When you hear the term "totalled car," it's easy to think it's worthless. But that's not the case at all. The value of a totalled car isn't its value as a pile of scrap metal; it’s the Actual Cash Value (ACV)—what your vehicle was worth on the open market a moment before the accident.

My Car Was Totalled What Happens Now

Hearing an adjuster declare your car a "total loss" is jarring. It’s a gut-punch moment. But it's important to understand that this isn't about your car being a complete write-off; it's a financial calculation your insurance company has to make. The decision is triggered when the estimated cost to repair your vehicle, plus its remaining salvage value, crosses a specific percentage of its pre-accident worth.

Think of it this way: if a home's foundation is so damaged that fixing it would cost more than the house is even worth, it makes more sense to start over. Insurers apply that same cold, hard logic to cars.

The Total Loss Threshold

Every state has its own rule for this, called a Total Loss Threshold (TLT). This is a set percentage that determines when a car must be declared a total loss. Typically, this number falls somewhere between 70% and 100% of the car's ACV.

Here’s a practical example. Let's say your car's ACV is calculated at $15,000, and you live in a state with a 75% TLT. If the repair estimate comes back at $11,250 or more, your insurer is required to total the vehicle. It’s a purely economic decision designed to keep them from sinking more money into a repair than the car is actually worth.

What to Expect During the Claims Process

Once the "total loss" call is made, the claims process kicks into high gear. It can feel like a whirlwind, but it follows a pretty standard path. Here’s a rough idea of what to expect:

- Initial Assessment: An adjuster will inspect your car to estimate the repair costs.

- ACV Calculation: The insurance company will then run a report, usually using special valuation software, to figure out your car's pre-accident market value.

- Settlement Offer: You’ll get an official settlement offer based on that ACV, minus your policy's deductible.

- Negotiation: This is the important part. You have every right to review their valuation report and negotiate if you feel their offer is too low.

The most important thing to remember is that the insurance company’s first offer is just that—an offer. You don't have to accept it, especially if you have evidence showing the value of your totalled car was higher than they claim.

Knowing these steps ahead of time can make a huge difference in getting a fair outcome. For a deeper dive into this, our guide on how much your totalled car is worth has even more detail. Next, we'll break down exactly how that ACV number is calculated and what you can do to make sure it’s accurate.

How Insurers Calculate Actual Cash Value

Your entire settlement comes down to one number: the Actual Cash Value (ACV). This is the figure the insurance company believes your vehicle was worth the second before the accident. It's the foundation of their entire settlement offer.

A lot of people think ACV is what they paid for the car, or what a new one costs. It’s neither. Think of it as a snapshot of your car's fair market value, factoring in all the miles and wear-and-tear it's picked up over the years.

The Tools Behind the Valuation

So, where does this number come from? Insurers don’t just guess. They subscribe to powerful third-party valuation services to determine the value of a totalled car. The two biggest names in the game you’ll likely see on your report are CCC ONE and Mitchell.

These aren't just fancy versions of Kelley Blue Book. They are sophisticated platforms that crunch massive amounts of real-world sales data from your specific area.

- Local Market Analysis: The software zeroes in on what cars like yours have actually sold for recently, right in your local market. A Honda CR-V in Portland, Oregon, will have a different value than the same CR-V in Phoenix, Arizona, simply because of regional demand and market conditions.

- Finding "Comps": It identifies recently sold vehicles—called "comparables" or "comps"—that are the same make, model, and year as yours.

- Adjusting for Details: From there, the system fine-tunes the value of those comps to match your vehicle's exact mileage, features, and overall condition.

At the end of the day, the insurer's software is trying to answer a single question: "What would a reasonable person have paid for this specific car, in its pre-accident condition, in this town, yesterday?" The report they give you is their attempt to justify that number.

Deconstructing the ACV Report

When that valuation report lands in your inbox, it can look intimidating. But once you know what you're looking at, it's really just a simple formula of additions and subtractions.

The final ACV starts with a base value and then gets adjusted up or down based on the details of your specific car.

- Base Value: This is the starting point, calculated from the average sale price of comparable cars in your area.

