When the insurance company says your car is a "total loss," it’s easy to feel a pit in your stomach. But all it really means is that they've calculated it would cost more to fix your car than it was worth right before the accident. This decision isn't the end of the road; it's the starting line for the total loss settlement negotiation. This is where you and the insurer work to agree on a fair payout, and knowing what's behind their decision is your first step toward getting what you're owed.

What Happens When Your Car Is Declared a Total Loss?

The adjuster's "total loss" declaration can sound final, but it's actually just the opening offer in a financial negotiation. It's not a random decision. It's based on a specific formula that pits the estimated repair costs against your car's Actual Cash Value (ACV)—in simple terms, what your vehicle was worth the moment before the collision.

This whole process is guided by something called the Total Loss Threshold (TLT). Each state has its own TLT, which is a set percentage. If the cost of repairs hits that percentage of your car's ACV, the insurer usually has to declare it a total loss. For instance, in a state with a 75% threshold, a car valued at $20,000 would be totaled if the repair bill was estimated to be $15,000 or more.

Before we dive deeper, it helps to get familiar with the language the adjusters will use. These terms will come up again and again during your claim.

Key Terms in a Total Loss Claim

Here's a quick reference guide to the essential terminology you'll encounter during your total loss settlement negotiation.

| Term | What It Means for You |

|---|---|

| Actual Cash Value (ACV) | This is the insurer's valuation of your vehicle right before the accident. It's the most important number in your settlement negotiation. |

| Total Loss Threshold (TLT) | A percentage set by your state. If repair costs exceed this percentage of the ACV, the vehicle is declared a total loss. |

| Salvage Value | The amount the insurance company can get by selling your damaged car for parts. They subtract this from your payout if you decide to keep the car. |

| Comparables (Comps) | These are similar vehicles for sale in your local market. They are used to help determine your car's ACV. You'll need to find your own to counter the insurer's lowball offer. |

| Appraisal Clause | A policy provision allowing you and the insurer to hire independent appraisers to resolve a dispute over the vehicle's value. It's a powerful tool if you reach a stalemate. |

Knowing these terms gives you a solid footing, so you're not caught off guard when the adjuster starts throwing them around.

Modern Tech is a Game Changer

You might be surprised to learn that the advanced technology in your car is a major reason why more vehicles are being totaled today. What looks like a simple fender-bender on the surface could have damaged a whole network of expensive sensors, cameras, and computers hidden inside the bumper.

These complex systems, often called Advanced Driver Assistance Systems (ADAS), can turn a repair that used to cost a few hundred dollars into a job that runs into the thousands. This spike in repair costs makes it far more likely for the estimate to blow past the state's Total Loss Threshold, even when the car looks like it could be fixed.

How the Market Affects Your Settlement

The economy has a direct say in your settlement amount, too. Over the last few years, we've seen prices for both new and used cars shoot up because of supply chain problems and inflation. This economic reality complicates things. On one hand, the higher market values mean your car's ACV should be higher. But on the other, the cost of parts and labor has also gone through the roof.

Your total loss payout today is a reflection of more than just crumpled metal. It’s a mix of your car's high market value, its complex technology, and soaring repair costs. Understanding this is key to a fair negotiation.

This is why what you do immediately after an accident is so critical. Documenting everything about the scene and your car's condition gives you the evidence you'll need later on. For a complete rundown, our guide on what to do after a car accident is a great place to start.

Ultimately, getting a handle on these concepts—ACV, the total loss threshold, and the influence of tech and market trends—is your foundation. It equips you to look at the insurance company's first offer with a healthy dose of skepticism and build a strong, data-backed case for what your car was truly worth.

Decoding the Insurer's Valuation Report

When the insurer's valuation report finally lands in your inbox, it's a pivotal moment in your total loss settlement negotiation. But don't mistake this document for a final, unchangeable verdict. Think of it as what it really is: the insurance company's opening bid.

These reports are often slapped together using automated systems like CCC ONE and can be riddled with errors, oversights, and lowball assumptions. Your job is to treat this report like a detective at a crime scene—you need to find the factual mistakes and challenge the subjective judgments that are working against you. The smallest details can easily add up to hundreds or even thousands of dollars in your pocket.

