A trustworthy totalled car value calculator is your best tool for pinning down your vehicle's Actual Cash Value (ACV) from before the accident happened. That number—not what it costs to fix the car—is what your insurance settlement is built on. Figuring this out on your own is the single most important first step you can take toward a fair negotiation.

Your Car Is Totalled What Happens Next

When the insurance adjuster says the words "it's a total loss," your head starts spinning. It's an overwhelming moment that immediately leads to a flood of questions about what your car was really worth and how you're supposed to be compensated for it.

A car gets the "totalled" label when the repair bill is higher than its pre-accident value—a threshold that actually changes depending on your state and insurance policy. From this point on, your focus shouldn't be on the crumpled metal, but on proving that pre-accident value.

This is where doing your homework becomes your greatest advantage. Before you even think about accepting an insurer's offer, you need to build a solid case for your car's true worth. An independent valuation gives you the facts and figures you need to have a real conversation with your adjuster, not just take what you're given.

The Rising Tide of Total Loss Claims

If it seems like more cars are being written off these days, you're not wrong. We're seeing historic highs in total loss claims. This surge is driven by a perfect storm of skyrocketing repair costs and the increasingly complex technology packed into modern vehicles.

Just look at the numbers from Copart, one of the biggest auto salvage auction companies. They reported a record-breaking total loss frequency of 22.2% in a recent fiscal year. That means more than one out of every five vehicles with an insurance claim ended up as a write-off instead of getting repaired. You can get more details on this trend and what it means for drivers from this Auto Body News report.

Key Takeaway: Remember, the insurance company wants to close your claim as quickly and efficiently as possible. Their first offer is just that—an offer. It's a starting point for discussion, not the final word, calculated with their own software that might not fully capture your car's unique condition or recent upgrades.

Why Your Own Valuation Matters

Simply accepting the insurance company's number can mean leaving a significant amount of money behind. Their valuation is based on their data and their interpretation, which can easily miss the details that made your car special. Taking matters into your own hands puts you in a much better negotiating position.

Here's why getting your own valuation is so critical:

- It sets a realistic baseline. You'll have a data-driven starting point for your negotiation, not just a gut feeling.

- It helps you spot discrepancies. You can compare your valuation report with the insurer's and easily find mistakes in mileage, condition ratings, or included features.

- It gives you leverage. Showing up with a valuation from a respected source proves you’ve done your research and are serious about getting a fair settlement.

The goal here is to shift your role. You're no longer just passively accepting an offer; you're becoming an active, informed participant in determining your car's true value.

Building Your Vehicle Evidence File

When an insurance adjuster looks at your claim, they see a number in a system. They haven't driven your car or seen how well you cared for it. It's your job to show them the real story, and that starts with building an undeniable file of proof.

Think of it as creating a complete biography of your vehicle. Every receipt, photo, and record you gather helps transform your car from a generic statistic into a specific, well-maintained asset. This file is your ammo, first for the totalled car value calculator and then for the negotiation table.

You're essentially painting a detailed picture for the adjuster, one so clear they can't ignore the true, higher value of your car.

Start With the VIN

The Vehicle Identification Number (VIN) is your starting point. It's the DNA of your car, and running a full vehicle history report is the single most important first step you can take. This isn't just a formality; it's how you establish a baseline of facts.

A good report will instantly confirm key details that directly influence value:

- Original Equipment: It lists every single factory-installed option—that premium sound system, the sunroof, the upgraded trim package. These are often missed by an insurer's initial assessment.

- Accident History: It shows any previous damage. It's best you know this upfront because you can be sure the insurance company will look for it.

- Title Status: Crucially, it verifies a clean title, which is fundamental to getting top dollar for your vehicle.

Document Every Dime You've Spent

Next, it's time to prove your car was in great shape and that you invested in keeping it that way. An adjuster isn’t just going to take your word for it when you say you just bought new tires. You need to show them the receipts.

Start digging through your glove box and file cabinets for anything and everything that proves the car's condition and value.

- Maintenance Records: Gather every receipt you have for oil changes, tire rotations, brake jobs—all of it. A consistent service history is a powerful argument for a higher condition rating.

- Recent Repairs & Upgrades: Did you put a new set of tires on last year? That $1,200 receipt is hard evidence. A $2,500 transmission service a few months back? That adds real, provable value.

