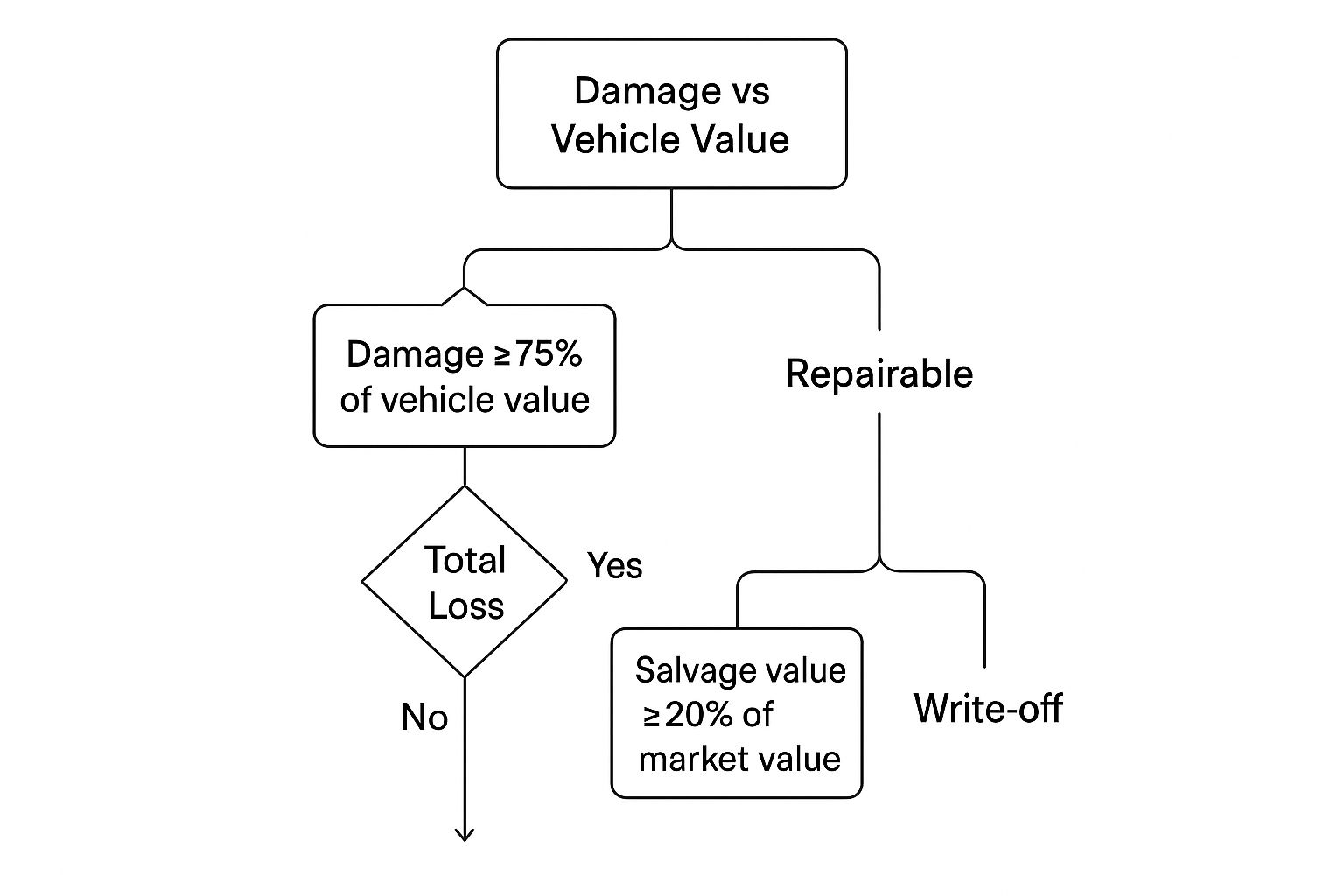

Understanding Your State's Total Loss Threshold

Did you know that whether your car gets totaled can come down to where you live? The final say on a total loss estimate isn't just the insurance adjuster's opinion. It’s actually guided by a state-specific rule called the Total Loss Threshold (TLT).

This threshold is a set percentage established by state law. If the projected cost to fix your car climbs past this percentage of its Actual Cash Value (ACV), the insurer is legally required to declare it a total loss. This process ensures dangerously damaged vehicles are taken off the road and given a salvage title, rather than being patched up poorly.

But here’s the thing: not every state plays by the same rules. Knowing which system your state uses is key to understanding how your claim might play out.

Two Main Systems for Totaling a Vehicle

States typically use one of two methods to decide when a car is officially a goner. The end goal is the same—keeping unsafe vehicles off the road—but the calculations are different.

- Total Loss Threshold (TLT): This is the most common approach. The state sets a firm percentage, usually somewhere between 75% and 100%. If the repair estimate tops this percentage of the car's pre-accident value, it's automatically totaled. It's a pretty straightforward calculation.