Scrutinize Every Last Detail

Start with the absolute basics. I mean, really basic. Does the report have the correct year, make, and model for your vehicle? You'd be surprised how often this gets bungled.

More importantly, you need to verify the trim level. This is a huge one. Is your car listed as a base model "LX" when it was actually the top-of-the-line "Touring" or "Limited" edition? A single mistake here can tank the value. A higher trim level means a more powerful engine, a sunroof, leather seats, a premium sound system—all things that carry real, substantial value. The adjuster might have missed this, especially if they never saw the car in person and just ran the VIN through a generic database.

Key Takeaway: Never assume the adjuster correctly identified your vehicle. The difference between a base model and a premium trim can be the single largest source of undervaluation in an initial offer.

Challenge the Condition and Mileage Ratings

Next, turn your attention to how they rated your car's condition. The report will probably use a label like "fair," "average," or "good." It’s almost a given that adjusters will default to "average," even if you treated your car like a prized possession. This is a purely subjective call, and that means it's wide open for negotiation.

- Their "average" isn't your reality. If your car had a pristine interior, no dings, and a perfect service history, it was not "average." It was "excellent" or "above average," and you should be paid accordingly.

- Mileage mistakes are surprisingly common. Triple-check that the mileage listed on the report is correct as of the accident date. A simple typo could tack on thousands of "phantom" miles, artificially dragging down its value.

This is where you bring your evidence. Have recent photos showing the car in immaculate condition? A stack of service records proving every oil change and tune-up? Use these to systematically dismantle a lazy "average" rating.

The Big Problem with Their "Comparable" Vehicles

The heart of the valuation report is the list of comparable vehicles, or "comps." These are supposedly similar cars currently for sale that the insurer uses to justify the Actual Cash Value (ACV) they're offering you. From my experience, this is where you can find the most leverage.

The software insurers use often pulls comps that aren't truly comparable at all. Here’s what you need to look for:

- Geographic Mismatch: Are their comps from dealerships 200 miles away in a totally different economic area? A car's value can swing wildly from one city to the next. Your vehicle's value must be based on your local market, since that's where you'd theoretically be shopping for a replacement.

- Incorrect Features: A "comparable" vehicle is anything but if it's missing your car's options. Did your truck have a factory tow package and a spray-in bedliner? Did your SUV have the upgraded tech package with adaptive cruise control? Every feature their comps are missing is another reason your car was worth more.

- Questionable Sources: Some reports will try to slip in comps from private party ads or even auction listings. These are not legitimate comparisons to what you would have to pay a reputable dealer for a replacement vehicle.

Your strategy is to patiently take their list of comps apart, piece by piece, by highlighting these flaws. For every bad comp they show you, be ready with a better one that you found yourself.

To get a real edge here, spending some time reviewing expert auto appraisal insights can make a world of difference. Doing this homework shifts the negotiation from their opinion versus yours to a data-driven discussion you are prepared to win.

Building Your Case for a Higher Payout

So, you’ve picked apart the insurance company’s lowball offer and you know exactly where they went wrong. Now, your total loss settlement negotiation gets a lot more interesting. It's time to stop reacting and start building a rock-solid case that shows what your vehicle was really worth. This isn’t about arguing—it’s about presenting facts they can't ignore.

The adjuster has their own data, but let's be honest, it's often curated to benefit their employer. Your job is to counter their report with better, more realistic evidence from the actual market. You need to prove what it would cost you, right now, to walk onto a local lot and buy a replacement for the car you lost.

Find Your Own Comparable Vehicles

The single most powerful piece of evidence you can have is a well-researched list of comparable vehicles, or "comps." This is your direct rebuttal to the insurer's list, especially if they’ve pulled cars from hundreds of miles away or with the wrong trim package.

Jump on popular auto sites like AutoTrader, Cars.com, and CarGurus. Don't forget to check the inventory of local dealerships in your area, too. Be methodical about it.

- Stick to Retail Value: You're looking for the retail asking price at a dealership. Ignore private party sales or trade-in values. The goal is to show the cost to buy a replacement from a dealer, which is exactly what a settlement should allow you to do.