- Pre-Accident Photos: This is a game-changer. Dated photos or videos showing your car looking pristine just before the accident can shut down any attempt by the insurer to slap a low "average" or "fair" condition rating on it.

By putting this file together, you’re moving the conversation from opinion to fact. Each receipt and photo is another reason the adjuster has to take your valuation seriously. This isn't just paperwork; it's leverage.

How Insurance Companies Calculate Your Car's Value

When your insurance company slides a settlement offer across the table, that number isn't just a random guess. It’s the result of a specific calculation to pinpoint your vehicle’s Actual Cash Value (ACV) at the very moment before the crash. If you want to spot where their offer might be falling short, you have to understand their process.

Think of ACV this way: it's not what you paid for the car, and it's certainly not what a brand-new one costs today. It’s the fair market replacement cost, minus depreciation. To get this figure, insurers rely on powerful software that crunches huge amounts of market data.

They’re trying to answer one core question: "What would a reasonable person have paid for this exact car yesterday?" Knowing what factors go into that answer is your key to using a totalled car value calculator effectively and arming yourself for a successful negotiation.

Breaking Down the ACV Formula

At its heart, the insurer's calculation starts with the basics—your car's year, make, and model. From there, they start adding and subtracting value based on its unique story.

Here’s what they look at:

- Mileage: This is a big one. More miles on the odometer almost always means a lower value due to expected wear and tear.

- Condition: The adjuster will grade your car's pre-accident condition (poor, fair, good, excellent). This is subjective and a common point of dispute.

- Factory Options: That panoramic sunroof, upgraded sound system, or tech package you paid extra for? They add value, but only if they’re actually noted in the report.

- Geographic Location: A 4×4 truck is worth more in a snowy place like Washington than it is in sunny Florida. Local market demand is a huge factor.

It's worth noting that rising repair costs are causing more vehicles to be declared total losses. Even with used car prices stabilizing, they're still way above pre-pandemic levels. Meanwhile, the cost to fix anything continues to climb. For more on this, you can explore the latest claims data.

Every one of these details creates a unique value profile for your vehicle. A simple mistake—like missing a key option package or misjudging the condition—can leave you with a settlement offer that’s hundreds, or even thousands, of dollars too low.

For a deeper dive into this, check out our guide on understanding what the Actual Cash Value of your car is and how adjusters come up with that number.

The Problem With "Comparable" Vehicles

To justify their ACV number, adjusters look for "comps"—comparable vehicles that have recently sold in your area. In theory, these are cars of the same make, model, and year, with similar features and mileage. The prices they sold for create a baseline for your car’s value.

But here's the catch: the quality of the comps they choose is everything.

An insurer might cherry-pick listings from a dealer known for lowball pricing or use a vehicle that was a base model when yours was fully loaded. This is often the weakest link in their valuation and the best place for you to push back by finding your own, more accurate comps.

Modern cars add another layer of complexity. Features like advanced driver-assistance systems (ADAS) boost a car’s value, but they also make repairs incredibly expensive. A fender-bender that takes out a few sensors can easily total a vehicle, making a valuable safety feature the very reason your car gets written off.

Key Factors Influencing Your Car's Total Loss Value

To really get a handle on your car's ACV, it helps to see all the moving parts in one place. The table below breaks down the primary elements that affect your vehicle's value and what you need to do to make sure each one is counted correctly.

| Factor | Description | Your Action Item |

|---|---|---|

| Year, Make, Model | The starting point for any valuation. This establishes the baseline value before any adjustments. | Double-check that the insurer has listed your exact model and trim level (e.g., a Honda Accord EX-L, not just an Accord). |

| Mileage | A primary driver of depreciation. Lower mileage than average for its age increases value; higher mileage decreases it. | Provide the exact mileage at the time of the accident. Find records of recent oil changes or service invoices that show the odometer reading. |

| Overall Condition | A subjective grade (excellent, good, fair, poor) based on interior/exterior wear, mechanical state, and tire condition. | Gather pre-accident photos, maintenance records, and receipts for recent work (like new tires or brakes) to prove your car's condition was better than "average." |

| Optional Features | Any factory-installed options beyond the base model, such as a premium sound system, sunroof, or advanced safety package. | Find your car's original window sticker or use a VIN decoder to create a complete list of all factory options. Do not let the insurer overlook them. |

| Geographic Market | The value of your car based on supply and demand in your specific city or region. | Ensure the comparable vehicles used in the valuation report are from your local market, not from hundreds of miles away where prices might be lower. |

By meticulously reviewing each of these factors in the insurance company's report, you can pinpoint inaccuracies and build a strong case for a higher, fairer settlement. Don't assume they got it right—your job is to verify everything.

