The phrase you're looking for when dealing with an insurer is Actual Cash Value (ACV). This isn't what you paid for the car or what it would cost to buy a new one. Instead, ACV represents your car's fair market value the moment before the crash happened, factoring in all the depreciation it's seen over the years. Getting your head around this concept is the first, most crucial step toward getting a fair payout.

Your Car Is Totaled What Happens Now

Hearing an insurance adjuster say your car is "totaled" is a gut-punch. It's a stressful moment that immediately floods your mind with questions about what’s next. At its core, a car is declared a total loss when the cost to fix it is higher than what the vehicle is actually worth.

It’s just like a house that's been severely damaged. If a fire causes $300,000 in damage to a home valued at only $250,000, it makes no financial sense to rebuild it. Your car is no different. The insurer has run the numbers and decided that paying for the repairs is a bad investment. Instead, they’ll offer you a cash settlement based on your car's pre-accident value.

Understanding the Total Loss Process

Once the "totaled" verdict is in, a surprisingly structured process kicks off. This journey involves a few key people, each playing a specific part in deciding the final payout. Knowing who does what will cut through the confusion and put you in a better position to navigate the system.

Here's how it usually unfolds:

- Initial Assessment: An insurance adjuster will look over your vehicle, estimating the repair bill and noting its condition before the accident.

- Total Loss Declaration: If the repair estimate crosses a certain threshold—a percentage of the car's value that varies by state—the insurer will officially declare it a total loss.

- Valuation Report: The insurance company puts together a report that breaks down how they arrived at your car's Actual Cash Value (ACV).

- Settlement Offer: You get the official offer. This is the amount they're prepared to pay for your car, minus any deductible you owe.

- Final Steps: From here, you can accept their offer, negotiate for more, or, in some states, choose to keep the wrecked car (with a reduced settlement).

When your vehicle is declared a total loss, understanding the right way of filing a car accident claim becomes your immediate priority.

Key Players in a Total Loss Claim

You're not on this journey alone—you'll be interacting with several different people. It's crucial to understand their roles so you can have a smoother, more effective claims process.

The key to a fair settlement is recognizing that while the process is standardized, the initial offer is often a starting point for discussion, not a final, unchangeable number.

This table breaks down who’s involved and what they’re responsible for when determining the value of your totaled car.

| Player | Primary Role | Key Responsibility |

|---|---|---|

| You (The Vehicle Owner) | Advocate for a Fair Value | Provide all necessary documentation, review the settlement offer with a critical eye, and be prepared to negotiate if the valuation seems off. |

| Insurance Adjuster | Company Representative | Inspect the vehicle damage, estimate repair costs, and calculate the initial settlement offer based on company guidelines and data. |

| Third-Party Valuation Company | Data Provider | Supply the insurer with market data and sales of comparable vehicles to help establish a baseline Actual Cash Value. |

| Independent Appraiser | Neutral Third-Party | Provide an unbiased vehicle valuation if you dispute the insurer's offer, which helps level the playing field during negotiations. |

Now that you've got the basics down, we'll dive deeper into how that ACV is actually calculated and, more importantly, what you can do to make sure the final number is fair.

Getting to the Bottom of Actual Cash Value: The Heart of Your Settlement

After the shock of an accident, if your insurance company declares your car a total loss, you're going to hear one term over and over again: Actual Cash Value, or ACV. This isn't just industry jargon; it's the single most important number that will determine the check you receive.

So, what is it? Think of ACV as your car's market price the exact moment before the accident occurred. It’s not what you paid for it years ago, and it’s certainly not what a brand-new one would cost today. It’s the amount a willing buyer would have paid for your specific car, in its pre-accident condition, on that day.

This is a crucial point to understand. Your policy is meant to indemnify you—to cover the value of what you lost—not to put you in a brand-new vehicle. This is why the value of a totaled car is fundamentally tied to depreciation.

The Basic ACV Formula

Insurers don’t just pick a number out of a hat. They follow a clear, methodical process to calculate their initial offer, which always starts with a basic formula.