- Mileage Adjustments: Did you have super low miles for the car's age? You should see a positive adjustment, or a credit. If your mileage was higher than average, you'll see a negative adjustment, or a debit.

- Options and Packages: The report must list all the factory-installed features your car had. A sunroof, a premium audio system, a tow package—each of these adds value.

- Condition Adjustments: This is the most subjective—and often contentious—part. The adjuster will rate your vehicle's pre-accident condition. If your car was immaculate, it should get a credit. If it had some dings, faded paint, or worn seats, expect a debit.

The final number after all these adjustments becomes the basis for their settlement offer. Because ACV is so tied to what's happening in the market, it’s crucial to have a firm grasp of what constitutes fair value. To dive deeper, you can learn more about how fair market value is determined in our detailed guide. Arming yourself with this knowledge is the single best thing you can do before you start negotiating.

Key Factors That Raise or Lower Your Payout

When an insurance company totals your car, the number they come up with isn't just pulled out of a hat. It's a detailed calculation, and that first offer for the Actual Cash Value (ACV) is really just a starting point. The nitty-gritty details of your specific vehicle are what can dramatically move that number up or down.

Imagine two identical 2019 Honda Civics. One is a garage-kept gem with 40,000 miles and a flawless interior. The other has seen 110,000 hard-driven miles, with dings on the doors and some wear on the seats. They’re the same make and model, but their pre-accident values are obviously miles apart. The insurance valuation has to reflect that reality.

The Devil Is in the Details

The adjuster's report will hit the big points, but it's the smaller details that often add up to a significant difference in your final check. This is why you have to comb through their valuation report—your goal is to make sure every last detail is accurate.

Here are the main things that will adjust your car's base value:

- Mileage: This is a big one. A car with surprisingly low mileage for its age gets a nice bump in value because it has less wear and tear. On the flip side, high mileage will knock the value down.

- Vehicle Condition: This is where things get a bit subjective. The adjuster will rate your car’s interior, exterior, and mechanical shape. Any pre-existing damage, like old dents, scratches, or worn-out tires, will lower the value.

- Geographic Location: A car's worth changes depending on where you live. A 4×4 truck, for example, is going to be in higher demand in a snowy state like Washington than in sunny Florida. The ACV is based on your local market.

- Factory Upgrades and Trim Level: A base model simply isn't worth as much as the fully loaded version. Things like a sunroof, premium sound system, leather seats, and high-tech safety features all need to be added to the value.

Your goal is to prove your car was an above-average example of its kind. Every positive detail you can document helps build a case for a higher payout, pushing back against a lowball offer.

How Key Factors Impact Your Car's Totalled Value

To see how these attributes play out, let's look at how they can either boost or reduce your car's final value.

| Factor | Positive Impact (Increases Value) | Negative Impact (Decreases Value) |

|---|---|---|

| Mileage | Significantly lower than average for the year. | Higher than average for the year. |

| Condition | Pristine paint, spotless interior, no prior damage. | Scratches, dents, rust, worn tires, or interior stains. |

| Trim/Options | High-end trim (e.g., Limited, Platinum) with premium features. | Base model with no factory add-ons. |

| Location | In-demand vehicle type for the local climate or terrain. | Common vehicle with low local market demand. |

| Maintenance | Complete service records showing regular, documented upkeep. | Inconsistent service history or evidence of neglect. |

Ultimately, a well-documented, well-cared-for vehicle will always stand a better chance of getting a higher valuation.

Proving Your Car’s Superior Condition

Documentation is your best friend in this fight. Beyond the obvious things like mileage, the car's overall condition before the accident is huge. This is where proof of consistent car maintenance can really help your case and influence the final payout.

