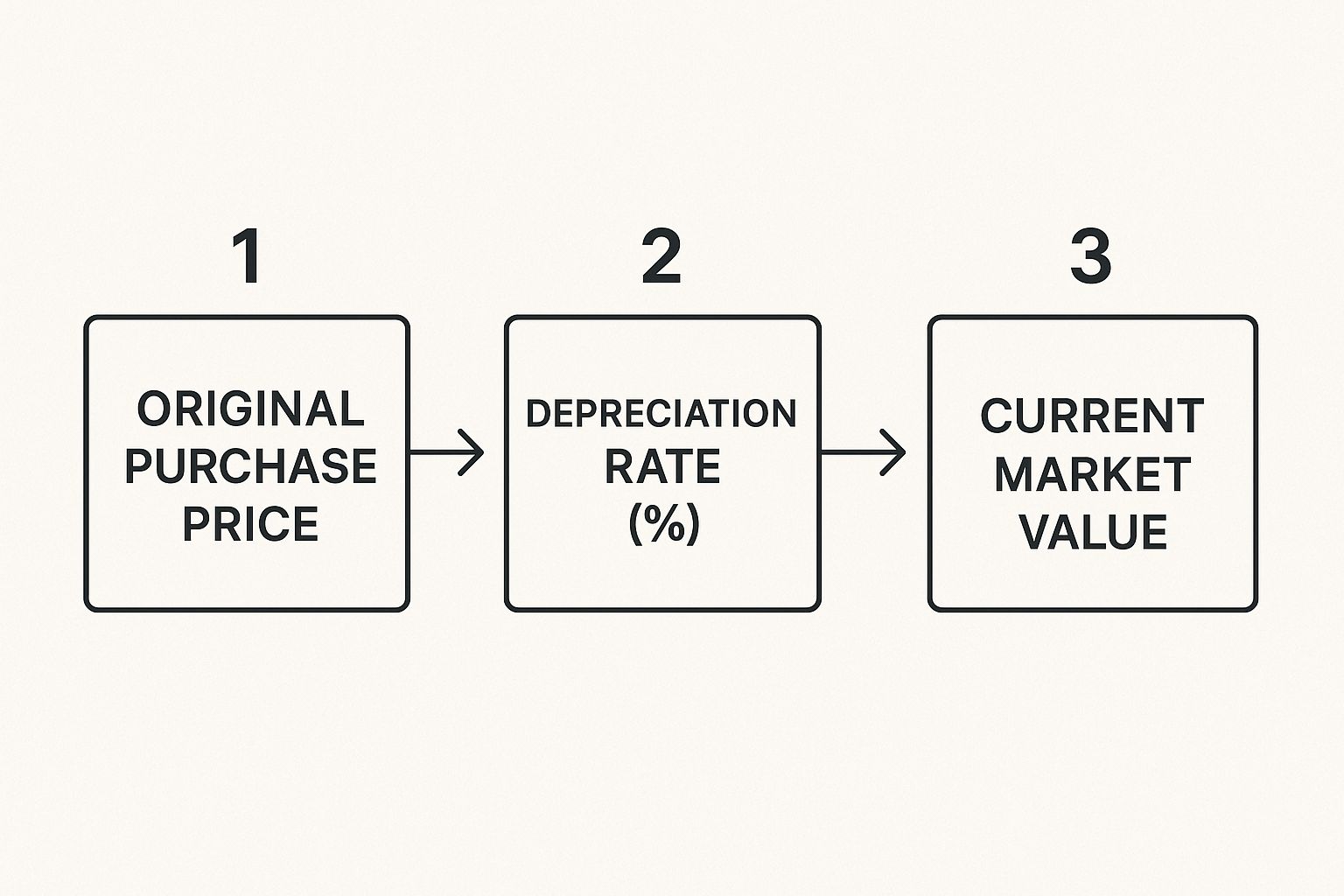

When an insurance company declares your car a total loss, they aren't looking at what you paid for it or how much you still owe on your loan. They're focused on a single, critical number: what your car was worth the moment before the accident happened.