- Total Loss Formula (TLF): A few states opt for this more nuanced formula. It doesn't just look at repair costs; it also factors in the vehicle's potential salvage value (what the wreck is worth). The formula is: (Cost of Repairs + Salvage Value) ≥ ACV. If the cost to fix it plus its scrap value meets or exceeds its pre-accident value, it’s totaled.

The decision tree below gives you a simple look at how this logic works, using a common TLT of 75%.

As you can see, the main trigger is when repair costs hit that critical percentage of the car's worth, which starts the total loss process.

How State Laws Create Different Outcomes

Let's put this into perspective with a real-world example. Say your car has an ACV of $10,000, and the body shop quotes $8,000 for repairs.

- In Texas (100% TLT): Your repair costs are 80% of the ACV ($8,000 ÷ $10,000). Since that’s under the 100% threshold, your insurer will likely move forward with the repairs.

- In Iowa (70% TLT): That same 80% repair cost is well over Iowa's 70% threshold. In this case, the insurance company has no choice—they must declare your car a total loss.

The exact same car, with the same damage, can be considered repairable in one state and a mandatory total loss right across the state line. This is why knowing your local rules is so critical for setting your expectations.

This difference between state laws is just one of the many moving parts in the insurance industry. The scale of claims can be staggering, especially after widespread disasters. In the first half of 2025 alone, global economic losses from natural catastrophes hit $162 billion, with the U.S. accounting for $126 billion of that.

You can dig into more data on the global insurance industry to see the financial pressures that influence these regulations. Ultimately, understanding your rights within this massive system is the best tool you have for navigating your own claim.

How to Negotiate a Low Total Loss Estimate

When the insurance company sends over their total loss offer, it’s easy to feel like that number is set in stone. But it's not.

Think of that initial offer as their opening bid in a negotiation. It's the beginning of the conversation, not the end. If the amount they’re offering won't even come close to replacing your vehicle, you have every right to challenge it.

The secret is to swap emotion for evidence. A successful negotiation isn't about getting into an argument; it's about building a solid, professional case that proves your car was worth more than their report claims. This is your chance to get in the driver's seat and fight for the settlement you actually deserve.

Start by Requesting the Valuation Report

Your first move is a simple one: ask the adjuster for a full copy of the valuation report they used to calculate their offer. This document is the playbook for their entire estimate, and you can't dispute what you haven't seen.

Most of the time, this report comes from a third-party data company like CCC Intelligent Solutions. It will list the "comparable" vehicles (comps) they used to land on a value for your car, along with every adjustment made for its mileage, condition, and options. Go through this report with a fine-tooth comb, looking for mistakes or things they might have missed.

Conduct Your Own Market Research

Now, it's time to do some digging of your own. Your mission is to find a set of real-world comparable vehicles that supports a higher value for your car. Stick to your immediate area and look for the exact same make, model, year, and trim.

Use online marketplaces to build your case:

- Dealership Websites: Local dealer inventory is a goldmine. Their asking prices are almost always higher and serve as powerful proof of what it costs to replace your car in the real world.

- Online Car Listings: Sites like AutoTrader and Cars.com give you a live snapshot of your local market. Don't forget to check Facebook Marketplace, too.

- Private Party Sales: While these prices might be a bit lower than a dealer's, they still provide excellent data on what actual people are willing to pay.

Take clear screenshots of every listing that's a better match or has a higher asking price than the comps in the insurance company's report. To build the strongest argument, focus on vehicles with similar (or higher) mileage that are listed in excellent condition.

An insurance company’s valuation is based on their data. Your counter-offer must be based on your data. Presenting just two or three strong, higher-priced local comps can completely change the negotiation.

Gather Proof of Your Vehicle's Value

Finding better comps is one thing, but you also need to prove your specific car was in great shape. This is where your personal records are worth their weight in gold. Dig up any and all documentation that tells your car's story and shows why it was worth more than average.

Pull together a file with everything you can find:

- Recent Maintenance Records: Got receipts for new tires, brakes, a battery, or a recent major service? This proves you invested in keeping the vehicle in top condition.

- Photos and Videos: Pre-accident pictures showing your car looking sharp are incredibly persuasive. A clean interior, shiny paint, or aftermarket wheels can make a real difference.

- Proof of Upgrades: Did you add a premium sound system, a new exhaust, or custom rims? Find the receipts for those additions.

Organize all this evidence into a clean, easy-to-review package. The more professional you are, the more seriously the adjuster will take your counter-offer. For a deeper look at the back-and-forth process, our complete guide has more tips on how to negotiate a total loss settlement effectively.

Present Your Case and Invoke the Appraisal Clause

Once you've got your research and documents in order, draft a polite and professional email or letter to the adjuster. State clearly that you are disputing their total loss estimate and attach all of your supporting evidence—your list of better comps, the service receipts, and any photos.