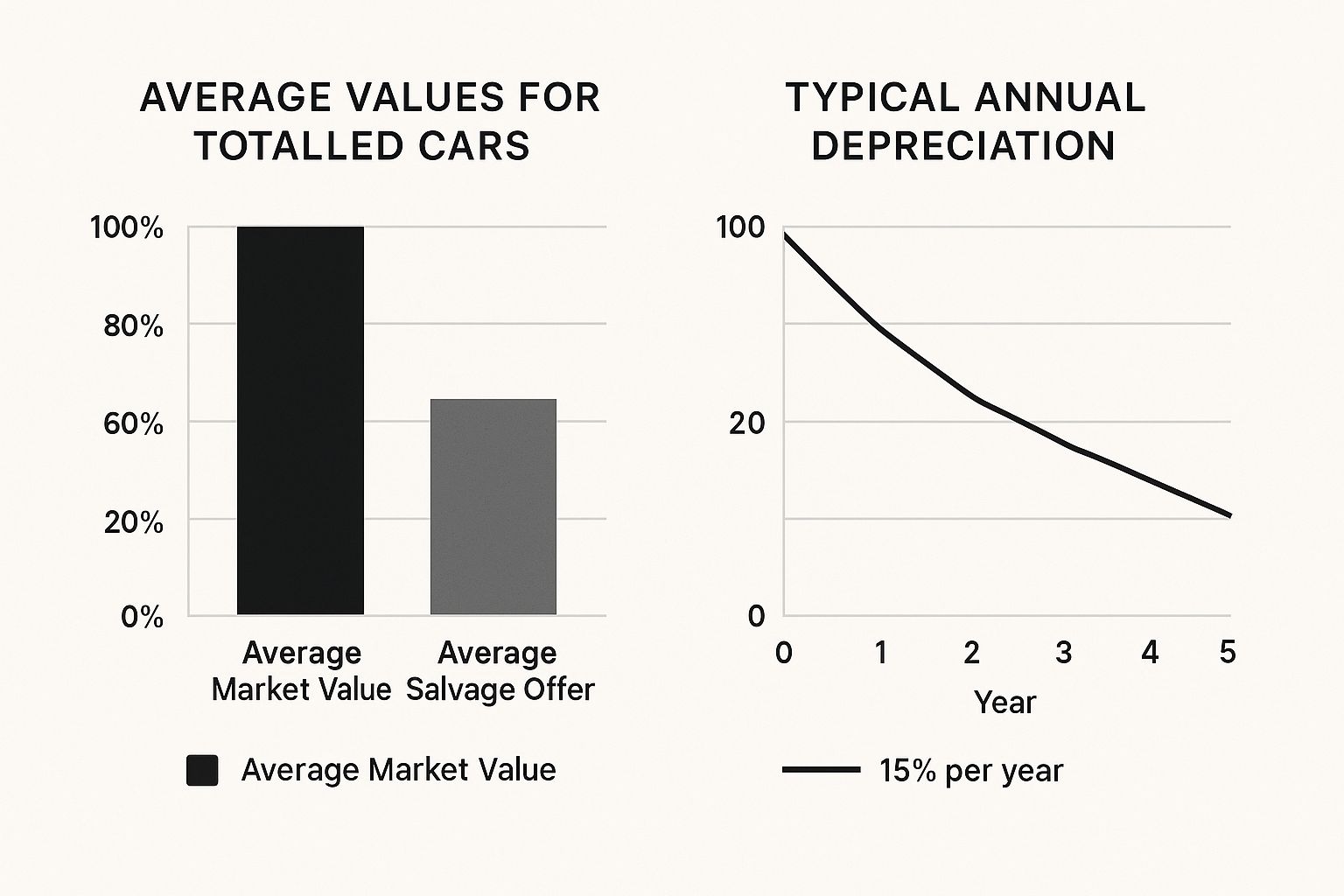

As you can see, there's a huge gap between what a car is actually worth on the market and what you might get from a salvage yard. This is precisely why fighting for a fair and accurate ACV is so important—it’s the key to getting a settlement that truly reflects what you lost.

Why Are So Many Cars Being Totalled These Days?

If you feel like you're hearing about more cars being "totalled" after an accident, you're not wrong. The reason is a mix of modern automotive evolution and plain old economics. A minor fender-bender that was a simple fix ten years ago can now set off a chain reaction of incredibly expensive and complex repairs.