This figure is known as the Actual Cash Value (ACV), and it's meant to represent the money you'd need to buy a similar replacement vehicle in your local area. Getting a handle on this concept is the first, and most important, step toward making sure you get a fair settlement.

Decoding Your Total Loss Vehicle Value

Hearing an adjuster say your car is a "total loss" is jarring. It immediately triggers a flood of questions, but the most important one is simple: "What was my car actually worth?" The answer to that question is its Actual Cash Value, the number at the very heart of your insurance claim.

The whole point of an insurance payout is to "indemnify" you. That’s a bit of industry jargon that just means they want to put you back in the same financial position you were in right before the crash. It isn't about getting you a brand-new car or paying off your loan; it’s about giving you enough cash to buy a comparable used vehicle.

ACV and the Principle of Indemnity

Let's break it down. Imagine you were driving a five-year-old sedan with 60,000 miles on the odometer. The insurance company’s job is to figure out what it would cost to buy another five-year-old sedan with similar mileage and features in your town. Their payout is designed to cover that cost—nothing more, nothing less. This keeps people from profiting from an accident, which is a foundational rule of insurance.

This is where many people get tripped up. The total loss value is tied to the car's reality in the current market, not your personal financial investment in it. Factors that seem important to you, like the original sticker price or what you still owe the bank, don't actually drive the ACV calculation.

The Actual Cash Value is a snapshot in time. It captures your vehicle’s fair market price, including depreciation, one second before the accident occurred. It's a measure of replacement cost, not original cost.

To really get this, it helps to see how ACV differs from other terms you'll hear thrown around. Each one tells a piece of your car's financial story, but only ACV is used to calculate your settlement check.

Vehicle Value Terms at a Glance

Getting a grip on the terminology is half the battle. This quick comparison table breaks down the key terms so you can see exactly what your adjuster is talking about and what they’re not.

| Valuation Term | What It Means for You | Used in Your Settlement? |

|---|---|---|

| Actual Cash Value (ACV) | The market value of your vehicle right before the accident, factoring in depreciation. | Yes – This is the primary figure. |

| Replacement Cost | The cost to replace your damaged vehicle with a brand-new car of the same make and model. | No (Unless you have special coverage). |

| Loan Balance | The amount you still owe to your lender for the vehicle. | No – This is separate from the car's value. |

| Sticker Price (MSRP) | The manufacturer’s suggested retail price when the car was brand new. | No – This does not account for depreciation. |

As you can see, the only number that truly matters for a standard policy is the Actual Cash Value. Your loan balance and the original price tag are part of your financial picture, but not the car's market value today.

How Insurers Calculate Your Car's Value

When your insurance adjuster comes back with a settlement number for your totaled car, it’s not something they’ve pulled out of thin air. The entire process is surprisingly data-driven. Insurers almost always rely on detailed valuation reports from big third-party companies like CCC Intelligent Solutions or Mitchell International to figure out the total loss vehicle value.

Think of these platforms as the industry's go-to source for this kind of thing. They're constantly crunching numbers from a massive pool of automotive sales data. Their main job is to pinpoint your car's Actual Cash Value (ACV)—essentially, what your exact car was worth in your local market just moments before the crash. To really make sense of your settlement offer, you have to get a handle on how these reports are put together.

Finding "Comps" in Your Local Market

The whole valuation process starts with a hunt for "comparable vehicles," or "comps" for short. This is the cornerstone of the entire report. The system scours recent sales records and current dealership listings to find cars that are a close match to yours.

It's a bit like a detective narrowing down a list of suspects. The system filters by several key data points:

- Make, Model, and Year: This is the obvious starting point, like finding all 2019 Honda CR-Vs.

- Trim Level: It then gets more specific, separating an EX-L from a base LX model, which can make a big difference in value.

- Major Options: Next, it looks for key features. Did your car have all-wheel drive, a sunroof, or that fancy tech package?