- Keep It Local: Draw a tight circle around your home—about a 50-75 mile radius is perfect. The cost to replace a car in your city is the only number that matters. If an adjuster tries to use a comp from another state, you can and should challenge it as irrelevant.

- Match the Specs: Filter your search to mirror your vehicle’s year, make, model, trim, and mileage as closely as you possibly can.

Your goal is to find at least three to five solid examples. When you find a good one, save the listing as a PDF or grab a detailed screenshot. Make sure the VIN, features, mileage, and asking price are all clearly visible. This documentation is the bedrock of your counteroffer.

Document Everything That Adds Value

Beyond finding comps, you have to prove what made your specific car special. Every dollar you put into maintaining or upgrading your vehicle added to its value before the accident, but the adjuster won't know about any of it unless you show them proof.

Start by pulling together maintenance records from the last year or two. Did you just put on a new set of premium tires? Find that receipt. Had the brakes and rotors replaced a few months back? Document it. These records prove your car was in excellent mechanical shape, justifying a higher valuation than the generic "average" condition the insurer probably assigned it.

A car with $2,000 in recent, documented work (like new tires and a timing belt service) is worth more than an identical one without it. Don't let that money disappear—prove its value with receipts.

The same goes for any aftermarket parts. While policies often have limits for custom equipment, many practical and valuable upgrades should absolutely be part of the conversation.

This could be things like:

- A high-end stereo system

- A remote starter

- A spray-in bedliner for your truck

- Upgraded wheels or a suspension lift

If you have the paperwork for these items, get it ready. This level of detail turns your claim from a vague "my car was in great shape" into a verifiable, fact-based argument for more money. It also paints a clear picture of your vehicle's true worth. And if you suspect your vehicle’s value was impacted by a prior incident before it was totaled, getting a free diminished value assessment can help you understand how that might factor in.

Present Your Case Professionally

Once you have your evidence—your list of local comps, service records, and receipts for upgrades—organize it all into a clean, professional package. Don't just email the adjuster a jumble of random files and expect them to connect the dots.

Draft a simple summary letter or email that lays out your argument. Start by stating the fair value you've calculated, then introduce your evidence. For example, "Attached you will find listings for three comparable vehicles for sale at local dealerships, showing an average asking price of $22,500."

When you build your case this way, you fundamentally change the dynamic of the negotiation. You’re no longer just the person questioning their numbers; you're the person who has done the homework and provided a detailed, evidence-backed report they have to take seriously.

Time to Talk: How to Negotiate with the Adjuster

Alright, you’ve done your homework. You have a folder (digital or physical) stuffed with comps, receipts, and proof of your car’s true value. Now comes the part where all that preparation pays off: talking to the insurance adjuster.

The key here isn’t to be aggressive or confrontational. The goal is to be firm, professional, and laser-focused on the facts you've gathered. You're not starting a fight; you're presenting a case.

Your opening move is to send a demand letter. It sounds formal, but it's really just a clear, professional way to present your counteroffer. This isn't the time for a long, complicated legal document. You're simply stating your position and showing the adjuster that you're organized, serious, and ready to talk specifics.

How to Write a Demand Letter That Gets Results

Think of your demand letter as your case presented on a single page. It needs to be logical, concise, and backed up by every piece of paper you’ve collected. Remember, adjusters are swamped. Making your argument easy to understand is half the battle.

Here’s how to structure it:

- Get Straight to the Point: Open by clearly rejecting their initial offer and stating your calculated value. For example, "I am writing to formally reject the settlement offer of $18,500. Based on my attached research, the fair market value for my vehicle is $22,500."

- Show Your Work: Briefly explain how you arrived at your number. You don’t need to write an essay. Just point them to the evidence. "This figure is based on the attached comparable vehicle listings from local dealerships, my vehicle's extensive maintenance history, and receipts for the recent tire and brake replacement."

- Stick to the Facts: Keep emotion completely out of it. Language like "I was insulted by your low offer" is a dead end. Instead, focus on the data. Try something like, "The initial valuation appears to have overlooked the premium sound system and used comparables from over 200 miles away, which don't reflect our local market."