Base Value − Depreciation & Adjustments = Actual Cash Value (ACV)

It begins with a "base value" for your car's make, model, and year, which they pull from market data of recently sold comparable vehicles in your area. From there, an appraiser will make a series of adjustments—some adding value, some subtracting it—to zero in on your car's unique worth. You can get a more detailed breakdown in our guide on what is actual cash value of my car.

Understanding this process is more important than ever. In 2021 alone, there were 4.2 collision claims per 100 drivers. With the average cost of full coverage insurance hitting around $2,019 in 2023, it’s clear that total loss claims are a reality for thousands of drivers every year. You can dive into more U.S. auto insurance trends to see the full picture.

How Adjustments Shape Your Final Offer

That base value is just a starting point. The real nitty-gritty of determining the value of a totaled car is in the adjustments. This is where an appraiser digs into the specific details of your vehicle, and these details can swing the final number significantly.

Key factors that influence your car's ACV:

- Mileage: This is a big one. A car with lower-than-average miles for its age is worth more. High mileage will pull the value down. It's a direct measure of wear and tear.

- Overall Condition: This covers everything from the paint job to the upholstery. Was it garage-kept and pristine, or did it have a few dings, scratches, and stains? Any pre-existing damage will result in a negative adjustment.

- Factory Options: That sunroof, leather interior, or premium tech package you paid extra for at the dealership absolutely adds value. A fully-loaded model will always have a higher ACV than a base model.

- Recent Upgrades & Maintenance: Did you just shell out for four new tires? Or a new battery? If you have receipts for recent, significant work, it can prove your car was well-maintained and add value back to the final offer.

A Practical Example of ACV in Action

Let's walk through a real-world scenario. Say you own a 2019 sedan. The insurance company’s market report shows that similar models in your zip code have been selling for around $18,000. That’s your base value.

Now, the appraiser’s report comes in with a few specific notes:

- Your car’s odometer is 20,000 miles below the average for its model year. (Positive Adjustment: +$750)

- It came from the factory with the upgraded sound system and tech package. (Positive Adjustment: +$400)

- There was some noticeable curb rash on the wheels and wear on the driver’s seat. (Negative Adjustment: -$350)

The insurer then crunches the numbers to find the final ACV:

$18,000 (Base Value) + $750 (Low Mileage) + $400 (Options) – $350 (Condition) = $18,800 (Final ACV)

This $18,800 is the number their settlement offer will be built on (before they subtract your deductible, of course). By seeing how these pieces fit together, you’re in a much stronger position to review their report and make sure the valuation is fair and accurate.