This shift makes it more important than ever to understand the value of a totalled car. Your insurer is running the numbers, and with repair costs going through the roof, it doesn't take much damage for a car to be declared a total loss.

The Sky-High Cost of Modern Tech

Think of your new car as a computer on wheels, because that's what it is. It's loaded with amazing technology—adaptive cruise control sensors, lane-assist cameras, bumper-mounted ultrasonic sensors—all designed to keep you safe. The downside? When these systems get damaged, they cost a fortune to fix.

What used to be a simple bumper replacement is now a whole different ballgame. The job now often involves:

- Recalibrating sensitive sensors for things like automatic emergency braking and lane-keeping systems.

- Replacing delicate cameras and all the wiring that's woven into the body panels.

- Working with specialized materials like aluminum or high-strength steel, which demand specific tools and highly trained technicians.

Every single one of these steps piles on more labor and parts costs. This explosion in repair expenses is a huge reason why we're seeing more and more total loss claims.

Pricey Vehicles and Shifting Market Tastes

Another piece of the puzzle is what we're choosing to drive. Trucks and SUVs are more popular than ever, and these bigger, more expensive vehicles naturally come with higher repair bills and, consequently, bigger insurance payouts when they're totalled.

The sheer complexity of modern cars has completely rewritten the insurance playbook. As vehicles get more advanced with new sensors and safety features, the cost to repair them climbs, making it far more likely that even moderate damage will result in a total loss.

It's a significant trend. In the United States alone, industry data reveals that roughly 1.5 million vehicles are declared total losses every year. As you can dig into with these key industry stats on Autokunbo.com, this isn't a small number—it's a massive slice of all auto insurance claims.

We're in a perfect storm of advanced tech meeting higher vehicle prices. The line between a "fixable" car and a "totalled" one has become incredibly thin. What looks like a straightforward repair to you might be a clear financial write-off for your insurance company, which is why getting a fair valuation is absolutely critical.

How New Vehicle Trends Affect Your Settlement

The kind of car you drive plays a huge role in what it's worth if it gets totalled. The cars on the road today are a world away from what we saw just ten years ago. We're in an era of bigger, pricier, and more technologically packed vehicles, and these changes have a direct line to how your insurance company figures out your settlement check.

One of the biggest forces at play is our love for trucks and SUVs. It’s not just a feeling; the numbers back it up.

Take a look at the sales charts. Models like the Ford F-Series, Chevy Silverado, and Ram pickups are dominating, with each selling well over 300,000 units in just the first half of 2025. These aren't cheap vehicles. The Ford F-Series, America's best-seller, starts around $35,000, and high-end versions can easily top $70,000. You can see these automotive sales trends for yourself over at MarkLines.com.

Naturally, since these vehicles cost more to buy new, their Actual Cash Value (ACV) starts at a much higher point. That often leads to a bigger settlement when one is declared a total loss.

The Electric Vehicle Complication

Then you have electric vehicles, or EVs, which throw a real curveball into the total loss calculation. All that amazing technology that makes them so popular also makes them incredibly sensitive to being written off after what looks like a minor fender-bender. It all boils down to one single, mind-bogglingly expensive part: the battery.

An EV’s battery isn't just a component; it's the heart of the car and its most valuable asset, frequently costing tens of thousands of dollars. It’s also built right into the vehicle's frame.

A collision that barely seems to scratch the surface can damage the battery's protective housing. If that happens, the entire pack is considered compromised, and the cost to replace it is so astronomical that the insurer will almost always call it a total loss.

What would have been a straightforward repair on a gas-powered car becomes a write-off for an EV, all because of that battery.

Why This Matters for Your Settlement

So, why should you care about all these market trends? Because they directly impact your wallet. If you're driving a popular truck, a fancy SUV, or an EV, your settlement negotiation is going to be a different ballgame than if you had an older, basic sedan.

Your vehicle's higher starting value means more money is at stake. It's on you to make sure your insurer's offer truly reflects what your vehicle was worth right before the crash. With EVs, you have to be extra vigilant, making sure the adjuster isn't lowballing the value just because its high-tech parts are considered a higher risk.