- Geographic Location: The search is hyper-local, focusing on vehicles sold recently in your area, usually within a 50- to 150-mile radius.

The system then takes a handful of these real-world examples to create a baseline value. For example, if three similar 2019 CR-Vs sold for an average of $22,500 near you, that figure becomes the starting point for your car's valuation. This is done to make sure the ACV reflects the reality of what it would cost you to buy a similar replacement vehicle nearby.

The Art of Adjustments: Fine-Tuning the Final Offer

Finding a few comps is just step one. Since no two used cars are ever truly identical, the next phase is all about making specific dollar-value adjustments. This is where the adjuster refines the baseline number to account for the unique differences between your car and the comparable ones. The details really matter here.

These are the most common adjustments you'll see:

- Mileage: This is a big one. If your car had 40,000 miles but the comps averaged 55,000 miles, you'll get a positive adjustment added to your car's value. On the flip side, higher-than-average mileage will result in a deduction.

- Condition: The adjuster gives your car a condition rating (excellent, average, fair, etc.). If your car was garage-kept and in pristine shape, you should see its value go up. Dents, scratches, or significant interior wear will pull the value down.

- Features and Packages: What if your car had extras that the comps didn't, like a premium sound system or a tow package? Each of those unique features should be accounted for with a positive adjustment.

Key Takeaway: Your final settlement offer is a custom-built number. It starts with a market baseline from comparable cars and is then meticulously adjusted up or down based on your vehicle's specific mileage, condition, and features.

This process is designed to be as objective as possible, but it's not foolproof. Mistakes can happen, which is why it's so important to review your valuation report with a critical eye. Since these calculations can get pretty complex, it helps to dive deeper and learn more about what Actual Cash Value really means for your car and how it directly shapes your settlement.

Key Factors That Influence Your Valuation

When an insurance company calculates your car’s value, the make, model, and year are just the starting point. The real story—and the final number on your check—is in the details. Dozens of smaller factors can swing the total loss vehicle value by hundreds or even thousands of dollars, so knowing what they are is your best defense against a lowball offer.

Think of it like appraising a house. Two homes on the same street, built in the same year, can be worth vastly different amounts depending on their upkeep, renovations, and unique features. It’s the exact same principle with your car, and the adjuster's report needs to reflect these critical nuances.

The Big Two: Mileage and Condition

Mileage is a huge one. An adjuster isn't just glancing at your odometer; they’re comparing that number to the typical mileage for a car of its age in your specific area. If your car has way fewer miles than average, it's worth more, and that should be reflected as a positive adjustment. On the flip side, a vehicle with a lot of road behind it will naturally see its value docked.

Condition is just as important, but it’s also where things can get subjective. The adjuster will grade your car’s interior and exterior, looking at everything from stains on the seats and cracks in the dashboard to dings, rust, and the amount of tread left on your tires. A meticulously maintained, garage-kept car in "excellent" shape is going to fetch a much higher price than one rated as "average" or "fair."

Pro Tip: If your car was in fantastic shape before the crash, dig up some recent, date-stamped photos to prove it. This kind of evidence is your best tool for challenging an unfairly low condition rating and pushing for a better valuation.

Where You Live and What You've Got: Location and Options

Believe it or not, your zip code matters. A vehicle's value is directly tied to local supply and demand. For instance, a 4×4 truck or an all-wheel-drive SUV is going to be a hotter commodity—and therefore more valuable—in a snowy state like Washington than it would be in sunny Southern California. Adjusters use local market data to account for these regional differences.

Factory options and trim packages can also create a massive gap in value. A base model and a fully loaded version of the same car could be thousands of dollars apart. You need to comb through the valuation report to make sure every single feature has been accounted for, including things like:

- Premium Packages: Sport, technology, or enhanced safety packages.

- Upgraded Features: A sunroof, leather seats, or a high-end sound system.

- Engine Type: A beefy V8 engine has a different value than the standard four-cylinder.