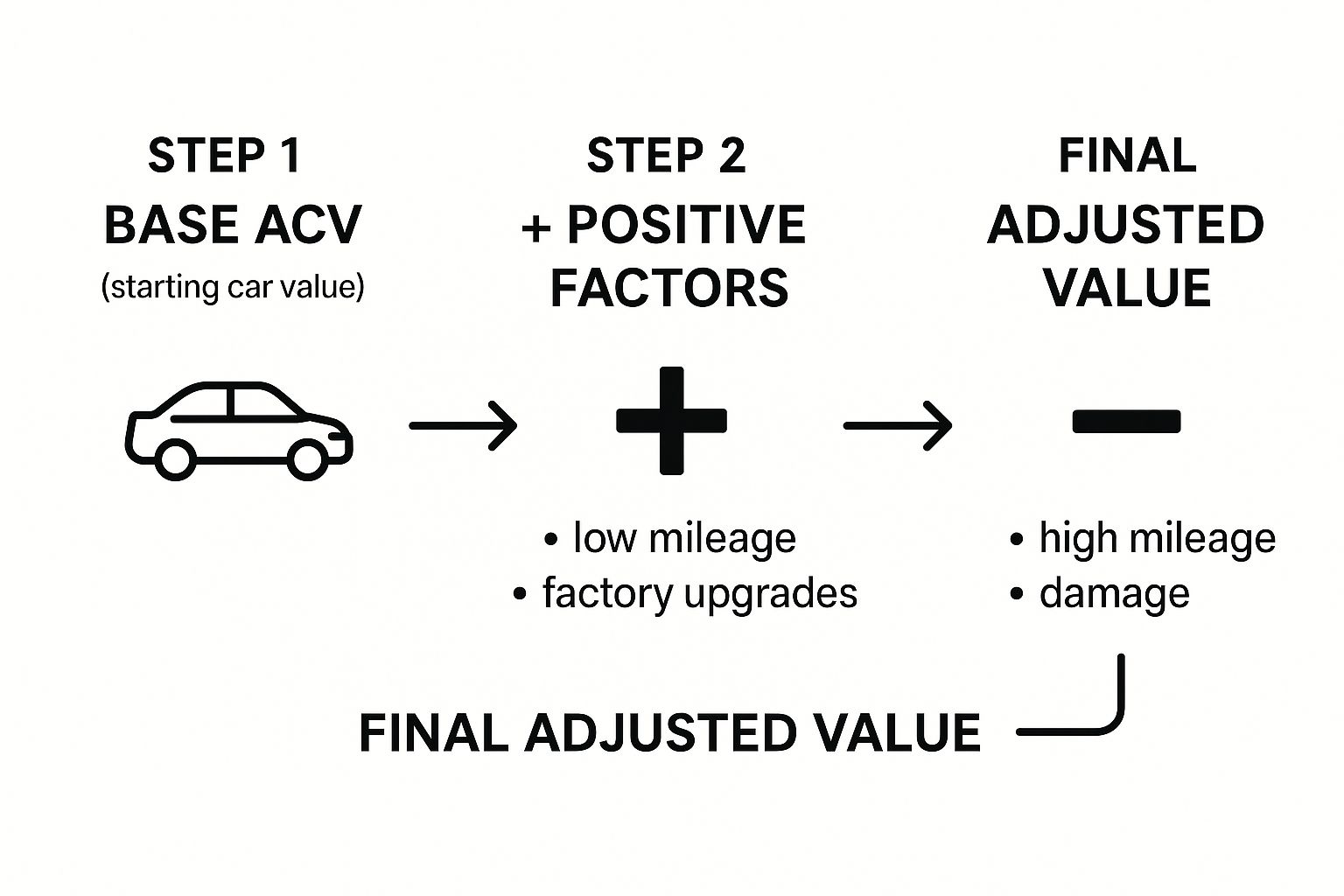

The Good, the Bad, and the Ugly: What Drives Your Car's Final Value

When an insurer calculates your totaled car's value, they aren't just looking up its make and model in a book. They're conducting a detailed audit where every little thing can push the final number up or down. Think of it like a report card for your car—from the shine on its paint to the miles on the odometer, every detail gets a grade.

Understanding these variables is your biggest advantage. It lets you see your car through the appraiser's eyes, anticipate their adjustments, and build a strong case for your car's true worth. Let's dig into the key elements that can swing the value of a totaled car one way or the other.

This infographic gives you a great visual of how an appraiser starts with a base value and then adds or subtracts based on the car's specific history and condition.

As you can see, the final settlement is almost never the sticker price. It’s a custom-tailored figure that reflects your car's unique life story.

The Upside: Factors That Increase Your Car's Value

Certain things make your car more desirable on the open market, and a good appraiser's report has to reflect that. If you have the paperwork to back these up, you’ve got a solid foundation for justifying a higher settlement.

Here are the big value-adders:

- Low Mileage: A car with fewer miles than the average for its age is always a winner. It immediately signals less wear and tear on the engine, transmission, and all the other expensive bits.

- Pristine Condition: This is all about the "curb appeal." A garage-kept car with flawless paint, a spotless interior, and no pre-existing dings or scratches will naturally fetch a higher price.

- Factory Upgrades: Those features added at the dealership—a sunroof, that premium sound system, leather seats, or an advanced tech package—add real, quantifiable value. A base model is worth far less than a fully loaded one.