If the adjuster still refuses to budge and offer a fair settlement, you have one last, powerful tool hidden in your insurance policy: the Appraisal Clause. This provision lets you and the insurance company each hire your own independent appraiser. The two appraisers then work together to agree on a value.

If they can't reach an agreement, they bring in a neutral third appraiser (an umpire) to make the final call. This process is binding, and it takes the decision completely out of the insurance company’s hands to ensure you get a fair, market-based valuation.

Your Options After a Total Loss Declaration

Once all the back-and-forth is over and the total loss estimate is set in stone, you’re at a crossroads. What happens next is your call. Knowing your options is the final step in putting this whole ordeal behind you.

For most people, the path forward is pretty clear. You accept the final settlement, sign the title over to the insurance company, and hand them the keys. They cut you a check for the car's Actual Cash Value, and you can use that money to pay off your loan and start looking for a new ride. It’s the most common and straightforward resolution.

Keeping Your Totaled Vehicle

But there’s another route you can take: owner retention. This is exactly what it sounds like—you decide to keep the wrecked car. If you choose this option, the insurance company still pays you, but they'll first subtract the car's salvage value. That’s the amount they would have gotten by selling the wreck to a salvage yard.

Before you jump at the chance to keep your car, you need to understand the serious obstacles involved.

- You're Stuck with a Salvage Title: Your state's DMV will rebrand your car's title as "salvage" or "rebuilt." This is a permanent red flag that kills its future resale value.

- Repairs Are All on You: From here on out, you're the one responsible for getting the car fixed and road-safe. It can be a costly and complicated undertaking.

- Good Luck with Insurance: Trying to get full coverage (comprehensive and collision) for a car with a salvage title is tough. Many insurers will only offer the bare-minimum liability policy.

Choosing owner retention means taking a smaller check now for a damaged car with a branded title. It’s a route really only meant for people with serious mechanical skills or a very specific, well-thought-out plan for the vehicle.

What If the Settlement Doesn't Cover Your Loan? The Role of Gap Insurance

So, what happens if the settlement offer isn't enough to pay off your auto loan? This is an unfortunately common problem known as being "upside down" on your loan, and it’s incredibly stressful. This is the exact scenario where Guaranteed Asset Protection (GAP) insurance can save the day.

If you have a gap policy, it springs into action right after your car insurance pays out the ACV. It covers the remaining difference—the "gap"—between what the insurer paid and what you still owe the bank. Without it, you’d be stuck making payments on a car you can't even drive anymore.

The broader insurance world is always in flux, which is why these protections matter. Consider that global insured losses from natural disasters are growing at a steady clip of 5% to 7% each year. These losses reached about $137 billion in 2024 and are projected to hit nearly $145 billion in 2025. You can read more about these catastrophic loss trends on swissre.com. This bigger picture just goes to show why something like gap insurance is so critical for shielding yourself from financial shocks.

Your Top Total Loss Questions, Answered

When you're dealing with a total loss estimate, a million questions can race through your mind. It's a stressful situation, so let's clear up some of the most common concerns people have.

Can I Refuse to Have My Car Totaled?

This is a big one, but the short answer is usually no. The decision isn't really up to you or even the insurance company—it's dictated by state law and the terms of your policy.

If the repair bill is higher than a certain percentage of your car's value, known as the Total Loss Threshold (TLT), the insurer is often legally obligated to declare it a total loss. You can, and should, negotiate the value of the car, but you can't typically prevent the "total loss" brand from being applied.

How Long Does a Total Loss Claim Take?

Patience is tough in these situations, but most total loss claims wrap up within 30 to 45 days. It's not a single event but a sequence: the car is inspected, the adjuster does their research to determine its value, there might be some back-and-forth negotiation, and finally, the payout and title transfer happen.

Things can get held up, of course. Delays often pop up if you and the adjuster are far apart on the Actual Cash Value or if there are snags getting the necessary paperwork from your lienholder.

Do I Still Make Car Payments After a Total Loss?

Yes, you absolutely have to. Think of your car loan as a completely separate agreement from your insurance policy. Your obligation to the lender doesn't just disappear because the car is gone.

You must keep making payments on time until your insurance settlement pays off the loan. If you stop, it will damage your credit score, plain and simple.

It's a common misunderstanding that the insurance company sorts out your loan for you from day one. In reality, you're responsible for that payment until the lender gets a check from the insurer and officially closes your account.

This is precisely where gap insurance becomes a lifesaver. It’s designed to cover the "gap" between what you owe on the loan and what the insurance company pays you, protecting you from paying out of pocket for a car you can no longer drive.

If you're in Oregon or Washington and feel your insurer's offer is way off the mark, you don't have to just accept it. At Total Loss Northwest, our certified appraisers are here to fight for the true market value you're owed. We invoke the Appraisal Clause in your policy to force a fair, evidence-based valuation. Get the settlement you truly deserve by visiting us at https://totallossnw.com.