This simple shift changes the entire conversation. You've moved it from a vague disagreement over opinions to a concrete discussion about facts and data. Now, the adjuster has to respond to your specific points.

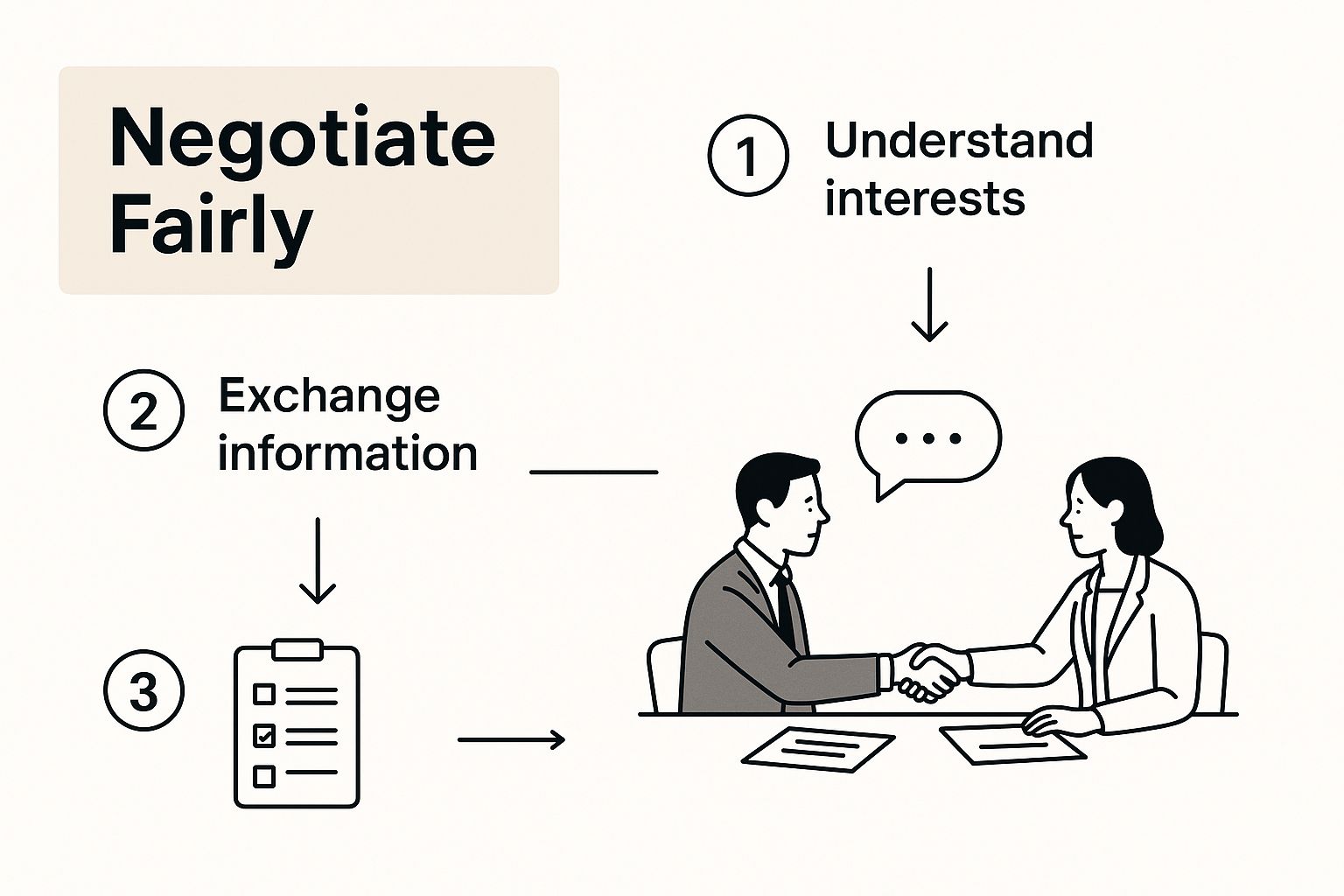

This infographic breaks down the core elements of a fair and effective negotiation.

As you can see, a successful negotiation is always built on a foundation of solid evidence and professional communication. That's what leads to a fair agreement.