- A+ Maintenance History: Can you prove the oil was changed every 5,000 miles on the dot? A thick stack of receipts from a reputable shop shows the car was cared for, boosting its reliability and, in turn, its value.

The key takeaway here is simple: provable, desirable features add real dollars to your settlement. The more documentation you have, the stronger your case will be.

The Downside: Factors That Decrease Your Car's Value

On the flip side, plenty of things can quickly chip away at your car’s ACV. Insurers are incredibly thorough when it comes to finding flaws that would have lowered its market price right before the accident.

Get ready for them to make deductions for things like:

- High Mileage: Just as low mileage helps, high mileage hurts. A vehicle with 150,000 miles is simply worth less than an identical one with only 50,000 miles. There’s no getting around it.

- Pre-Existing Damage: That cracked windshield you never fixed? The dent in the fender from a rogue shopping cart? Worn-out tires? All of these pre-existing cosmetic and mechanical issues will be noted and deducted from the final value.

- Prior Accident History: Even if it was fully and professionally repaired, a car with a previous accident on its record often carries a lower market value. This is called diminished value, and it will absolutely be factored into the ACV.

- Weird Modifications: You might have loved those aftermarket rims or that cannon-sized exhaust, but non-standard modifications can actually shrink the pool of potential buyers, which can lower the car’s overall market value.

To see how this plays out in the real world, let's compare two identical cars with very different histories.

Valuation Impact Comparison: Identical Make and Model

This table shows how two similar cars can end up with vastly different values based on their condition and history.

| Valuation Factor | Car A (Good Condition) | Car B (Poor Condition) | Impact on ACV |

|---|---|---|---|

| Mileage | 55,000 (Below Average) | 125,000 (Above Average) | Car B's value is significantly reduced due to high mileage and expected wear. |

| Condition | Excellent, no pre-existing damage | Fair, has dings, scratches, worn tires | Car B's ACV is lowered to account for reconditioning costs. |

| History | Clean, no accidents | One minor reported accident | Car B's value is reduced due to diminished value from its accident history. |

| Features | Sunroof, leather seats | Base model, cloth seats | Car A's factory upgrades add a premium to its final valuation. |

As you can see, even for the same make and model, the final ACV can differ by thousands of dollars based on these factors.

How Your Zip Code Impacts the Final Offer

Here’s a factor that catches many people by surprise: your location matters. A lot. The market value of a car can change dramatically depending on where you live because appraisers use local comparable sales to set the baseline.

For example, a rugged 4×4 truck is almost always more valuable in a snowy, rural area than it is in a dense city with perfect roads. On the other hand, a small, fuel-sipping hybrid might command a premium in a metro area known for high gas prices and tight parking. This regional adjustment isn't a trick; it's a standard and logical part of any accurate valuation.

How Insurance Companies Calculate Your Settlement Offer

When an insurance company declares your car a total loss, they don't just pull a number out of a hat. The reality is that determining the value of a totaled car is a highly data-driven process, relying on powerful third-party software and massive market databases. Their goal is to base the offer on real-world sales data, not just an educated guess.

While the system is designed to be objective, it’s not perfect. Knowing how the sausage gets made is the first step toward making sure you get a fair and accurate settlement for what your car was really worth just before the accident.

At its heart, the process is all about finding "comparables," or "comps." It’s a lot like how a real estate agent figures out the value of a house—they don’t guess. Instead, they look at what similar homes have recently sold for in the same neighborhood.

The Role of Third-Party Valuation Software

Most major insurance carriers don’t build their own valuation tools. They use specialized services from companies like CCC Intelligent Solutions (often known as CCC ONE) or Mitchell. Think of these platforms as giant data engines that are constantly scanning the used car market.

Here’s a quick rundown of how it usually works:

- Create a Vehicle Profile: The adjuster starts by plugging in your car’s key details—year, make, model, trim, mileage, and all its factory options.

- Scan the Market: The software then dives into its database, hunting for identical (or nearly identical) vehicles that have recently sold at dealerships in your local area.