Getting an Independent Valuation with a Total Loss Calculator

Alright, you've got your folder full of documents and photos. Now it's time to put that information to work and come up with your own number. This is where you shift from defense to offense. Using a trusted online calculator, like the ones from Kelley Blue Book (KBB) or Edmunds, lets you generate an independent, data-backed valuation.

The goal isn't to find one magic number. It's about building a credible, defensible value range that you can use to push back against the insurance company's almost-always-low initial offer.

Be obsessive about accuracy when you're punching in the details. Every single factory option matters—that sunroof, the upgraded sound system, the tech package. They all add up. It’s also critical to select the correct trim level. A Honda Accord EX-L is worth a lot more than a base LX model, and your valuation needs to reflect that reality.

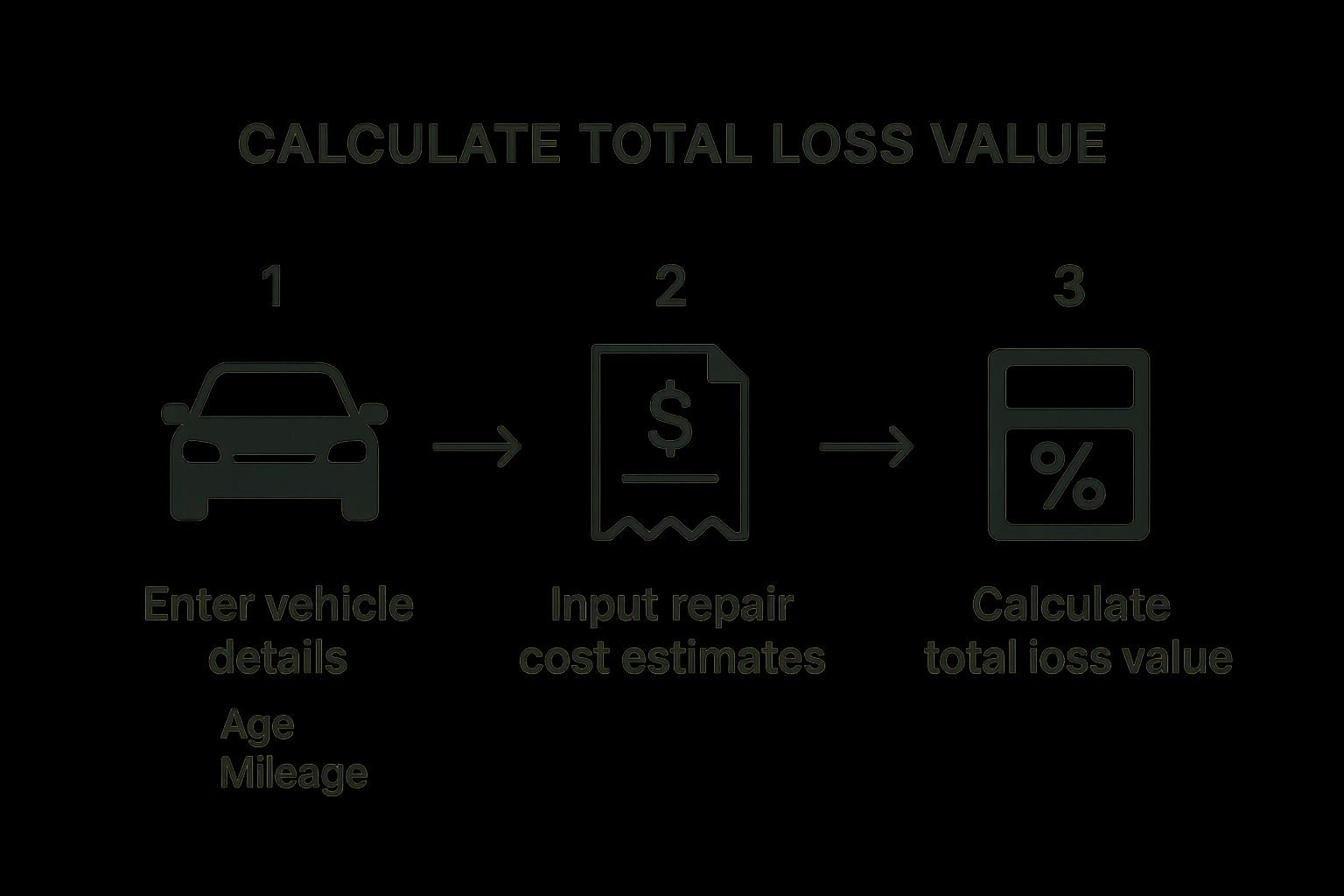

The whole process is pretty simple. You plug in your car's details and the repair estimates, and it spits out a value.