Handling the Phone Calls and Follow-Ups

Once you send your demand letter, the adjuster will likely call you. Every single conversation from this point on is part of the negotiation. Your job is to be polite, patient, but absolutely persistent.

Keep in mind who you're talking to. The adjuster is an employee with performance targets and a massive caseload. When you present an organized, evidence-based argument, you actually make their job easier. It gives them the justification they need to approve a higher amount and close your file.

My Favorite Pro Tip: After every phone call, send a quick follow-up email. It's a game-changer. Just summarize what was discussed. For example: "Hi [Adjuster's Name], just wanted to recap our call. As we discussed, you'll be reviewing the five local comps I sent and re-evaluating my vehicle's condition from 'average' to 'excellent.' Thanks!" This creates a paper trail and holds everyone accountable.

Don't forget that outside forces can impact your claim. Widespread events, like the semiconductor shortages a few years back, can dramatically increase the value of used cars. That shortage slowed new car production, which in turn drove up demand and prices for used vehicles. Insurers had to raise their total loss payouts to reflect this new reality. If you want to dive deeper, you can learn more about how market trends impact insurance payouts on totallossappraisals.com.

Knowing When to Push and When to Be Patient

In any negotiation, patience is your superpower. After you’ve sent your counteroffer, give the adjuster some breathing room to review everything. A week is perfectly reasonable. If you haven't heard back by then, a polite and friendly follow-up call or email is in order.

That said, don't let them string you along forever. If you feel like you're being stonewalled or just getting the runaround, it's time to apply a little gentle pressure. You might casually mention that you’re aware of your state’s Department of Insurance guidelines for timely claim handling.

It’s a balancing act, for sure. You want to be cooperative, but you also need to be taken seriously. At the end of the day, the adjuster wants to close your file. By being the claimant with the logical, well-documented case, you make it easy for them to give you a fair settlement and move on.

When the Adjuster Just Won't Budge

So you've done everything right. You've built a rock-solid case for your vehicle's value, presented it clearly, and negotiated in good faith. And still, the adjuster is stuck on a lowball number that just doesn't make sense.

This is a frustrating, but common, scenario. Don't throw in the towel. Your total loss settlement negotiation isn't over—it's just time to escalate. You have a few powerful tools at your disposal, and knowing how to use them can break the deadlock.

Your Secret Weapon: The Appraisal Clause

The first, and often best, move is to invoke a special provision hiding in plain sight within your auto policy: the appraisal clause. Most people have no idea it’s there, but it’s essentially a built-in dispute resolution process.

Think of it as calling in the referees. Invoking this clause takes the decision away from the adjuster and puts it into the hands of independent experts.

Here’s the play-by-play:

- You hire your own appraiser. This needs to be a certified, independent professional who will perform their own detailed valuation based on your car's actual condition, all its features, and the real-world local market.

- The insurance company hires theirs. They'll do the same, bringing in their own independent appraiser to value the vehicle.

- The two appraisers talk. Their job is to hash it out and agree on a fair number. If they can't reach an agreement, they jointly select a neutral third appraiser, known as an umpire, to cast the deciding vote. The umpire's valuation is almost always binding.

This process forces everyone to get serious by bringing in objective third parties. Yes, you have to pay for your own appraiser, but that investment can easily pay for itself. A successful appraisal can result in a final settlement that's thousands of dollars higher than the insurer’s “final” offer.

Expert Take: The appraisal clause is your contractual right to a fair second opinion. It replaces a potentially biased adjuster’s valuation with a professional, market-driven assessment. It’s the single most effective tool you have.

Getting the State Involved

What if your policy doesn't have an appraisal clause, or if the insurer is dragging its feet, not returning calls, or using other bad-faith tactics? Your next step is to file a complaint with your state's Department of Insurance (DOI).

This isn't just a venting session; it's a formal grievance that gets a regulator's attention.

Filing a complaint is free and usually straightforward to do online. You'll submit all your evidence—your valuation report, your counteroffer letter, and a log of your communications. The DOI will then open a case and formally demand an explanation from the insurance company. That official inquiry from a government agency is often all it takes to get an insurer to suddenly become much more reasonable.