Getting a Fairer Payout: Your Negotiation Playbook

When an insurer tells you your car is totalled and slides an offer across the table, it can feel like a done deal. But here's something they don't always advertise: that first number is almost always just a starting point for negotiation. You absolutely have the right to push back and argue for a payout that actually matches what your car was worth moments before the accident.

Think of it less as a confrontation and more as a business discussion. Your job is to show the adjuster, with proof, why their valuation falls short. The goal isn't just to say "I want more money"; it's to build an airtight case that their report missed the mark on your vehicle's real-world market value.

Build Your Case with Solid Evidence

Before you even think about calling the adjuster, it's time to do some homework. A successful negotiation is won with facts, not feelings. Your mission is to gather undeniable proof that your car is worth more than they're offering.

- Find "Comps" in Your Local Market: Jump onto local online car listings. Look for the exact same make, model, year, and trim as your car. You're searching for vehicles in similar condition with similar mileage. Screenshot these listings—they are powerful proof of what it would cost to actually replace your car in your area.

- Dig Up Your Service Records: Did you just put on a brand-new set of tires? Replace the battery last winter? Have a major service done recently? Find those receipts. This documentation proves your car was well-maintained, which often justifies a higher condition rating than the one the adjuster initially assigned.

The secret to a successful negotiation isn't about being confrontational. It's about presenting a clear, evidence-backed case that shows your car was an above-average example of its kind and, because of that, is worth more than the insurance company's initial offer.

Your Secret Weapon: The Appraisal Clause

What if you've presented all your research and the adjuster still won't move their number? It's time to check your policy for a powerful but often overlooked tool: the appraisal clause.

This provision is essentially an escape hatch from a valuation stalemate. It allows you to hire your own independent, certified appraiser to determine the car's value. The insurance company hires one, too. The two appraisers then try to agree on a number. If they can't, they bring in a neutral third appraiser (called an "umpire") to cast the deciding vote, which is typically binding for both sides.

Yes, there's a cost involved, but it takes the decision out of the hands of the insurer's biased software. Understanding how to effectively negotiate a total loss settlement means knowing when to use every tool you have, and this clause can be the key to unlocking a truly fair payout.

Got Questions? We've Got Answers

When your car is declared a total loss, it’s natural for your head to be swimming with questions. It’s a stressful situation, and the process can feel confusing. Let's tackle some of the most common concerns people have.

Can I Keep My Car After It's Totalled?

Believe it or not, yes, you often can. This option is called "retaining salvage," and it’s available in most states.

Here’s how it works: the insurance company pays you the car's actual cash value, but first, they subtract what they would have gotten for it at a salvage auction. You get the car and a check for the difference.

Just be aware, the car will get a salvage title. This makes it tough to insure or sell down the road, so this path really only makes sense if you're a skilled mechanic planning to fix it yourself or if you want to sell it for parts.

What Happens If I Owe More on My Loan Than the Car is Worth?

This is a tough spot to be in, and unfortunately, it's pretty common. It’s often called being "upside down" or "underwater" on your loan. Your insurance settlement is based only on the car's value right before the crash, not what you owe the bank.

If the settlement check isn't enough to pay off your loan, you're still on the hook for the remaining balance.

This is exactly why GAP insurance is so important. If you have a Guaranteed Asset Protection (GAP) policy, it's designed to cover that exact "gap" between the insurance payout and what you still owe. It can be a real financial lifesaver.

How Long Does This Whole Settlement Process Take?

It really depends. A straightforward claim might wrap up in just a few days, but more often, you’re looking at a couple of weeks.

Things can get delayed if your vehicle is unique and hard to value, if you decide to dispute the insurer's first offer, or simply if the claims department is backed up. The best you can do is provide all your documents quickly and follow up with your adjuster regularly. A little patience and persistence go a long way.

If you're staring at a settlement offer that just doesn't seem right, you don't have to accept it. Total Loss Northwest specializes in helping people get what they're truly owed. Our certified appraisers use the Appraisal Clause in your policy to challenge lowball offers and fight for a fair market value. Don't settle for less—visit Total Loss Northwest to get an expert on your side.