The Paper Trail: Documenting Upgrades and Vehicle History

This is where your own records can really pay off. Did you recently put on a new set of tires? Or maybe you had major work done, like a new transmission or engine? These kinds of investments can seriously boost your car's value, but only if you have the receipts to prove it. Without documentation, the adjuster has no reason to add a dime for those improvements.

A clean vehicle history also adds to its worth. A car with a single owner and no previous accidents is always more appealing than one with a spotty past. Any prior accidents, even if they were properly repaired, can drag down the ACV.

Depreciation is the constant force pulling your vehicle's value down. In a recent year, the average vehicle depreciated 12.5%, and some models took an even bigger hit. To learn more about these trends and the long-term financial impact of a prior accident, you can find a great overview at DiminishedValueofGeorgia.com.

Market Trends and Their Economic Impact

Ever wonder why the value of a car seems to fluctuate so much? It’s not a number cooked up in a back room; your vehicle's worth is tied directly to the wild, often unpredictable, used car market. The settlement offer you get from an insurer is a direct result of big-picture economic news, from supply chain headaches across the globe to what kind of cars people are suddenly desperate to buy.

Think of your total loss vehicle value like a stock price. It bobs and weaves based on supply, demand, and the general health of the economy. It’s not just about your car's mileage or condition, but its place in this massive, constantly moving system. Once you understand these forces, you can see your valuation for what it really is: a snapshot in a fast-changing marketplace.

Getting a handle on this is key. When you know how market trends shape a car's worth, you're in a much better position to understand the true fair market value of your vehicle and figure out if your insurance offer is actually fair.

The Ripple Effect of Supply and Demand

The simple economic rule of supply and demand has a huge, real-world impact on your car's value. The last few years have been a perfect storm to illustrate this. When global shutdowns and chip shortages slammed the brakes on new car production, dealer lots started looking pretty empty.

That scarcity sent a massive ripple through the entire auto industry. Buyers who couldn't find a new car turned to the used market, causing demand for good pre-owned vehicles to explode. With everyone clamoring for a limited supply, used car prices shot up to levels we'd never seen before.

As a result, the Actual Cash Value (ACV) for many popular cars jumped significantly. A car valued at $18,000 one year might suddenly be worth $21,000 the next, all thanks to these outside pressures. If your car was totaled during that time, this chaos likely worked in your favor, leading to a much higher settlement than you might have expected.

Key Insight: Your car’s value is a moving target. It’s directly linked to the availability of new and used cars on the market, making it sensitive to everything from factory slowdowns to shifts in what everyone wants to drive.

This market volatility has made things tricky for everyone. While prices have started to settle down a bit, the market is still finding its footing. Recent data highlighted on ClaimsJournal.com projects that the average total loss vehicle market value in the U.S. will be 8.5% above historical trends by next May. Canada is on track for an even bigger jump of 13.2%, showing just how strong the rebound is.

Inflation and the Bigger Economic Picture

It's not just about how many cars are for sale. Broader economic forces, especially inflation, have a major say in your vehicle's value. When the price of everything from a gallon of milk to a new pair of shoes goes up, you can bet the cost of cars—both new and used—will climb right along with it. This directly impacts the valuation databases insurers use.

Think about how these factors connect:

- Cost of Parts and Labor: As inflation makes steel, plastic, and microchips more expensive, the cost to build and repair cars rises. This, in turn, makes existing cars on the road more valuable.

- Consumer Buying Power: When the economy feels shaky, people tend to hang onto their cars longer. This tightens the supply of used vehicles for sale, which helps keep prices firm.

- Interest Rates: Rising interest rates make new car loans more expensive. This can push more buyers into the used car market, bumping up demand and prices.

All these pieces are tangled together. Higher manufacturing costs mean higher sticker prices on new cars, which suddenly makes a well-kept used car look like a much better deal. Understanding this web of influences helps you see that your car's total loss value isn't just some random number—it’s a direct reflection of the economy we're all living in.