This infographic breaks it down visually:

As you can see, combining your vehicle's specific features with the cost of damages gives you a clear valuation. This is the ammo you need for your claim.

Understanding the Different Value Types

When you use these online tools, you’ll see a few different values pop up. The two you absolutely need to know are "Private Party" and "Retail." Knowing which is which is a cornerstone of your negotiation strategy.

- Private Party Value: This is what you could realistically expect to get if you sold your car to another person. Think of it as the middle-of-the-road price.

- Retail Value: This is what a dealership would slap on the windshield if they were selling the exact same car on their lot. It's always higher because it accounts for their overhead, reconditioning costs, and profit.

For your total loss claim, you need to anchor your argument to the retail value. Why? Because your insurance policy is meant to make you whole again. "Making you whole" means giving you enough money to go out and buy a comparable replacement vehicle. Most people do that at a dealership, not from a stranger on Craigslist.

Key Takeaway: Insurance adjusters love to base their first offer on the private party value or, even worse, the rock-bottom "trade-in" value. By starting the conversation with a well-documented retail valuation, you immediately reframe the negotiation and put them on the back foot.

This is more important than ever. While newer cars being totalled has climbed to nearly 10%, older vehicles still represent a huge chunk of total loss claims at about 32%. You can learn more about these total loss statistics and what other consumers are experiencing to get a better feel for the market.

Turning Your Numbers Into a Negotiation Tool

Once you have your valuations, don't just jot them down. Print out the full, detailed reports from at least two different sources (KBB and Edmunds are a great pair). These printouts are now official exhibits in your evidence file. They're no longer just your opinion—they are objective, third-party assessments of what your car was worth moments before the crash.

Now, when you talk to the adjuster, you're not just saying, "I feel like my car was worth more."

Instead, you’re presenting evidence and stating, "According to established industry guides, the retail replacement cost for my vehicle is X, and here are the reports to prove it." This data-first approach carries far more weight and is much harder for an insurer to brush aside.

If you want to dive deeper, our guide on using a car value after accident calculator offers more specific tools and tips. A little bit of prep work here can completely change the tone of your claim, turning it from a simple plea into a well-supported case for the compensation you deserve.

Knowing When to Call in an Independent Appraiser

A total loss calculator is a fantastic starting point. It gives you a solid, data-backed baseline to work from. But what happens when your research and the insurance company’s offer are miles apart?

When you’ve presented your facts and the adjuster won't budge, or the numbers are off by thousands, it's probably time to bring in a professional.

Think of hiring a certified independent appraiser not as giving up, but as leveling the playing field. These experts work for you, not the insurance company. They provide an unbiased, deeply researched valuation that holds up under scrutiny—and often carries real legal weight.

Their entire job is to dig deeper than an overworked adjuster ever will. They conduct a thorough, hands-on inspection and scour the local market, building a detailed report that can uncover the value your insurer conveniently missed. It's a clear signal that you’re serious about getting a fair settlement.

Red Flags That Scream "Get an Expert!"

It can be tough to know when to escalate a claim. But from my experience, a few situations almost always call for a professional's touch. If any of these sound familiar, it's a good sign you should at least consider hiring an appraiser.

Here are the biggest tell-tale signs:

- There’s a Huge Value Gap: The insurer's offer is $2,000, $3,000, or even more below what your research shows. This isn't a simple rounding error; it’s a major disagreement on your car's fundamental worth.

- Your Vehicle is Special: You've got a classic, a heavily customized ride, or a model with rare factory options. The cookie-cutter software insurers use is notoriously bad at valuing anything outside the norm.

- They Downplay Your Car's Condition: The adjuster slapped an "average" or "fair" condition rating on your garage-kept, meticulously maintained car, torpedoing its value. An appraiser provides an expert, documented opinion on its true pre-accident condition.