- Establish a Baseline Value: It pulls together the sales data from these "comps" to generate a baseline market value for a vehicle just like yours.

- Make Condition Adjustments: Finally, the adjuster applies credits or deductions based on your car's pre-accident condition, mileage, and unique features to arrive at the final Actual Cash Value (ACV).

This automated method keeps things consistent, but it can also overlook the little things that make a big difference. The software might not give proper credit for a rare trim package or that expensive set of new tires you just bought. This is where you come in. You can learn more about the nuts and bolts in our guide to calculating a total loss vehicle's value.

Understanding the Total Loss Threshold

Before an insurer even begins calculating your car’s ACV, they have to officially determine that it is a total loss. This decision isn't arbitrary; it’s based on a state-specific rule called the Total Loss Threshold (TLT).

The TLT is a percentage. It’s the tipping point where the estimated cost of repairs plus the car's potential salvage value climbs above a certain percentage of its ACV. For instance, if your state has a 75% TLT, any car with damages adding up to more than 75% of its pre-accident value is automatically totaled.

This threshold isn't a point of negotiation; it's a legal standard set by state regulators. The main goal is to keep dangerously damaged and poorly repaired cars from getting back on the road.

This is where the bigger picture comes into play. For example, industry data showed the U.S. private auto physical damage loss ratio was 53.9% in Q2 2025. This number reflects what insurers pay out in claims compared to the premiums they collect. When that ratio climbs, it can subtly influence how they approach repair costs and total loss decisions. You can dive deeper into these insurance market dynamics to understand the pressures they face.

By realizing that your settlement offer is the product of a data-heavy system—one that hinges on market comps and is bound by state law—you’re in a much better position to review their valuation report. You can check their work, make sure their "comps" are truly comparable, and argue that every last positive detail about your vehicle has been counted.

Your Guide to Negotiating a Better Settlement

https://www.youtube.com/embed/QoLogihhzp8

When the insurance company sends over their settlement offer for your totaled car, it’s easy to think the conversation is over. But it’s not. That first number is just their opening bid. Insurers use automated systems to come up with a value, but these platforms often overlook the unique details and care you put into your vehicle.

The good news? The first offer is rarely the final one. Negotiating isn't about being confrontational; it’s about coming prepared. With the right documentation and a clear strategy, you can build a powerful case for the true value of a totaled car and secure the fair settlement you’re entitled to.

Step 1: Scrutinize the Valuation Report

Your first move is to ask the adjuster for a complete copy of their valuation report. This document is the playbook for their offer, and it’s where you’ll find the leverage you need to build a solid counteroffer. Don’t just give it a quick glance—you need to dissect it line by line.

Think of yourself as a detective looking for clues. Small errors can add up to a big difference in the final payout. Keep an eye out for these common mistakes:

- Incorrect Trim or Package: Did they list your car as the base model when you paid extra for the sport or luxury trim? This is a huge, and surprisingly common, oversight.

- Missing Factory Options: Check if they accounted for valuable add-ons like a premium sound system, a sunroof, leather seats, or advanced driver-assist features.

- Unfair Condition Rating: The report will grade your car’s pre-accident condition. If they’ve marked it as "average" when you kept it in "excellent" shape, that’s an immediate red flag that has unfairly dragged down the value.

- Poorly Chosen “Comps”: The comparable vehicles, or "comps," they use to justify their price are critical. Are they actually similar to your car in mileage, condition, and options? Or did they pick ones from a hundred miles away with more wear and tear?

Every discrepancy you find is a valid point for negotiation. This initial review is what lays the groundwork for a successful counteroffer.

Step 2: Build Your Case with Solid Evidence

Once you've poked holes in the insurer's report, it's time to build your own case with hard evidence. Your opinion of what your car was worth won't move the needle, but a folder full of proof will.

Start by digging up your car's records. You want to paint a clear picture of a well-maintained, valuable vehicle.