How Your Car's Age and Type Shake Up Its Value

It’s no surprise that not all cars are valued the same way, but the differences can be stark when you're dealing with a total loss vehicle value. The age and type of your vehicle aren't just minor details; they are major factors that can completely change the numbers on a settlement offer. An almost-new sedan, a decade-old pickup truck, and a brand-new electric vehicle (EV) are all worlds apart in the eyes of an appraiser.

To get a fair payout, you have to understand these nuances. The market forces that prop up the value of a three-year-old car are totally different from what makes a classic collectible or a high-tech hybrid desirable. Each has its own depreciation curve, market quirks, and valuation headaches.

The Predictable Value of Newer Cars

When a car is only a few years old, its value tends to be more stable and easier to pin down. In recent years, with new car production struggling to keep up, these "gently used" vehicles have become hot commodities. That surge in demand means their values hold up surprisingly well, slowing down the steep depreciation that usually happens in the first few years.

The data backs this up. A recent analysis of total loss trends showed that vehicles between zero and three years old saw their average market value climb by 0.96% in a single quarter. Meanwhile, older cars (seven to nine years old) actually dropped in value over the same period. You can explore more about these trends and what they mean for total loss valuations to see how the market is shifting.

The Wild West of Valuing Older and Classic Cars

Once a vehicle starts to get on in years, the game changes. Its value becomes less about the original sticker price and more about its real-world condition and what buyers are willing to pay for it today. A ten-year-old car might have a low "book value," but if it's a popular model that's been babied its whole life, its true market value could be way higher than what some software spits out.

And then there are classic or collector cars. Standard valuation methods are practically useless here. Their worth is a unique blend of things like:

- Rarity: How many were made? How many are left?

- Originality: Is it "numbers matching" with the factory engine?

- Condition: Is it a pristine restoration or a well-preserved survivor?

- Provenance: Can you trace its ownership history?

For a special vehicle like this, a standard total loss offer will almost always be too low. You'll need a specialized appraisal to even get close to its true value.

Key Takeaway: An older car's value is less about its age and more about its condition, reliability, and current market demand. A classic car's value is a completely different story, driven by rarity and historical significance.

The New Frontier: EV and Hybrid Valuations

Electric and hybrid vehicles are the latest puzzle for insurance appraisers. This market is moving so fast that the usual valuation playbooks can’t keep up, making it tough to calculate an accurate total loss vehicle value.

A few key factors make their values much more volatile than gas-powered cars. The biggest one is battery health and degradation—after all, the battery is the most expensive part of the car. On top of that, technology is advancing at lightning speed, which can make a three-year-old EV feel ancient and hurt its resale value. Throw in ever-changing government tax credits and incentives, and you have a recipe for unpredictable market swings.

Getting a fair valuation for an EV or hybrid isn't impossible, but it demands a real understanding of this specific, fast-changing corner of the auto world.

How to Negotiate Your Settlement Offer

Getting that first settlement offer for your totaled car can be a real gut punch, especially when it’s far lower than you expected. But here’s something the insurance company might not tell you: that first number is rarely the final number. Think of it as their opening bid in a negotiation. You absolutely have the right to question their math and fight for what your car was actually worth.

This isn't about getting into a shouting match. It's a business discussion, and the person with the best data usually wins. The insurance adjuster has laid out their case with a valuation report. Now, it's your turn to build a strong, evidence-backed counter-case. The secret is to stay professional, organized, and armed with solid proof of your vehicle's true total loss vehicle value.

Scrutinize the Insurer's Report

Your first step is to get a copy of the insurance company's valuation report and go through it with a fine-tooth comb. Don’t just look at the final dollar amount. You need to understand exactly how they got there, because small mistakes can add up to big money.

Look closely for common errors like these:

- Wrong Trim or Options: Did they value your fully-loaded Limited model as a base trim? That’s a difference of thousands of dollars right there.

- Missing Features: Make sure every single factory option is accounted for—the sunroof, the premium sound system, that advanced safety package.