- The Adjuster Hits a Wall: You’ve sent them your calculator report, comparable listings, and service records, but the adjuster simply refuses to have a meaningful negotiation. They just keep repeating their initial lowball number.

An independent appraiser's report isn't just a "second opinion." It’s a formal, evidence-based challenge to the insurance company's valuation. When you invoke the "Appraisal Clause" in your policy, their findings can force the insurer to defend their low offer against an expert's detailed analysis.

What the Appraisal Process Actually Looks Like

Once you bring in an expert, things move pretty quickly. The appraiser will start by reviewing all the documentation you’ve gathered. Then, they'll perform their own inspection—even on the wrecked vehicle—and dive into the local market to find truly comparable sales.

They take all this information and compile it into a comprehensive valuation report.

This report is your ultimate negotiation weapon. It’s not just a number on a page; it’s a point-by-point argument for your car's real value, backed by market data, photos, and professional analysis. If you're ready to find a qualified pro, our guide can help you locate an independent auto appraiser near you to fight on your behalf.

Yes, there's an upfront cost for the service, but it’s a flat fee—not a percentage of your settlement. In most cases, that initial investment pays for itself many times over by securing a final payout that truly reflects what you lost.

Wrestling with the Aftermath: Your Top Total Loss Questions Answered

Getting a fair value for your car is a huge step, but it’s often just the beginning. The total loss process can quickly spiral into a confusing mess of paperwork, jargon, and tough decisions. Suddenly, you're juggling questions about your loan, what happens to your insurance rates, and whether you can even keep the car.

It’s a stressful time, no doubt. But knowing what to expect can make a world of difference. I've walked countless people through this process, and the same questions come up time and time again. Let's tackle them head-on so you can move forward with confidence.

Can I Keep My Car If It's Declared a Total Loss?

Believe it or not, yes, you usually can. This is called "owner retention," and it’s an option most insurance companies offer.

Here’s the catch: the insurer will pay you the car's Actual Cash Value (ACV) minus its salvage value. That salvage value is what they would have gotten by selling the wreck at auction. The bigger issue, though, is that your car will be branded with a "salvage title." Getting a car with a salvage title legally repaired, re-registered, and, most importantly, insured can be an uphill and expensive battle. It's rarely worth the headache.

What Happens If I Owe More Than the Car Is Worth?

This is the dreaded "upside-down" scenario, and it's unfortunately common. If your loan balance is higher than the insurance payout, you are on the hook for that remaining amount. You’ll have to pay it out of pocket.

This is exactly why GAP (Guaranteed Asset Protection) insurance exists. If you have a GAP policy, it steps in to cover that financial "gap" between the insurance settlement and your loan balance. Without it, you're stuck making payments on a car that's sitting in a salvage yard.

A Pro Tip: When you're upside down on a loan, fighting for a fair ACV is absolutely critical. Every single dollar you can get the insurance company to add to their offer is a dollar you don't have to pay back to the bank. A solid valuation is your best leverage.

How Do I Negotiate a Better Settlement Offer?

Successful negotiation is all about facts and evidence, not frustration. The only way to counter a lowball offer is to build a rock-solid case for why your car was worth more.

First, dissect the insurance company’s valuation report. They make mistakes all the time. Look for errors in:

- Mileage: Is it correct? Even a small error can change the value.

- Condition: Did they mark your meticulously cared-for car as just "average"?

- Features: Are all your options and packages listed? Sunroof, premium sound system, tow package—they all add value.

Next, you bring your own proof to the table. Arm yourself with valuation reports from online calculators, receipts for recent work (like new tires or a major service), and listings for truly comparable cars for sale right in your area. Keep your communication professional and polite, but always circle back to the data.

Will a Total Loss Wreck My Insurance Rates?

It depends, and the deciding factor is fault. If you were found to be at fault for the accident, you can almost certainly expect your premiums to go up when your policy renews. From the insurer's perspective, you're now a bigger risk.

If you weren't at fault, your rates probably won't be affected, but it’s not a guarantee. Every company and state has slightly different rules. The best thing to do is just ask your agent directly what to expect so there are no surprises down the road.

Dealing with a total loss is a tough situation, but you shouldn't feel like you're in it alone. If the insurance company is playing hardball and their offer just doesn't add up, it's time to call in a professional. At Total Loss Northwest, our certified appraisers specialize in fighting for the true market value of your vehicle, making sure you get the settlement you deserve. Learn how we can help you get a fair and accurate appraisal today.