- Maintenance Records: Pull together every receipt you have for oil changes, new brakes, tire rotations, and scheduled maintenance. A thick service history is undeniable proof that your car was anything but neglected.

- Recent Upgrades: Did you put on a brand-new set of tires last year? A new battery a few months ago? Find those receipts. These are recent investments that add real, tangible value.

- Pre-Accident Photos: If you have photos of your car looking clean and pristine before the crash, they can be your best weapon against a low condition rating from the adjuster.

Next, it’s time to find your own comps. Hop on a few auto listing sites and search for cars for sale in your area that are a near-perfect match to yours—same make, model, year, trim, and mileage. Screenshot those listings, because they represent the real-world cost to replace your car today.

Step 3: Craft a Compelling Counteroffer

With all your evidence organized, you're ready to make your move. Draft a professional, fact-based email or letter to the adjuster. Now is not the time for emotion; stick to the facts and keep your tone business-like.

Start by politely acknowledging their offer, then pivot to laying out your case. Go point-by-point through the errors you found in their report and present your counter-evidence. For example: "Your report valued my vehicle as a base model. However, as the attached window sticker shows, it is the Limited trim, which includes the panoramic sunroof and leather interior."

Then, introduce the comparable listings you found, explaining that they provide a more accurate picture of the current local market value.

A well-reasoned, evidence-backed counteroffer isn’t a complaint—it’s a business proposal. You're simply showing the adjuster that their initial calculation was missing key information and that your number is a more accurate reflection of reality.

Step 4: Invoke the Appraisal Clause

What if you've presented a rock-solid case and the insurance company still won't offer a fair number? Don't give up. You have a powerful tool left: the appraisal clause.

This clause, buried in the fine print of most auto insurance policies, is your right to an independent valuation. You can find more details in our guide on how to negotiate your total loss settlement.

It works like this: you hire a certified, independent appraiser, and the insurance company hires their own. The two of them then negotiate a value. If they can’t reach an agreement, they bring in a neutral third appraiser (an "umpire") to cast the deciding vote. The final number is binding. This process takes the insurer’s biased software out of the picture and puts the decision in the hands of neutral experts, giving you your best shot at getting the true value for your car.

Answering Your Top Questions About Totaled Cars

Even after you get a settlement offer, the total loss process can feel a bit like a maze. It's completely normal to have a few questions still floating around. Getting those final details ironed out will help you close out the claim feeling confident you've been treated fairly.

Let's walk through some of the most common questions people have once their car has been declared a total loss. These answers should help you navigate the final steps and understand what your totaled car is really worth.

Can I Keep My Totaled Car?

Yes, you almost always have the option to keep your car. In most states, this is called "owner retention."

If you go this route, the insurance company will pay you the car's Actual Cash Value, but they'll first subtract its salvage value. That’s the amount they would have gotten by selling the wreck at a scrap auction.

Just be aware, your car will be issued a "salvage title." This new title can make it tougher to insure and sell down the road. Still, it can be a great choice if the car has a lot of sentimental value, or if the damage is mostly cosmetic and it’s still perfectly safe to drive.

What Happens If I Owe Money on My Car Loan?

If you're still making payments on the car, the insurance settlement has to go to your lender first. The check will typically be made out to both you and the bank or credit union that holds the loan.

If the settlement amount is less than what you still owe, you're on the hook for the difference. This is exactly the situation that Guaranteed Asset Protection (GAP) insurance is built for.

Does the Settlement Include Taxes and Fees?

This is a big one, and the answer comes down to your policy and, more importantly, your state's laws. Many states require insurers to include sales tax and title transfer fees in the settlement to truly make you "whole" again.

Always check the settlement breakdown to see if these costs are included. If they aren't, and your state law says they should be, you've just found a powerful and legitimate reason to negotiate for a better offer.

If you're staring at a lowball settlement offer for your totaled car, don't just accept it. At Total Loss Northwest, our certified independent appraisers work to get you the true market value you deserve. We build detailed, evidence-based reports to make sure you get a fair shake. Find out more about how we help clients get fair settlements.