- Unfair Condition Rating: If your car was pristine but they’ve knocked it down to "average" condition, that’s a huge red flag and a major point you need to dispute.

- Bad "Comps": Are the "comparable" vehicles they used to set the price really comparable? Dig into the details. A car with 30,000 more miles or a history of accidents isn't a fair comparison to your well-maintained vehicle.

Build Your Own Valuation Case

Once you know where their report falls short, it's time to build your own. This is where you go on the offensive, proving what it would actually cost to replace your car in your local market today.

Put on your detective hat. Jump onto sites like Autotrader and Cars.com, and don't forget to check local dealership websites. Your mission is to find at least three to five vehicles for sale that are a direct match: same make, model, year, and trim, with very similar mileage. Screenshot or save these listings—they are your gold-standard evidence.

Next, package everything up professionally. You want to send the adjuster a file that includes:

- A clear, point-by-point list of the errors you found in their report.

- The real-world comparable listings you found.

- Receipts for recent, significant work like new tires, a new transmission, or major brake service.

- If you have them, date-stamped photos showing your car's great condition before the accident.

Key Takeaway: A successful negotiation is built on evidence, not emotion. Your goal is to calmly and logically walk the adjuster through your findings, showing them exactly why your valuation is more accurate than theirs.

For a deeper dive into these tactics, our guide on how to negotiate a total loss settlement offers even more strategies to make sure you're in the strongest possible position.

Escalate if Necessary

What if you present your rock-solid case and the adjuster still won't budge? You're not out of options. Most auto insurance policies have something called an "Appraisal Clause."

This clause is your right to an impartial second opinion. It lets you and the insurance company each hire an independent, certified appraiser. Those two experts then try to agree on a fair value. If they can't agree, a neutral third-party "umpire" is brought in to make the final call, which is binding on everyone.

Yes, hiring your own appraiser costs money upfront. But if the gap between their offer and your car's real value is thousands of dollars, it’s often an investment that pays for itself many times over. An expert appraisal brings a level of credibility that an insurance company simply can't ignore, forcing them to look beyond their own biased software and settle based on the real-world market.

Frequently Asked Questions About Total Loss Claims

Even when you understand the basics of how a total loss vehicle value gets calculated, the real-world process can still leave you with a ton of questions. Let's tackle some of the most common things drivers ask after their car has been declared a total loss.

Can I Keep My Car After It's Totaled?

Yes, in most cases, you can. This is called "owner retention."

Here's how it works: the insurance company will calculate your car's Actual Cash Value (ACV) and then subtract its salvage value (what they could get for it at a scrap auction). You get paid the difference.

Just be warned, it's not a simple process. The car will be given a salvage title, which means it can't be legally driven until it passes a tough state inspection. On top of that, finding an insurer willing to cover a salvage-title vehicle can be difficult and expensive.

What if I Owe More on My Loan Than the Settlement Offer?

This is a tough spot to be in, and it's more common than you might think. It’s known as being "upside-down" or having "negative equity."

Your insurance payout is based strictly on the car's market value, not your loan amount. If there's a shortfall, you are still on the hook for paying the remaining balance to your lender.

This is exactly why GAP (Guaranteed Asset Protection) insurance exists. If you purchased a GAP policy, it's designed to cover that very "gap" between what the insurance company pays and what you still owe the bank.

The total loss timeline can vary, but you should typically see the valuation report within one to two weeks of the declaration. If you need to negotiate, that will add more time. Once you accept an offer, payment is usually sent out within 3-7 business days.

It's also worth looking into what smaller items are covered. For example, some policies have specific provisions for things like car key replacement insurance, which can be a separate but related headache.

If your insurance company's settlement offer feels off, don't just accept it. At Total Loss Northwest, our certified appraisers are here to fight for the fair value you're actually owed. We dig into real market data to challenge lowball offers and make sure you have the funds you need to move forward. Visit us at https://totallossnw.com and get an expert in your corner.