It’s also helpful to know that negotiation is a standard part of the claims process in the U.S. While settlement rates for insurance claims can be as low as 15% in some parts of Europe, they are often above 66% in countries like Australia. Here in the States, settlement rates are consistently above 20%. This shows that pushing back is not unusual; it's an expected part of the system. You can see a full breakdown of these figures in this study on global claim settlement trends.

Bringing in the Big Guns: Hiring an Attorney

If all else fails, it might be time to consider hiring an attorney. This is the final escalation point and is usually necessary only in specific situations, like if the insurance company is acting in clear bad faith, refusing to honor the contract, or if your claim also involves significant personal injuries.

A good lawyer can be a powerful ally. But they don't work for free. Most personal injury and bad faith attorneys work on a contingency fee, meaning they take a percentage of your final settlement. For a straightforward dispute over a few thousand dollars on vehicle value, the cost of an attorney might eat up any gains.

In most cases, the appraisal clause or a DOI complaint is a far more cost-effective path. But if you truly believe the insurer is breaking the law or screwing you over, a legal consultation is the best way to understand and protect your rights.

Got Questions? Let's Talk Total Loss Scenarios

No matter how much homework you do, you're bound to hit a few tricky spots during a total loss settlement negotiation. This is where the rubber meets the road, and specific, sometimes sticky, situations pop up that can leave you second-guessing your strategy. Let's walk through some of the most common questions I hear from clients and give you the straightforward answers you need.

So, Can I Keep My Wrecked Car?

This question comes up all the time. The short answer is: probably. The official term for this is "retaining salvage," which is just a fancy way of saying you buy the wrecked car back from the insurance company.

Here’s how it works. The insurer will figure out the car's salvage value—basically, what it would fetch at a scrap auction. They then subtract that amount from your settlement. For example, if your car's value is settled at $15,000 and the salvage value is $1,500, you’d get a check for $13,500 and keep the car.

A word of caution, though. Once you do this, the state will issue a salvage title. Getting that car legally back on the road involves extensive repairs and a rigorous inspection process, not to mention finding an insurance company willing to cover it. It can be a real headache, so make sure you understand the full cost and effort involved before you say yes.

What If Their "Comparable" Cars Are a Joke?

This is a classic move. The adjuster sends you a valuation report, and the "comps" they used are nothing like your car. Don't just accept it; this is a major negotiation point. Your job is to call them out on it.

Politely but firmly, you need to dissect their list and explain why it's inaccurate. I see these common problems all the time:

- Wrong Trim Level: They're comparing a base model to your top-of-the-line, fully-loaded version. That's not a fair comparison.

- High Mileage: A comp with 30,000 more miles is obviously worth less.

- Bad Condition: Are the photos showing dings, rust, or a trashed interior? Point it out.

- Wrong Location: A car listed 300 miles away doesn't reflect your local market. It needs to be a vehicle you could reasonably go out and buy today.

You have to dismantle their flawed evidence and replace it with your own research. Show them what it would actually cost to buy a true replacement for your car, right here in your area.

The entire point of a total loss negotiation is to agree on a real-world replacement cost. Your own research into local, comparable vehicles is the strongest card you can play to prove what that number truly is.

Does the Settlement Include Taxes and Fees?

This is a detail that can easily add up to hundreds of dollars, and it's something adjusters often "forget" in their first offer. Whether the insurance company has to cover sales tax and title fees comes down to two things: your state's laws and the fine print in your policy.

In many states, insurance regulations are clear that a settlement must make you "whole." Being made whole means covering the entire cost of replacing your vehicle, which absolutely includes the taxes and fees the government will charge you to register your new car.

Take a few minutes to check your state's Department of Insurance website for its rules on total loss claims. If the law says they have to pay, you need to bring this to the adjuster's attention and insist it's included in the final payout. It's your money, don't leave it on the table.

If you're hitting a brick wall with a stubborn adjuster or just feel in over your head, you don’t have to fight this alone. Loss Values Auto Appraisals is in the business of fighting for vehicle owners in Washington. We invoke the Appraisal Clause in your policy to force a fair, market-based settlement backed by certified evidence. Get the expert help you need to secure the payout you're truly owed. Find out how we can help at totallossnw.com.